Stealth Technologies Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

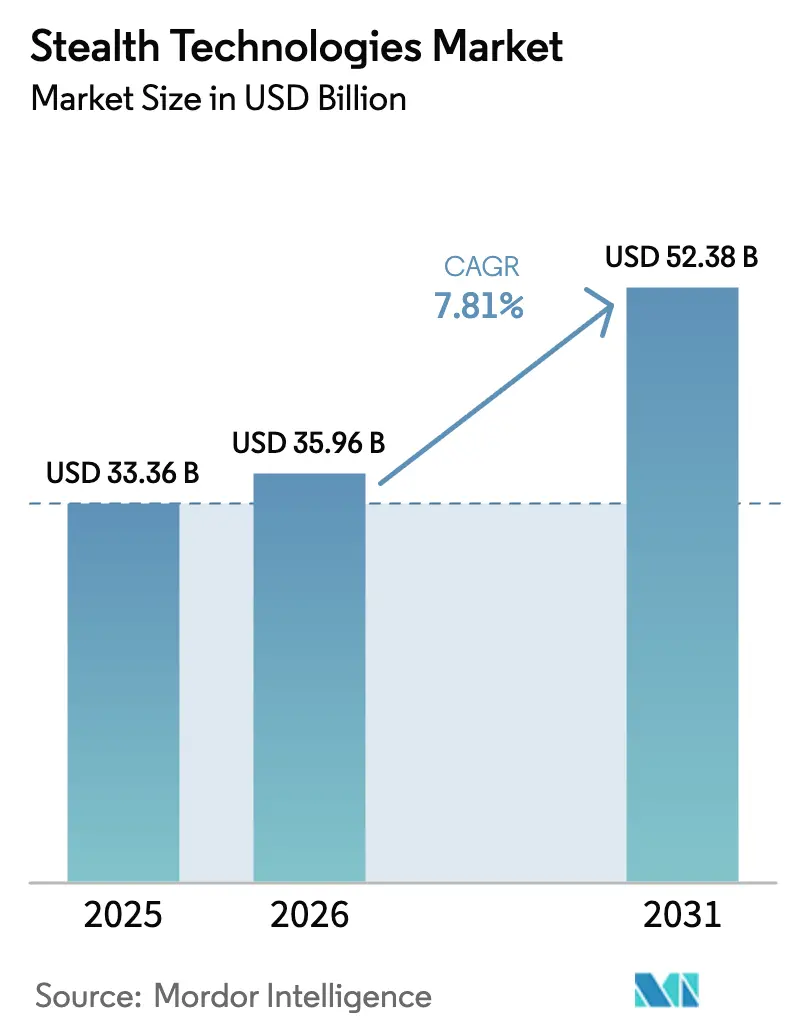

| Market Size (2026) | USD 35.96 Billion |

| Market Size (2031) | USD 52.38 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

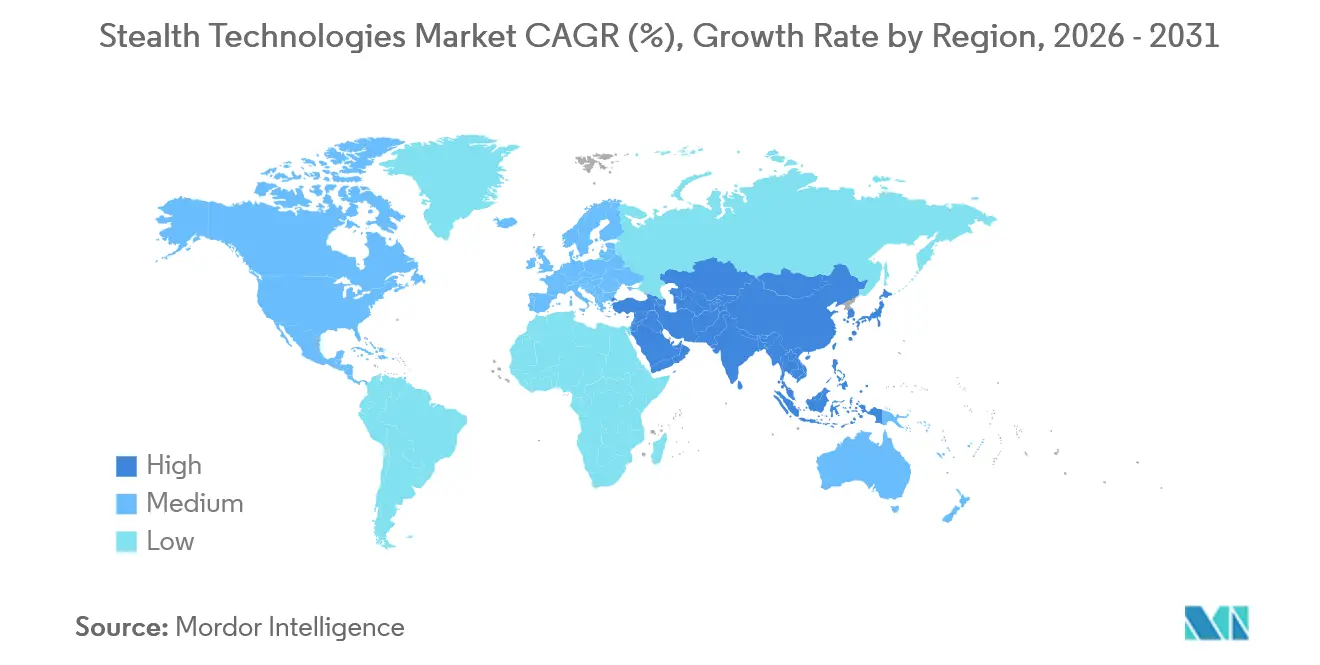

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

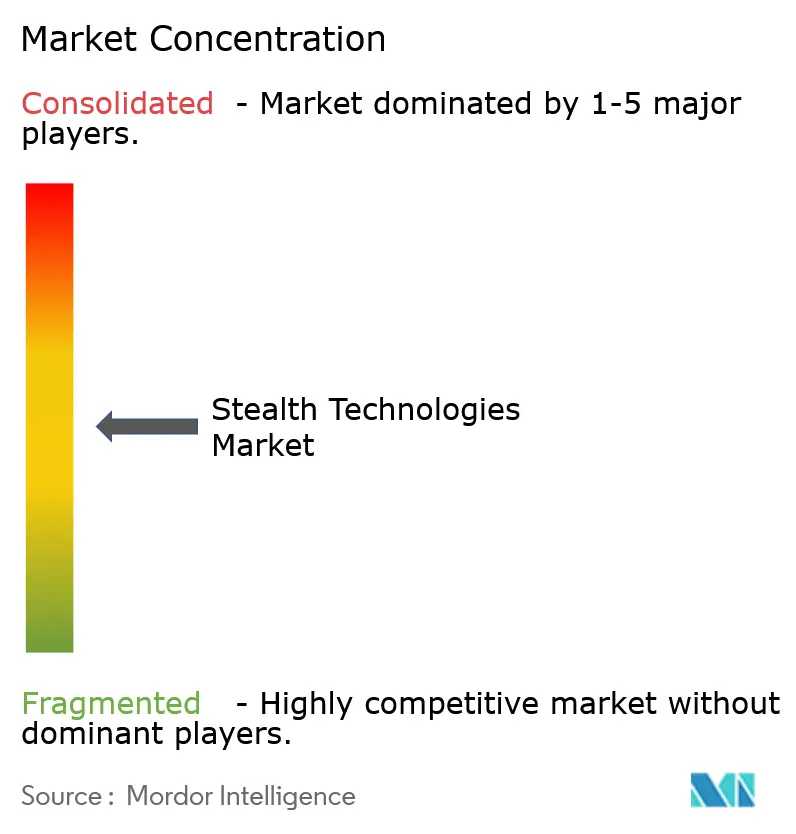

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stealth Technologies Market Analysis by Mordor Intelligence

The stealth technologies market size is expected to grow from USD 33.36 billion in 2025 to USD 35.96 billion in 2026 and is forecasted to reach USD 52.38 billion by 2031 at a 7.81% CAGR over 2026-2031. The accelerated fielding of multi-static low-frequency radars, hypersonic vehicle programs, and low-observable satellite constellations is stimulating rapid material innovation, rather than displacing low-observable design altogether. Boeing’s March 2025 victory in the USD 20 billion Next Generation Air Dominance (NGAD) competition illustrates how sixth-generation fighters will embed signature reduction inside open-architecture EW frameworks that can be re-programmed against emerging sensor threats. In parallel, the US Air Force’s plan to acquire more than 1,000 Collaborative Combat Aircraft (CCA) is shifting the economics of survivability toward swarms of low-cost, unmanned platforms that can absorb attrition while extending the sensor reach of manned assets. Northrop Grumman’s B-21 Raider, China’s J-20 Block 3, and Japan’s entry into the four-nation Global Combat Air Programme (GCAP) confirm that new strategic investments are proliferating across every central defense region.

Key Report Takeaways

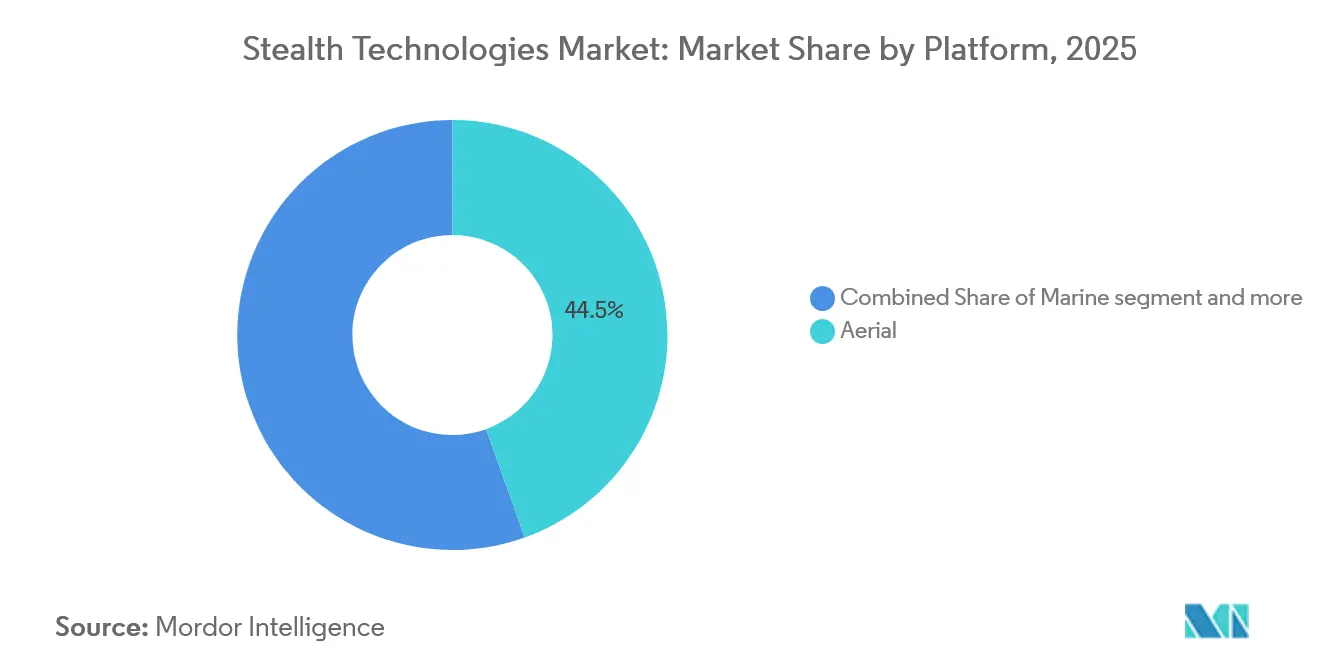

- By platform, aerial systems led with 44.54% of the stealth technologies market share in 2025, while terrestrial vehicles are forecast to post the fastest CAGR of 9.18% through 2031, as ground forces become increasingly resistant to ubiquitous sensors.

- By technology type, radar-absorbent materials are expected to hold a 36.59% revenue share; plasma and electromagnetic cloaking are poised for the fastest growth, with an 8.71% CAGR, driven by DARPA and Space Force prototype demonstrations.

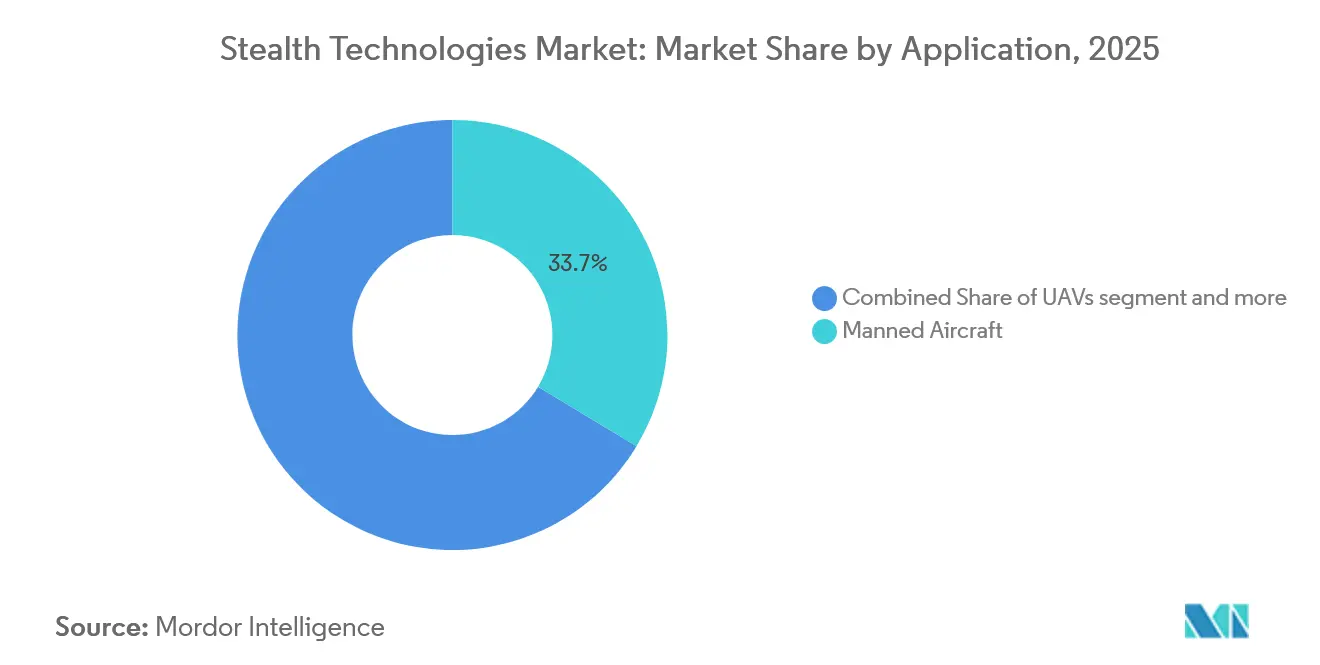

- By application, manned aircraft captured 33.65% of the revenue in 2025; however, unmanned aerial vehicles are expected to expand at a 10.15% CAGR, driven by the CCA program and loyal-wingman projects in Australia and Europe.

- By geography, North America dominated with 34.89% revenue in 2025, supported by the B-21 test fleet and NGAD funding. In contrast, Asia-Pacific is projected to register the highest CAGR of 9.93% through 2031, as China, South Korea, and India accelerate the production of fifth- and sixth-generation fighters.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stealth Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ubiquity of multi-static low-frequency radars driving RAM upgrades | +1.2% | Global, with concentration in Eastern Europe, Indo-Pacific | Medium term (2-4 years) |

| Shift toward combined stealth-EW architectures for sixth-generation fighters | +1.5% | North America, Europe, Asia-Pacific (China, Japan, South Korea) | Long term (≥ 4 years) |

| Mass production of low-observable UAV swarms for ISR and decoy missions | +1.8% | North America, Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Hypersonic-related aero-heating challenges increasing demand for advanced CMC RAM | +1.0% | North America, China, Russia | Medium term (2-4 years) |

| Growing interest in plasma-magnetic signature suppression for LEO satellites | +0.6% | Global, led by North America and China | Long term (≥ 4 years) |

| Additive manufacturing of graded-density metamaterials reducing program costs | +0.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ubiquity of Multi-Static Low-Frequency Radars Driving RAM Upgrades

Multi-static VHF and UHF radar networks now cover the Baltic region and the South China Sea, exposing shape-optimized airframes at ranges exceeding 200 km and forcing operators to invest in broadband coatings that absorb energy from 30 MHz to 18 GHz.[1]Multi-Static Radar Networks Challenge Stealth, NATO Science & Technology Organization, sto.nato.int China’s YLC-8E system achieved live tracking of low-RCS targets in 2024, accelerating US procurement of rare-earth-rich broadband RAM despite triple material costs relative to a narrowband alternative. The US FY-2025 defense budget allocates USD 340 million for F-35 radar cross-section sustainment, 28% above the 2024 levels, underscoring the urgency of upgrades. Smaller Eastern European air forces are retrofitting fourth-generation fighters with modular applique panels during depot maintenance, spawning a niche aftermarket. The resulting demand boosts the stealth technologies market, despite the proliferation of counter-stealth sensors.

Shift Toward Combined Stealth-EW Architectures for Sixth-Generation Fighters

Boeing’s F-47 NGAD integrates cognitive EW processors that modulate surface impedance in real time, transforming the airframe skin into a reconfigurable antenna rather than a passive absorber. The contract mandates open-mission-systems interfaces, allowing third-party payloads to update signature profiles via software updates instead of physical respray cycles. Parallel design choices in GCAP’s Tempest require active frequency-selective surfaces that are reprogrammable in the field, a capability that passive F-35-era coatings cannot match. China’s J-20 Block 3 embeds distributed RF apertures along wing edges to alternate between low-observable and electronic-attack modes. Lockheed Martin’s F-35 lineage, rooted in fixed coatings, was judged less adaptable, underscoring a paradigm shift that rewrites competitive advantage in the stealth technologies market.

Mass Production of Low-Observable UAV Swarms for ISR and Decoy Missions

The US Air Force caps CCA unit costs at below USD 30 million, enabling a planned fleet of over 1,000 aircraft that can be sacrificed to saturate adversary defenses. Anduril’s Fury employs a blended-wing body to achieve bird-sized radar signatures while omitting expensive thermal-management systems carried by manned penetrators, cutting life-cycle costs. General Atomics’ XQ-67A flew autonomously with F-35s during Red Flag, validating manned-unmanned teaming at operational scale. Boeing Australia’s MQ-28 Ghost Bat finished carrier trials in 2025, broadening naval swarm concepts. China’s GJ-11 Sharp Sword entered serial production, confirming a parallel focus on inexpensive low-observable UAVs. The cost calculus is USD 300 million for ten CCAs versus over USD 100 million for a single F-35, cementing swarming as a primary growth vector for the stealth technologies market.

Hypersonic-Related Aero-Heating Challenges Increasing Demand for Advanced CMC RAM

Mach-5-plus weapons raise leading-edge temperatures above 2,000 °C, eclipsing the limits of carbon-carbon composites used on subsonic aircraft. NASA testing has proven that zirconium diboride and hafnium carbide ceramic matrix composites retain their absorption at 2,200 °C for 10 minutes, a requisite for boost-glide profiles.[2]NASA Hypersonic Materials Research, NASA Technical Reports Server, ntrs.nasa.gov DARPA’s Hypersonic Air-Breathing Weapon Concept pairs C/C-SiC substrates with graded ZrB2-SiC outer layers to balance thermal shock with X- and Ku-band attenuation. Oak Ridge National Laboratory reduced the UHTC part cycle time from 72 hours to 18 hours, resulting in a 40% cost reduction and making the production of hypersonic radar-absorbing components viable. China’s DF-17 glide vehicle reportedly uses similar ceramics, while Russia’s Avangard relies on carbon-carbon with boron carbide additives, though oxidation remains a vulnerability. As hypersonic prototypes enter procurement, ultra-high-temperature RAM becomes a material science frontier within the stealth technologies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tri-band passive radar proliferation reducing operational advantage | -0.8% | Eastern Europe, Indo-Pacific, Middle East | Short term (≤ 2 years) |

| Regulatory barriers on ITAR-controlled advanced composites | -0.6% | Global, most acute for non-US allies | Medium term (2-4 years) |

| High O&M costs of radar-absorbent coatings in humid littoral climates | -0.5% | Indo-Pacific, Middle East, South America | Medium term (2-4 years) |

| Thermal-acoustic signature trades limiting platform endurance | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tri-Band Passive Radar Proliferation Reducing Operational Advantage

ERA’s VERA-NG network, deployed across NATO’s eastern flank, achieved 400 km tracking of stealth surrogates by fusing VHF, UHF, and L-band illuminators, compressing undetected loiter windows to under 20 minutes. China’s DWL-002 sites, arrayed along the Taiwan Strait, are expected to expand to 12 installations by 2025, providing early warning without emitting energy that can be targeted, thereby complicating suppression missions. RAND analysis shows passive radar investments cost one-tenth of active AESA arrays, democratizing counter-stealth and eroding the value premium of low-observable platforms. US Air Force doctrine updates now emphasize rapid ingress and egress, as well as standoff munitions, a shift that reduces platform loiter time and undermines some investment cases for highly stealthy platforms. Market growth persists, albeit at a moderated pace, as operators weigh the cost-effectiveness of their strategies against shrinking tactical windows.

Regulatory Barriers on ITAR-Controlled Advanced Composites

ITAR restrictions on carbon-nanotube RAM and metamaterial designs slow multinational programs and raise duplication costs. The United Kingdom waited 14 months for US approval to co-produce Tempest RAM, pushing BAE to build redundant lines at a 35% cost premium.[3]Tempest ITAR Review, Financial Times, ft.com Japan’s GCAP participation triggered the adoption of compartmentalized tech-sharing rules, which complicate the cross-licensing of frequency-selective surfaces. South Korea’s KF-21 Block 2 schedule slipped 18 months after denials of F-35 coating IP, forcing local R&D efforts. India’s AMCA program pivoted to domestic materials when export licenses were denied, yet early tests show 20% lower broadband absorption performance. Such frictions incentivize foreign self-reliance, while delaying program milestones and restraining the growth of the stealth technologies market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Ground Vehicles Accelerate Signature Management

Terrestrial vehicles are forecast to post a 9.18% CAGR from 2026 to 2031, the fastest among platform groups, as armies retrofit main battle tanks and infantry fighting vehicles with applique RAM to counter the proliferation of drone and loitering-munition sensors. Israel Aerospace Industries’ Carmel demonstrator achieved a 60% reduction in radar cross-section relative to legacy hulls, validating modular kits that can be fitted during depot overhauls. The aerial segment held a 44.54% market share in stealth technologies in 2025, driven by the development of sixth-generation fighters and CCA prototyping. Yet unit costs for exquisite manned aircraft drive a shift toward mass-produced unmanned swarms, redistributing procurement budgets. Maritime platforms integrate tumblehome hulls and active-cancellation arrays as seen on the US Navy’s DDG(X), while submarine anechoic tiles advance acoustic stealth. Space and missile segments remain niche but draw R&D as low-Earth-orbit operators test plasma sheaths and as standoff missiles adopt low-observable skins. Collectively, cross-domain demand reinforces the strategic importance of stealth technologies.

In the aerial domain, additive manufacturing is shortening iteration cycles for blended-wing-body UAVs, enabling rapid concept verification. On land, 3D-printed metamaterial tiles allow armored brigades to tailor signatures for urban or open-terrain operations within hours. Naval designers increasingly prioritize electromagnetic signature balance over pure radar reduction to avoid compromising infrared and acoustic profiles. The convergence of materials science across these environments indicates that the stealth technologies market will remain platform-agnostic, with providers selling standard chemistries and design toolchains to multiple domain integrators. This dynamic supports a healthy supplier ecosystem even as individual platform programs fluctuate.

By Technology Type: Plasma Cloaking Transitions From Concept to Prototype

Radar-absorbent materials secured 36.59% of 2025 revenue, remaining the workhorse of the stealth technologies market. Next-generation polymer matrices infused with rare-earth microflakes now exceed a 20 GHz bandwidth, but incremental gains face diminishing returns in terms of cost per decibel. Shaping and geometric design continue to underpin every program; yet, the cost of fine-tuning curvatures rises sharply beyond the 0.001 m² radar-cross-section threshold. Infrared signature management, crucial for defeating imaging seekers, competes with radar stealth for space and power budgets, forcing design-tradeoff algorithms to optimize across multiple spectral bands. Active cancellation is particularly suitable for surface ships, where power margins are generous; DDG(X) prototypes incorporate reconfigurable impedance panels flush with their topside structures.

Plasma and electromagnetic cloaking is forecast to grow at an 8.71% CAGR as DARPA and Space Force prototypes migrate from laboratory rigs to orbital testbeds. Demonstrations show 15 dB attenuation across 2-to-18 GHz, albeit at significant power expense. Additive manufacturing of graded-density metamaterials smooths impedance transitions, widening absorption by 40% and reducing layer counts by half, which in turn lowers maintenance cycles. These advances signal that active, software-defined approaches will supplement, not supplant, conventional materials, blending physical and electronic defenses into an integrated signature-management stack that defines the future of the stealth technologies industry.

By Application: Unmanned Aerial Vehicles Outpace Manned Platforms

Unmanned aerial vehicles are projected to expand at a 10.15% CAGR from 2026 to 2031, as CCAs, loyal wingmen, and expendable decoys transition into production. The segment benefits from relaxed crew-safety constraints, allowing sharper planform angles and minimal infrared suppression, as loss tolerance is higher. Manned aircraft accounted for 33.65% of the revenue in 2025, supported by F-35 and B-21 deliveries; however, rising procurement costs are tilting marginal investment toward unmanned fleets. Surface ship stealth advances center on enclosed masts and radar-transparent composites, with China’s Type 055 destroyer fielding faceted superstructures across 25 hulls by 2025. Submarine programs focus on broadband anechoic tiles that attenuate active sonar while withstanding deep-water hydrostatic loads, a dual requirement driving the development of new elastomer chemistries.

Ground combat vehicles integrate signature kits during routine depot visits, providing cost-effective upgrades for fleets that are typically 25 years in age. Missile and precision-guided munition designers embed serpentine inlets and low-observable skins; Lockheed Martin’s AGM-158 JASSM-ER reports penetration probabilities above 90% against modern SAMs. Together, these applications confirm that platform type no longer dictates technology leadership; instead, mission profile and acceptable unit risk define the adoption curve inside the stealth technologies market.

Geography Analysis

North America generated 34.89% of global revenue in 2025, as the B-21 Raider entered flight testing and NGAD funding was secured through multi-year research outlays. The United States also leads the hypersonic race, investing in UHTC supply chains and ordering 1,000-plus CCAs, which collectively anchor domestic demand despite budget scrutiny. Canada’s Department of National Defence is allocating funds to retrofit CF-18 replacements with broadband coatings, reflecting an alignment with allied nations around US supply chains.

Asia Pacific is forecast to register the highest a 9.93% CAGR through 2031 as China raises annual J-20 production toward 60 airframes and tests J-35 carrier variants. South Korea’s KF-21 Block 2 funding secures stealth upgrades, while Japan’s GCAP participation grants access to sixth-generation architectures in cooperation with the UK, Italy, and Sweden. India’s AMCA aims for first flight by 2029, marking a strategic move to reduce import dependence despite technology gaps. Australia champions swarming concepts through the MQ-28 Ghost Bat program, and Southeast Asian nations are pursuing low-observable missile boats to counterbalance regional power asymmetries.

Europe maintains robust funding for the GCAP and France-Germany-Spain’s rival, the Future Combat Air System, though trans-Atlantic ITAR frictions complicate component flows. Eastern European states procure passive multiband radars and retrofit legacy fighters with applique RAM instead of buying fifth-generation jets, a pragmatic response to budget limits and proximity to potential conflict zones. The Middle East is acquiring low-observable aircraft and naval assets to offset missile threats; the UAE’s interest in the F-35 and Saudi participation in Tempest exemplify regional modernization. South America remains a niche adopter; Brazil’s KC-390 transport includes limited stealth features but no dedicated low-observable combat aircraft pipeline.

Regulatory Landscape

Stealth-enabling materials, designs, and associated technical data are closely managed through export-control and program-protection regimes, led by the United States International Traffic in Arms Regulations (ITAR) administered by the Department of State under the U.S. Munitions List (USML). The July 2025 Federal Register update cycle for ITAR-related rules reinforces that cross-border transfers of low-observable (LO) composites, metamaterials, and related technical data remain a gating factor for multinational programs, consistent with the report context on ITAR frictions affecting GCAP/Tempest and other allied efforts.

On the acquisition side, DoD compliance requirements increasingly influence qualification and supplier readiness for LO sustainment and signature-management work. The Technology and Program Protection (T&PP) framework (aligned to DoDI 5000.83) and DoD Scientific and Technical Information Program requirements (DoDI 3200.12) guide how contractors safeguard sensitive design and test information. Access to controlled technical drawings commonly requires Joint Certification Program (JCP) eligibility and NIST SP 800-171 DoD assessment visibility in SPRS. In March 2026, a Naval Undersea Warfare Center Division Newport solicitation for Radar Absorbing Surfaces and hardware kits explicitly required protection of controlled information and security compliance, showing how handling rules can affect sourcing, lead times, and competition for stealth-related components.

Value Chain Analysis

The stealth technologies value chain starts with advanced material inputs (polymers, carbon-based reinforcements, rare-earth microflakes, ceramics for ultra-high-temperature use) and moves into formulation and processing into coatings, structural composites, metamaterial tiles, and frequency-selective or impedance surfaces. The workflow relies on precision layup and cure for composites, additive manufacturing for graded-density structures, and controlled application or repair processes for low-observable coatings, followed by test and verification using radar cross-section (RCS) ranges and multispectral measurement. Integration is dominated by prime contractors and major platform integrators across air, land, sea, and missile programs, while sustainment organizations and depot networks drive recurring revenue through inspection, repair, and reapplication cycles.

Recent program and industrial moves point to where bottlenecks and localization emerge. In July 2025, Rheinmetall Aviation Services began operations at a 60,000 sq. m facility in Weeze, Germany, to manufacture F-35A center fuselage sections with Northrop Grumman and Lockheed Martin, indicating growing emphasis on regionalized production nodes for sensitive structures. Capacity scaling constraints can surface in adjacent precision-defense supply chains, and Reuters reported in July 2024 that component bottlenecks affected US-Japan efforts to expand PAC-3 Patriot missile production, highlighting how specialized sub-tier parts can limit output even when prime-level assembly capacity is available. At the platform test-validation end of the chain, Boeing validated the MQ-28 Ghost Bat RCS performance in June 2026, reinforcing the role of measurement infrastructure and acceptance testing as key gates before procurement, export, or broader production ramps.

Competitive Landscape

The market exhibits moderate concentration: the top four primes, Lockheed Martin Corporation, Northrop Grumman Corporation, The Boeing Company, and BAE Systems plc, controlled an estimated 55%-60% of 2025 revenue, yet contract awards in 2024-2026 reveal increasing pressure from agile entrants. Boeing’s NGAD win and Northrop Grumman’s B-21 progress secure near-term backlog, but Lockheed Martin’s failure to capture NGAD underscores that F-35 incumbency does not guarantee next-generation dominance. Anduril’s USD 1.8 billion CCA contract demonstrates that Silicon Valley development cadence resonates with acquisition executives focused on unit cost and refresh speed.

Materials suppliers are consolidating. Northrop Grumman’s 2024 purchase of Composite Technology Development locks in resin and fiber IP, while CoorsTek and Kyocera enter hypersonic thermal-protection niches once occupied by traditional RAM vendors.[4]Northrop Grumman CTD Acquisition, Northrop Grumman, northropgrumman.com Patent filings increased 18% year-over-year in 2025, driven by advancements in reconfigurable impedance surfaces and printed metamaterials. Boeing’s April 2025 patent for a varactor-loaded skin exemplifies the convergence of hardware and software within structural components.[5]Boeing Reconfigurable Impedance Patent, U.S. Patent and Trademark Office, uspto.gov Vertical integration strategies aim to capture high-margin subsystems, including cognitive EW processors and additive printable chemistries, rather than relying solely on platform margins.

Competitive tactics emphasize rapid prototyping, open architectures, and transparency in costs. Kratos demonstrates flyaway prices of less than USD 5 million for expendable decoys, eroding legacy primes’ cost-plus models. Saab and Mitsubishi Heavy Industries leverage shared R&D to offset ITAR chokepoints, ensuring a smooth technology flow within GCAP. Investment flows into additive manufacturing lines capable of printing graded-density metamaterials at scale, reducing capital barriers for mid-tier firms. Collectively, these dynamics indicate sustained contestation for a share of the stealth technologies market through the next decade.

Stealth Technologies Industry Leaders

BAE Systems plc

Lockheed Martin Corporation

Northrop Grumman Corporation

RTX Corporation

The Boeing Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One clear opportunity is shifting from maintenance-heavy external radar-absorbent coatings toward structural stealth, where absorbing or impedance-tuning functionality is built into composite airframes and outer mold lines. This direction tracks the report-identified restraint around high O&M costs of coatings in harsh climates, and it aligns with the broader move toward combined stealth-EW architectures, where signature control is increasingly software-defined and adaptable across threat bands rather than tied to fixed, narrow solutions.

Another opportunity is scaling low-observable, attritable systems, along with the industrialization of their stealth verification and production methods. In June 2026, Boeing validated MQ-28 Ghost Bat RCS performance through testing, providing an example of a low-observable unmanned platform moving through measurable stealth acceptance gates that support procurement, export pathways, and repeatable production processes. On the program-funding side, US congressional activity around NGAD provides an anchor for ongoing integration of stealth with open-architecture electronic warfare frameworks, and the CRS NGAD brief cites USD 3.19 billion provided for F-47 development in FY2026 while directing quarterly program updates. That spending reinforces demand for reprogrammable signature-management approaches, including associated materials, test systems, and sustainment toolchains. In parallel, 2026 academic advances in radar-infrared compatible materials, including MXene- and carbon-aerogel-based composites, expand the solution space for multi-spectral signature management across aircraft, missiles, and terrestrial platforms where radar, thermal, and acoustic tradeoffs influence procurement decisions.

Recent Industry Developments

- July 2026: The Global Combat Air Programme (GCAP) advanced into its full engineering phase following a multi-billion-dollar contract award, formalizing the next stage of sixth-generation aircraft development. This step tightens the link between airframe stealth, electronic warfare, and open-architecture mission systems, expanding demand for reprogrammable signature-management materials and structures across the partner ecosystem.

- May 2026: Northrop Grumman reported that the B-21 Raider Combined Test Force compressed a 180-day test plan to 73 days while completing a significant portion of planned missions. The acceleration indicates maturing test processes for low-observable aircraft and increases pull-through for production-ready stealth materials, measurement, and sustainment workflows tied to flight-test learning.

- March 2024: Northrop Grumman completed the acquisition of Composite Technology Development, adding specialized resin and fiber intellectual property to its internal supply base. Vertical integration at the materials level strengthens control over critical low-observable structures and can reshape supplier access for advanced composites used in stealth platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the stealth technologies market is defined as the revenue generated from technologies that reduce the detectability of defense platforms across radar, infrared, and other sensing modes. The scope covers the materials, design features, and counter-detection techniques used in military use cases.

Scope exclusions: Exclusions include purely commercial stealth use cases and general defense electronics that do not materially change platform signatures.

Segmentation Overview

- By Platform

- Aerial

- Marine

- Terrestrial

- Space-Based

- By Technology Type

- Radar-Absorbent Materials (RAM)

- Shaping and Geometric Design

- Infrared Signature Reduction

- Active Cancellation (Electronic Stealth)

- Plasma/EM Cloaking

- By Application

- Manned Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Surface Ships

- Submarines

- Ground Combat Vehicles

- Missiles and Precision-Guided Munitions

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial picture of demand, funding, and platform activity that drives stealth adoption. We relied on public defense budget documents and procurement releases, along with sources such as SIPRI military expenditure data, NATO defense spending summaries, and UN Comtrade trade statistics for relevant materials and components.

To keep assumptions grounded, the research also used technical and policy references such as FAA and ICAO publications for aircraft fleet context, and peer-reviewed aerospace and materials journals that discuss radar cross section reduction, infrared suppression, and coatings performance. For company-level context, filings and investor presentations were reviewed where available, and reputable defense press was used to time major platform programs. In a few areas, paid subscriptions were used for company financials and patent databases to cross-check innovation activity and supplier presence. These examples are indicative only, and many other sources were also used for data collection, clarification, and validation checks.

Primary Interviews and Surveys

Primary work focused on validating what is actually being procured and integrated, and how spending is split across platform types and technology areas. We spoke with a mix of platform-focused stakeholders, materials specialists, integrators, and procurement-aligned experts across key regions so that desk research gaps on adoption rates, upgrade cycles, and pricing ranges could be closed.

Interview feedback was also used to sanity check assumptions on when stealth features are counted (new build vs retrofit), how multiyear defense programs are phased, and which technology lines are seeing the fastest funding momentum.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 22% | Managers: 49% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where defense platform procurement and upgrade pipelines are translated into a demand pool, and then filtered using stealth penetration rates by platform category. We then corroborate results with selective bottom-up approximations using sampled program level bill-of-material logic, supplier revenue disclosures where available, and price range checks for major stealth material and subsystem types.

Key inputs used in the model include new aircraft and naval platform deliveries, retrofit and MRO driven upgrade cadence, defense RDT&E and procurement budget splits, observable platform program timelines, and indicative pricing progression for stealth materials and signature management subsystems. Where a data point was missing for a country or platform, the gap was handled by mapping it to comparable fleets and budgets, followed by a primary check so the assumption did not drift.

For forecasting, scenario analysis was used because defense procurement is sensitive to program delays, budget reallocations, and geopolitical shifts. Baseline growth reflects the most common expert view on platform fielding schedules and steady adoption of RAM, shaping related upgrades, infrared signature reduction, and electronic stealth methods, with upside and downside ranges applied around funding and delivery timing.

Data Validation & Update Cycle

Outputs were validated through multiple checks so totals stayed consistent with real world signals. We compared model results against independent indicators such as defense procurement totals, public platform delivery counts, and known program milestone timing, and then investigated any large variances before internal sign-off.

When inconsistencies showed up, assumptions were revisited and respondents were re-contacted selectively to confirm whether the issue was pricing, penetration, or timing related. Reports are refreshed annually, with interim updates when material events occur such as major contract awards, program cancellations, or rapid shifts in defense budgets. Before delivery, a final analyst pass is completed so clients receive the most current view supported by the same repeatable checks.

Mordor Intelligence's Stealth Technologies Market Size Compared With Other Published Estimates

Published market sizes for stealth technologies often differ because the included revenue streams are not the same, and because the timing assumptions for defense programs can move totals up or down by year. Differences also come from whether values are captured at the technology level only or expanded to include adjacent services and broader platform related spending.

Testing, evaluation, and MRO service revenues can push totals higher, and those items sit outside Mordor Intelligence's scope, which stays focused on stealth technology revenues tied to platform integration across the defined technology types and applications. Other gaps usually come from how radar absorbent materials and electronic stealth are priced over time, how retrofits are counted versus new builds, and whether currency conversion is taken at an annual average or a point-in-time rate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.36 B (2025) | |

| Global Consultancy A | USD 36.76 B (2025) | Includes broader factory-gate market values and related services such as testing, evaluation, systems integration, and MRO, which inflates the addressable pool beyond technology integration spend. |

| Industry Publisher B | USD 7.80 B (2024) | Uses a narrower definition that appears closer to select stealth subsystems and mixes in commercial and civil end users, which reduces the defense platform integration value captured in the total. |

The spread in estimates mainly comes down to what gets counted as market revenue, and the year and pricing path assumed for major programs. By keeping inputs traceable to platform demand signals, adoption rates, and realistic pricing ranges, the resulting number is easier to reconcile and to update when program timing shifts.

Key Questions Answered in the Report

What is the current size and growth rate of the stealth technologies market?

The stealth technologies market size is USD 35.96 billion in 2026 and is expected to reach USD 52.38 billion by 2031 at a 7.81% CAGR.

Which platform segment is growing fastest?

Terrestrial vehicles show the quickest expansion, forecast at a 9.18% CAGR as armies retrofit tanks and armored vehicles with radar-absorbent kits.

Why are unmanned systems pivotal to future stealth investments?

The US Air Force’s planned purchase of 1,000+ CCAs and similar programs abroad drive a 10.15% CAGR for UAV applications, leveraging lower unit costs and attritable swarm tactics.

Which region will add the most new spending by 2031?

Asia-Pacific leads with a projected 9.93% CAGR, fueled by China’s J-20 and J-35 output and South Korea’s KF-21 upgrades.

How are hypersonic programs influencing material innovation?

Temperatures above 2,000 °C on hypersonic vehicles spur demand for ultra-high-temperature ceramic matrix composites that retain radar-absorbent properties at extreme heat levels.

What competitive shifts occurred after NGAD and CCA awards?

Boeing’s NGAD win and Anduril’s CCA contract demonstrate that open-architecture designs and rapid prototyping can unseat traditional primes for next-generation programs.

Page last updated on: