Steam Autoclaves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

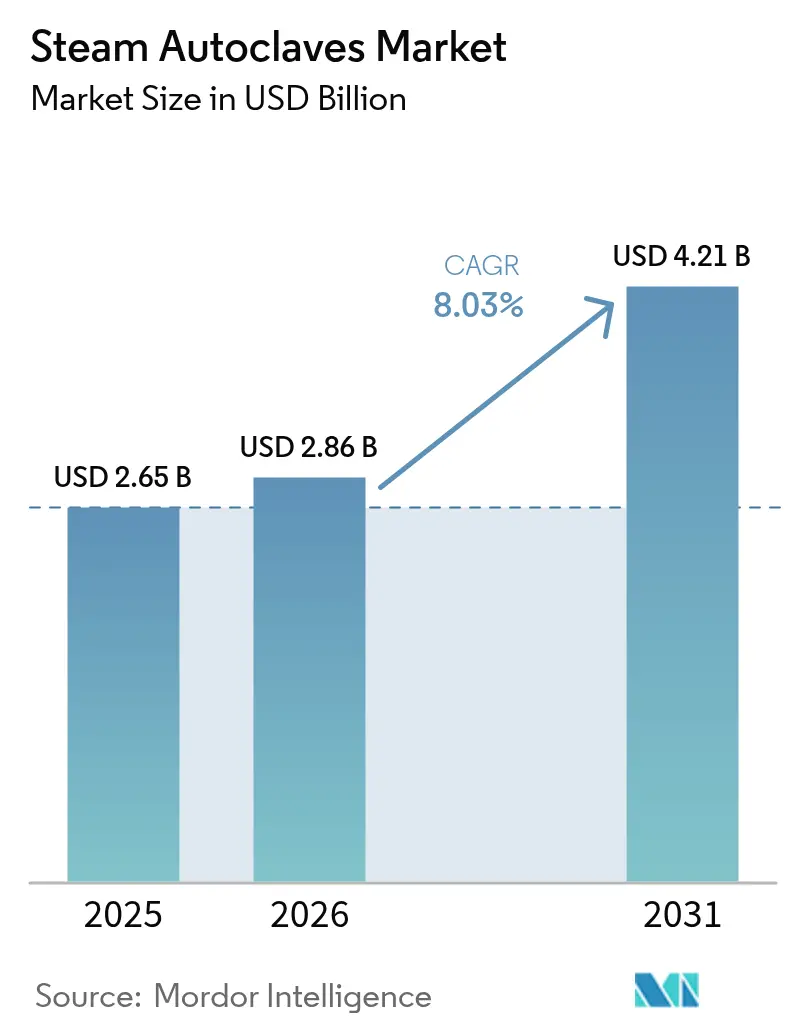

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 4.21 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

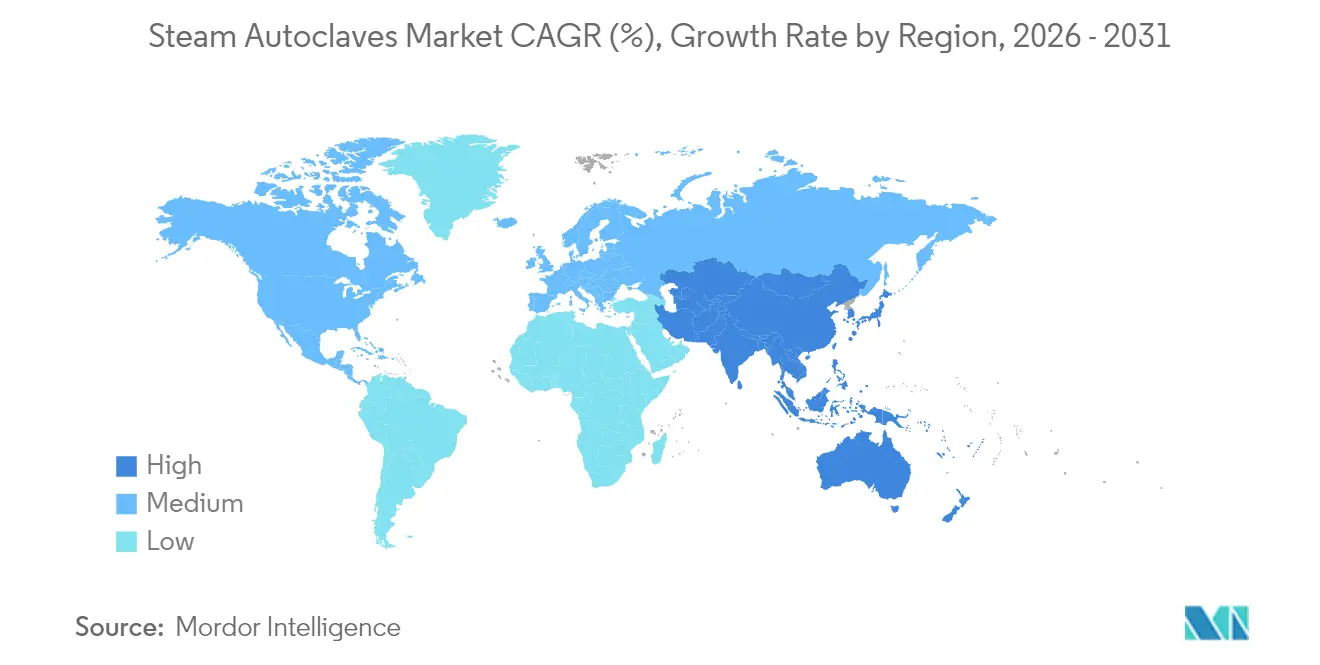

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

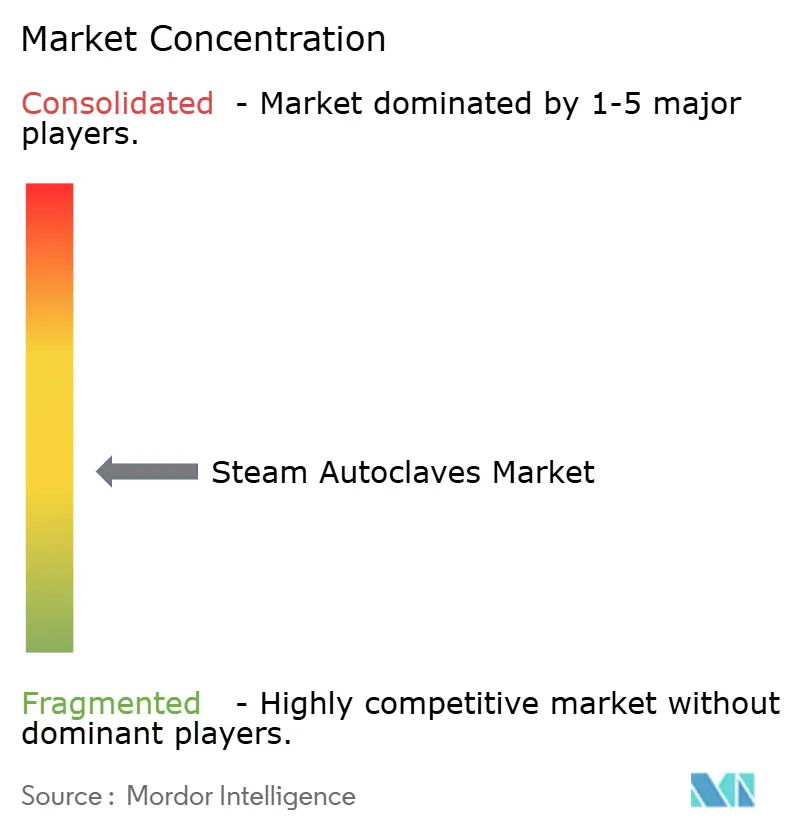

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Steam Autoclaves Market Analysis by Mordor Intelligence

The steam autoclaves market size is expected to grow from USD 2.65 billion in 2025 to USD 2.86 billion in 2026 and is forecast to reach USD 4.21 billion by 2031 at 8.03% CAGR over 2026-2031. Rising infection‐control requirements, tightening emissions rules for ethylene oxide, and the growing urgency to contain healthcare-associated infections are keeping capital expenditure on steam sterilization resilient, even as health systems weigh cost and sustainability trade-offs. North American hospitals continue to refresh their fleets in line with accreditation cycles, while Asia-Pacific providers accelerate first-time installations in response to infrastructure expansion and medical device manufacturing growth. Regulatory shifts—such as the U.S. FDA’s alignment of quality system rules with ISO 13485 and the EU’s GMP Annex 1 update—favour digitally connected units that automate validation and record‐keeping, spurring premium segment demand. Concurrently, vendors are redesigning chambers and cycles to curb water and power usage, appealing to buyers intent on meeting decarbonisation targets without compromising sterilisation efficacy.

Key Report Takeaways

- By product type, vertical units led with 41.95% of steam autoclaves market share in 2025; table-top/benchtop models are projected to expand at a 9.94% CAGR through 2031.

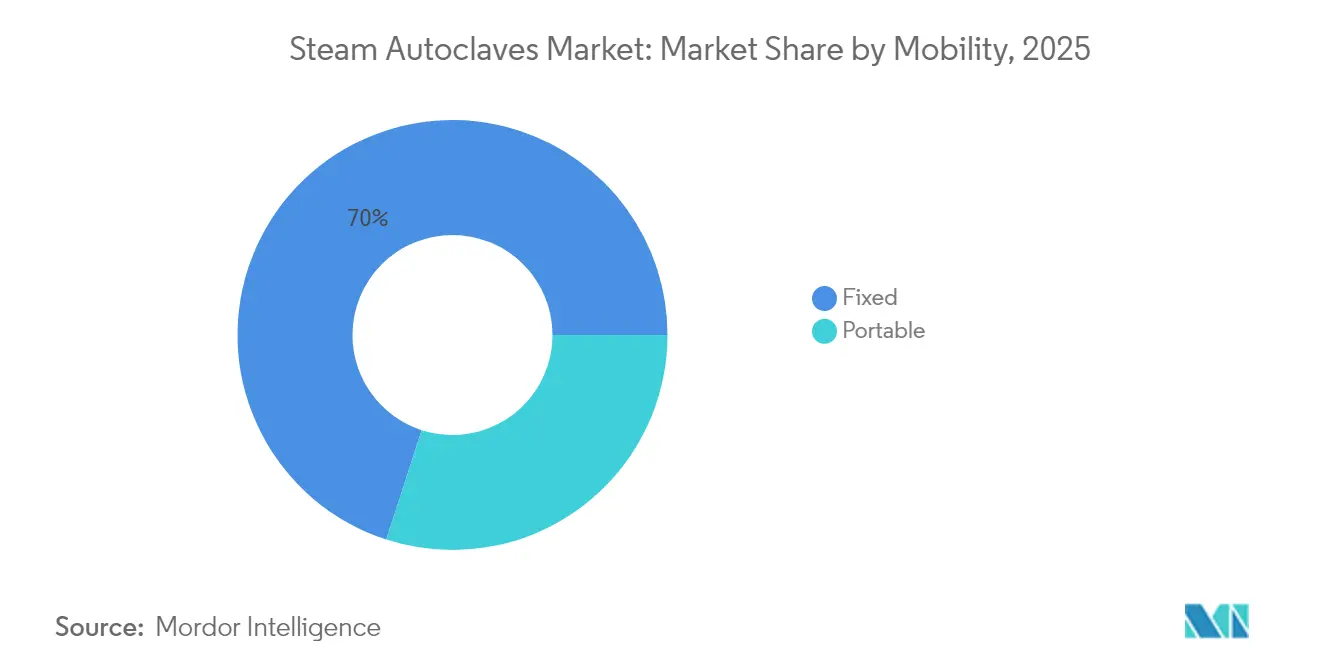

- By mobility, floor-standing systems accounted for 70.02% of steam autoclaves market size in 2025, whereas portable units show the fastest 12.31% CAGR outlook.

- By sterilisation technology, gravity displacement held 46.05% of steam autoclaves market size in 2025, while pre-vacuum technology is set to grow at a 10.66% CAGR.

- By end user, hospitals and clinics represented 54.30% of steam autoclaves market share in 2025, yet dental facilities are advancing at a 10.43% CAGR.

- By geography, North America commanded 34.55% of revenue in 2025; Asia-Pacific is forecast to climb at an 11.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Steam Autoclaves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Hospital-Acquired Infections | +1.8% | Global, with highest impact in North America & Europe | Short term (≤ 2 years) |

| Stringent Infection-Control & Accreditation Norms | +1.5% | Global, led by North America, Europe, followed by APAC | Medium term (2-4 years) |

| Growing Need To Manage Bio-Hazardous / Medical Waste | +1.2% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Shift Toward Point-Of-Use Sterilization In Ambulatory Settings | +0.9% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Emergence Of Energy-Efficient 'Green' Autoclaves | +0.7% | Europe leading, North America & APAC following | Long term (≥ 4 years) |

| Integration Of IoT Sensors For Remote Cycle Validation & Compliance | +0.6% | North America & Europe early adoption, APAC emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hospital-Acquired Infections

Hospitals worldwide still record roughly 1 in 31 inpatients with at least one healthcare-associated infection, sustaining investment in reliable steam cycles that eradicate resistant organisms. Although the CDC noted double-digit declines in MRSA and CLABSI rates between 2022 and 2023, administrators recognise that prevention remains cheaper than treatment, keeping new-build and replacement demand intact across surgical, critical-care and transplant units[1]Centers for Disease Control and Prevention, “Current HAI Progress Report,” cdc.gov. Steam autoclaves deliver rapid, reproducible lethality without chemical residuals, aligning with operating-room turnaround imperatives and environmental, health and safety policies. Suppliers are therefore embedding IoT sensors for automatic cycle tracking, enabling infection-control teams to audit loads in real time and trigger corrective action before breaches escalate. This capability resonates most in tertiary centres where diverse instrument sets require differentiated parameters yet strict chain-of-custody documentation.

Stringent Infection-Control & Accreditation Norms

The FDA’s 2025 update to 21 CFR 880.6880 formalised the need for integrated monitoring and electronic records in steam sterilizers, pushing facilities to phase out legacy equipment lacking automated data export. In Europe, Annex 1 places explicit emphasis on contamination-control strategies and quality-risk management that many providers meet by deploying autoclaves with closed-loop sensors and validated leak-rate testing. Dental practices face comparable scrutiny; CDC guidance issued in late 2024 mandates weekly biological monitoring, a requirement easier to satisfy with benchtop units offering built-in printouts or cloud reporting. Comparable regimes in Canada, Japan and Australia mirror these expectations, creating a coordinated global pull for digitally native platforms capable of harmonised audit trails. Resulting procurement cycles favour manufacturers with cross-regional regulatory teams and post-installation service networks that sustain compliance across a device’s 15-year life.

Growing Need to Manage Bio-Hazardous Medical Waste

The U.S. EPA now obliges commercial sterilizers using ≥ 100 lbs of ethylene oxide annually to achieve 99.99% emission reduction, accelerating migration toward on-site thermal treatment in hospitals and reference labs[2]U.S. Environmental Protection Agency, “National Emission Standards…,” federalregister.gov. California’s Medical Waste Management Act similarly stresses pre-disposal treatment, with steam autoclaving listed as a primary method to render waste non-infectious. On-premise autoclaves cut transportation risks, lower disposal costs by shrinking waste volume through steam-mediated cell lysis, and help organisations meet decarbonisation goals by avoiding incinerators’ higher greenhouse footprint. Manufacturers are capitalising by offering waste-dedicated chambers equipped with shredders and condensate filtration, appealing to life-science campuses and teaching hospitals seeking turnkey “treat-and-toss” solutions. Demand is particularly acute in North America and Western Europe, where environmental services departments shoulder compliance penalties for untreated waste interceptions.

Shift Toward Point-of-Use Sterilisation in Ambulatory Settings

Ambulatory surgery centres and dental clinics value fast cycle times that enable same-day instrument reuse without couriering to central sterile departments. Advances in microprocessor control, compact vacuum pumps and water-recirculation loops permit benchtop autoclaves to complete wrapped loads in under 15 minutes, facilitating chairside workflows. Portable units weighing < 25 kg are also gaining adoption in home-health programmes and military field hospitals that need rugged, low-maintenance sterilisers operable on limited power. Traceability software embedded in these devices supports barcode scanning, bridging documentation gaps between decentralised care sites and central quality teams. Consequently, table-top models represent the fastest expanding slice of the steam autoclaves market, with manufacturers bundling leasing plans that ease capital hurdles for small practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs Of Large Units | -1.3% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Growing Adoption Of Disposable Single-Use Instruments | -0.8% | North America & Europe leading, APAC following | Medium term (2-4 years) |

| Space & Utility Constraints In Resource-Limited Clinics | -0.6% | Emerging markets in APAC, MEA, Latin America | Short term (≤ 2 years) |

| Complex Qualification / Re-Validation Documentation Burden | -0.4% | Global, with highest impact in regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Large Units

Floor-standing, double-door autoclaves can command list prices above USD 250,000, excluding site upgrades for electrical, steam and water utilities, a hurdle for resource-strained public hospitals. Annual upkeep—ranging from gasket replacement to chamber re-qualification—adds recurring cost, prompting many facilities in Latin America, the Middle East and parts of Southeast Asia to defer purchases or opt for outsourced reprocessing. Energy and water data further complicate budgeting: a single 400-litre jacketed unit may consume 60 gallons per cycle, challenging sustainability pledges as providers track Scope 1 and Scope 2 emissions. Vendors respond with modular chamber designs and heat-recovery systems, yet payback periods remain lengthy, restraining uptake in price-sensitive territories.

Growing Adoption of Disposable Single-Use Instruments

Minimally invasive surgery and interventional cardiology increasingly rely on pre-sterilised, single-patient disposables that bypass reprocessing altogether[3]European Commission, “Reprocessing of Medical Devices,” health.ec.europa.eu. EU rules now hold reprocessors to the same requirements as original manufacturers, discouraging hospitals from in-house reuse and nudging surgeons toward throw-away kits. While disposables raise waste-management challenges, they eliminate sterility failures linked to complex lumens and hinged joints. Consequently, demand growth for small-batch hospital autoclaves moderates in orthopaedics and ophthalmology, even as total procedure volumes rise. Manufacturers target mitigation by emphasising hybrid models—sterilising reusable core instruments while single-use consumables handle the most intricate geometries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vertical Units Lead Market Share

Vertical units accounted for 41.95% of steam autoclaves market share in 2025, confirming their popularity in theatres and labs that value narrow footprints and ergonomic top loading. Rising refurbishment of secondary hospitals in Europe and India maintains baseline demand, as these vertical chambers sterilise gowns, handpieces and culture media without extensive plumbing. Table-top models, in contrast, are set to post a 9.94% CAGR through 2031, fuelled by ambulatory centres installing point-of-care sterilisation to shorten instrument turnaround. The CDC’s 2024 dental guidance reinforced weekly biological monitoring, encouraging clinics to replace ageing heat-only sterilisers with automated benchtop steam units that document each cycle.

Manufacturers differentiate through cycle versatility and intuitiveness. Touch-screen HMIs, pre-programmed lumened-device cycles and cloud integration have become standard, while optional water-savings kits and HEPA exhaust filters add sustainability. Horizontal floor-standing units still underpin high-throughput central sterile departments, yet their uptake is tempered by space constraints and the -1.31% CAGR drag associated with acquisition and maintenance costs. Nonetheless, orthopaedic centres performing back-to-back joint replacements will continue ordering 600-litre chambers capable of handling large trays, shielding this niche from displacement.

By Sterilisation Technology: Gravity Displacement Maintains Leadership

Gravity displacement processes held 46.05% of steam autoclaves market size in 2025 thanks to simplicity, low capital cost and minimal maintenance. In small clinics, gravity cycles remain adequate for solid instruments and liquid media, especially where budgets rule out vacuum pumps. Yet complexity in surgical devices is driving a shift toward pre-vacuum systems that demonstrate a leading 10.66% CAGR. These high-vac units draw air through a series of negative pulses, ensuring steam penetrates lumens and porous wraps, which is essential for robotic instruments and micro-laparoscopes in tertiary hospitals.

Steam-flush pressure pulse (SFPP) chambers serve labs needing rapid turnarounds, cycling loads in under 25 minutes without high-energy vacuum pumps. Meanwhile, pass-through double-door designs address unidirectional workflows between dirty and clean zones, a regulatory requirement in many GMP manufacturing suites. Vendors layer in passive heat recovery and jacket insulation to shrink utility draws by up to 25%, targeting green procurement metrics and life-cycle cost justifications for pre-vacuum installations.

By Mobility: Fixed Units Dominate Despite Portable Growth

Floor-standing models contributed 70.02% of steam autoclaves market size in 2025, supported by integrated central sterile departments where high-capacity, PLC-driven systems align with ISO 11134 validation and HVAC integration. Their robust construction and chamber volumes above 300 litres enable batch processing that keeps operating-room schedules on track. Portable autoclaves, though a modest revenue base, are accelerating at a 12.31% CAGR. Rural outreach programmes, battlefield medicine and veterinary clinics appreciate their plug-and-play utility, 115-volt compatibility and compact design that fits mobile vans.

Field units increasingly adopt lithium-ion battery packs and solar chargers for off-grid sterilisation, while ruggedised casings resist vibration during transport. Manufacturers provide smartphone apps for cycle monitoring, an attractive feature for NGOs auditing infection-control practices in dispersed locations. This convergence of durability and digital oversight strengthens value propositions and ensures that portable categories continue widening their addressable market within the broader steam autoclaves market.

By End User: Hospitals Lead While Dental Grows Fastest

Hospitals and clinics captured 54.30% of steam autoclaves market share in 2025, underpinned by multi-disciplinary instrument needs, large sterile processing departments and mandated accreditation checks. Operating rooms account for the bulk of loads, sterilising basins, forceps and implants several times daily. Dental facilities, however, present the fastest trajectory at a 10.43% CAGR, reflecting increased oral-health coverage and the CDC’s insistence on strict sterilisation documentation in chairside settings. Compact Class B autoclaves with fractionated pre-vacuum cycles suit dental handpieces, driving replacement cycles every 7-10 years.

Pharmaceutical and biotech environments apply steam for terminal sterilisation of vials, stoppers and media. EU Annex 1 pushes for real-time particulate monitoring, spurring investment in validated pass-through autoclaves integrated with cleanrooms. Research institutes demand cycle flexibility to accommodate agar, pipettes and biohazard waste, often specifying cross-linked data logs to prove chain-of-custody. Veterinary hospitals and contract sterilisers emerge as niche adopters, moving up from desktop pressure cookers to programmable units to meet evolving animal-care standards.

Geography Analysis

North America retained the largest revenue share at 34.55% in 2025 thanks to mature replacement cycles, advanced accreditation requirements and rapid adoption of IoT-enabled sterilisation suites. Hospitals continue swapping legacy gravity units for energy-efficient high-vac autoclaves that integrate with central sterile tracking platforms. Federal incentives for sustainable infrastructure also push providers toward water-saving models, cushioning total-cost-of-ownership concerns.

Europe follows closely, yet faces the dual burden of Medical Device Regulation compliance and Brexit-related supply disruptions. Annex 1 and harmonised standards clamp down on manual documentation, driving upgrades to machines with automated load release and Wi-Fi audit trails. Germany, France and the Nordics lead substitution, whereas Eastern European markets still rely on refurbished imports.

Asia-Pacific is the fastest expanding geography, with an 11.42% CAGR projected through 2031. Extensive hospital construction in China and India, coupled with rising domestic device manufacturing, fuels demand for both large central units and portable field models. Government-subsidised health-insurance schemes in Southeast Asia further incentivise clinics to meet infection-control benchmarks. Meanwhile, Middle East and Africa, along with South America, witness steady adoption as private operators open tertiary centres and specialty clinics, although foreign-exchange volatility and import tariffs temper the pace in select economies.

Competitive Landscape

The steam autoclaves market exhibits moderate concentration. Major players collectively command a significant revenue share, benefitting from multi-regional service reach and decades of regulatory expertise. STERIS’s launch of Verafit sterilisation bags in 2024 demonstrates agility in aligning product pipelines with EU Annex 1, differentiating its consumables portfolio. Getinge reported resilient order intake in Q3 2024 despite logistics delays, underscoring robust underlying demand and the strategic importance of diversified manufacturing footprints.

Companies increasingly compete on embedded connectivity, predictive maintenance and cloud dashboards that cut unplanned downtime and facilitate paperless audits. SteelcoBelimed—a joint venture between Miele and Metall Zug—illustrates consolidation aimed at scaling R&D and leveraging complementary channel strengths across Europe, the Americas and Asia. New entrants focus on green‐tech value propositions, such as heat-pump-assisted steam generators promising 30% lower energy draw. Yet capital intensity and certification hurdles restrict rapid share shifts.

Strategic moves include Getinge’s acquisition of Healthmark Industries to broaden consumable lines, and Tuttnauer’s investment in IoT-driven “smart laboratory” platforms that allow real-time load traceability. Vendors also diversify through as-a-service models, wrapping hardware, consumables and data analytics into subscription bundles that smooth cash outflows for hospitals while cementing long-term relationships.

Steam Autoclaves Industry Leaders

TESALYS Group

Astell Scientific

BMM Weston Ltd.

Celitron Medical Technologies

Belimed AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: The Medical Device Coordination Group published updated guidance on legacy device compliance with EU Medical Device Regulation requirements.

- June 2024: Miele finalised the SteelcoBelimed joint venture with Metall Zug, creating four European production hubs for cleaning, disinfection and sterilisation solutions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the steam autoclaves market as all newly manufactured pressure vessels that sterilize medical, dental, laboratory, and bio-hazard loads using saturated steam at temperatures above 121 deg C, supplied either as gravity-displacement or pre-vacuum systems and sold to end-users worldwide.

Scope Exclusions: dry-heat sterilizers, ethylene-oxide chambers, and benchtop gadgets marketed strictly for home tattoo or beauty uses are not counted.

Segmentation Overview

- By Product Type

- Vertical Steam Autoclaves

- Horizontal Steam Autoclaves

- Table-top / Benchtop Autoclaves

- Large-capacity Floor-standing Autoclaves

- By Sterilization Technology

- Gravity Displacement

- Pre-vacuum (High-vac)

- Steam-Flush Pressure Pulse (SFPP)

- Double-door Pass-through

- By Mobility

- Fixed / Floor-standing

- Portable

- By End User

- Hospitals & Clinics

- Pharmaceutical & Biotech Companies

- Research & Academic Institutes

- Dental Facilities

- Veterinary Clinics

- Contract Sterilization Service Providers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infection-control nurses, biomedical engineers, procurement heads, and regional distributors across North America, Europe, Asia-Pacific, and the Gulf. Conversations tested average selling prices, cycle counts per bed, and expected life-span shifts after recent energy-efficiency upgrades, filling gaps present in desk findings.

Desk Research

We began with public datasets such as WHO hospital bed density tables, CDC and ECDC surgical procedure statistics, UN Comtrade pressure-vessel trade codes, and FDA 510(k) device clearances, which gave us baseline unit flows and regulatory cadence. Trade association releases (Global CSSD Forum, Dental Trade Alliance), peer-reviewed journals on infection control, and national procurement portals enriched price corridors and replacement cycles. Paid aggregators that Mordor subscribes to, including D&B Hoovers for company revenues and Dow Jones Factiva for shipment news, complemented open data. The sources mentioned illustrate the range; many additional materials were reviewed for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down reconstruction converts procedure volumes and medical-waste output into demand pools, which are then filtered by sterilization penetration rates and typical autoclave capacity to yield annual unit needs. Results are corroborated through selective bottom-up checks, sampled supplier revenues, and channel inventory to fine-tune totals. Key model inputs include: (1) inpatient surgical episodes per 1,000 population, (2) CSSD installation rates in new hospitals, (3) average replacement cycle length in years, (4) weighted ASP trends by chamber volume, and (5) stainless-steel cost index that influences price drift. A multivariate regression captures how these drivers interact, and scenario analysis stress-tests currency swings or sudden regulation changes.

Data Validation & Update Cycle

Outputs pass variance screens against historical shipment patterns and independent import data before team review. We refresh every twelve months and trigger interim revisions for material recalls, trade disruptions, or regulation changes. A final analyst pass ensures clients receive the most current view.

Why Our Steam Autoclaves Baseline Commands Reliability

Published values often diverge because firms pick contrasting scopes, price bases, and refresh speeds.

Key gap drivers include inclusion of allied sterilizers, exclusion of high-capacity CSSD fleets, currency conversion timing, and whether retail or ex-factory prices are used. Mordor reports current-year factory-gate revenue and a global scope that aligns with device regulatory codes, then reconciles with bottom-up supplier signals, which many studies omit.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.65 B (2025) | Mordor Intelligence | - |

| USD 3.10 B (2024) | Global Consultancy A | Counts adjacent low-pressure sterilizers and applies retail ASPs |

| USD 1.25 B (2023) | Trade Journal B | Excludes hospital CSSD installations and limits coverage to five regions |

| USD 1.80 B (2025) | Industry Association C | Uses supplier shipments only, without aftermarket price adjustments |

Taken together, the comparison shows why our disciplined scope setting, dual-path modelling, and yearly refresh deliver a balanced, transparent baseline that decision-makers can trace back to tangible variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the steam autoclaves market by 2031?

The market is forecast to reach USD 4.21 billion by 2031, growing at an 8.03% CAGR.

Which product category holds the largest revenue share today?

Vertical units lead with 41.95% of steam autoclaves market share as of 2025.

Why are dental facilities seen as a high-growth end-user segment?

Stricter CDC sterilisation guidelines and rising dental care utilisation drive a 10.43% CAGR for dental settings.

Which region shows the fastest market expansion?

Asia-Pacific is expected to post an 11.42% CAGR through 2031 due to large-scale healthcare infrastructure investments.

How do environmental regulations influence purchasing decisions?

EPA limits on ethylene oxide emissions and hospital decarbonisation goals push facilities toward energy-efficient steam autoclaves.

What technological features are hospitals prioritising in new autoclave purchases?

IoT integration for cycle tracking, automated documentation, and energy-saving designs are key purchasing criteria.

Page last updated on: