Styrene Butadiene Styrene Rubber Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

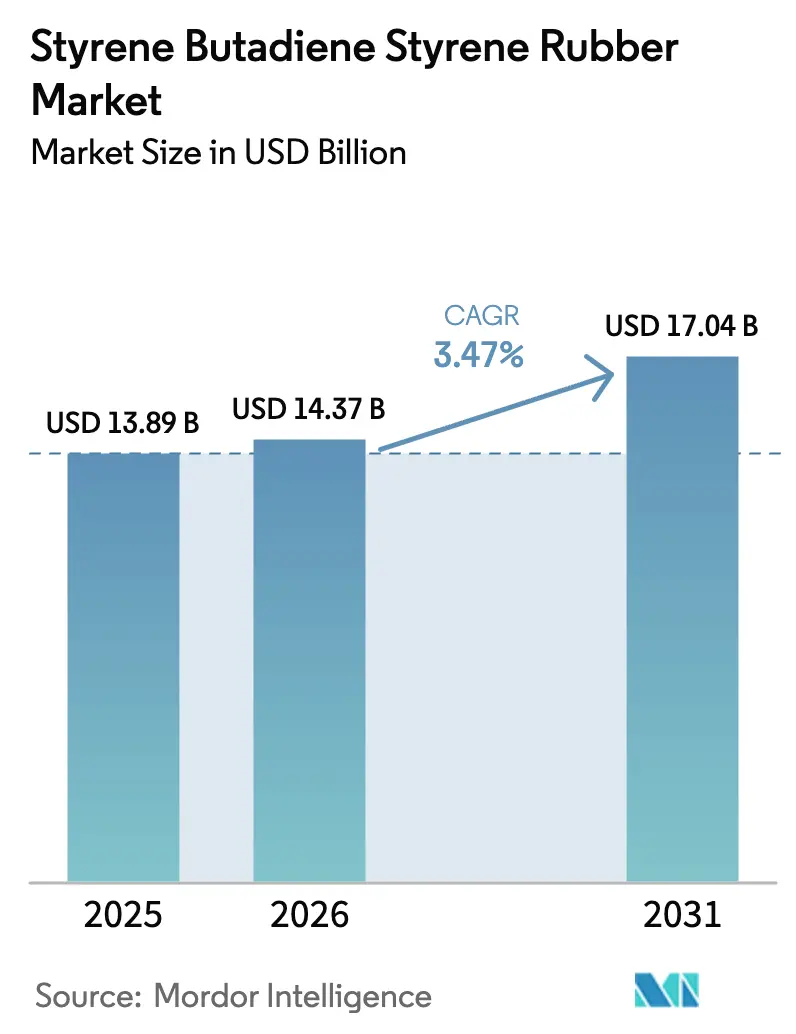

| Market Size (2026) | USD 14.37 Billion |

| Market Size (2031) | USD 17.04 Billion |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

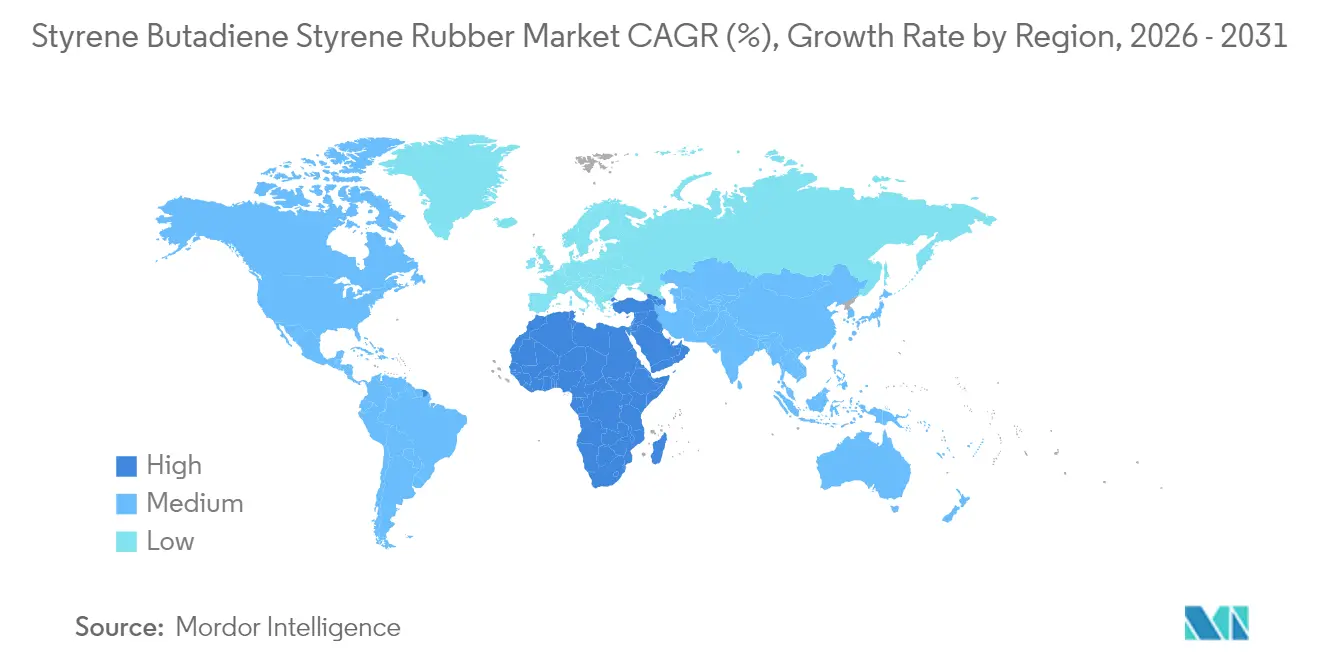

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Styrene Butadiene Styrene Rubber Market Analysis by Mordor Intelligence

The Styrene Butadiene Styrene Rubber market size is expected to grow from USD 13.89 billion in 2025 to USD 14.37 billion in 2026 and is forecast to reach USD 17.04 billion by 2031 at 3.47% CAGR over 2026-2031. Persistent infrastructure upgrades in emerging economies, along with ongoing demand for high-performance footwear, compounds, and the irreplaceable balance of elastomeric behavior with thermoplastic processability, continue to drive consumption. Integrated supply chains in Asia-Pacific, where upstream feedstocks connect seamlessly with downstream processing clusters, create cost advantages that support resilient volume growth even as the industry matures. Product differentiation now centers on purity, bio-attributed content, and application-specific performance improvements more than on bulk price positioning, a shift reinforced by tightening sustainability mandates. Companies that secure reliable styrene and butadiene streams while reducing the carbon intensity of production are well-positioned to protect margins against raw material volatility.

Key Report Takeaways

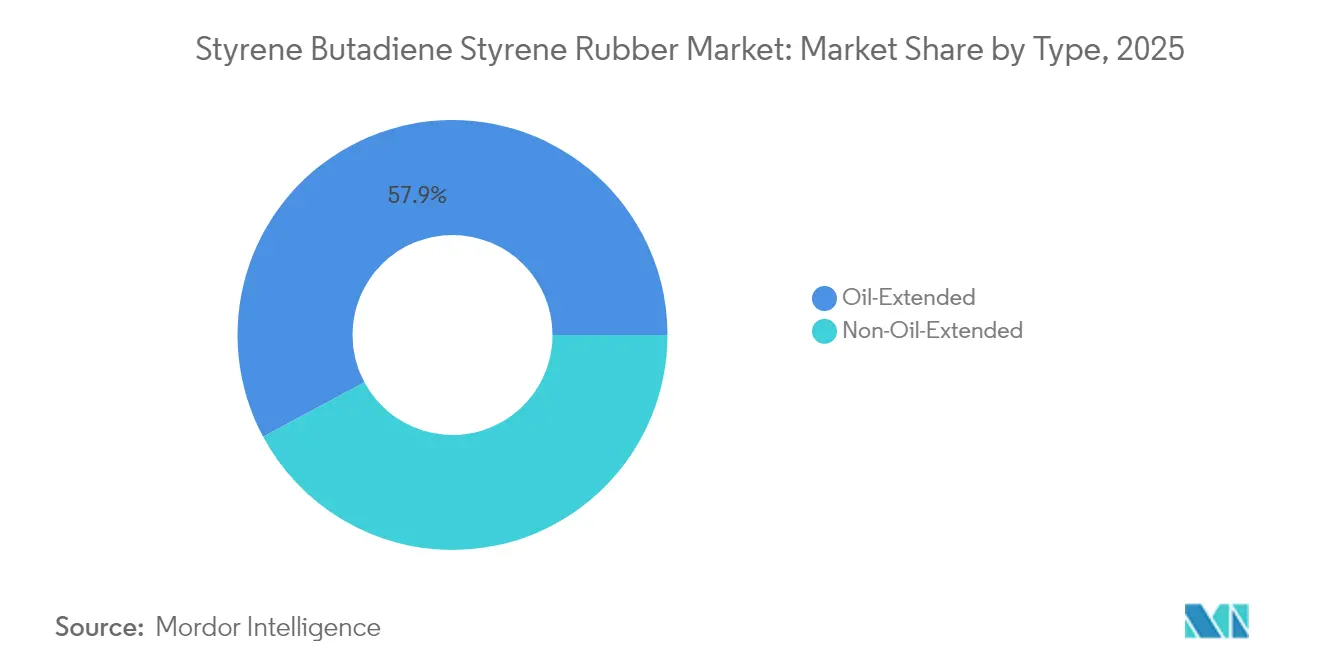

- By type, oil-extended grades accounted for 57.85% of the Styrene Butadiene Styrene Rubber market share in 2025. However, the market share of the non-oil-extended type is expected to increase with the fastest CAGR of 4.05% during the forecast period.

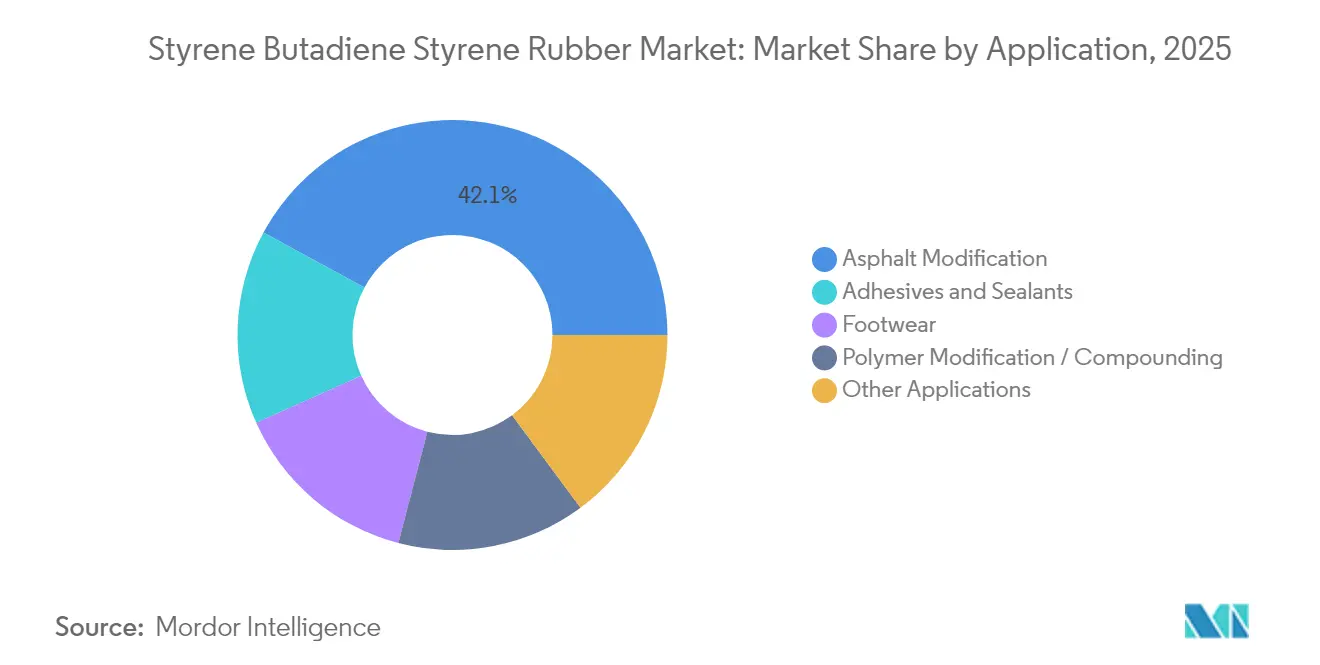

- By application, asphalt modification commanded a 42.10% share of the Styrene Butadiene Styrene Rubber market size in 2025, while adhesives and sealants are projected to advance at a 4.86% CAGR through 2031.

- By geography, the Asia-Pacific region held a 45.75% revenue share in 2025; the Middle East and Africa region is forecast to expand at a 3.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Styrene Butadiene Styrene Rubber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of footwear manufacturing hubs | +0.8% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Rising SBS-modified bitumen use in road and roofing projects | +1.2% | Global, with concentration in MEA and APAC | Long term (≥ 4 years) |

| Accelerating demand from hot-melt adhesives and sealants | +0.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Thermoplastic elastomer substitution for recyclable consumer goods | +0.6% | EU and North America, regulatory-driven | Medium term (2-4 years) |

| 3-D printing adoption for flexible and transparent parts | +0.4% | North America & EU, technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Footwear Manufacturing Hubs

Vietnam, China, and Indonesia now form a contiguous manufacturing corridor that demands specialized SBS grades engineered for midsoles, outsoles, and cushioning inserts. High-elastic variants deliver energy return properties sought by performance footwear brands while maintaining anti-slip coefficients critical for workplace and athletic safety. Sustainability targets from global shoe brands are spurring pilot orders for bio-attributed SBS, and SCG Chemicals’ USD 700 million ethane upgrade at its LSP Vietnam complex underlines the priority of monomer self-sufficiency for regional sole compounders[1]SCG Chemicals, “SCG invests USD 700 million in LSP ethane upgrade,” scgchemicals.com. Clustered production also shortens lead times, enabling just-in-time inventory models that lower working capital for finished-goods assemblers.

Rising SBS-Modified Bitumen Use in Road and Roofing Projects

Government-funded highway expansions and urban roofing retrofits specify SBS-modified binders for resilience against rutting at 60°C and cracking at -20°C. Rheological testing confirms service-life extensions of up to 40% versus conventional asphalt, offsetting the higher initial polymer cost. National infrastructure plans in Saudi Arabia and India require performance-grade asphalt with polymer modification, positioning SBS at the top of bidder specifications for both new lane construction and resurfacing programs.

Accelerating Demand from Hot-Melt Adhesives and Sealants

Packaging converters are transitioning from solvent-borne systems to SBS-based hot melts, which are processed at 150-170°C, thereby reducing cycle times and minimizing VOC emissions. Formulators blend 15-25% SBS with hydrogenated hydrocarbon resins to achieve pressure-sensitive tack that retains peel strength down to -40°C for automotive wire harness tapes. Hygiene product makers specify medical-grade SBS for diaper fastening systems, valuing its skin-friendly rebound and odor neutrality.

Thermoplastic Elastomer Substitution for Recyclable Consumer Goods

European extended producer responsibility laws require designs that tolerate multiple melt-recycle loops without significant property loss. Non-oil-extended SBS maintains tensile strength above 18 MPa even after two reprocessing cycles, supporting circular packaging initiatives. PLAYMOBIL’s migration of its toddler line to plant-based styrenics with SBS content illustrates how mass-balance certification de-risks brand exposure to future bans[2]INEOS Styrolution, “INEOS Styrolution to permanently close Sarnia styrene plant,” ineos-styrolution.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High feedstock (styrene, butadiene) price volatility | -1.1% | Global, acute in regions with limited integration | Short term (≤ 2 years) |

| Competition from hydrogenated SEBS and other advanced TPEs | -0.7% | North America & EU, premium applications | Medium term (2-4 years) |

| Tightening VOC / environmental regulations on styrenics | -0.5% | EU and California, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Feedstock Price Volatility

The permanent shutdown of INEOS Styrolution’s 430 kt styrene unit in Sarnia constrains North American monomer supply and lifts spot prices, prompting smaller SBS formulators to negotiate short-term imports or pay premiums for domestic volumes. Kraton raised global SBS list prices in April 2025 to defend margin against styrene spikes, highlighting the 31% cost-of-goods exposure to raw materials. Parallel expansions in S-SBR tire elastomers siphon butadiene from SBS producers, further tightening balances.

Competition from Hydrogenated SEBS and Other Advanced TPEs

Styrene-Ethylene-Butylene-Styrene (SEBS) copolymers, with superior UV resistance, thermal stability, and weatherability, are surpassing traditional SBS in outdoor and automotive applications, where durability justifies higher costs. The hydrogenation process enhances SEBS's performance under UV exposure and high temperatures, making it ideal for applications that require a service life of over a decade. Propylene-based elastomers (PBEs), developed using advanced metallocene catalysts, are emerging as strong competitors due to their recyclability and potential for bio-based feedstocks. Commercial PBE grades, such as ExxonMobil's Vistamaxx, Dow's Versify, and Mitsui's Tafmer, offer elongation at break exceeding 1,700% and elastic recovery rates of 80-94%, rivaling SBS.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Oil-Extended Dominance Faces Non-Oil-Extended Growth

Oil-extended grades continued to command a 57.85% volume share in 2025, sustained by asphalt and footwear compounders who appreciate the melt-viscosity reduction that can be achieved at loadings of up to 25% process oil. This share reflects economic optimization where tensile retention above 12 MPa satisfies application thresholds, and processing windows widen for high-throughput extrusion. Non-oil-extended SBS delivers superior clarity and chemical resistance, positioning it for applications such as medical plugs, automotive vent gaskets, and electronics housings that require passing stringent VOC benchmarks. Rising demand lifts non-oil-extended consumption at a 4.05% CAGR, outpacing overall styrene butadiene styrene market growth.

Lower-viscosity oil-extended grades simplify hot-melt adhesive coating at 180 m/min for packaging lines, while non-oil-extended variants are suitable for injection-molded soft-touch grips that require dimensional stability. Bio-based process oils offer a hybrid approach that retains processing advantages while enhancing sustainability scores, potentially shifting some buyers back toward oil-plasticized offerings as commercial volumes increase.

By Application: Asphalt Modification Leads While Adhesives Accelerate

Asphalt modification’s 42.10% share in 2025 indicates that the expansion of the styrene butadiene styrene market size is still primarily driven by road surfacing and roofing systems. National highway agencies specify SBS loadings of 3–7% to achieve rut depth reductions and crack resistance, which can lengthen pavement life by up to 40%. Life-cycle cost analyses validate the SBS premium when traffic volumes exceed 10,000 vehicles per day.

Adhesives and sealants post the fastest 4.86% CAGR, reflecting a pivot to high-value, low-VOC bonding solutions for automotive lightweighting and recyclable packaging. Formulators exploit SBS tack and thermofusibility to create one-component systems, eliminating the need for multi-polymer blends. Footwear compounds remain a stable volume outlet, and polymer modification continues to serve as a niche enhancer for rigid styrenics, where added impact resistance offsets minor stiffness losses. Emerging 3-D-printing filaments and transparent medical tubing provide incremental but higher-margin tonnage.

Geography Analysis

The Asia-Pacific region held 45.75% of 2025 revenue and remains the anchor for the styrene butadiene styrene market due to integrated petrochemicals in China and ASEAN manufacturing corridors. Footwear exports from Vietnam increased by 11% in 2024, directly boosting SBS sole-compound consumption. Government road programs in India and Indonesia also specify SBS-modified bitumen for climate resilience, supporting steady regional drawdown.

North America’s refinery rationalization reduces domestic styrene output, and the Sarnia closure shifts the region toward import dependence for commodity SBS, even as elevated automotive and construction standards sustain demand for premium grades with low VOC signatures. Producers leverage application development services to protect their share against imported material.

Europe shows mature volume yet steady uptake for recyclable consumer goods, where SBS’s thermoplastic recoverability aligns with circular-economy directives. Stringent REACH protocols are pushing formulators toward low-styrene-residual and bioattributed variants.

The Middle East and Africa’s 3.75% CAGR through 2031 is driven by sovereign infrastructure megaprojects and the region’s advantage in feedstock-rich petrochemical parks that can backward integrate SBS. South America relies on macroeconomic recovery; Brazil’s uptick in automobile production supports adhesives and interior trim applications, despite limited local SBS resin capacity.

Competitive Landscape

The Styrene-Butadiene-Styrene Rubber market is moderately concentrated, placing vertically integrated majors, such as LG Chem, Kumho Petrochemical, and INEOS Styrolution, at the cost-curve bottom due to their ownership of styrene and butadiene streams. Producers vie to certify ISCC mass-balance SBS and develop bio-feed pathways that enable converters to meet their Scope 3 emission targets. R&D budgets target easy-process oil-extended grades with lower VOC emissions and medical-compliant non-oil-extended products for wearable devices. Mergers, joint ventures, and feedstock-swap contracts align with the need for scale to weather feedstock volatility.

Styrene Butadiene Styrene Rubber Industry Leaders

LG Chem

LCY

Kumho Petrochemical Co., Ltd.

Kraton Corporation

Dynasol Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kraton Corporation announced a general price increase in North America applicable to the SBS, SIS, and HSBC product lines. The company is implementing these price increases following a thorough review of the impact of recently enacted tariffs and associated cost increases.

- April 2023: Kraton Corporation, recognized for its sustainable production of specialty polymers and high-value biobased products, unveiled plans to enhance its supply capability for styrene-butadiene-styrene block copolymers (SBS) at its Belpre, Ohio, facility.

Global Styrene Butadiene Styrene Rubber Market Report Scope

Styrene Butadiene Styrene Rubber is created by polymerizing styrene and butadiene in an organic solvent. It is utilized as an asphalt modifier, waterproof sheet, adhesive, compounding, and plastic modifier.

The Styrene Butadiene Styrene Rubber market is segmented by type, application, and geography. By type, the market is segmented into oil extended and non-oil extended. By application, the market is segmented into footwear, asphalt modification, polymer modification, adhesives and sealants, and other applications. The report also offers market size and forecasts for 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Oil-Extended |

| Non-Oil-Extended |

| Footwear |

| Asphalt Modification |

| Polymer Modification / Compounding |

| Adhesives and Sealants |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Type | Oil-Extended | |

| Non-Oil-Extended | ||

| By Application | Footwear | |

| Asphalt Modification | ||

| Polymer Modification / Compounding | ||

| Adhesives and Sealants | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the styrene butadiene styrene market in 2031?

It is forecast to reach USD 17.04 billion by 2031 on the back of a 3.47% CAGR.

Which application is expanding fastest for SBS through 2031?

Adhesives and sealants, driven by automotive lightweighting and packaging, is growing at a 4.86% CAGR.

Why does Asia-Pacific dominate global SBS demand?

The region concentrates footwear production, asphalt projects, and integrated petrochemical supply chains that together account for 45.75% of 2025 revenue.

How are sustainability goals influencing SBS product development?

Producers are launching bio-attributed and ISCC-certified grades to meet circular-economy mandates while retaining thermoplastic processing benefits.

What key factor negatively impacts SBS margins today?

Volatility in styrene and butadiene feedstock prices can cut operating margins, especially for producers without vertical integration or long-term supply contracts.

Page last updated on: