Europe Sharps Containers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

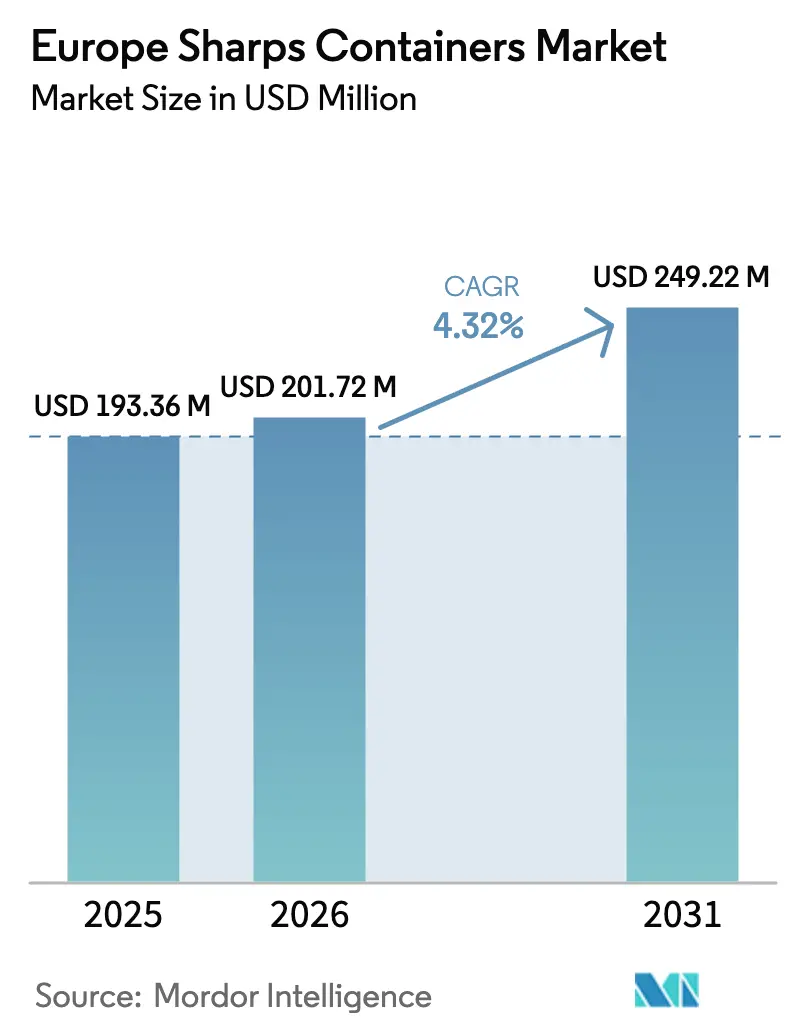

| Base Year Market Size (2025) | USD 193.36 Million |

| Market Size (2026) | USD 201.72 Million |

| Market Size (2031) | USD 249.22 Million |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

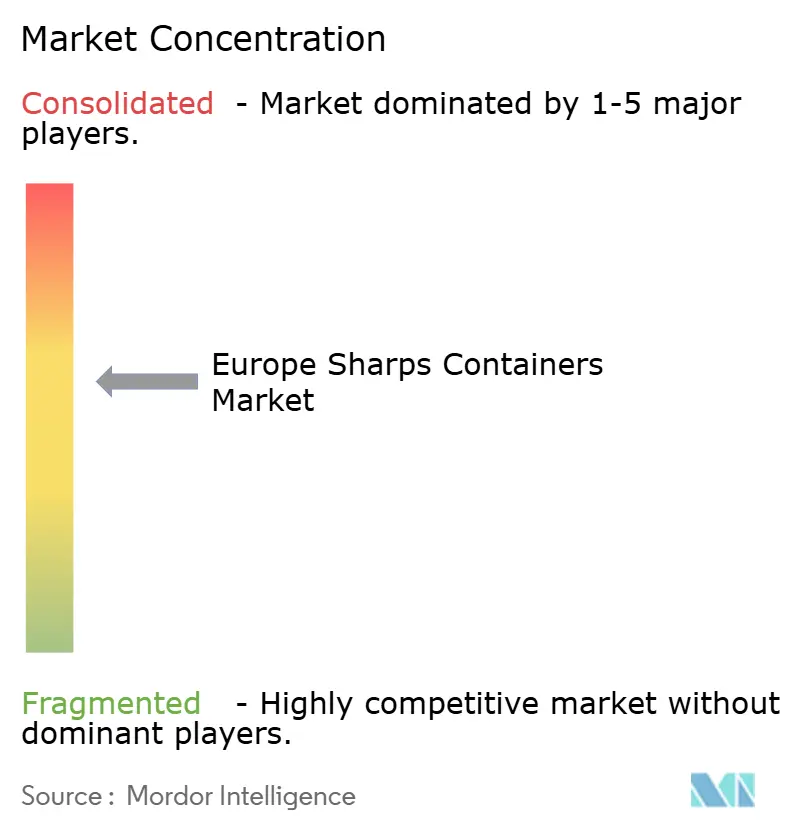

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Sharps Containers Market Analysis by Mordor Intelligence

The Europe sharps containers market size is expected to grow from USD 193.36 million in 2025 to USD 201.72 million in 2026 and is forecast to reach USD 249.22 million by 2031 at 4.32% CAGR over 2026-2031. Demand is guided by tighter EU circular-economy directives, hospital decarbonization roadmaps, and rising surgical throughput that together press buyers to reconsider long-standing single-use habits. Suppliers able to prove lower lifecycle emissions, automated compliance reporting, and resilient local supply chains gain traction as hospitals translate net-zero commitments into procurement scorecards. Supply insecurity linked to polymer levies and plastics-tax cost pass-throughs adds to the urgency of sourcing containers with high recycled content or reusable architectures. The Europe sharps containers market therefore evolves from a pure cost-plus commodity arena toward a value-based purchasing environment that ranks sustainability metrics alongside safety performance.

Key Report Takeaways

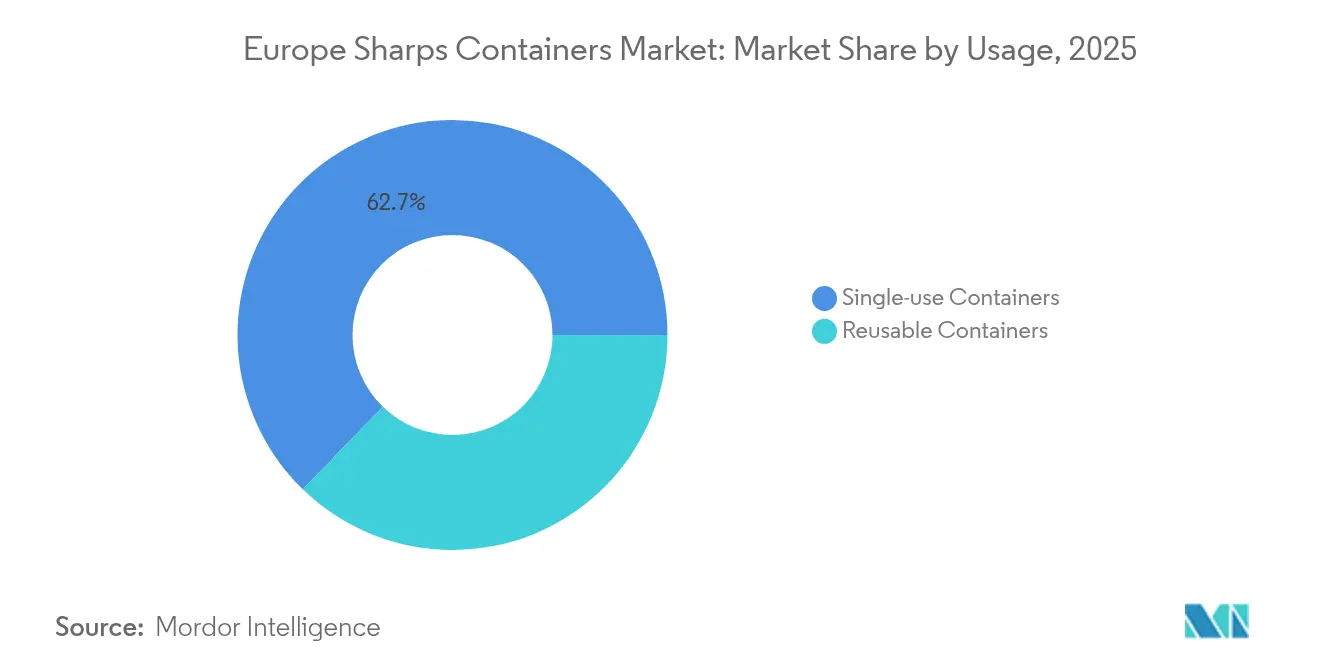

- By usage, single-use containers held 62.74% of Europe sharps containers market share in 2025 while reusable units are projected to grow 8.22% CAGR to 2031.

- By container type, patient-room formats led with 41.10% revenue share in 2025; multipurpose designs record the fastest expansion at 7.46% CAGR through 2031.

- By container size, 2-4 gallon products accounted for 46.05% of Europe sharps containers market size in 2025, whereas 4-8 gallon models are advancing at a 7.43% CAGR.

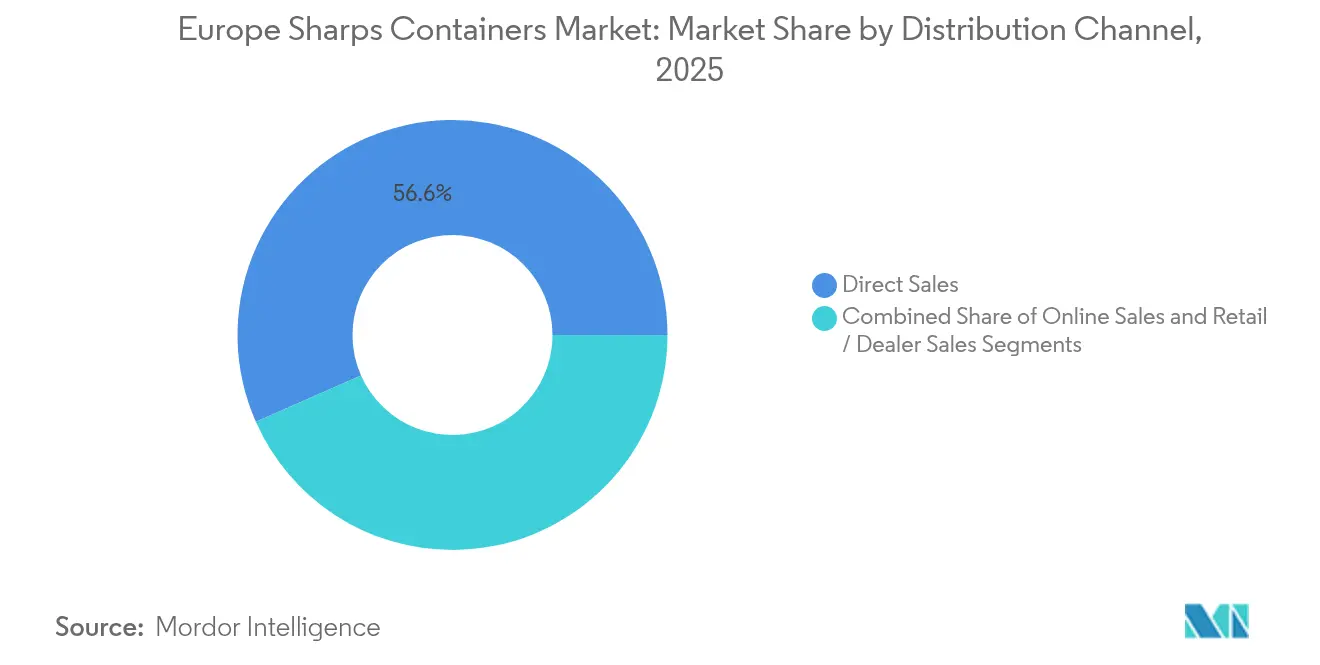

- By distribution channel, direct sales contributed 56.62% revenue in 2025, while online procurement is set to accelerate at 9.18% CAGR.

- By end-user, hospitals generated 59.48% demand in 2025, whereas home-healthcare settings are expanding at an 10.94% CAGR.

- By country, Germany commanded 39.72% share in 2025, and Spain is forecast to rise at 8.07% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on sharps containers market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Sharps Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU circular-economy mandates boost reusables | +1.2% | EU-wide, strongest in Germany, Netherlands, Denmark | Medium term (2-4 years) |

| Growth in surgical volumes & outpatient care | +0.9% | Germany, France, UK | Short term (≤ 2 years) |

| Hospital decarbonization/net-zero targets | +0.8% | UK, Netherlands, Portugal; expanding EU-wide | Long term (≥ 4 years) |

| Stricter infection-control regulations | +0.6% | EU-wide, tougher in CEE nations | Short term (≤ 2 years) |

| Smart IoT inventory tracking | +0.5% | Germany, UK, Netherlands, Nordics | Medium term (2-4 years) |

| Re-shoring of container moulding | +0.3% | Germany, France, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Circular-Economy Mandates Boost Reusable Sharps Demand

European legislation now ranks reuse above recycling for medical waste, moving hospital buyers toward multi-cycle container fleets that can survive 500-plus sterilization cycles without compromising puncture resistance. Hospitals evaluating five-year depreciation models validate that reusable fleets cut total waste mass by over 80% and lower annual procurement spending even after factoring EUR-denominated wash-line operating costs. Denmark’s 2025 rules that authorize single-use device reprocessing underscore a continental tilt toward circular solutions, prompting suppliers to publish verified lifecycle assessments and material traceability data. Procurement teams in Germany and the Netherlands already allocate weighted tender scores to products demonstrating quantifiable waste avoidance. As extended producer-responsibility schemes tighten, reusable sharps containers shift from optional green initiatives to mandatory compliance tools.

Growth in Surgical Volumes & Outpatient Clinics

Elective surgeries continue their migration from inpatient theatres to same-day facilities, with ambulatory surgery centres reporting double-digit procedure growth. Every additional procedure suite seeds demand for multiple container points—pre-op, intra-op, PACU, and ancillary labs. Parallel expansion of outpatient parenteral antimicrobial therapy creates community drop-off nodes that diversify supply footprints beyond hospital walls. Concentrated growth in Germany, France, and the UK enables manufacturers to cluster regional warehouses, trimming lead times and lowering logistics emissions. The Europe sharps containers market benefits directly as every incremental surgery yields predictable sharps throughput and shorter container replacement cycles[1]Health Industry Distributors Association, “Ambulatory Surgery Center Market Report,” hida.org.

Hospital Decarbonization/Net-Zero Targets

Legal net-zero pledges convert procurement teams into carbon accountants. NHS modelling shows reusable sharps fleets shrink container-related emissions by up to 56% and cut budget outlays by 30-59% over seven years. Similar audits in Portugal and the Netherlands produce parallel findings as Scope 3 emissions dominate healthcare footprints. RFPs now request cradle-to-grave carbon metrics, and vendors unable to substantiate reductions risk delisting. Strategic alliances with sterilization service partners help hospitals overcome CapEx hurdles while still scoring emissions wins. These dynamics elevate Europe sharps containers market providers that pair hardware with data-rich sustainability dashboards[2]Health Care Without Harm, “Operation Zero,” europe.noharm.org.

Stricter Infection-Control Regulations

Council Directive 2010/32/EU mandates sharps-injury prevention, pushing facilities to swap aging bins for models with reinforced sidewalls, overfill windows, and one-handed closures. ECDC surveillance data linking container integrity to lower contamination incidents accelerates replacement demand, especially across Central and Eastern Europe where hospital modernization funds are earmarked for infection-control upgrades. Standards convergence forces suppliers to maintain multi-country conformity dossiers, raising entry barriers for low-cost imports. Compliance upgrades bolster the premium segment of the Europe sharps containers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insufficient staff training on waste rules | −0.7% | CEE & rural EU facilities | Short term (≤ 2 years) |

| High CapEx for reusable fleets & wash-lines | −1.1% | Smaller hospitals across EU | Medium term (2-4 years) |

| EU plastics-tax inflating polypropylene cost | −0.9% | EU-wide, notable in Spain, Italy, Germany | Short term (≤ 2 years) |

| Limited third-party sterilization capacity | −0.4% | Poland, Czechia, Hungary, Romania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Insufficient Staff Training on Hazardous-Waste Protocols

Many rural clinics still rely on ad-hoc sharps segregation that undermines container utilization efficiency. Undertrained staff frequently overfill bins, heightening needlestick risks and triggering premature disposal cycles that inflate costs. EU-funded training programs aim to raise compliance, yet language diversity and staff turnover slow progress. Until coaching penetrates deeper, uptake of advanced container features may lag in these zones, dampening the Europe sharps containers market expansion potential.

High CapEx for Reusable Fleet & Wash-Lines

Full conversion to reusable systems can reach EUR 500,000 for large campuses, a figure beyond the capital envelopes of mid-tier public hospitals. Budget committees often prioritize diagnostic equipment over waste infrastructure, pushing reusable adoption into phased pilots that temper short-term volumes. Leasing models and shared sterilization hubs emerge to bridge the affordability gap, yet contract complexity still delays approvals in several member states. This CapEx hurdle remains the single largest drag on Europe sharps containers market acceleration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage: Reusables Challenge Single-Use Dominance

Reusable containers carved an 8.22% CAGR through 2031 while single-use units still anchor the Europe sharps containers market at 62.74% in 2025. Carbon-footprint audits, plastics levies, and hospital ESG scorecards combine to tilt tenders toward reusable propositions, particularly among Germany’s university hospitals and Dutch green-hospital pilots. Budget-constrained rural facilities, however, cling to single-use simplicity, perpetuating a dual-speed pattern that will persist until leasing and centralized washing services mature. Manufacturers that bundle containers, logistics, and sterilization under service-level agreements mitigate CapEx fears and hasten reusable penetration. Lifecycle total-cost models predict breakeven after 18–24 months in high-volume sites, but up to five years for sub-200-bed hospitals. The Europe sharps containers market therefore exhibits a widening performance gap between institutions able to leverage scale and those locked into legacy workflow habits.

Secondary infection-control audits still favour single-use bins for ultra-high-risk wards such as transplant units where zero contamination tolerance guides policy. Yet reusable vendors counter with closed-latch designs rated for 1,500 wash cycles and validated sterility indicators. Denmark’s reprocessing precedent signals future rule harmonization that could compress the residual single-use niche further. Continuous R&D around biopolymers reinforces the economic narrative that reusables will eventually eclipse disposable alternatives.

By Container Type: Multipurpose Units Gain Traction

Patient-room models generated 41.10% revenue in 2025, reflecting their role as default point-of-care solution across wards, clinics, and diagnostic bays. Multipurpose containers, engineered to accept sharps, soft infectious, and barber waste, are climbing 7.46% CAGR as hospitals consolidate waste streams to cut labour and bin-swap frequency. Workflow mapping in Spanish ambulatory centres shows staff time savings of 22% after switching to multipurpose bins, freeing nursing hours for direct patient care. The Europe sharps containers market thus rewards suppliers offering modular inserts and colour-coded apertures that maintain segregation compliance while lowering SKU counts. IoT sensors now embed seamlessly across all container types, but adoption is highest in multipurpose lines where mixed waste fractions require tighter fill-level visibility to avoid cross-contamination.

Design innovation focuses on universal mounting rails, pivot lids that suit high-acuity zones, and polymer blends that retain puncture strength after multiple autoclave cycles. Phlebotomy-specific mini-bins remain essential in outpatient labs yet contribute limited incremental growth. The technology frontier gravitates toward patient-engagement features such as QR-coded recycling instructions in home-dialysis settings, signalling future consumer-facing pivots for the Europe sharps containers market.

By Container Size: Larger Units Drive Efficiency

Containers in the 2-4 gallon class hold 46.05% share thanks to balanced ergonomics, but 4-8 gallon formats post a 7.43% CAGR as hospitals extend replacement intervals to offset nurse shortages and plastics-tax surcharges. Lifecycle studies at UK acute trusts found that shifting 60% of wards to 6-gallon smart bins cut annual haulage trips by 28% and saved 14 tCO₂e. Larger units now feature moulded grip handles and foot-pedal lids that neutralize historic concerns over manual-handling injuries. Smaller 1-2 gallon containers hold niches in community infusion and paediatric home-care where space constraints override cost-per-volume metrics. As carbon accounting deepens, container-size decisions increasingly factor freight emissions per litre of sharps capacity, elevating demand for roomy bins backed by detailed cradle-to-gate footprint disclosures. This dynamic feeds sustained growth momentum within the Europe sharps containers market.

By Distribution Channel: Digital Transformation Accelerates

Direct selling retains 56.62% value share, safeguarded by complex tenders that bundle container hardware, pickup contracts, and compliance software. Online platforms, however, accelerate at 9.18% CAGR as post-pandemic procurement teams embrace e-catalogues and e-signature contract flows. Sophisticated ERP plug-ins let hospitals auto-replenish stock based on IoT sensor data, linking usage analytics to punch-out ordering pages. Vendors that curate transparent price grids, instant compliance certificates, and self-service configurators capture a widening slice of Europe sharps containers market growth. Dealer networks persist among small private clinics that value local demo support and low minimum order quantities, yet their aggregate share edges downward amid digital migration. Platform consolidation is likely as hospital groups converge on preferred marketplaces that integrate green-procurement filters evaluating recycled content percentages.

By End-User: Home Healthcare Drives Growth

Hospitals still account for 59.48% of 2025 demand, anchoring the Europe sharps containers market through sheer waste volume and regulatory oversight. Yet home-healthcare registers 10.94% CAGR as ageing demographics push insulin therapy, biologic self-injections, and outpatient dialysis into domestic settings. Safety regulations are gradually broadening to mandate puncture-proof sharps disposal in private residences, prompting insurers to bundle container kits with drug-delivery devices. Container makers adapt by shrinking form factors and adding child-resistant lids, while logistics partners pilot postal-return schemes to comply with ADR transport rules. Ambulatory surgery centres and group practices form a stable mid-tier, benefitting from rising day-surgery caseload without the nursing intensity of inpatient wards. Collectively these shifts diversify demand, compelling suppliers to service a spectrum of volume profiles from multi-tonne hospital accounts to single-box monthly home shipments.

Geography Analysis

Germany leads the Europe sharps containers market at 39.72% share due to dense hospital infrastructure, robust medical-device manufacturing, and early sustainability adoption. Federal plastics levies since 2024 raise material costs, nudging hospitals to embrace reusable fleets backed by domestic wash-line operators that shorten transport distances. Public procurement frameworks rank carbon credentials alongside unit pricing, advantaging suppliers able to supply audited lifecycle assessments. Local moulding capacity around Baden-Württemberg shelters buyers from global freight volatility, reinforcing Germany’s regional supply security.

The United Kingdom exhibits mature demand where NHS purchasing templates standardize specifications nationwide. Binding net-zero law accelerates uptake of reusable containers with verified 50% plus emissions reductions. The 2024 Plastic Packaging Tax raises costs for virgin-polymer bins, further tilting selection toward high recycled-content or multi-cycle products. Post-Brexit regulatory divergence allows niche designs optimized for UK carriage regulations, creating modest barriers for continental exporters without localized compliance teams. IoT pilots under NHS Supply Chain’s Scan4Safety program elevate interest in sensor-equipped sharps containers and spur vendor investments in GS1 standard labelling.

France and Italy contribute steady volumes, driven by surgical-capacity expansion. France’s extensive ambulatory network sustains container demand across distributed day-surgery sites, each requiring multi-point sharps infrastructure. Italy faces combined pressure from a July 2024 plastic tax and rising labour costs, prompting larger private hospital groups to trial 6-gallon reusable fleets that reduce pickup frequency. Both markets witness growing interest in RFID tagging to streamline waste manifesting and simplify environmental reporting obligations.

Spain posts the fastest 8.07% CAGR through 2031, buoyed by EU structural funds that finance hospital modernization and by pioneering all-electric private hospital chains that embed circular-economy KPIs into supplier scorecards. The 2023 national plastics-packaging tax at EUR 0.45 per kilogram strengthens the economic case for reusable bins and high recycled-content formulas. Spanish outpatient expansion spurs geographically dispersed demand, making agile e-commerce channels attractive for timely delivery to rural clinics.

Central and Eastern European member states remain smaller in value but deliver above-average growth as facility upgrades catch up to western standards. Limited third-party sterilization capacity restrains reusable penetration, yet EU cohesion-policy grants earmarked for waste-management modernization could unlock latent demand over the forecast horizon.

Competitive Landscape

Europe’s sharps containers market is moderately fragmented, with the top five suppliers controlling significant revenue. Stericycle, Daniels Sharpsmart, and Becton Dickinson anchor the leader group by coupling containers with integrated pickup and destruction services, allowing hospitals one-invoice simplicity. Mid-tier challengers differentiate through IoT ecosystems that overlay real-time location and fill-level analytics, reducing client labour spend and improving regulatory reporting accuracy. New entrants concentrate on bio-based polymer formulations and circular leasing models that obviate capital outlay, appealing to budget-constrained public hospitals seeking immediate emissions reductions.

Technology capability is emerging as the prime competitive lever. Daniels Sharpsmart’s 2024 launch of a fully enclosed eight-gallon reusable line with embedded UHF RFID chips cut container loss rates by 95% at pilot sites in the Netherlands. Becton Dickinson extended its BD Cantest programme to include carbon-impact dashboards, enabling trusts to track monthly CO₂ savings from reusable adoption. Stericycle entered a strategic partnership with SenSonEO in 2025 to integrate container telemetry into its route-optimisation software, slashing road miles and strengthening sustainability narratives[3]SENSONEO, “Smart Waste Management System,” sensoneo.com.

Consolidation pressures persist, evidenced by a 2025 minority investment from a European infrastructure fund into a Scandinavian sharps container washing network, signalling financial appetite for recurring-revenue waste-services platforms. Nonetheless, barriers to entry stay manageable; established moulders can still win tenders regionally if they certify to EN ISO 23907-1 standards and exhibit adequate quality-management systems. Competitive intensity is thus expected to sharpen as digital features become table-stakes rather than premiums.

Europe Sharps Containers Industry Leaders

Alleva Medical

Henry Schein, Inc.

Sharps Medical Waste Services

Mauser Packaging Solutions

Daniels Sharpsmart Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NHS England published its 4th Health and Climate Adaptation Report, embedding sustainable medical-waste procurement into net-zero pathways.

- October 2024: Health Care Without Harm Europe issued updated sustainable waste-management guidelines that prioritise reusable containers within a waste-hierarchy model.

Europe Sharps Containers Market Report Scope

As per the scope of the report, a sharps container is a hard plastic container utilized for the disposal of hypodermic needles and other sharp medical items, including IV catheters and disposable scalpels, in a safe manner. The containers are frequently sealable, self-locking, and robust, thereby blocking waste from penetrating the container's surfaces.

The European sharps containers market is segmented by usage, type, container size, distribution channel, and geography. By usage, the market is segmented into single-use containers and reusable containers. By type, the market is segmented into patient room containers, phlebotomy containers, and multipurpose containers. By container size, the market is segmented into 1-2 gallons, 2-4 gallons, and 4-8 gallons. By distribution channel, the market is segmented into direct sale, online sale, and retail sale. By geography, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. The report offers the market sizes and forecasts in value terms (USD) for the above segments.

| Single-use Containers |

| Reusable Containers |

| Patient-Room Containers |

| Phlebotomy Containers |

| Multipurpose Containers |

| 1-2 Gallons |

| 2-4 Gallons |

| 4-8 Gallons |

| Direct Sales |

| Online Sales |

| Retail / Dealer Sales |

| Hospitals |

| Ambulatory Surgery Centers |

| Physician & Dental Offices |

| Home-Healthcare Settings |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Usage | Single-use Containers |

| Reusable Containers | |

| By Container Type | Patient-Room Containers |

| Phlebotomy Containers | |

| Multipurpose Containers | |

| By Container Size | 1-2 Gallons |

| 2-4 Gallons | |

| 4-8 Gallons | |

| By Distribution Channel | Direct Sales |

| Online Sales | |

| Retail / Dealer Sales | |

| By End-User | Hospitals |

| Ambulatory Surgery Centers | |

| Physician & Dental Offices | |

| Home-Healthcare Settings | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European sharps container business today and what growth is expected?

Revenue stands at USD 201.72 million in 2026 and is forecast to reach USD 249.22 million by 2031 on a 4.32% CAGR.

Which country accounts for the biggest demand?

Germany supplies 39.72% of regional sales thanks to dense hospital capacity, strict compliance standards, and local moulding plants.

What is driving hospitals to switch from single-use to reusable bins?

EU circular-economy rules, hospital net-zero pledges, and plastics taxes incentivise multi-cycle containers that lower waste volumes and cut lifecycle carbon by up to 56%.

How fast are reusable sharps containers expanding compared with disposables?

Reusable units are growing 8.22% CAGR to 2031, while single-use formats remain dominant but advance more slowly.

What cost pressures should procurement teams prepare for?

The EUR 0.80-per-kg plastics levy and similar national taxes inflate polypropylene prices, while installing wash-line infrastructure for reusables can exceed EUR 500,000.

How are digital tools changing sharps container procurement?

RFID- and IoT-enabled bins automate fill-level alerts, cut logistics labour by 58%, and link directly to e-procurement portals for auto-reordering and compliance reporting.

Page last updated on: