Structural Steel Fabrication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 162.45 Billion |

| Market Size (2031) | USD 200.30 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Structural Steel Fabrication Market Analysis by Mordor Intelligence

The Structural Steel Fabrication Market size is expected to grow from USD 150.20 billion in 2025 to USD 162.45 billion in 2026 and is forecast to reach USD 200.30 billion by 2031 at 4.28% CAGR over 2026-2031.

The structural steel fabrication market, propelled by post-pandemic infrastructure stimulus and robust non-residential construction activity, pushed demand beyond long-term trends. Projections for 2026 to 2031 indicate a deceleration, attributed to maturing construction cycles in major economies, subdued real-estate-driven steel consumption in China, and a pivot towards specialized fabrication categories. These categories, while technically advanced, yield lower tonnage. The World Steel Association forecasts a modest 0.7% annual growth in finished steel demand through 2030. Future growth is expected to be supported by higher-value applications such as renewable energy and data centers. Demand in the structural steel fabrication market remains buoyed by government-backed infrastructure initiatives, energy transition efforts, digital fabrication advancements, and the burgeoning expansion of data centers and industrial reshoring. However, challenges loom; the market grapples with margin pressures stemming from steel price fluctuations, a dearth of skilled labor in welding and assembly, and intensified competition from mass timber and precast systems in certain building types.

Key Report Takeaways

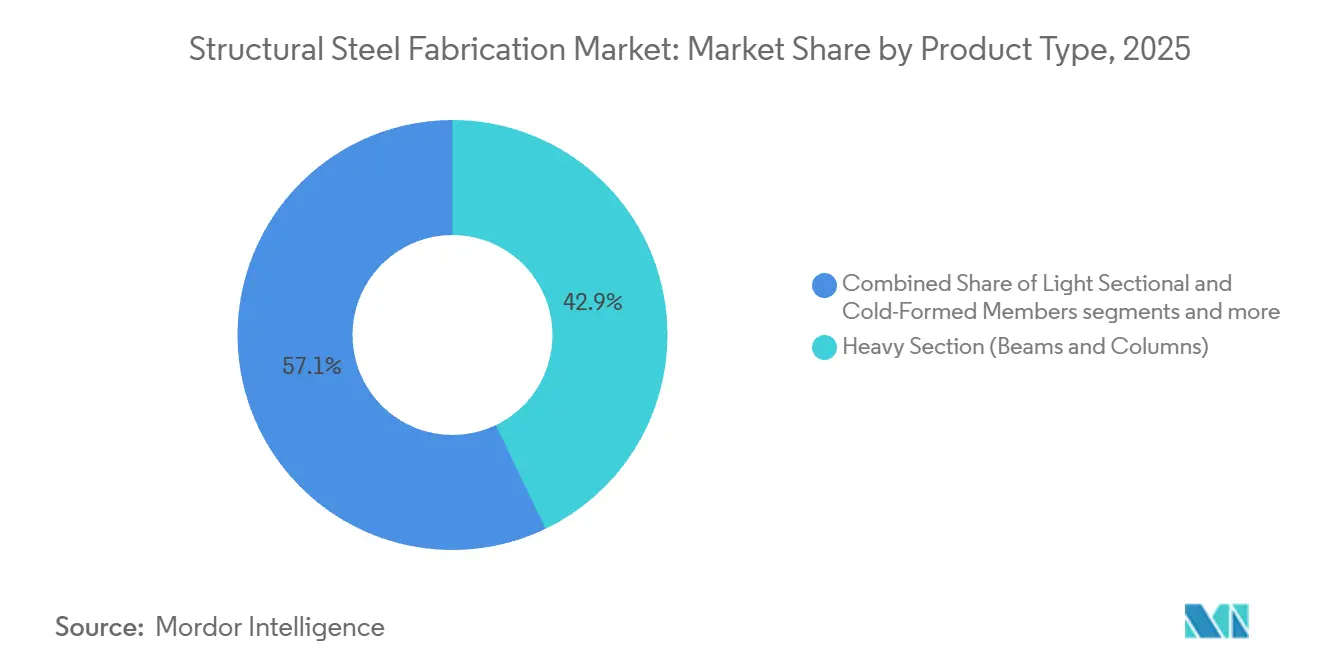

- By product type, heavy section (beams & columns) accounted for 42.87% share of the structural steel fabrication market size in 2025 and is also projected to grow at a 6.05% CAGR through 2031.

- By end-user industry, construction and infrastructure remained the largest segment in 2025, while renewable energy infrastructure is forecast to expand at 7.45% CAGR through 2031.

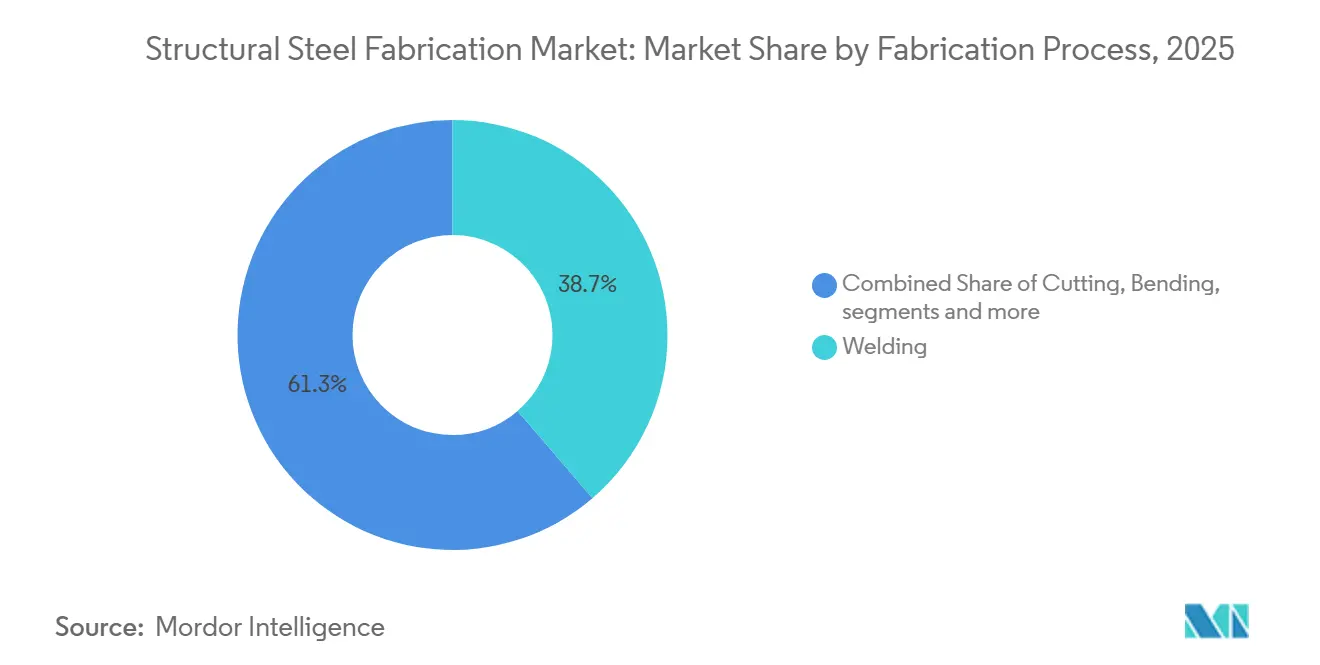

- By fabrication process, welding held 38.72% share in 2025, while cutting is projected to grow at a 7.78% CAGR through 2031.

- By geography, Asia-Pacific held 43.44% of the structural steel fabrication market share in 2025, while the Middle East & Africa is projected to advance at a 6.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Commercial Construction, Airports, Stadiums, and High-Rise Projects | +1.0% | Global, concentrated in North America, Asia Pacific, and Gulf Cooperation Council growth corridors | Medium term (2-4 years) |

| Rising Investments in Bridges, Rail Corridors, Ports, and Industrial Infrastructure | +0.8% | North America, Europe, and Asia Pacific are the core markets, with expansion into the Middle East and Africa and South America | Long term (≥ 4 years) |

| Rising Use of Robotic Welding, CNC Cutting, and BIM-Integrated Fabrication | +0.7% | North America and Europe lead adoption, with rapid uptake in South Korea and China | Medium term (2-4 years) |

| Growth of Renewable Energy Projects, Including Wind Towers and Solar Mounting Structures | +0.6% | Global, with mature markets in Europe and North America and faster expansion in Asia Pacific and the Middle East and Africa | Long term (≥ 4 years) |

| Expansion of Data Centers, Warehouses, and Logistics Parks | +0.5% | North America dominates, with expanding adoption across Asia Pacific and Europe | Short term (≤ 2 years) |

| Increasing Adoption of Prefabricated and Modular Construction Methods | +0.4% | Asia Pacific is the core market, with expansion into North America and the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Commercial Construction, Airports, Stadiums, and High-Rise Projects

Commercial construction continues to support the structural steel fabrication market, as major public and private projects require complex steel assemblies rather than simple commodity sections. Airport terminals, stadiums, convention centers, and mixed-use towers depend on transfer trusses, long-span members, facade supports, and other engineered components that require advanced detailing and fabrication discipline. The FHWA FY 2026 budget request included USD 30.8 billion for the National Highway Performance Program and USD 14.9 billion for the Surface Transportation Block Grant Program, supporting broader non-residential development along transport and urban growth corridors.[1]U.S. Department of Transportation, Federal Highway Administration, “Budget Estimates Fiscal Year 2026 Federal Highway Administration,” U.S. Department of Transportation, transportation.gov Public-assembly buildings also operate within strict structural design and seismic codes, and those code requirements continue to reinforce steel use in high-occupancy settings.[2]American Society of Civil Engineers, “ASCE 7 Minimum Design Loads and Associated Criteria for Buildings and Other Structures,” American Society of Civil Engineers, asce.org Mixed-use projects that combine office, retail, advanced manufacturing, and high-power-density floor systems often require heavier framing than standard commercial buildings. That combination keeps premium fabrication demand firm and helps the structural steel fabrication market retain value even when basic building activity becomes less predictable.

Rising Investments in Bridges, Rail Corridors, Ports, and Industrial Infrastructure

Bridge and transport infrastructure remains one of the clearest demand anchors for the structural steel fabrication market because few materials can match steel’s strength-to-weight ratio, weldability, and fatigue performance under repetitive loading. The FHWA identified a USD 191.3 billion bridge rehabilitation backlog across the National Bridge Inventory, and proposed funding was expected to reduce that backlog by 26.8% by 2026. That backlog translates into ongoing demand for plate girders, wide-flange members, truss elements, and fracture-critical connection assemblies that require certified fabrication and close quality control. The FHWA final Buy America framework, which became effective in March 2025 and further tightens for projects obligated from October 2026, strengthens the order pool for domestic suppliers on federally funded highway work.[3] U.S. Department of Transportation, Federal Highway Administration, “Buy America Requirements for Iron, Steel, and Manufactured Products Q&A,” Federal Highway Administration, fhwa.dot.gov Similar infrastructure programs in rail, ports, and industrial zones across Asia and the Gulf also favor fabricated steel because these projects need repeatable structural performance and reliable erection speed. This keeps the structural steel fabrication market tied to long-cycle public capital spending, which is usually more stable than speculative building demand.

Rising Use of Robotic Welding, CNC Cutting, and BIM-Integrated Fabrication

Automation has become a direct growth driver for the structural steel fabrication market, as labor constraints now limit throughput in many fabrication shops. The American Welding Society estimated 771,000 welding professionals in the United States in 2025 and projected a need for 320,500 additional professionals by 2029, with nearly 80,000 annual openings and an average welder age of 55. AWS D1.1:2025 established a clearer qualification pathway for robotic and mechanized welding, reducing one of the main compliance barriers that had slowed adoption in code-governed structural work. BIM-linked fabrication workflows also improve fit-up accuracy because CNC cutting, drilling, and layout can be driven directly from model data rather than through repeated manual transfer. Better digital traceability supports stronger quality documentation and can improve certification performance in procurement-driven projects. As a result, the structural steel fabrication market is becoming less dependent on incremental labor expansion and more dependent on capital investment in automated capacity.

Growth of Renewable Energy Projects, Including Wind Towers and Solar Mounting Structures

Renewable energy projects are opening a distinct demand channel for the structural steel fabrication market, as their investment cycle follows energy policy and grid build-out rather than building activity alone. Offshore wind foundations, transition pieces, and jacket structures require heavy-plate fabrication and strict weld quality, placing these projects at the high-value end of the market. The Oceantic Network estimated that 70 GW of offshore wind projects already leased or proposed in the United States would require nearly 22 million tons of steel over two decades. Solar tracker systems also create volume demand for precision-formed structural sections such as posts, channels, and torque tubes, where dimensional consistency matters at scale. In parallel, transmission expansion and renewable equipment manufacturing facilities create new structural demand before electricity production even begins. This gives the structural steel fabrication market a broader mix of end uses and reduces its dependence on traditional commercial construction alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Carbon Steel Plate, HRC, and Structural Section Prices | -0.8% | Global, most acute in North America and Europe, where spot price swings affect fixed-price backlogs | Short term (≤ 2 years) |

| Skilled Labor Shortages in Welding, Fitting, and Structural Assembly | -0.6% | North America and Europe most severe, with structural pressure also present in Japan and South Korea | Long term (≥ 4 years) |

| High Transportation Costs and Logistical Challenges for Oversized Fabricated Structures | -0.4% | Global, especially constraining in MEA and inland South America | Medium term (2-4 years) |

| Increasing Competition from Precast Concrete and Engineered Timber Structures | -0.3% | North America, Europe, and Australia, strongest where embodied-carbon disclosure is active | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Carbon Steel Plate, HRC, and Structural Section Prices

Price volatility remains a serious drag on the structural steel fabrication market because fabricators often bid on projects before steel is fully procured. That timing gap leaves fixed-price contracts exposed when input costs rise quickly. The United States Bureau of Labor Statistics producer price index for carbon hot-rolled bars, plates, and structural shapes increased from 165.262 in November 2025 to 171.096 in March 2026, representing a 3.5% rise over four months. Even a short-term move of that size can compress margins because labor, overhead, detailing, and erection schedules are usually committed before the full steel cost is locked in. When structural steel prices rise faster than the broader construction cost base, some developers delay awards, and fabricators become more selective in bidding. This pressure does not remove demand from the structural steel fabrication market, but it can slow order conversion and reduce profitability during active project cycles.

Skilled Labor Shortages in Welding, Fitting, and Structural Assembly

Labor shortages limit the structural steel fabrication market not only through vacancies but also through compliance and quality-control burdens. The American Welding Society continues to project nearly 80,000 annual welding openings in the United States through 2029, indicating a structural shortage rather than a short-cycle imbalance. AWS D1.1:2025 still requires qualified procedures, inspection discipline, and process-specific documentation, which means automation shifts the nature of labor demand but does not eliminate it. Shops need certified personnel to manage welding procedure specifications, procedure qualification records, inspection records, and robotic system qualification. That creates pressure on project schedules when experienced supervisors, fitters, and inspectors are in short supply. The structural steel fabrication market, therefore, faces a dual challenge: finding enough labor and maintaining sufficient qualified oversight to keep code-governed projects on schedule.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Lead Demand While HSS and HSLA Support Premium Applications

Heavy Section (Beams & Columns) accounted for 42.87% of the structural steel fabrication market share in 2025 and is projected to grow at a 6.05% CAGR through 2031. This segment leads because high-rise buildings, industrial plants, transport structures, and bridge superstructures continue to depend on wide-flange beams and columns for primary load-bearing performance. These sections remain central to the structural steel fabrication market because they offer predictable design behavior under established structural codes and are widely specified across public and private projects. Demand also remains firm in factory buildings and logistics facilities, where long spans and crane-support requirements favor heavy fabricated members over lighter framing systems. The segment is also supported by infrastructure programs and industrial reshoring activity, which continue to generate orders for large structural frames and bridge-related assemblies in North America and Asia-Pacific.

Tubular and Hollow Structural Sections, along with higher-performance steel grades, are gaining importance in the premium end of the material mix, even though they do not yet match the volume of heavy sections. ASTM A1085 HSS is seeing stronger specification preference in commercial and institutional projects because tighter wall tolerances and higher strength improve structural efficiency in exposed or high-specification applications. HSLA and other advanced structural grades are also finding wider use in bridge girders, wind tower base sections, and seismically detailed frames, where engineers seek lower structural weight without compromising strength. This shift does not weaken the heavy-section base of the structural steel fabrication market. Still, it does raise the value of fabrication work by moving more projects toward tighter tolerances, higher qualification requirements, and more specialized production capabilities.

By End-User Industry: Construction Leads Volume, Renewable Energy Registers Fastest CAGR

Construction and infrastructure remained the largest end-user segment, accounting for 42.31% of the market in 2025, while renewable energy infrastructure is projected to expand at a 7.45% CAGR through 2031. Commercial, industrial, and transport projects still form the broadest foundation for fabricated steel because they use structural frames across a wide range of project sizes and complexities. Industrial reshoring has added another layer of demand, especially in semiconductor, battery, and defense manufacturing, where clear spans and heavy overhead systems favor steel framing. Residential demand is still smaller, but steel is capturing a growing portion in multifamily and modular formats that require precision, repeatability, and faster assembly. Oil and gas, along with manufacturing-equipment support structures, continue to add stable demand in projects that require corrosion-resistant, seismic, or blast-resistant design considerations.

Renewable energy is the fastest-growing end-user category because it combines new generation assets, transmission expansion, and factory construction into one demand stream. Offshore wind towers, solar mounting systems, and related grid infrastructure need heavy or precision-fabricated assemblies that sit outside normal commercial building cycles. Policy-backed project pipelines also make this demand easier to forecast than many private building categories. Another important layer is that clean energy component factories create structural steel demand before turbines, panels, or electrical equipment begin operating. Automotive and transportation projects add a separate mid-growth layer through metro infrastructure, railway bridges, and intermodal terminals. This wider demand mix gives the structural steel fabrication market greater resilience and reduces reliance on any single construction cycle.

By Fabrication Process: Welding Leads Current Demand While Cutting Records the Fastest Growth

Welding accounted for 38.72% of the structural steel fabrication market share in 2025, making it the largest fabrication process segment. The segment leads because welding is essential across nearly all structural applications, from routine beam connections to full-penetration welds in heavy industrial and energy-related assemblies. Its position reflects the central role of weld quality, joint integrity, and code compliance in fabricated steel structures. The structural steel fabrication market continues to rely on welding as the main value-adding process in bridge components, building frames, tower sections, and complex structural assemblies. The 2025 update to AWS D1.1 also kept welding standards and qualification procedures at the center of project execution for code-governed structural work.

Cutting is projected to grow at the fastest CAGR of 7.78% through 2031. This growth is supported by wider adoption of CNC cutting systems, BIM-linked production workflows, and automated profile processing that improve dimensional accuracy and reduce fabrication cycle times. Precision cutting is becoming more important as projects demand tighter tolerances, better fit-up, and stronger production traceability across public and high-specification commercial work. Fabricators are also investing more in digital cutting platforms because these systems support downstream welding and assembly efficiency by reducing rework and alignment issues. This keeps cutting in a strong growth position within the structural steel fabrication market, even though welding remains the largest process segment by current revenue share.

Geography Analysis

Asia-Pacific held 43.44% of the structural steel fabrication market share in 2025, making it the largest regional base by value. The region benefits from China’s manufacturing scale, India’s infrastructure build-out, and Southeast Asia’s continued investment in logistics, factories, and urban transport systems. China remains important to the structural steel fabrication market because of its industrial base, but the next phase of growth is likely to be less real-estate-driven than before. The OECD Steel Outlook 2025 indicated that Chinese steel demand is expected to decline through 2030 as the real-estate sector contracts and the economy shifts structurally. Even so, India and Southeast Asia are well positioned to offset some of that moderation, as their infrastructure needs and manufacturing expansion remain well below developed-market saturation levels.

North America remains a high-value region for the structural steel fabrication market, as infrastructure spending, industrial reshoring, and data center expansion all support demand for certified fabrication. The FHWA FY 2026 budget request totaled USD 72.6 billion, and the tighter Buy America framework strengthens the role of domestic producers and fabricators in federally funded work. Europe remains strategically important because it favors high-documentation, compliance-heavy structural work, even though broader industrial demand has been weaker. The OECD also pointed to deindustrialization pressures in parts of Europe, which limit near-term volume growth even as the region pushes toward stricter decarbonization and traceability requirements. Those embodied-carbon and quality requirements give larger fabricators an advantage because they can manage documentation, material traceability, and certified procedures more effectively.

The Middle East & Africa is the fastest-growing regional segment, with a 6.30% CAGR through 2031. Saudi Arabia’s Vision 2030 project pipeline, including NEOM, Red Sea Global, and the King Salman International Airport program, continues to support demand for heavy sections, tubular frames, and prefabricated modules. Local content expectations in the Gulf are also encouraging more in-market fabrication, which can reshape competitive dynamics in the regional structural steel fabrication market. Across Africa, urbanization and infrastructure investment continue to support demand for industrial buildings, transport links, and lower-complexity fabricated sections.

Competitive Landscape

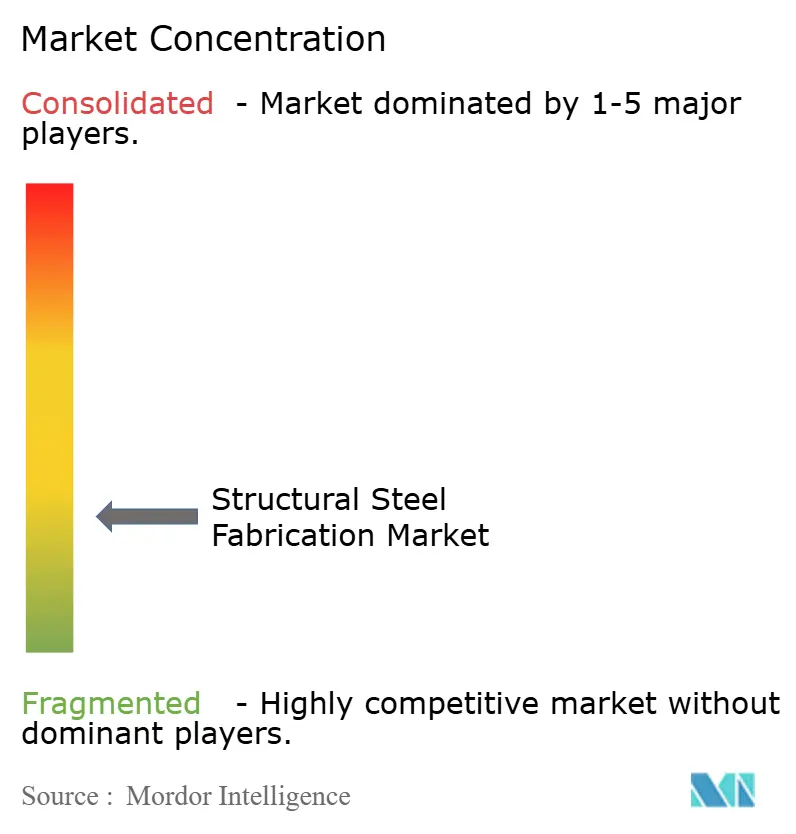

The global structural steel fabrication market is fragmented. Regional players still compete strongly on cost in standard sections, yet certification, documentation, and digital production capability create clear barriers in premium work. That is why competition is shifting away from pure tonnage pricing toward reliability, compliance, speed, and depth of project execution. AISC certification and ISO quality expectations increasingly serve as screening tools, favoring better-capitalized firms with established systems. In practice, companies with integrated fabrication capabilities are better positioned to compete that can combine detailing, fabrication, quality control, and field coordination rather than rely solely on low-cost shop output.

One clear sign of strategic pressure came in February 2026, when SGH and Steel Dynamics submitted a best-and-final offer to acquire BlueScope Steel, and BlueScope rejected the offer as materially undervaluing its operations. That episode showed how much value the market assigns to production geography, downstream capabilities, and integrated steel-to-fabrication positioning. Severfield’s move into the Hornsea 3 offshore wind project also showed how established structural fabricators are following demand into renewable infrastructure rather than staying tied to traditional building work. The company’s work on the Agratas battery manufacturing facility in 2025 similarly reflected a deliberate push toward battery and advanced manufacturing construction, where project complexity and execution quality matter more than commodity pricing. These examples show that the structural steel fabrication market is rewarding firms that reposition toward long-cycle, specification-heavy end uses.

Smaller regional fabricators still have room to compete, especially where cobot welding and CNC beam processing narrow the quality gap with larger plants. Even so, certification costs, process qualifications, and digital documentation remain meaningful barriers to scaling into public and premium private projects. Companies that stay focused on standard carbon-steel sections may lose share as owners and engineers shift toward higher-strength grades or stricter traceability requirements. The structural steel fabrication market, therefore, remains open enough for regional competition, but the strongest margins increasingly sit with fabricators that pair automation, certified quality systems, and end-market specialization.

Structural Steel Fabrication Industry Leaders

Vulcraft

Canam Group Inc.

Severfield plc

Zekelman Industries

Balfour Beatty plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Steel Dynamics and SGH submit a "best and final" bid of USD 21.8 per share, total consideration approximately USD 10.1 billion, to acquire BlueScope Steel. BlueScope rejects the proposal as materially undervaluing its North American, Australian, Asian, and New Zealand operations, a rejection that signals the strategic premium attached to integrated steelmaking and value-added fabrication assets in the current market.

- February 2026: Severfield commenced work on the Agratas battery manufacturing facility in Bridgwater, Somerset, a USD 5.0 billion project led by Sir Robert McAlpine, completing the structural steel frame for the first principal building. The project represents one of the most significant industrial construction programs currently active in the United Kingdom and positions Severfield at the center of the country's emerging battery manufacturing supply chain.

Global Structural Steel Fabrication Market Report Scope

The Structural Steel Fabrication Market is Segmented by Product Type (Heavy Section, Light Sectional & Cold-Formed Members, and more), by End-User Industry (Construction, Power & Energy, and more), by Fabrication Process (Cutting, Bending, Welding, Machining, Forming, Casting, Others), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are in Terms of Value (USD).

| Heavy Section(Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrastructure (Transport) | |

| Power & Energy | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation | |

| Other End User Industries |

| Cutting |

| Bending |

| Welding |

| Machining |

| Forming |

| Casting |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Heavy Section(Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-User Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrastructure (Transport) | ||

| Power & Energy | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation | ||

| Other End User Industries | ||

| By Fabrication Process | Cutting | |

| Bending | ||

| Welding | ||

| Machining | ||

| Forming | ||

| Casting | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for structural steel fabrication?

The structural steel fabrication market is valued at USD 162.45 billion in 2026 and is projected to reach USD 200.3 billion by 2031 at a 4.28% CAGR.

Which region leads global demand for fabricated structural steel?

Asia-Pacific led with 43.44% of global value in 2025, supported by China’s industrial base and ongoing infrastructure expansion in India and Southeast Asia.

Which end-user group is growing the fastest through 2031?

Renewable energy infrastructure is the fastest-growing end-user category, with a forecast CAGR of 7.45% through 2031.

Why is automation becoming more important in fabrication shops?

Robotic welding, CNC cutting, and BIM-linked workflows help fabricators raise throughput, improve weld traceability, and manage a persistent skilled labor shortage.

What is the biggest cost risk facing fabricators in 2026?

Steel price volatility remains a key risk because contracts are often fixed before material is fully purchased, which can compress margins when input prices rise quickly.

Which process segment is expanding the fastest?

Robotic welding and automated fabrication are the fastest-growing process segments, with a projected CAGR of 7.78% through 2031.

Page last updated on: