Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

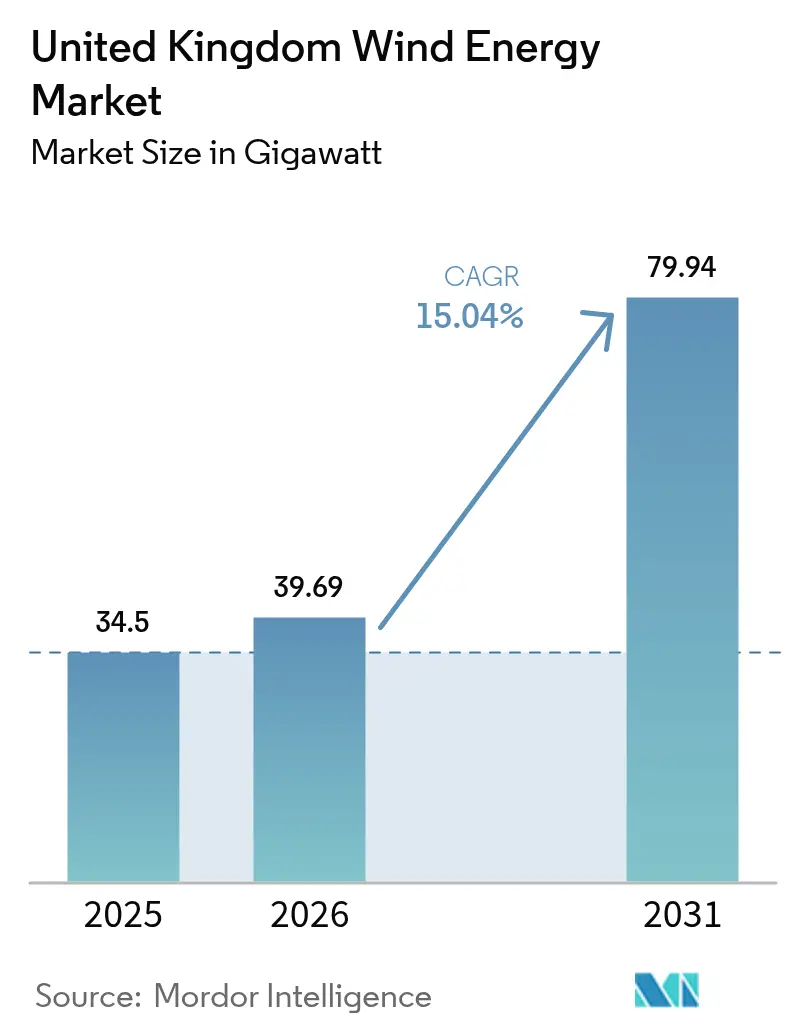

| Base Year Market Size (2025) | 34.5 gigawatt |

| Market Volume (2026) | 39.69 gigawatt |

| Market Volume (2031) | 79.94 gigawatt |

| Growth Rate (2026 - 2031) | 15.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Wind Energy Market Analysis by Mordor Intelligence

The United Kingdom Wind Energy Market size is expected to grow from 34.5 gigawatt in 2025 to 39.69 gigawatt in 2026 and is forecast to reach 79.94 gigawatt by 2031 at 15.04% CAGR over 2026-2031.

This expansion follows the July 2024 policy change, which removed England’s onshore restrictions and aligned wind energy with other energy infrastructure. Liberalized planning has revived stalled onshore proposals, accelerated repowering, and stimulated record tender activity. Offshore growth benefits from ScotWind and Celtic Sea leasing rounds, while inflation-indexed Contract for Difference (CfD) strike prices shelter developers from cost volatility. The sector must, however, navigate supply-chain gaps in steel monopiles and subsea cables, rising gilt-linked finance costs, and vessel shortages that threaten project schedules.

Key Report Takeaways

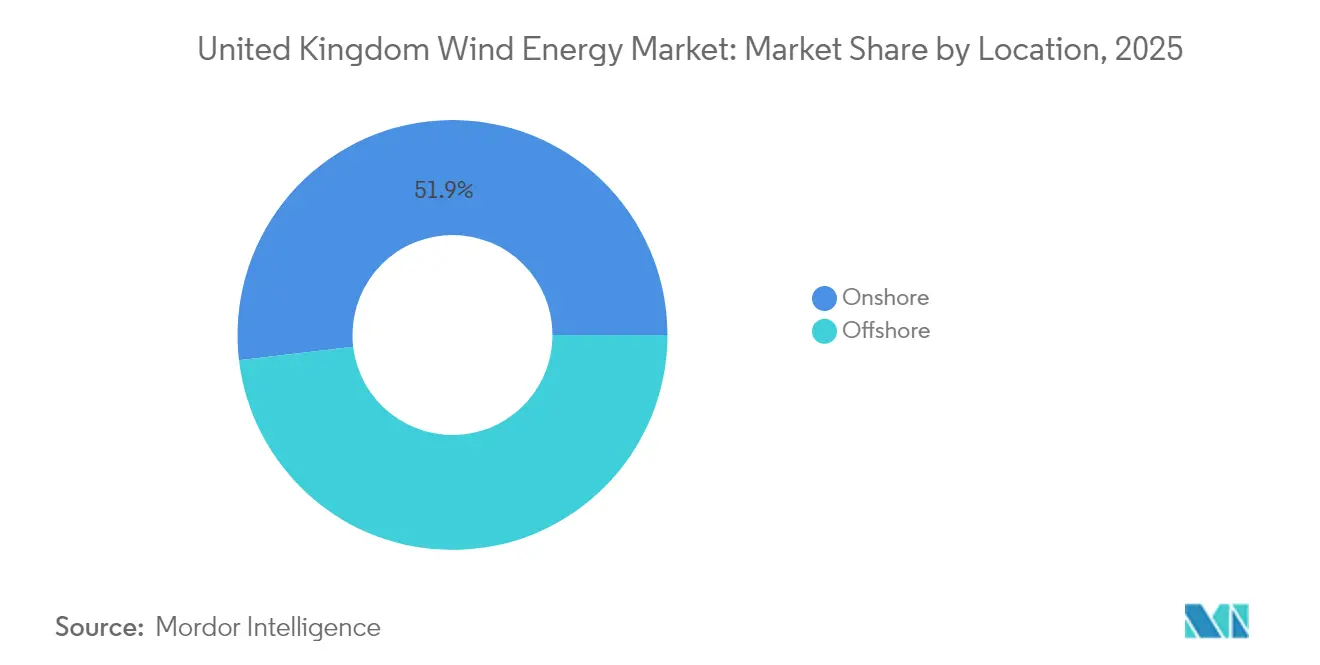

- By location, onshore wind held 51.88% of the UK wind power market share in 2025, while offshore wind is projected to expand at a 20.18% CAGR through 2031.

- By turbine capacity, units exceeding 6 MW captured a 74.42% share of the UK wind power market size in 2025, and this segment is forecasted to grow at a 18.22% CAGR to 2031.

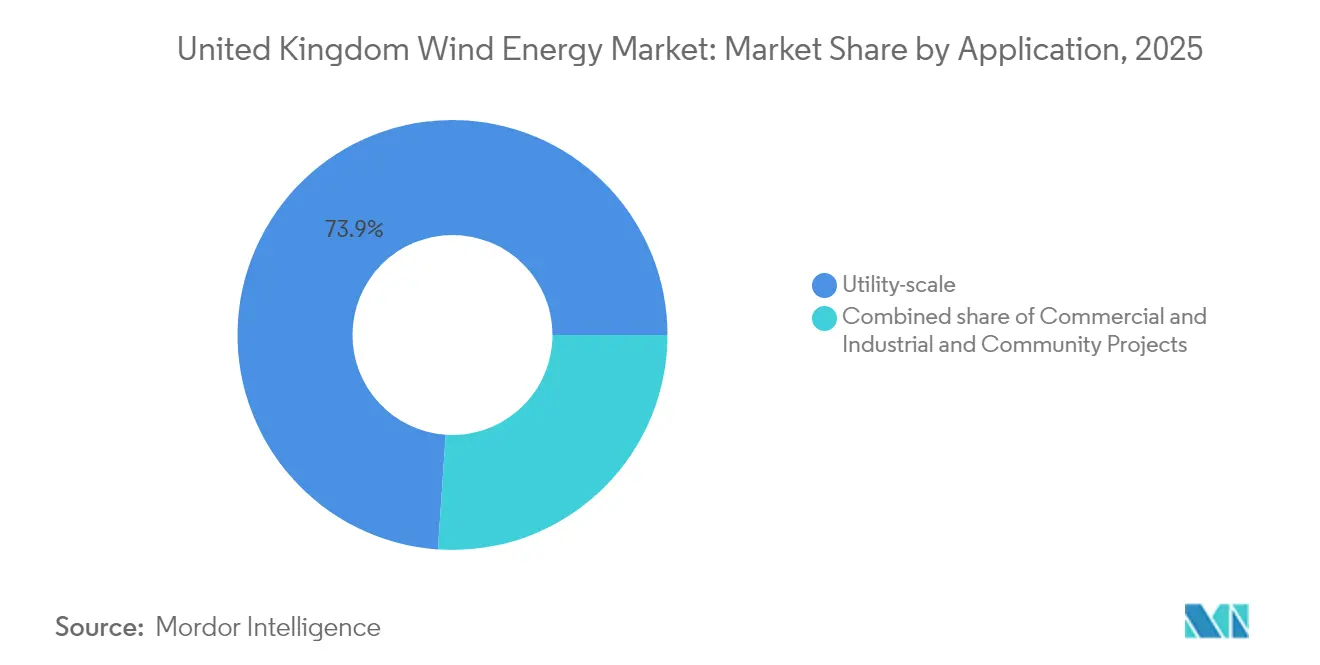

- By application, utility-scale projects accounted for 73.92% of the UK wind power market size in 2025, while community projects are expected to advance at a 20.72% CAGR between 2026 and 2031.

- ScottishPower, Ørsted, and SSE Renewables together controlled an estimated 40.35% share of installed capacity in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid build-out of Round 3 & ScotWind offshore lease projects | +3.2% | Scotland, North Sea waters | Medium term (2-4 years) |

| Repowering of early on-shore fleets reaching 20-year life | +2.1% | Scotland, England, Wales | Short term (≤ 2 years) |

| Contract for Difference AR6 price-floors linked to CPI(X) | +2.8% | UK-wide | Medium term (2-4 years) |

| Grid-balancing revenues from National Grid's Dynamic Services reform | +1.4% | England, Wales | Short term (≤ 2 years) |

| Co-location with green hydrogen electrolysers at port hubs | +1.9% | Scotland, Wales coastal regions | Long term (≥ 4 years) |

| AI-enabled predictive O&M cutting LCOE below £40/MWh | +2.2% | UK-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid build-out of Round 3 and ScotWind offshore lease projects

The Crown Estate’s ScotWind awards opened a 25 GW pipeline across 17 leases that already possess surveys, grid links, and vessel bookings, trimming typical development cycles by almost two years.[1]The Crown Estate, “Industrial Growth Plan,” thecrownestate.co.uk East Anglia Hub’s 2.9 GW build and other Round 3 schemes cluster contracts, lift local content, and unlock economies of scale in foundations and logistics. The Industrial Growth Plan estimates 10,000 additional jobs each year and a GBP 25 billion economic value by 2035, assuming annual deployment remains near 6 GW. Yet, Ørsted’s cancellation of Hornsea 4 underscores the need for realistic strike prices and resilient supply chains.

Repowering of early onshore fleets reaching 20-year life

Projects such as Hagshaw Hill replaced 1990s turbines with half the unit count yet quintupled output, cutting LCOE and minimizing fresh land take. Octopus Energy aims to refurbish 1,000 legacy machines, potentially adding 5 GW on pre-consented footprints. Proven wind data, existing community support, and grid capacity shrink lead times compared with greenfield builds. Modern 6-8 MW platforms also provide grid-formative services, enhancing system value.

CfD AR6 price-floors linked to CPI(X)

CfD AR6 secured 990 MW onshore at GBP 50.90/MWh and revised offshore prices to GBP 73/MWh, restoring bid realism after AR5’s zero-award outcome.[2]Department for Energy Security and Net Zero, “Clean Power 2030 Action Plan,” gov.uk Indexation protects developers against inflation in steel and cable costs, while consumers share in the productivity gains. Draft AR7 rules propose terms longer than 15 years and flexible budget caps to crowd in 12 GW of capacity. These tweaks reduce cost-of-capital pressure caused by higher gilt yields.

Grid-balancing revenues from National Grid’s Dynamic Services reform

Dynamic Containment and Regulation contracts pay wind farms for inertia, frequency, and voltage services concurrently with energy sales. A GBP 328 million six-year deal already saves billpayers GBP 128 million. New-build projects now specify advanced converters and on-site batteries to capture these dual revenues, lifting project IRRs and supporting a grid target of 100% zero-carbon operation by 2035.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain bottlenecks in XXL monopiles & HVDC cables | -2.8% | North Sea, Celtic Sea offshore areas | Short term (≤ 2 years) |

| Community opposition in scenic highlands delaying permits | -1.4% | Scotland, Wales, Northern England | Medium term (2-4 years) |

| Rising cost of capital from higher UK gilt yields | -1.9% | UK-wide | Short term (≤ 2 years) |

| Scarcity of experienced offshore installation vessels | -1.7% | UK offshore waters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain bottlenecks in XXL monopiles and HVDC cables

Europe’s fabrication capacity is projected to cover only 70% of steel demand by 2029, with the UK's needs alone at 3.8 million tonnes for 2025-2027. Limited plants capable of producing more than 2,000 tons of monopiles drive 40-50% price jumps and multi-year lead times. SeAH Wind’s Teesside line, due 2026, helps but fills just a fraction of the gap. HVDC cable slots exhibit similar strain, potentially risking grid connection delays.

Community opposition in scenic highlands delaying permits

Landscape concerns halted Faw Side and Lowther Hills applications despite compliance with the energy policy.[3]BBC News, “Scottish Government Rejects Faw Side Wind Farm,” bbc.co.uk The Scoop Hill proposal also encountered difficulties in securing local council votes. Government-mandated benefit sharing aims to align host communities; however, inconsistent adoption still prolongs consent by 18-24 months on average.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Onshore resurgence drives market acceleration

The UK wind power market size for onshore installations reached 17.9 GW in 2025, accounting for 51.88% of the total capacity. Onshore’s cost advantage, rapid build cycle, and revived policy status attract at least six developers exploring fresh English sites and large-scale repowering. Projects such as Scout Moor II, at 100 MW, underscore the scale unlocked after the ban was lifted. Repowering older clusters quadruples capacity on proven ground and capitalizes on existing grid access.

Policy momentum also fuels community support schemes that tie local ownership to bill credits, thereby smoothing the planning process. Yet grid headroom in northern England and Scotland narrows, making reinforcement indispensable to double onshore to the targeted 30 GW by 2030. Digital forecasting and flexible connections mitigate curtailment risk as National Grid’s stability markets mature.

Offshore accounted for 16.6 GW in 2025 and is on track for 50.03 GW by 2031, advancing at a 20.18% CAGR. The segment benefits from mean capacity factors above 50% and project modularity above 1 GW, which improves financing scale and export potential. ScotWind’s 25 GW leasing and Celtic Sea’s 4.5 GW floating awards dominate the project tracker. While monopile and vessel constraints temper near-term build rates, inflation-indexed CfD strike prices now better reflect higher capex, restoring bid appetite.

By Turbine Capacity: Large turbines dominate efficiency drive

Turbines above 6 MW held 74.42% of the UK wind power market share in 2025, reflecting developer preference for maximizing energy per foundation. Siemens Gamesa’s 14 MW units selected for East Anglia TWO prove bankability at this scale. Larger rotors reduce balance-of-plant costs per MWh and generate additional income from frequency services.

The UK wind power market size for machines exceeding 6 MW is expected to reach 69.67 GW by 2031, growing at an 18.22% CAGR. Manufacturers co-locate blade and nacelle plants in Scotland and the Humber to reduce transport bottlenecks and capitalize on local content bonuses. The 3-6 MW class remains relevant for landlocked or weak-grid onshore sites, but its share is expected to slide beneath 19.80% by 2031 as planners favor higher nameplate capacities to optimize scarce land and grid slots.

Small turbines under 3 MW fill niche roles in estate and repowering applications where crane, road, or planning limitations apply. Octopus Energy’s programme targets single-MW retrofits on existing pads, pairing them with community PPAs for faster payback. However, the absence of a domestic supply chain for these sizes may constrain volumes.

By Application: Utility-scale dominance faces community challenge

Utility-scale plants controlled 73.92% of the UK wind power market size in 2025, leveraging deep balance sheets and vertical integration. Operators bundle merchant, CfD, ancillary, and storage revenue into diversified portfolios. ScottishPower has doubled its UK investment pipeline to GBP 24 billion through 2028, signaling confidence in this model. Utilities also pioneer co-located batteries, as seen in the 600 MWh Hornsea 3 storage adjunct, which improves grid compliance and arbitrage spreads.

Community projects, while small, expand fastest. Growth at 20.72% CAGR springs from revised benefit protocols that guarantee host villages up to GBP 5,000 per MW annually and partial equity stakes. Lower technology costs and retail-linked platforms encourage civic groups to crowdfund turbines or partner with energy suppliers. Their aggregate capacity could top 3.4 GW by 2031, contributing to social license and local grid services.

Commercial and industrial self-supply completes the application mix, with supermarkets and manufacturers installing behind-the-meter turbines to cut Scope 2 emissions. Long-dated corporate PPAs align with decarbonization targets and hedge volatile grid prices.

Geography Analysis

Scotland supplied 33.62% of the 2025 national output and anchors more than 39.75% of the forward pipeline. Its North Sea resource, port infrastructure, and streamlined Marine Scotland consents allow multigigawatt clusters like Moray West to progress swiftly. Vestas's proposed Leith blade plant complements existing fabrication at Nigg and Aberdeen, strengthening domestic content.

Wales is evolving into a leading hub for floating wind power. The Celtic Sea plan allocates 4.5 GW across three pre-commercial arrays, which will trial 14 MW units on semi-sub platforms. Port Talbot's GBP 500 million redevelopment positions it as an assembly hub, with the wider freeport projected to support 16,000 roles. Project Erebus will showcase technology readiness by 2026 and unlock export of fabrication services to other Atlantic markets.

England re-opens its onshore prospectivity after the July 2024 reforms. Scout Moor II and numerous smaller sites in Lincolnshire and Yorkshire populate a fresh 6-8 GW pipeline. Network reinforcements under the Holistic Network Design accelerate grid access, though community benefit compliance varies by county. Offshore, Dogger Bank continues phased commissioning, with Dynamic Stability contracts enhancing revenue stacking. Northern Ireland maintains 14.65% of the UK's installed onshore capacity and exploits cross-border trading to the Irish Single Electricity Market, while Belfast Harbour upgrades enable turbine staging for both Irish and Scottish projects.

Regulatory Landscape

The United Kingdom wind energy regulatory framework is anchored by the Department for Energy Security and Net Zero (DESNZ) and the UK planning regime for major infrastructure, with updated policy guidance under the National Policy Statement for Renewable Energy Infrastructure (EN-3, 2025) published on 6 January 2026. A key planning shift took effect on 31 December 2025 through the Infrastructure Planning (Onshore Wind and Solar Generation) Order 2025, which reclassified onshore wind projects above 100 MW as nationally significant infrastructure and moved large schemes into a more centralized consenting pathway.

Market economics and grid delivery are also influenced by auction and network regulation. DESNZ issued a government response on Allocation Round 8 (AR8) refinements in July 2026, adjusting elements such as sealed bid visibility and the auction price base for offshore categories including floating and other deepwater projects. On the networks side, Ofgem set RIIO-3 electricity transmission price controls for 1 April 2026 to 31 March 2031 and is running offshore transmission owner (OFTO) regime consultations in 2026, including May 2026 proposals on early and late competition models. These steps align offshore connection governance with strategic network planning led by the National Energy System Operator.

Competitive Landscape

Market leadership rests with a cluster of integrated utilities and specialist offshore developers. Ørsted operates 5.6 GW across 12 UK sites, but recently absorbed a DKK 3.5-4.5 billion hit from canceling Hornsea 4, citing inflated capital expenditure and financing costs. SSE Renewables couples generation with transmission ownership, diversifying cash flows, whereas ScottishPower’s GBP 24 billion capital plan focuses on strengthening UK-based supply chains.

Technology providers such as Siemens Gamesa, Vestas, and GE Vernova supply most nacelles above 8 MW. Vestas plans to establish a blade factory in Leith to secure domestic content and mitigate logistics risks.[6]BBC News, “Vestas Blade Factory Proposal,” bbc.co.uk Supply-chain newcomers like SeAH Wind invest £300 million in Teesside monopiles, addressing a chronic shortfall and positioning themselves for Celtic Sea floating contracts.

Competition intensifies in the floating wind sector, where oil-service majors Equinor and TechnipFMC bring their expertise in mooring and subsea technologies. Energy retailers such as Octopus Energy are diversifying into generation, acquiring stakes in East Anglia One and marketing direct-to-household green tariffs. Installation vessel operators Cadeler and DEME expand their fleets, but the current scarcity still constrains project sequencing.

United Kingdom Wind Energy Industry Leaders

Ørsted A/S

SSE Renewables

ScottishPower Renewables

RWE Renewables

Vattenfall AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Auction-backed buildout and leasing visibility create whitespace across offshore, floating, and onshore pipelines, while also expanding adjacent opportunities in manufacturing and port infrastructure. The government Clean Power 2030 Action Plan sets capacity ambitions of 43-50 GW of offshore wind and 27-29 GW of onshore wind by 2030, including up to 5 GW of floating wind. It also ties near-term awards to Allocation Round 7 (AR7), which awarded 8.4 GW of offshore wind capacity (results published in January 2026). The Crown Estate further signaled future seabed access by outlining Offshore Wind Leasing Round 6 in the first half of 2027, with an approximate 6 GW target, supporting multi-year project origination beyond current leasing rounds.

Supply-chain localization and grid integration are central opportunity areas because they map to documented bottlenecks and the policy levers driving procurement. In Scotland, Vestas announced plans in March 2026 for a new nacelle and hub assembly factory, contingent on AR7 and AR8 order intake, strengthening the domestic manufacturing case tied to auction delivery and local-content priorities. For ScotWind, developers have reported supply-chain commitments and spending plans, with July 2026 reporting citing an average predicted spend of about GBP 1.6 billion per project across sixteen projects, totaling GBP 25.5 billion. That outlook keeps near-term demand focused on foundations, subsea cables, ports, and installation services. England-focused onshore openings also extend repowering and new-site development pathways, supported by the Onshore Wind Taskforce strategy and ongoing consultation work on permitted development rights for small-scale non-domestic turbines, with the consultation closing 10 June 2026.

Recent Industry Developments

- June 2026: RWE completed installation of all 100 turbines at its 1.4 GW Sofia offshore wind farm. The milestone de-risks the construction schedule for one of the UK’s largest projects and tightens demand planning for installation vessels and commissioning resources across the wider offshore pipeline.

- May 2026: The Department for Energy Security and Net Zero granted development consent for the 1 GW North Falls offshore wind farm, a joint project involving RWE and SSE Renewables. The consent decision advances a utility-scale project into the bankable delivery stage and reinforces the role of large consenting outcomes in keeping the UK offshore build schedule moving.

- May 2025: Ørsted discontinued the Hornsea 4 offshore wind project in its current form, citing increased supply-chain costs, higher interest rates, and execution risk, with expected breakaway costs of DKK 3.5 to 4.5 billion. The decision highlighted strike-price and cost-of-capital sensitivity for very large offshore schemes and sharpened the market focus on auction design, supply-chain resilience, and contract structures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers wind power in the United Kingdom, measured in installed wind capacity. We track additions and retirements through the total operating gigawatts (GW), split across onshore and offshore wind.

Scope exclusions: it does not count broader renewable generation assets outside wind, and it does not treat electricity price movements as the market itself.

Segmentation Overview

- By Location

- On-shore

- Off-shore

- By Turbine Capacity

- Up to 3 MW

- 3 to 6 MW

- Above 6 MW

- By Application

- Utility-scale

- Commercial and Industrial

- Community Projects

- By Component (Qualitative Analysis)

- Nacelle/Turbine

- Blade

- Tower

- Generator and Gearbox

- Balance-of-System

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base on UK wind buildout and operations, so the capacity series stays consistent year to year. We mainly used public datasets such as UK government energy statistics and planning releases, National Grid ESO publications, renewable obligation and contract award disclosures, and trade association dashboards that track offshore and onshore project activity.

Next, the capacity timeline was cross-checked with project announcements, annual reports, and investor presentations to confirm commissioning dates, repowering events, and known decommissioning risk. Where public sources were not granular enough, we used a paid subscription for company financials and intelligence selectively to clarify ownership changes and project status. We also referenced a patent database at a high level to sanity check technology shifts (for example, larger turbine ratings). This list is illustrative only, and many other public sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary checks were used to pressure-test what desk sources cannot fully explain, especially the timing of offshore commissioning, curtailment constraints, and how turbine upsizing is changing capacity additions. We spoke with a mix of developers, EPC and service providers, and grid and industry experts across the UK. After the calls, we adjusted assumptions where multiple interviews pointed to the same operational reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | |

| Mid tier: 53% | Functional/Unit leaders: 35% | |

| Smaller Players: 21% | Managers: 51% |

Market-Sizing & Forecasting

Sizing is built from a top-down reconstruction of the UK wind capacity base, where annual commissioning, repowering, and retirements are applied to reach the installed total for each year. Only after the operating base was made internally consistent were segment splits applied, so the location mix (onshore versus offshore), turbine rating bands, and application mapping do not drift away from the total.

Key model inputs include published capacity additions, project pipeline milestones (lease awards, final investment decision signals, and expected grid connection dates), typical turbine nameplate ratings by installation year, and observed repowering patterns in mature onshore sites. We also used constraints that matter in the UK, such as grid connection readiness, offshore construction windows, and known permitting lead times, to prevent unrealistically smooth growth curves.

For forecasting, scenario analysis was used, with a central case supported by expert consensus on delivery timing and a slower and faster case that mainly flex offshore commissioning slippage and repowering pace. Bottom-up approximations were used as a cross-check, where sampled project lists and typical MW per project were rolled up and compared with the top-down totals. Gaps were handled by applying conservative carry-over rules for projects that were delayed but still active in the pipeline.

Data Validation & Update Cycle

Outputs are validated through stepwise checks against independent signals, such as whether implied annual additions align with known auction outcomes, construction activity, and grid connection progress. If a year shows an unusual jump, it is reviewed again, and follow-up calls are triggered when the variance cannot be explained by a visible commissioning event or a repowering wave.

Before sign-off, a second analyst reviews the main assumptions and the math to catch input overlap, missing retirements, or double counting between onshore and offshore. The report is refreshed annually, and interim updates are made when major auctions, policy changes, or large project delays materially shift the forward pipeline. Right before delivery, we do a final sweep so the newest public releases are reflected in the current view.

Mordor Intelligence's United Kingdom Wind Energy Market Size Versus Other Published Estimates

Different sources often show different market sizes for UK wind because some treat the market as installed capacity, while others convert activity into revenue using their own price and service boundaries. Even when the year is the same, the total can shift based on whether late-year commissioning is captured, and whether the estimate is kept in capacity terms or translated into USD.

A common gap driver is refresh cadence and currency timing, since large offshore projects can move in or out of the counted year, and USD conversions can swing totals if an average annual rate is used. Another driver is ASP logic, where some estimates blend equipment, installation, and long-term O&M into one value, while this study stays anchored on the operating GW base and validates year-by-year changes through repeated anomaly checks and re-contacts. The results are then reflected in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 34.50 B (2025) | |

| Global Consultancy A | USD 39.30 B (2024) | The figure is presented as a USD value that appears to bundle multiple cost pools (equipment, installation, and services), so the total depends heavily on assumed ASP progression and the exchange rate window used for conversion. |

| Industry Publisher B | USD 38.30 B (2024) | This approach is described as a broader activity-based value estimate including design, production, installation, and maintenance, which can pull in spending beyond the operating capacity base and can be sensitive to how pipeline timing is refreshed. |

Across the three figures, the spread is mostly explained by whether the market is treated as installed capacity or converted into a spending-based USD total, and by how often late project timing changes are incorporated. By keeping the annual capacity base consistent first and only then applying splits and checks, our sizing stays traceable to clear build and operating signals that can be re-tested each refresh.

Key Questions Answered in the Report

How large is installed capacity today?

Installed capacity will reach 39.69 GW in 2026 and is forecast to 79.94 GW by 2031.

What CAGR is expected through 2031?

Capacity is projected to grow at 15.04% between 2026 and 2031.

Which segment expands fastest?

Offshore wind leads with a 20.18% CAGR thanks to ScotWind and Celtic Sea projects.

Why are larger turbines preferred?

Units above 6 MW cut balance-of-plant costs and dominate 74.42% of 2025 installations.

What key policy supports revenue?

The inflation-indexed CfD scheme locks in price floors and lowers investment risk.

Which region leads future pipeline?

Scotland holds more than 39.75% of the development queue due to ScotWind leases.

Page last updated on: