Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

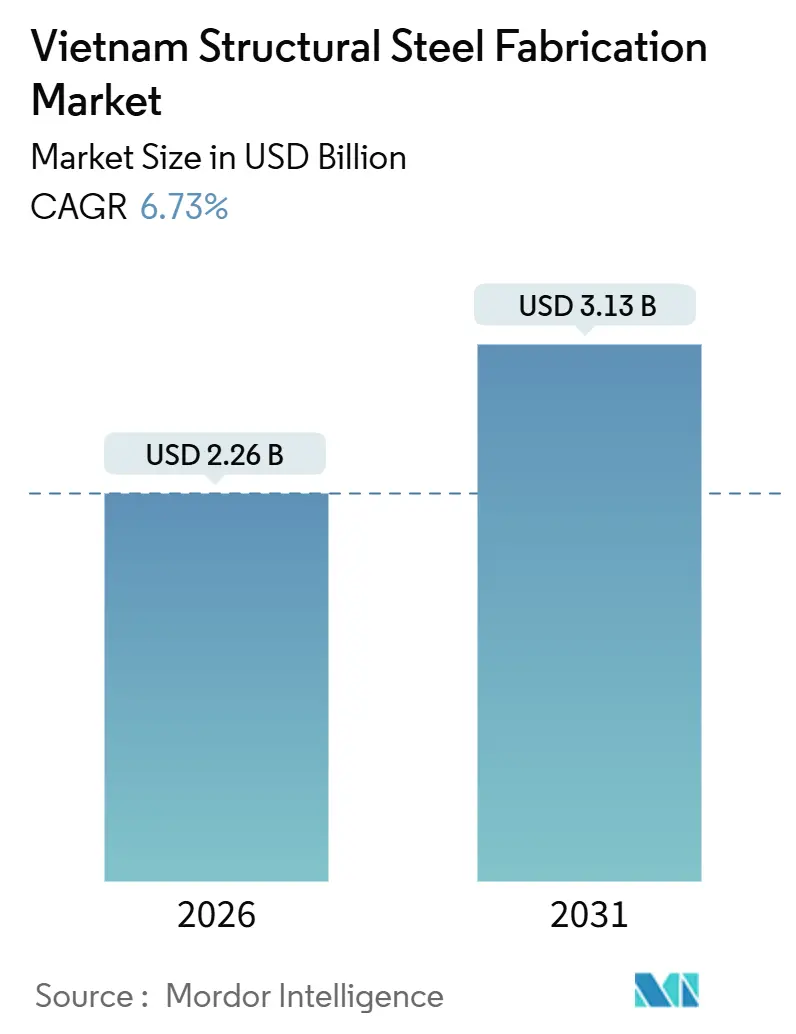

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Structural Steel Fabrication Market Analysis by Mordor Intelligence

The Vietnam structural steel fabrication market reached a market size of USD 2.26 billion in 2026 and is projected to climb to USD 3.13 billion by 2031, registering a 6.73% CAGR over the period. Demand is no longer tied only to square-meter additions but to the rising share of high-specification work, data-center frames, offshore wind towers, and composite cores that call for narrower tolerances and certified quality management. Automation of cutting and welding lines is accelerating because certified labor remains scarce and wages keep rising, while foreign investors keep moving capacity from China to Vietnam to diversify supply risk. The government’s USD 120 billion infrastructure plan deepens the project pipeline, and the shift toward low-carbon buildings favors domestic mills that can supply high-strength, lower-emission steel.

Key Report Takeaways

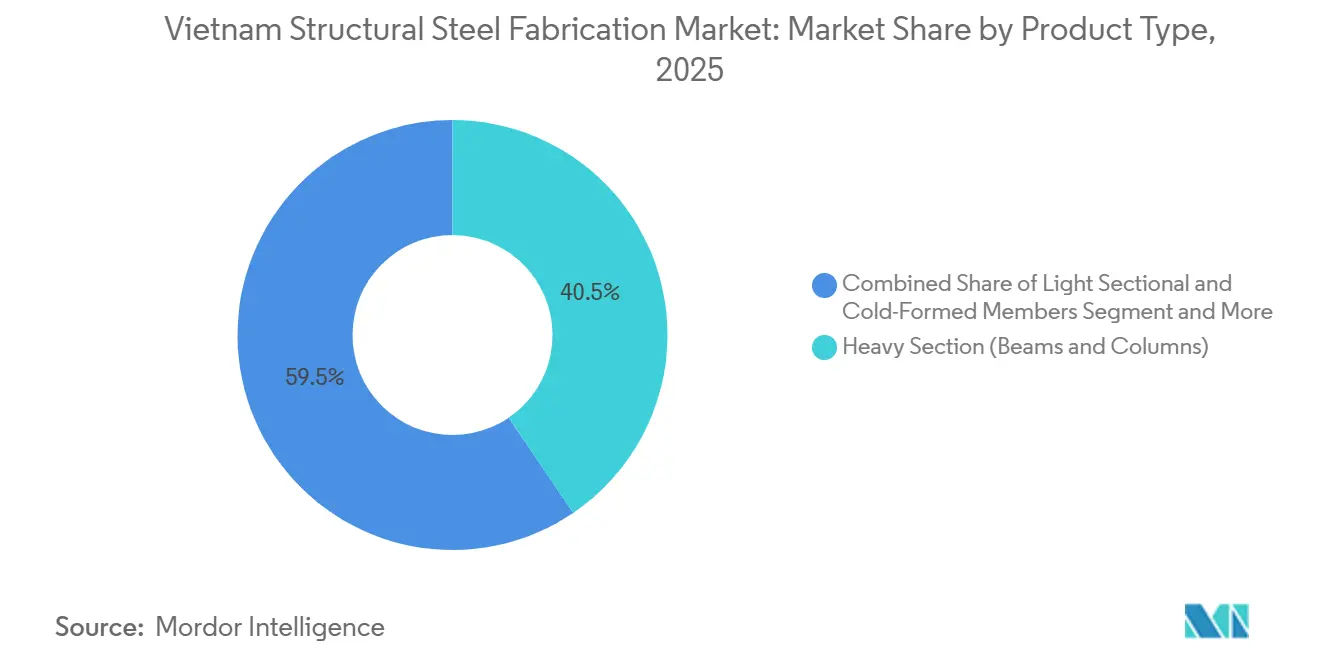

- By product type, heavy section beams and columns held 40.51% of the Vietnam structure steel fabrication market share in 2025, while the Other Product Types segment is forecast to expand at an 8.59% CAGR through 2031.

- By end-user industry, construction captured 46.73% of 2025 revenue and Infrastructure Transport is projected to grow at an 8.84% CAGR to 2031.

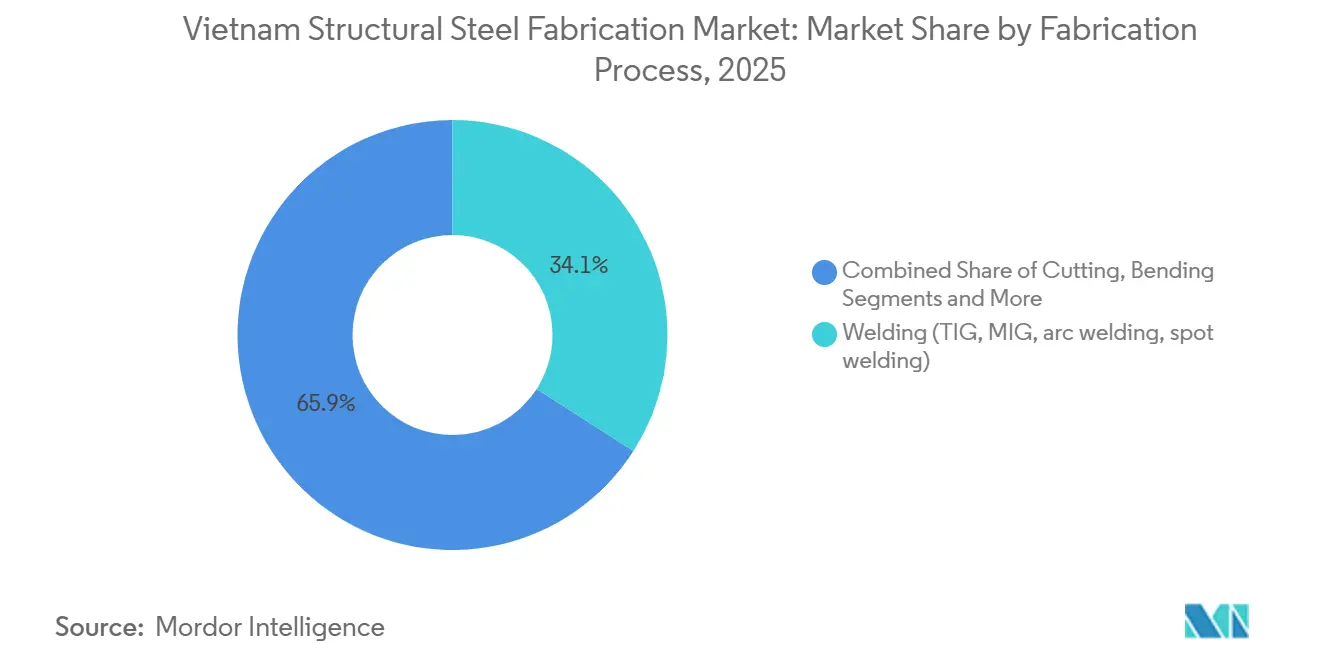

- By fabrication process, welding dominates with a 34.07% share of the 2025 value, whereas cutting is set to post the fastest 8.23% CAGR during the forecast horizon.

- By geography, Ho Chi Minh City accounted for 34.4% of 2025 spending, and the Rest of Vietnam is expected to log the quickest 8.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China + 1 foreign direct investment wave | +1.8% | Binh Duong, Dong Nai, Ba Ria–Vung Tau, Red River Delta | Medium term (2-4 years) |

| USD 120 billion 2021-30 infrastructure pipeline | +1.5% | National, early gains in Hanoi, Ho Chi Minh City, Da Nang | Long term (≥ 4 years) |

| Urban densification driving composite and steel-core high-rises | +1.0% | Hanoi, Ho Chi Minh City, Da Nang | Medium term (2-4 years) |

| Hyperscale data-center build-out | +0.9% | Hanoi, Ho Chi Minh City, spillover to Binh Duong | Short term (≤ 2 years) |

| Offshore wind tenders for >2 GW | +0.7% | Ba Ria–Vung Tau, Binh Thuan, Ninh Thuan, Tra Vinh | Medium term (2-4 years) |

| Green-building adoption of HSLA and modular steel | +0.6% | Nationwide, led by Hanoi and Ho Chi Minh City | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China + 1 FDI Wave Keeps Industrial Parks and Warehouse Builds on Record Pace

Multinationals committed USD 36.6 billion in 2024, 60% of it into manufacturing, as firms diversified away from China[1]Reuter Staff, “Vietnam lures record foreign investment as ‘China plus one’ strategy gains steam,” Reuters, reuters.com. These investors favor clear-span steel warehouses that can be delivered in weeks, pushing fabricators to deploy CNC shearing and automated welding to hit four-week lead times. Industrial land rents in Binh Duong and Dong Nai jumped 15–20% in 2024, underscoring demand. As long as port dredging and grid upgrades keep pace, the Vietnam structure steel fabrication market will keep capturing FDI-led orders.

USD 120 Billion Infrastructure Pipeline Accelerates Long-Span Demand

Expressways, airports, and metros under the 2021-30 plan require tens of thousands of tonnes of fabricated girders[2]World Bank Press Office, “World Bank approves USD 500 million to support Vietnam’s green energy transition,” World Bank, worldbank.org. Long Thanh International Airport alone calls for 90,000 m² of steel framing designed to TCVN 9386:2012 seismic codes. These projects widen the opportunity set for fabricators certified to EN 1090-1 execution classes, although land-acquisition delays can defer steel procurement by a year and compress margins when orders finally arrive.

Urban Densification Spurs Composite and Steel-Core High-Rises

Central-city land prices top USD 5,000 per m², so developers shift to taller towers that benefit from steel cores, slicing build time by 20-30%. These jobs demand ±2 mm tolerance over 100 m heights and mill certificates for HSLA grades, steering work to vertically integrated mills such as Hoa Phat. Mortgage tightening could, however, steer construction back to concrete-frame mid-rises.

Hyperscale Data-Centers After 2024 Localization Rules

Google opened a Vietnam Cloud region in September 2024. Server racks weighing 1.5–2 t/m² need seismic-rated frames with redundant load paths. Because typical project cycles run 12–18 months, clients award contracts only to fabricators that integrate BIM and pre-emptively resolve clashes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported slab and coil price volatility | –0.8% | Nationwide, especially import-dependent fabricators | Short term (≤ 2 years) |

| Stricter 2025 environmental permits and CO₂ fees | –0.6% | Smaller shops lacking ISO 14001 nationwide | Medium term (2-4 years) |

| Shortage of certified welders and NDT technicians | –0.5% | Most severe in Hanoi and Ho Chi Minh City | Short term (≤ 2 years) |

| Concrete and CLT gaining low-rise contracts | –0.3% | Residential and light-industrial segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Slab and Coil Price Volatility Erodes Margins

Hot-rolled coil imports hit 1.2 million t in September 2024, a 34% surge, with Chinese HRC undercutting domestic prices by USD 30–70/t. Fixed-price construction contracts lock revenue, so sudden input spikes squeeze margins. Integrated players such as Hoa Phat enjoy cost stability, while smaller fabricators struggle to secure hedging lines and may cede share within the Vietnam structure steel fabrication market.

Stricter 2025 Environmental Permits Raise Cap-Ex

Circular 45/2024/TT-BTNMT caps particulate and SO₂ emissions from July 2025, forcing plasma shops to invest USD 0.5 million in extractors and EAF operators to add USD 5 million in baghouses[3]Ministry of Natural Resources and Environment, “Circular 45/2024/TT-BTNMT and Decree 119/2025 on environmental regulations,” monre.gov.vn. MRV audits add USD 50,000–100,000 annually. Non-compliant yards risk permit suspension, accelerating consolidation toward ISO 14001-certified firms inside the Vietnam structural steel fabrication market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Dominate, Custom Modules Accelerate

Heavy section beams and columns secured 40.51% of 2025 revenue, reflecting their critical role in high-rise towers, bridges, and airport terminals across the Vietnam structure steel fabrication market. Standard W-shapes and H-piles shipped at volumes that let integrated mills like Hoa Phat offer bundle discounts, but tight competition and lower engineering intensity limit margin upside. Players differentiate through delivery speed and adherence to AISC tolerances, yet commoditization invites price pressure whenever Chinese imports dip below domestic offers.

The Other Product Types segment, plate-worked girders, custom modules, and skids will grow the fastest at an 8.59% CAGR. Energy and petrochemical clients prefer factory-assembled modules that cut field labor by 30–40%, and offshore-wind towers need thick plate beyond local rolling capacities until Ninh Binh’s new Steckel mill comes online. Fabricators able to pair TEKLA 3D modeling with CNC drilling that holds ±0.5 mm positional accuracy win these engineered orders and gain pricing power. As a result, the Vietnam structure steel fabrication market size for custom modules could reach USD 0.85 billion by 2031, moving the revenue mix toward higher-value work.

By End-User Industry: Construction Leads, Infrastructure Transport Surges

Construction end-users commanded 46.73% of 2025 spending, split among commercial, residential, and industrial buildings that require everything from lightweight purlins to composite cores. Warehouse demand linked to FDI inflows kept order books full, yet saturation in mature industrial parks may slow momentum after 2027. Fabricators serving this base often rely on ISO 9001 lines and standard design libraries, keeping average project margins moderate.

Infrastructure Transport is the fastest-growing end-user, projected at an 8.84% CAGR. North–South Expressway bridges need long-span girders, metro extensions in Hanoi and Ho Chi Minh City call for seismic-rated track slabs, and Long Thanh International Airport tops procurement lists for wide-flange steel. Contract awards favor bidders that certify to TCVN 9386:2012 and execute EN 1090-1 documentation; thus, integrated mills with design teams and robotic welding have a clear edge. Given the pipeline, this segment could capture 20% of the Vietnam structure steel fabrication market size by 2031.

By Fabrication Process: Welding Dominates, Cutting Gains Precision Share

Welding processes held 34.07% of the value in 2025 because every beam-to-column joint and tower seam relies on TIG, MIG, or flux-cored passes. Robotic gantries from Voortman and Lincoln Electric improve throughput by 30–40% and hold repeatability within ±0.5 mm, but complex positional welds on offshore flanges still demand certified human hands. Rising welder wages justify more automation, creating a split where large yards invest while small ones remain labor-intensive.

Cutting-lasers, plasmas, and water-jets will outpace all other methods at an 8.23% CAGR. Fiber-laser tables achieve ±0.03 mm kerf precision, meeting tolerance calls for data-center racks and wind-tower flanges. Domestic OEM VN-J offers budget machines, but top-tier buyers still specify Trumpf or Voortman hardware. As more projects reward first-time fit-up, spending on laser systems will lift cutting’s share inside the Vietnam structure steel fabrication market.

Geography Analysis

Ho Chi Minh City controlled 34.4% of 2025 revenue thanks to its dense FDI clusters in Binh Duong and Dong Nai and ready access to Vung Tau plate mills and Cai Mep deep-water docks. Industrial land scarcity and congestion, however, will curb growth to about the national average as lease rates and wages climb. Large fabricators are already scouting satellite yards two hours away to avoid trucking delays that added 18 months to the city’s first metro line.

Hanoi remains the political hub and a magnet for metro and airport upgrades. Yet fewer integrated mills nearby mean longer haul distances for plate, which trims margins or forces higher bid prices. Da Nang bridges the north-south gap with lower land costs and incentives for exporters serving Laos and Thailand, drawing mid-tier fabricators to set up satellite plants.

Rest of Vietnam - Ninh Binh, Thanh Hoa, Binh Thuan, Tra Vinh, Nghe An, will post the fastest 8.1% CAGR as expressways and wind farms spread beyond the deltas. Xuan Thien’s USD 380 million green-steel complex in Ninh Binh illustrates the push to locate heavy plate near renewable power and coastal ports. Provincial enforcement of new emission rules will determine whether compliant players keep their premium or face undercutting by non-certified rivals.

Competitive Landscape

Competition in the Vietnam structure steel fabrication market is fragmented. Hoa Phat’s 12 million-ton integrated capacity gives it cost leverage on commodity longs, yet specialist firms such as ATAD, PEB Steel, and Zamil Steel thrive by supplying turnkey industrial buildings with ISO 9001 and MBMA certifications. These mid-caps deploy CNC lines and BIM-enabled design to guarantee four-week fabrication-to-erection cycles that global clients demand[4]PEB Steel Buildings, “Company profile,” Peb Steel, slideshare.net.

Conglomerates have begun upstream expansion. Vingroup founded VinMetal in October 2025 with a 5 million-ton phase-one capacity aimed at EV-grade and rail steel, feeding captive demand from VinFast and Vinhomes while selling surplus to public projects. Their entry may squeeze independent fabricators by bundling steel with turnkey contracting.

Technology investment now separates winners. Fiber-laser tables priced at USD 0.8 million and robotic welding cells at USD 0.3 million each let large yards lift output per worker and cut defect rates to near zero. Smaller shops, facing certified-welder shortages and emission-control cap-ex, risk relegation to low-spec warehouses unless they merge or secure equity injections. Offsetting fragmentation, new environmental rules and price volatility could prompt a wave of consolidation, gradually raising the market’s concentration.

Vietnam Structural Steel Fabrication Industry Leaders

Hoa Phat Group

Formosa Ha Tinh Steel

Hoa Sen Group

Nam Kim Steel

Viet Y Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Xuan Thien and Primetals agreed to build two green-steel lines employing EAF Ultimate furnaces and Steckel plate rolling in Ninh Binh.

- October 2025: Vingroup launched VinMetal with USD 380 million capital to build a high-tech steel complex in Ha Tinh.

- October 2024: Ho Chi Minh City’s 19.7 km Metro Line 1 became Vietnam’s first operational metro, showcasing demand for elevated steel guideways.

- September 2024: Google inaugurated its Vietnam Cloud region, triggering a surge in seismic-rated data-center fabrication.

Vietnam Structural Steel Fabrication Market Report Scope

By Product Type

| Heavy Section (Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

By End-user Industry

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrastructure Transport | |

| Power & Energy | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation | |

| Other End-user Industries (Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, Telecommunications) |

By Fabrication Process

| Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) |

| Bending (Press brakes, roll bending, rotary bending) |

| Welding (TIG, MIG, arc welding, spot welding) |

| Machining (Milling, turning, drilling, grinding, CNC machining) |

| Forming (Stamping, forging, rolling, hydroforming) |

| Casting (Sand casting, die casting, investment casting) |

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) |

By Geography

| Ho Chi Minh City |

| Hanoi |

| Da Nang |

| Rest of Vietnam |

| By Product Type | Heavy Section (Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-user Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrastructure Transport | ||

| Power & Energy | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation | ||

| Other End-user Industries (Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, Telecommunications) | ||

| By Fabrication Process | Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) | |

| Bending (Press brakes, roll bending, rotary bending) | ||

| Welding (TIG, MIG, arc welding, spot welding) | ||

| Machining (Milling, turning, drilling, grinding, CNC machining) | ||

| Forming (Stamping, forging, rolling, hydroforming) | ||

| Casting (Sand casting, die casting, investment casting) | ||

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) | ||

| By Geography | Ho Chi Minh City | |

| Hanoi | ||

| Da Nang | ||

| Rest of Vietnam | ||

Key Questions Answered in the Report

What is the current value of the Vietnam structure steel fabrication market?

The market is valued at USD 2.26 billion in 2026 and is projected to reach USD 3.13 billion by 2031.

Which product type contributes most to revenue?

Heavy section beams and columns provided 40.51% of 2025 revenue, driven by high-rise and infrastructure projects.

Which end-user segment will grow quickest through 2031?

Infrastructure Transport is forecast to post the fastest 8.84% CAGR thanks to expressway, metro, and airport builds.

Why are cutting processes gaining share in Vietnam’s fabrication shops?

Fiber-laser tables deliver ±0.03 mm accuracy needed for wind-tower flanges and data-center frames, pushing cutting to an 8.23% CAGR.

Which geography will see the fastest market expansion?

Provinces outside the three big cities - the Rest of Vietnam group are expected to grow at 8.1% CAGR as expressways and wind farms disperse demand.

How will new environmental rules affect small fabricators?

Circular 45/2024 and Decree 119/2025 require costly emission controls and CO₂ monitoring, raising compliance costs that smaller shops may struggle to absorb.

Page last updated on: