Spunbond Nonwovens Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

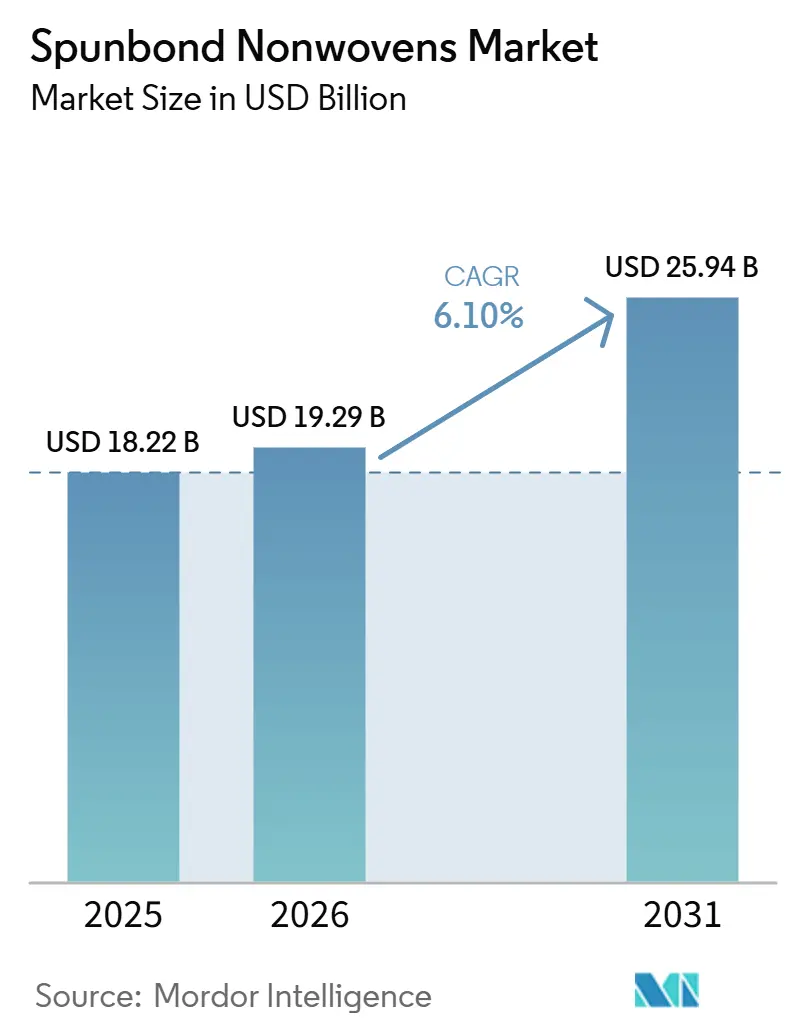

| Market Size (2026) | USD 19.29 Billion |

| Market Size (2031) | USD 25.94 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

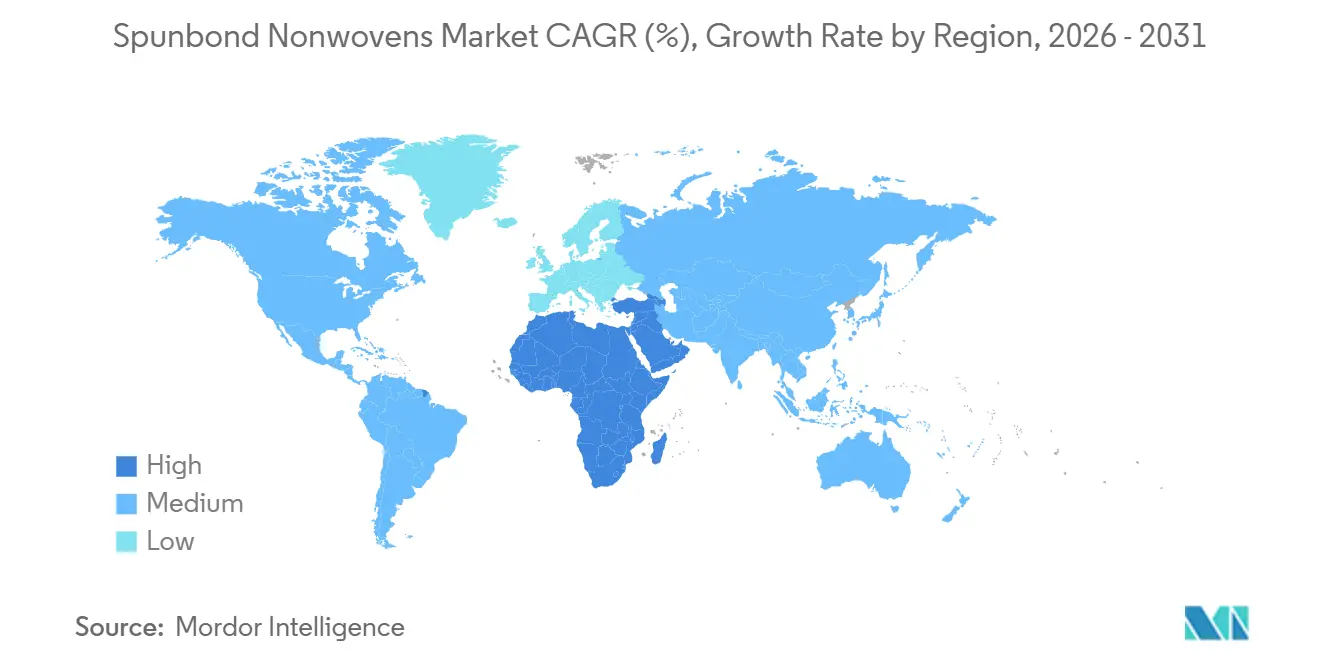

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spunbond Nonwovens Market Analysis by Mordor Intelligence

The Spunbond Nonwovens Market size is projected to be USD 18.22 billion in 2025, USD 19.29 billion in 2026, and reach USD 25.94 billion by 2031, growing at a CAGR of 6.10% from 2026 to 2031. Robust purchasing of hygiene disposables across India, Indonesia, and Vietnam continues to drive volume growth, while the EU Packaging and Packaging Waste Regulation (PPWR) is compelling European converters to redesign products using mono-material polypropylene to meet minimum recycled-content thresholds. Durable categories such as geotextiles and automotive interiors are expanding more rapidly than disposables, supported by government investments in climate-resilient infrastructure like roads, rail corridors, and flood barriers, as well as automakers' efforts to reduce cabin component weight to meet emission limits. Feedstock price volatility, highlighted by a 20% increase in global polypropylene prices in March 2026 due to shipping disruptions in the Strait of Hormuz, is prompting integrated polymer producers to backward-integrate and hedge margins. Simultaneously, vertically integrated suppliers capable of certifying recycled or bio-circular inputs under ISCC PLUS are securing long-term contracts, as brand owners require auditable chain-of-custody documentation to comply with upcoming due diligence laws in Europe and North America.

Key Report Takeaways

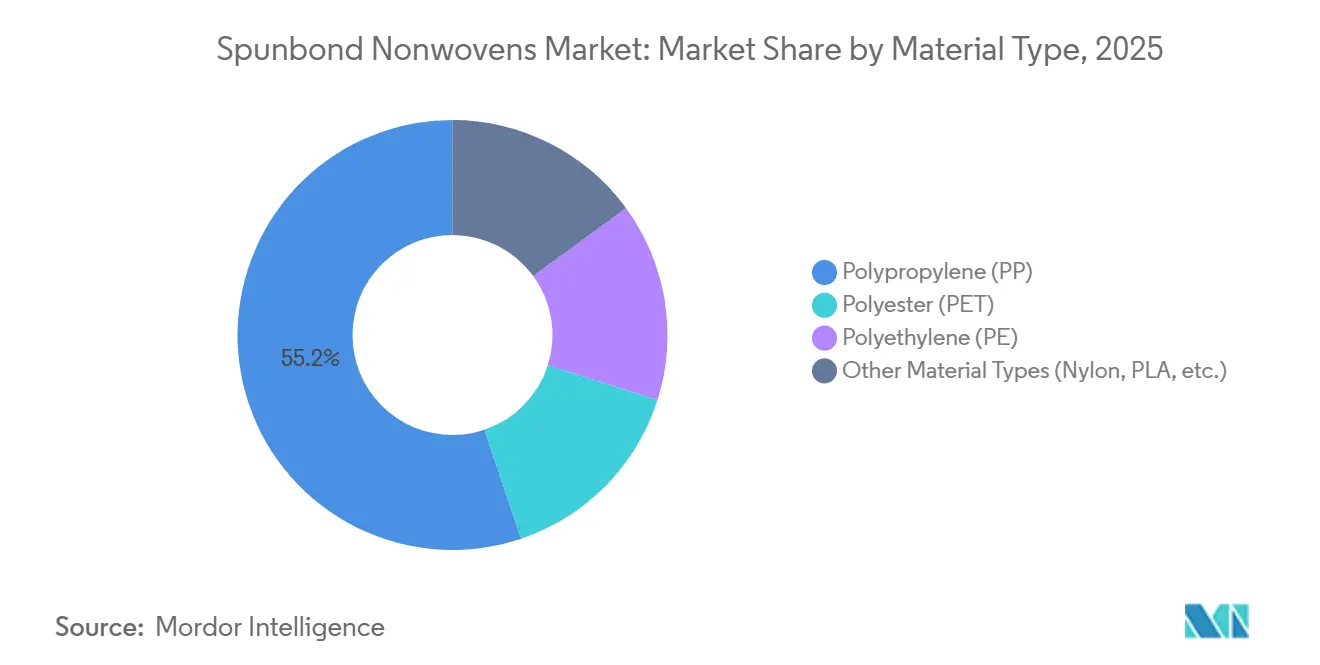

- By material type, polypropylene commanded 55.18% of the spunbond nonwovens market share in 2025, while other material types (nylon, PLA, etc.) are projected to post the fastest growth at 7.24% CAGR through 2031.

- By function, disposable accounted for 48.60% of the spunbond nonwovens market share in 2025, but durable is on track to expand at a 7.12% CAGR through 2031.

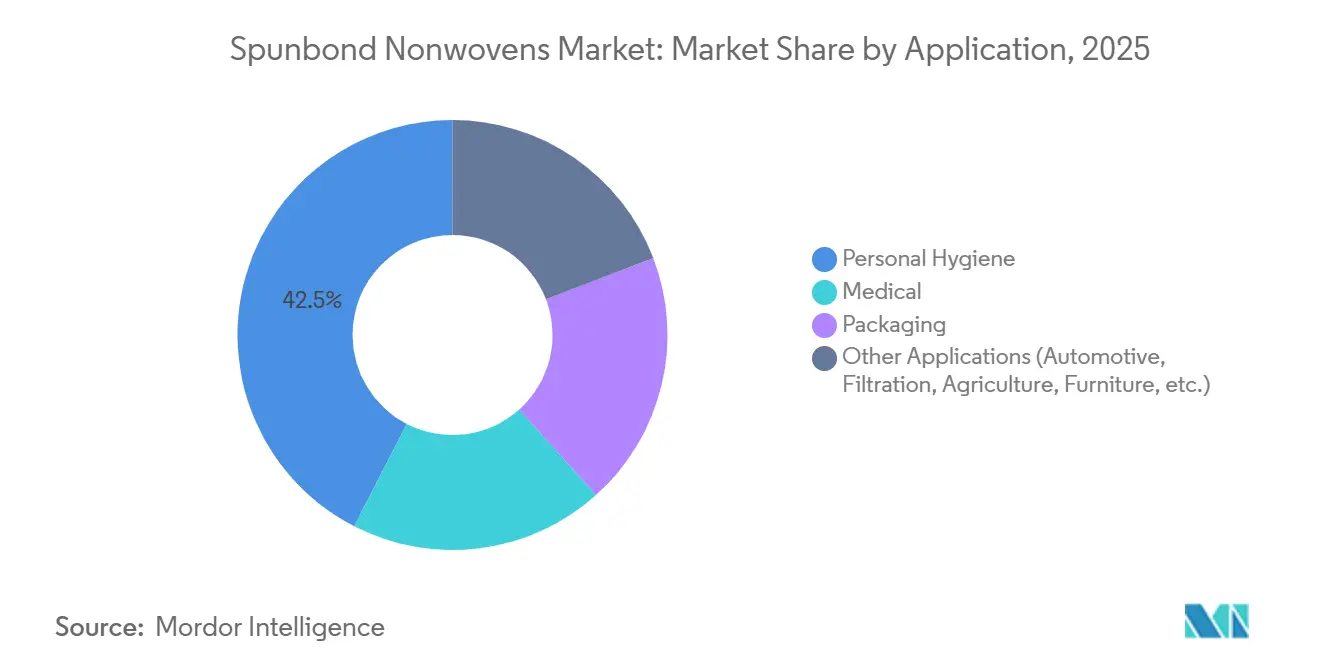

- By application, personal hygiene led with a 42.45% of the spunbond nonwovens market share in 2025, whereas medical is forecast to grow at a 7.30% CAGR through 2031.

- By geography, Asia-Pacific held 39.10% of the spunbond nonwovens market share in 2025; the Middle-East and Africa region is the fastest riser, expected to advance at a 7.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spunbond Nonwovens Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for hygiene disposables in emerging economies | +1.8% | APAC (India, Indonesia, Vietnam), MEA (Egypt, Saudi Arabia) | Medium term (2-4 years) |

| Expansion of medical protective-gear market | +1.2% | Global, with concentration in North America, Europe, China | Short term (≤ 2 years) |

| Cost- and performance-advantage over woven fabrics | +0.9% | Global | Long term (≥ 4 years) |

| Adoption of spunbond geotextiles in climate-resilient infrastructure | +0.7% | APAC, Middle-East, South America | Medium term (2-4 years) |

| Brand-owner shift to mono-material PP packaging | +0.6% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Hygiene Disposables in Emerging Economies

India’s diaper market is projected to grow from USD 1.996 billion in 2025 to USD 8.288 billion by 2035, driven by dual-income families, increased e-commerce access, and sanitation programs that are promoting disposable products in smaller cities[1]Government of India, “Swachh Bharat Mission Updates,” goi.gov.in. In Indonesia, rural areas lag behind with only 25% diaper penetration compared to 70% in Jakarta, creating a two-tiered demand pattern that favors low-basis-weight spunbond topsheets optimized for cost-sensitive consumers. North America is emerging as an export hub after Avgol installed a USD 100 million multi-beam line in Mocksville, North Carolina, in 2025 to supply premium hygiene materials to fast-growing Asian markets. Global players such as Procter & Gamble and Kimberly-Clark have localized converting operations in India, Vietnam, and Thailand, reducing lead times and enabling rapid SKU rollouts that combine spunbond polypropylene with natural fibers to cater to regional preferences.

Expansion of Medical Protective-Gear Market

Hospital procurement policies now require independent certification for 78% of surgical gown orders, up from 62% in 2024, reflecting stricter ANSI/AAMI PB70:2022 barrier standards. DuPont’s Tyvek APX 400 coveralls, launched in March 2026, demonstrate a shift toward breathable yet high-barrier spunbond-based laminates designed for clean-room and pharmaceutical environments. Reinforced SMS gowns accounted for 65% of 2025 revenue despite representing only 38% of shipped units, highlighting a premiumization trend driven by infection-control protocols for oncology and transplant surgeries. Harmonized ISO 13485:2016 quality-system standards have enabled Asian converters to serve Western hospitals under mutual-recognition agreements, accelerating cross-border trade and product registration timelines.

Cost- and Performance-Advantage over Woven Fabrics

Spunbond sheets are 30-40% cheaper per square meter than woven polypropylene because they eliminate the need for yarn spinning and weaving, with production speeds exceeding 600 meters per minute. Mechanical properties can be customized by adjusting polymer type, fiber denier, and thermal-bond settings, allowing converters to meet specific tensile and elongation requirements without over-engineering. In automotive trunk liners, spunbond polyester reduces weight by 20% compared to traditional needle-punched felts, helping automakers comply with U.S. CAFE and EU CO₂ regulations. Bulk-bag manufacturers are transitioning from woven polypropylene to spunbond due to its consistent pore structure, which ensures stable moisture-vapor transmission rates critical for agricultural and chemical packaging.

Brand-Owner Shift to Mono-Material PP Packaging

The PPWR, set to take effect in August 2026, mandates 100% recyclability by 2030 and a minimum recycled content of 30-35% for most packaging formats, prompting brands to replace multi-material laminates with single-polymer designs[2]European Commission, “Packaging and Packaging Waste Regulation,” europa.eu. Borealis’ HG485FB grade, introduced in January 2026, enables spunbond producers to meet barrier requirements without polyethylene layering, simplifying recycling processes. Fibertex Personal Care’s certified-circular spunbond, produced using SABIC TRUCIRCLE polypropylene via mass-balance feedstock recycling, is scaling beyond pilot volumes to meet the needs of hygiene companies facing eco-modulation fees from 2030. Suominen reported that plant-based inputs accounted for 62% of its raw materials in 2024, but recycled content remained at just 1%, indicating room for improvement before stricter PPWR penalties take effect.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns over polypropylene | -0.8% | Europe, North America, APAC (coastal/urban areas) | Medium term (2-4 years) |

| Volatility in propylene feedstock pricing | -1.1% | Global | Short term (≤ 2 years) |

| Machine-width limits for high-loft furniture grades | -0.4% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns over Polypropylene

Extended producer responsibility schemes in France, Germany, and the Netherlands now impose eco-modulation fees of up to 20% of product value on non-recyclable polypropylene items, increasing costs for converters still reliant on conventional spunbond. Mechanical recycling of post-consumer hygiene products remains challenging because adhesives and elastics degrade melt flow, keeping recycled-content inclusion below 5% in most commercial polypropylene grades. Fraunhofer’s solvent-based dissolution process reduces foreign-polymer contamination by 80% and produces yarns strong enough for geotextiles, but its capital-intensive solvent recovery requirements hinder widespread adoption. Advocacy groups emphasize that ASTM D6400 compostability standards require 90% degradation within 180 days, a benchmark traditional polypropylene spunbond cannot meet, exposing brand owners to accusations of greenwashing.

Volatility in Propylene Feedstock Pricing

While new steam-cracker capacity in China and the Middle-East reduced propylene prices by 3-5% through Q3 2025, the March 2026 Strait of Hormuz disruption caused a 20% spike in global polypropylene prices and increased container-freight rates by up to 35%. This volatility compressed converter margins and necessitated contract renegotiations. Japanese companies Asahi Kasei, Mitsui Chemicals, and Mitsubishi Chemical committed JPY 21.2 billion in January 2026 to decarbonize ethylene production, though benefits are not expected until after 2030, leaving short-term volatility unresolved. Indorama Ventures’ 2025 earnings revealed a 35% EBITDA decline in fibers due to regional feedstock price disparities, illustrating the challenges even integrated producers face when arbitrage opportunities diminish. This volatility is expected to reduce the global CAGR by 1.1 percentage points until supply routes stabilize and derivative hedging becomes more accessible to mid-scale converters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: PP Dominance Challenged by Bio-Based Entrants

Polypropylene retained a 55.18% share of the spunbond nonwovens market size in 2025 on the back of low raw-material costs and high throughput, yet other material types are moving quickly, with PLA, nylon, etc. forecast at a 7.24% CAGR to 2031. Polyester commands the durable niche because of its elevated tensile performance, winning share in automotive interiors and geotextiles, even at a 20% price premium. NatureWorks’ Ingeo 6500D PLA, which carries a 62% lower carbon footprint than PP, is being adopted for hygiene topsheets as converters pursue PPWR incentives. With global PLA capacity expected to double to roughly 1 million tons by 2026, availability fears that once dampened adoption are fading. On the polypropylene side, Borealis’ HG485FB grade is expanding the mono-material design window, helping converters keep ahead of recyclability mandates without costly equipment upgrades. Nylon spunbond remains niche but could scale once chemical-recycling ventures such as Samsara Eco’s plant come on-stream in 2028.

Second-generation mechanical recyclers like Kipas and Meltem Kimya are opening feedstock taps for GRS-certified rPET chips, letting spunbond producers hit PPWR recycled-content targets without surrendering mechanical performance. These shifts frame a two-track outlook: PP holds near-term cost advantage; bio-based and recycled alternatives climb the value chain as regulation and consumer scrutiny tighten. Overall, polymer diversification raises switching costs for converters and could spur more joint ventures between resin makers and roll-goods suppliers to secure forward offtake.

By Function: Durable Gains Outpace Disposable Revenue

Disposable function occupied 48.60% of 2025 revenue, with diapers, feminine care, and wipes absorbing the lion’s share of tonnage. The segment is price-sensitive but enormous; incremental basis-weight reductions and surfactant treatments still deliver meaningful margin lifts, keeping it attractive despite saturation in mature economies. In contrast, durable functions are expanding at a 7.12% CAGR through 2031 as infrastructure spending and automotive lightweighting accelerate. The spunbond nonwovens market share for geotextiles is expanding in tandem with Saudi, Indian, and Brazilian public-works budgets, each of which embeds spunbond specifications into tender documents. Automotive demand is moving toward recycled-content polyester substrates that balance durability with circular-economy mandates; European OEMs already require 25% recycled plastic content per vehicle.

Filtration media, although smaller in tonnage, carry margins 40-60% above commodity hygiene grades because pleat stability and chemical resistance are mission-critical for HVAC and industrial cartridges. Agriculture covers remain seasonal but benefit from climate change pressures that stretch growing seasons and water-use rules. Furniture and bedding applications are partially constrained by installed machine widths yet retrofit programs using wider blown-air systems are underway, indicating future upside once capacity is in place.

By Application: Medical Outgrows Hygiene on Regulatory Tailwinds

Personal hygiene retained a 42.45% revenue slice in 2025, but its growth curve is flattening in urban China and Europe, where diaper and feminine-care usage is near the biological maximum. Medical, on the other hand, is riding a 7.30% CAGR through 2031 crest thanks to ANSI/AAMI PB70:2022 and national strategic-stockpile replenishment that require higher-barrier gowns and drapes. DuPont’s renewable-attribution Tyvek has become a template for low-carbon medical packaging that eases Scope 3 accounting for device OEMs. Mono-material packaging spunbond is another breakout application; HG485FB polypropylene lets converters replace outdated laminate sacks and FIBCs with PP-only structures that slide cleanly through existing recycling plants, a key condition under PPWR.

Other applications, notably automotive acoustics and filtration, are set to climb as regulatory frameworks like ASHRAE 52.2 and ISO 16890 tighten particulate thresholds. Agriculture fabrics using UV-stabilized spunbond PP now receive subsidy support in Mediterranean regions and parts of Brazil, rewarding growers with longer seasons and reduced pesticide spend. Furniture upholstery is a niche but profitable one; high-loft polyester nonwovens containing recycled fibers align with mattress producers’ circular-economy commitments.

Geography Analysis

Asia-Pacific locked in 39.10% of global revenue in 2025, supported by China’s 1.2 million-ton installed capacity and India’s double-digit diaper growth. Chinese consolidation, Zhejiang Kingsafe ranked eighth worldwide with USD 840 million sales in 2024, signals an industry pivot from commodity grades to higher-margin medical and filtration niches. Japan’s landscape shifted after 2025, when Teijin and Asahi Kasei merged technical-textile units, while Toray closed unprofitable PP lines under its Darwin cost-saving program. Southeast Asia remains the frontier; Indonesia and Vietnam boast rural diaper penetration below 30%, so regional suppliers are adding basis-weight-optimized lines to capture first-time users.

North American dynamics are shaped by vertical integration and nearshoring. Avgol’s Mocksville plant addresses domestic hygiene needs but also exports to Asia, leveraging U.S. logistics resilience. FDA surgical-gown regulations steer hospital buyers toward ISO-13485-certified local or mutual-recognition suppliers, limiting penetration by low-cost Asian imports in critical medical grades. Canada and Mexico act as auxiliary hubs under USMCA, giving U.S. brands tariff-free, three-day truck access to converted goods.

Europe is firmly in regulatory overdrive as PPWR applicability arrives in August 2026. Borealis, Fibertex, and Suominen are pouring funds into compliant mono-material lines, and German OEMs are scrutinizing supply chains to guarantee post-consumer resin inclusion. Infrastructural geotextile demand is shifting toward Nordic countries, where coastal-protection projects soak up spunbond rolls that Russian customers would previously have taken. Middle-East and Africa is the fastest-growing region at a 7.04% CAGR through 2031, buoyed by Vision 2030 rail corridors and desalination plants that specify spunbond underlayers, and by Egypt’s burgeoning hygiene complex where Gülsan runs 40,000 tons per year of installed capacity. South America is smaller but accelerating: Brazil and Argentina combine low rural hygiene penetration with state-backed sanitation drives, and Fitesa’s USD 1.2 billion sales underline the region’s scaling potential.

Competitive Landscape

Global supply is moderately fragmented. Strategic themes cluster around polymer integration, sustainability positioning, and capacity pruning. Borealis invested EUR 49 million in new Borstar Nextension capabilities to guarantee downstream spunbond grades that meet PPWR rules. DuPont and Fibertex are pushing renewable or circular feedstocks, certified under ISCC PLUS, to lock in brand-owner demand. Toray has exited commodity PP spunbond via its Darwin Project, closing lines that soaked up cash but delivered poor return.

Private equity is sniffing technical niches; the CorpAcq buyout of NONWOVENN in January 2026 shows appetite for specialty assets that serve protective clothing and wound-care verticals. Digitalization is another differentiator. Indorama Ventures unified 95% of enterprise data by early 2025, letting AI optimize working capital and lift fiber-segment EBITDA 43% quarter over quarter, even as raw-material spreads tightened. Equipment makers are responding with wider machines such as Reifenhäuser’s RF6, which debuted at INDEX 2026 and promises 15-20% energy savings per ton alongside inline hyperspectral basis-weight control better than ±2%. Complying with ISO 13485 and ASTM F2407 is now table stakes for medical supply contracts, further narrowing the field to certified players.

Spunbond Nonwovens Industry Leaders

Amcor plc

Fitesa S.A.

Mitsui Chemicals, Inc.

KCWW

Indorama Ventures Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Indorama Ventures Public Company Limited inaugurated a USD 100 million high-speed, 3-layer laminated, multiple-beam nonwovens production line at its Mocksville, NC facility. This expansion significantly boosted the production capacity for sustainable high-loft and spunbond materials, catering to the baby diaper, adult incontinence, and feminine hygiene markets in North America.

- May 2024: Mitsui Chemicals, Inc. developed EcoRISETM PLA spunbond nonwoven, a compostable material designed for agricultural and packaging applications. The product decomposed into water and carbon dioxide, complying with certification standards from BPI (U.S.), TÜV AUSTRIA, and the Japan BioPlastics Association (JBPA).

Global Spunbond Nonwovens Market Report Scope

Spunbond nonwovens are nonwoven textiles manufactured through a continuous process that involves spinning polymer chips into continuous filaments, arranging them into a web, and bonding the web using heat and pressure. This process eliminates the need for traditional weaving or knitting, enabling faster and more cost-efficient production of textiles with high tensile strength and durability.

The Spunbond Nonwovens Market is segmented by material type, function, application, and geography. By material type, the market is segmented into polypropylene (PP), polyester (PET), polyethylene (PE), and other material types (e.g., nylon, PLA). By function, the market is segmented into disposable and durable. By application, the market is segmented into personal hygiene, medical, packaging, and other applications (e.g., automotive, filtration, agriculture, furniture). The report also covers the market size and forecasts for spunbond nonwovens in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Polypropylene (PP) |

| Polyester (PET) |

| Polyethylene (PE) |

| Other Material Types (Nylon, PLA, etc.) |

| Disposable |

| Durable |

| Personal Hygiene |

| Medical |

| Packaging |

| Other Applications (Automotive, Filtration, Agriculture, Furniture, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Polypropylene (PP) | |

| Polyester (PET) | ||

| Polyethylene (PE) | ||

| Other Material Types (Nylon, PLA, etc.) | ||

| By Function | Disposable | |

| Durable | ||

| By Application | Personal Hygiene | |

| Medical | ||

| Packaging | ||

| Other Applications (Automotive, Filtration, Agriculture, Furniture, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the spunbond nonwoven market?

The spunbond nonwoven market stands at USD 19.29 billion in 2026 and is projected to reach USD 25.94 billion by 2031.

Which material type dominates sales in 2025?

Polypropylene retains the lead with 55.18% of 2025 revenue, although bio-based alternatives are the fastest-growing segment.

Why are durable spunbond wovens growing fastest through 2031?

Infrastructure investment, automotive lightweighting, and stricter filtration requirements are lifting demand for durable spunbond wovens to a 7.12% CAGR through 2031.

How does the PPWR influence product design?

The regulation requires 100% recyclable packaging and at least 30-35% recycled content by 2030, pushing brands to adopt mono-material polypropylene structures that can flow through existing recycling systems.

Page last updated on: