Cashew Nut Shell Liquid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 1.11 Million tons |

| Market Volume (2031) | 1.41 Million tons |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

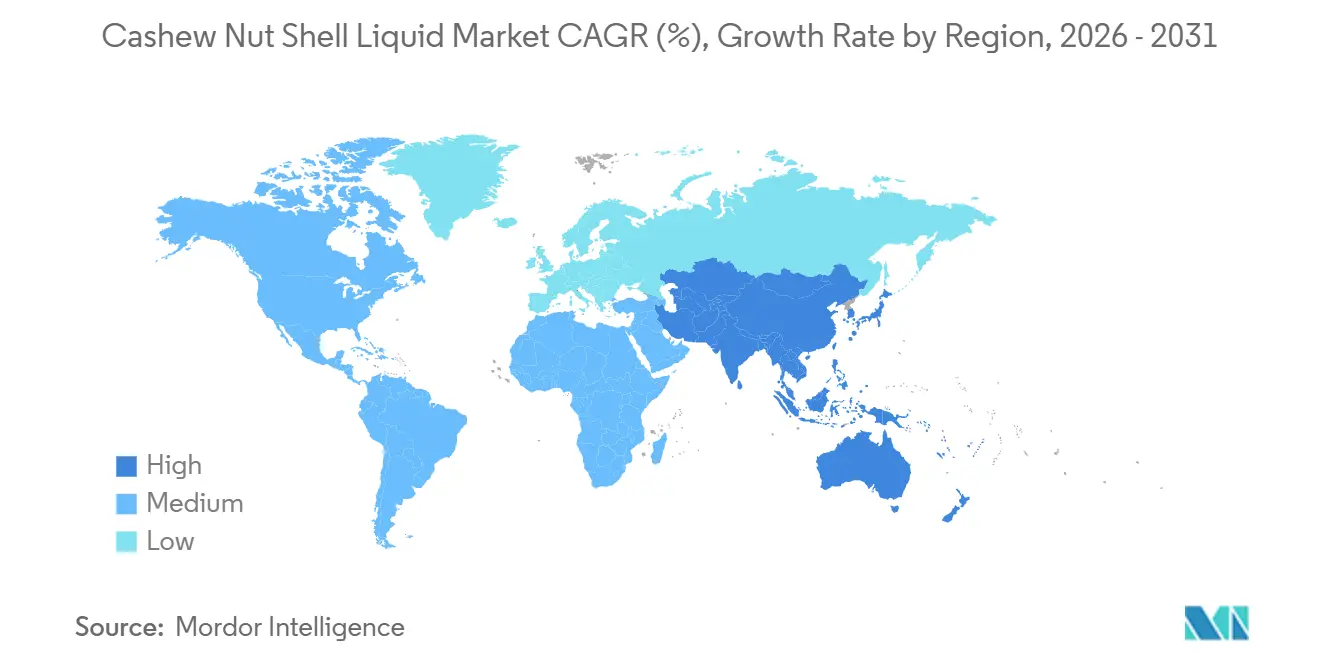

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cashew Nut Shell Liquid Market Analysis by Mordor Intelligence

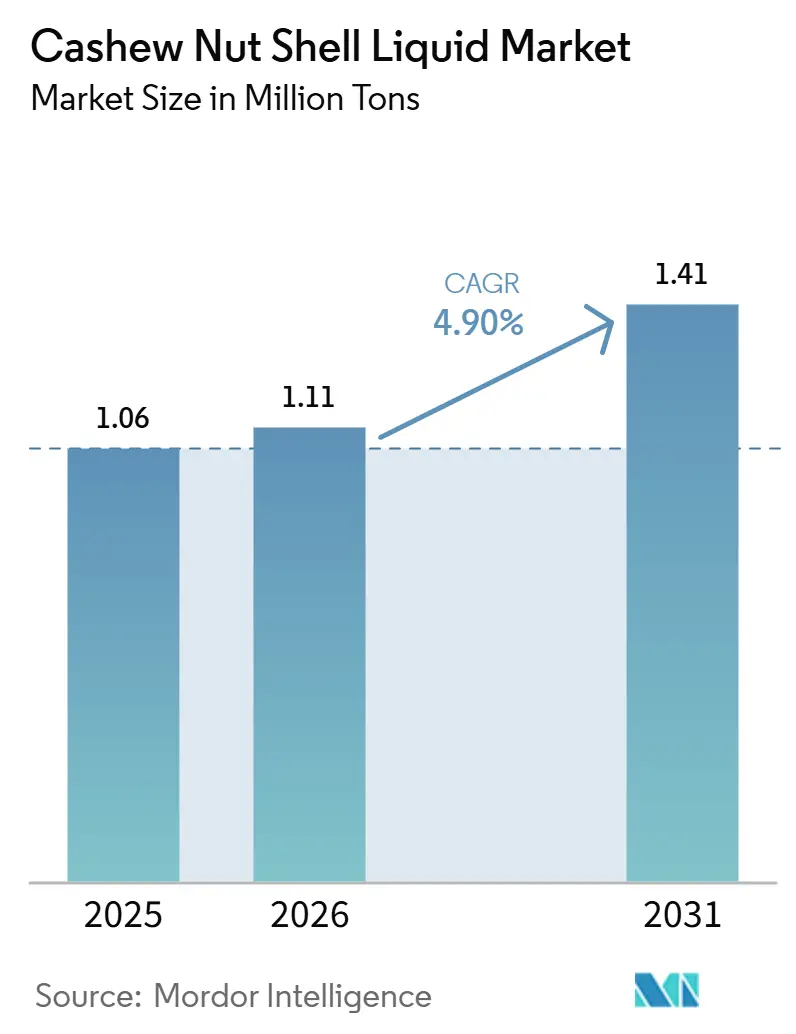

The Cashew Nut Shell Liquid Market size was valued at 1.06 million tons in 2025 and is estimated to grow from 1.11 million tons in 2026 to reach 1.41 million tons by 2031, at a CAGR of 4.90% during the forecast period (2026-2031). The demand for phenolic bio-resins is influenced by changes in automotive friction-material formulations, marine-coating regulations, and wind-energy blade manufacturing, which increasingly prefer these bio-resins over petroleum-derived alkyl-phenols. Technical CNSL (Cashew Nut Shell Liquid) is primarily used in friction and industrial coatings, while cardanol, a high-purity derivative, is gaining market share as downstream manufacturers enforce stricter impurity limits on epoxy curing agents. Solvent extraction remains the primary method for feedstock production; however, supercritical CO₂ processes are expanding in specialty-grade applications where residue-free cardanol is required. The Asia-Pacific region holds the largest market share, supported by India's processing capabilities and Vietnam's export-focused refineries. Growth in end-use applications is driven by the building and construction sector, as green-building initiatives accelerate the adoption of bio-based adhesives and coatings.

Key Report Takeaways

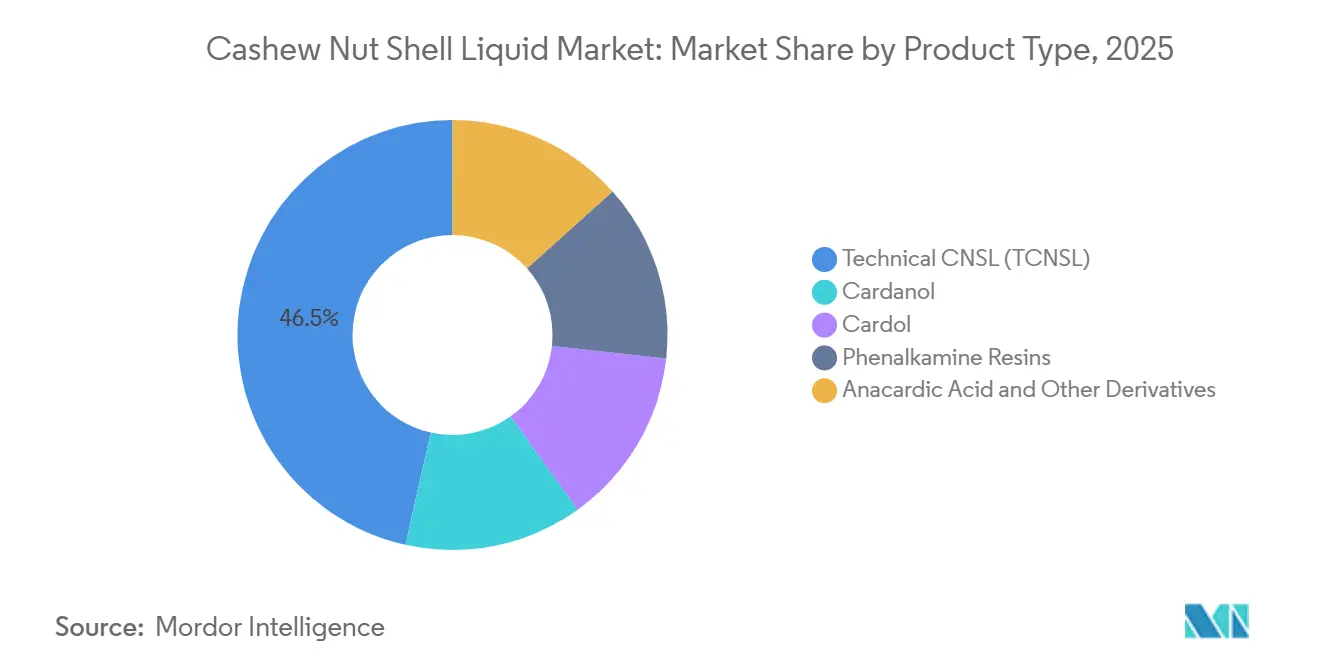

- By product type, technical CNSL led with 46.5% of the Cashew Nut Shell Liquid market share in 2025, while cardanol is forecast to expand at a 5.12% CAGR through 2031.

- By grade, distilled and refined material accounted for 5.23% CAGR growth potential between 2026-2031, outpacing technical grade’s 42.1% volume base.

- By extraction method, solvent extraction captured 42.5% of the Cashew Nut Shell Liquid market size in 2025; supercritical CO₂ routes are projected to climb at a 5.1% CAGR over 2026-2031.

- By application, friction materials held 35.5% of volume in 2025, whereas paints and coatings are advancing at a 5.21% CAGR to 2031.

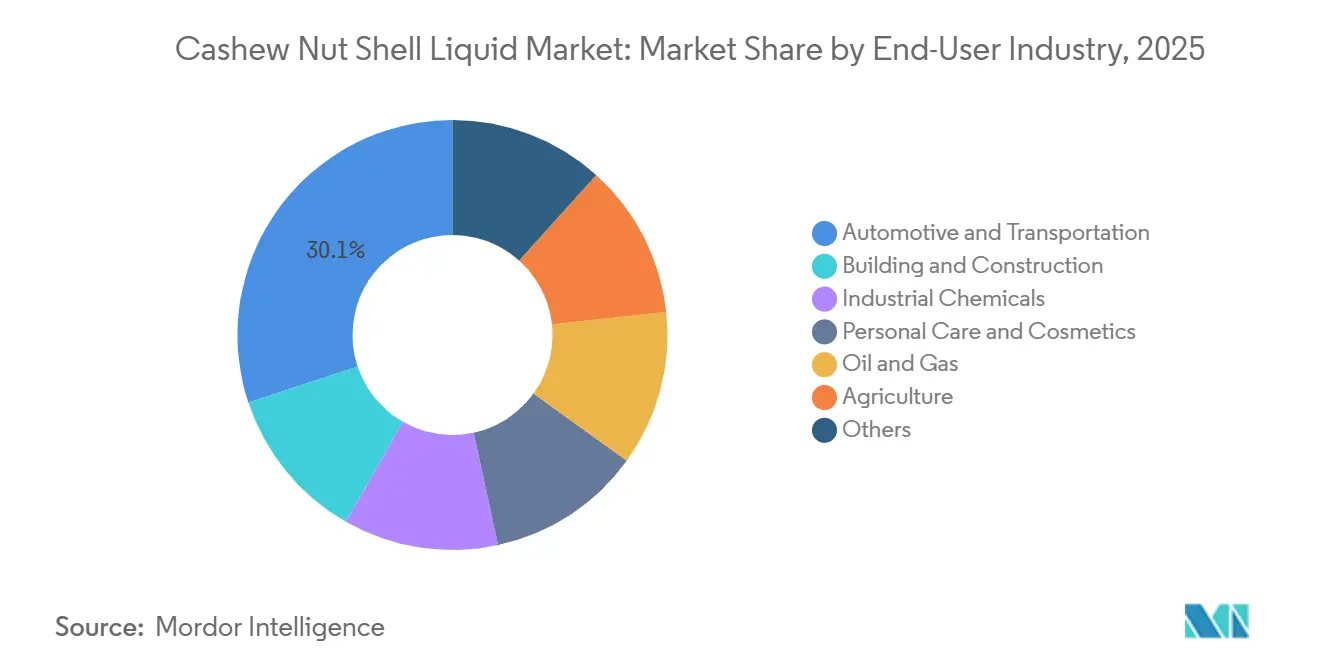

- By end-user, the automotive and transportation segment commanded 30.1% share of the Cashew Nut Shell Liquid market in 2025, while building and construction is projected to post the fastest 5.3% CAGR through 2031.

- By geography, Asia-Pacific held 39.1% share in 2025 and is forecast to grow at a 5.25% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cashew Nut Shell Liquid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing OEM demand for high-performance friction linings | +1.2% | Global, with concentration in Asia-Pacific automotive hubs (India, China, Thailand) and North America heavy-duty vehicle markets | Medium term (2-4 years) |

| Regulatory push for bio-based, low-VOC industrial coatings | +1.5% | North America & EU (IMO marine regulations, EPA Safer Choice), spill-over to APAC export-oriented manufacturers | Long term (≥ 4 years) |

| Expansion of wind-energy blade manufacturing composites | +0.8% | Europe (offshore wind), North America, China (onshore/offshore capacity additions) | Long term (≥ 4 years) |

| Shift to phenalkamine curing agents in marine epoxy systems | +0.9% | Global maritime routes; EU and North America shipyards; Asia-Pacific ship-repair facilities (Singapore, South Korea) | Medium term (2-4 years) |

| Rapid adoption of CNSL-based bio-pesticides in agro-chemicals | +0.6% | Asia-Pacific (India, Vietnam, Indonesia), Sub-Saharan Africa, South America (Brazil) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing OEM Demand for High-Performance Friction Linings

Automotive and commercial vehicle manufacturers are replacing conventional phenol-formaldehyde with cardanol-based phenolic resins in brake pads to comply with stricter particulate emission and copper content regulations. This shift is driven by European Union (EU) Regulation 2019/631 and China’s National VI standards. Additionally, electric vehicle platforms require friction materials capable of handling infrequent but high-energy braking events[1]Cardolite Corporation, “High-Bio Phenalkamine Curing Agents,” cardolite.com. In response to rising demand, Palmer International expanded its Texas production capacity in 2025, following reports of significant growth in orders for bio-based linings from North American truck original equipment manufacturers (OEMs). Peer-reviewed studies indicate that cashew nutshell liquid (CNSL)-phenolic composites offer improved wear resistance and reduced noise, vibration, and harshness, supporting their increased usage. Indian suppliers based in Chennai and Pune are utilizing domestic feedstock and International Organization for Standardization (ISO) 9001 certification to fulfill global contracts, further strengthening the Asia-Pacific region's position in this market.

Regulatory Push for Bio-Based, Low-VOC Industrial Coatings

The International Maritime Organization's Volatile Organic Compound (VOC) caps and national ecolabels support phenalkamine-cured epoxies due to their ability to cure efficiently at low temperatures and their high renewable-carbon content. Cardolite’s LITE 514HP, introduced in May 2025, exceeds ASTM B117 salt-spray thresholds of 3,000 hours, making it suitable for applications such as offshore wind towers and marine hulls. Regulatory programs like the European Union Registration, Evaluation, Authorization, and Restriction of Chemicals (EU REACH) and the United States Environmental Protection Agency (U.S. EPA) Safer Choice discourage the use of nonylphenol ethoxylates, increasing demand for cardanol-based diluents despite their higher cost. European buyers consistently pay a 15-20% premium for distilled Cashew Nut Shell Liquid (CNSL) accompanied by traceability documentation, establishing a structural price floor for high-purity supply.

Expansion of Wind-Energy Blade Manufacturing Composites

Recyclable epoxy matrices synthesized from cardanol enable chemical depolymerization, facilitating glass-fiber recovery at the end of their lifecycle. This development was validated through laboratory trials in 2025[2]Scientific Reports, “Lipidomics of Solvent-Extracted CNSL,” nature.com . Additionally, extrudable cardanol epoxies have been successfully three-dimensional (3D) printed into wood-composite components, reducing mold waste and tooling time. Offshore projects in the North Sea and the United States (U.S.) Atlantic is increasingly adopting these resins to meet circular economy objectives. Meanwhile, China's expanding onshore wind market is driving demand as domestic formulators explore bio-based epoxy alternatives.

Shift to Phenalkamine Curing Agents in Marine Epoxy Systems

Shipyards in Europe, South Korea, and Singapore have reported faster turnaround times after replacing polyamide hardeners with cardanol-derived phenalkamines, which cure at temperatures below 0 degrees Celsius. The long aliphatic side chain enhances flexibility, reducing the risk of cracking on tanker hulls subjected to thermal cycling. The implementation of International Maritime Organization (IMO) sulfur-cap regulations has increased dry-dock costs, making operators prioritize coatings that extend maintenance intervals. Phenalkamines' early water resistance minimizes downtime, further supporting this transition.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cashew crop yields and raw-shell pricing | -0.9% | Global, acute in West Africa (Ivory Coast, Ghana, Benin), India (import-dependent processors), Vietnam (export-oriented) | Short term (≤ 2 years) |

| Availability of low-cost synthetic alkyl-phenols | -0.5% | Asia-Pacific (China, India, price-sensitive adhesive/plasticizer markets), South America | Medium term (2-4 years) |

| Scale-up challenges for supercritical CO₂ extraction | -0.3% | Global, particularly in Africa and South America, where capital access limits technology adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Cashew Crop Yields and Raw-Shell Pricing

Unpredictable monsoons and pest outbreaks have resulted in feedstock shortages, increasing shell prices, and reducing processor margins. In the first quarter (Q1) of 2026, India experienced a notable decline in raw-nut imports due to logistical challenges in West Africa. This situation led to smaller extractors halting operations and raised refined-grade prices to USD 975-1,025 per ton. West African countries continue to utilize most shells for energy, foregoing potential extraction revenue and contributing to global supply fluctuations. Integrated players with plantation connections secure long-term contracts, while spot buyers face margin pressures during periods of crop shortages.

Availability of Low-Cost Synthetic Alkyl-Phenols

Chinese nonylphenol is priced 20-30% lower than cardanol, making it a cost-effective option for formulators in adhesives and plasticizers that do not require strict ecological labeling compliance. While regulators in the European Union (EU) and the United States (U.S.) continue to impose restrictions on nonylphenol ethoxylates, enforcement gaps in emerging markets sustain the demand for lower-cost petro-phenols. The cost difference narrows in ultra-light-color grades, where advanced refinery technologies, such as wiped-film distillation, reduce impurities and produce higher-value cardanol. However, the availability of these higher-grade volumes remains limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technical CNSL Dominates, Cardanol Gains on Purity Demands

Technical Cashew Nut Shell Liquid (CNSL) is expected to account for 46.5% of the volume in 2025, reflecting its cost efficiency in friction materials and generic industrial coatings. Cardanol is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.12%, driven by demand from epoxy and phenalkamine formulators requiring specifications such as Gardner color less than or equal to 1, potassium content below 10 parts per million (ppm), and a consistent amine value.

Distillation processes concentrate cardanol to 78% purity, enabling formulators to meet Original Equipment Manufacturer (OEM) requirements for electric vehicle brake systems and marine coatings that cure at sub-zero temperatures. Margin pressures caused by raw-shell price volatility are encouraging Indian and Vietnamese processors to expand wiped-film and ion-exchange purification lines to capture higher value from specialty derivatives. Additionally, phenalkamine resins remain a profitable sub-segment, with prices reaching up to USD 3,500 per ton for offshore coating applications.

By Grade: Distilled and Refined Grades Lead Quality Migration

Distilled and refined grades are projected to grow at a Compound Annual Growth Rate (CAGR) of 5.23% through 2031, driven by downstream demand for consistent chemical profiles and low trace metal content in high-end composites. In 2025, technical grade accounted for 42.1% of the Cashew Nut Shell Liquid market size; however, its market share is expected to decline as global Original Equipment Manufacturers (OEMs) standardize supplier quality audits.

European importers pay up to 20% more for Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant refined materials, creating a price differential that supports technology upgrades in Asia-Pacific production facilities. Acid-grade output continues to cater to niche wood-adhesive applications, although many plywood manufacturers are transitioning to low-formaldehyde cardanol options, which offer improved performance compared to traditional phenol-formaldehyde binders.

By Extraction Method: Solvent Leads, Supercritical CO₂ Gains in Specialty

Solvent extraction accounted for 42.5% of the volume in 2025, due to its efficiency in yield and preservation of anacardic acid, which is essential for biopesticide production. Supercritical Carbon Dioxide (CO₂) methods represented only 5% of the 2025 throughput but are projected to grow at a Compound Annual Growth Rate (CAGR) of 5.1%, driven by increasing demand from pharmaceutical and cosmetic industries for solvent-free products.

Mechanical pressing remains widely used among small-scale African processors where limited capital constrains technology adoption. However, its higher fiber content restricts its applications to biodiesel and boiler fuel production. Thermal cracking continues to be utilized due to its simplicity, but it compromises cardanol yield and produces polymeric residue, reducing its competitiveness in export markets that require light-colored feedstock.

By Application: Friction Materials Hold Share, Paints and Coatings Accelerate

Friction materials accounted for 35.5% of demand in 2025, supported by their established use in asbestos-free and copper-reduced brake pads. The paints and coatings segment is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.21%, driven by demand from shipyards and offshore wind developers for rapid-cure, corrosion-resistant epoxies. Adhesives and laminates are benefiting from global formaldehyde regulations, while polymers and composites are gaining visibility due to applications such as recyclable wind blades and 3D-printed tooling.

Surfactants, plasticizers, and niche chemical intermediates represent smaller market segments but achieve higher margins, particularly in cases where cardanol substitutes phthalates in Polyvinyl Chloride (PVC) or nonylphenol ethoxylates in personal care products.

By End-User Industry: Automotive Leads, Building and Construction Fastest

The automotive segment accounted for a 30.1% market share in 2025, driven by the prevalence of friction materials. However, growth in this segment is expected to moderate as regenerative braking systems extend the lifespan of brake pads. The building and construction segment is anticipated to lead with a projected Compound Annual Growth Rate (CAGR) of 5.3%, supported by the adoption of Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM) certifications for low-Volatile Organic Compound (VOC), bio-based coatings, and wood adhesives.

Industrial chemicals represent a stable mid-stream application, converting Cashew Nut Shell Liquid (CNSL) into products such as phenalkamines, glycidyl ethers, and polyols. In the personal care industry, formulators procure small but high-margin quantities of pharmaceutical-grade cardanol. Meanwhile, the oil and gas sector relies on phenalkamine-cured epoxies for the maintenance of subsea pipelines and offshore platforms.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 39.1% of the Cashew Nut Shell Liquid (CNSL) market and is projected to grow at a compound annual growth rate (CAGR) of 5.25% from 2026 to 2031. India processes approximately 45% of the global CNSL supply, benefiting from its proximity to cashew farms. Vietnam focuses on exporting refined CNSL grades, which are priced higher in European and North American markets. Meanwhile, China’s resin producers are advancing research on cardanol-epoxy systems to localize supply chains and reduce import dependency. This is supported by multiple peer-reviewed studies in 2025 on graphene-reinforced cardanol matrices.

North America sources the majority of its CNSL feedstock from Asia but maintains strong demand for high-performance applications, such as friction binders and phenalkamine coatings. Palmer International’s capacity expansion in 2025 reflects robust downstream orders, particularly from electric vehicle platforms that require bio-based materials. Additionally, Canada’s wind energy sector is incorporating cardanol epoxies in blade repair resins, further expanding the market’s addressable volume.

Europe remains the largest importer of refined and distilled CNSL grades, often paying traceability premiums to meet the requirements of Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) and Ecolabel certifications. Nordic countries are prioritizing recyclable epoxy systems for offshore wind projects, driving research and development efforts. These initiatives are supported by circular-economy grants that align with CNSL chemistry advancements.

South America, despite its abundance of raw cashew nuts, extracts limited volumes of CNSL. Brazilian researchers are pioneering new applications for CNSL, but industrialization in the region is hindered by capital shortages. The Middle East and Africa exhibit modest CNSL offtake. However, West Africa’s surplus of raw cashew nuts presents an opportunity for localized extraction, which could enable the region to capture more value within the supply chain.

Competitive Landscape

The cashew nut shell liquid market is moderately concentrated. A concentrated group of derivative specialists, including Cardolite, SI Group, Elementis, and Palmer International, dominates the market with expertise in phenalkamine synthesis and epoxy-novolac modification, supported by numerous regional processors. Cardolite's planned doubling of its Mangalore production capacity by 2025 aims to secure the supply of its marine-coating curing agents. Meanwhile, SI Group's USD 1.7 billion balance-sheet recapitalization is set to fund pipeline innovations and expand its market presence through a strategic alliance with Azelis in October 2025.

Element Solutions is consolidating its specialty-chemical platforms, including cashew nutshell liquid (CNSL)-derived surfactants, through acquisitions of Micromax and EFC, valued at nearly USD 870 million combined, by 2026. In India and Vietnam, fragmented processors are upgrading their facilities with distillation columns to compete in the production of ultra-light-color grades, raising technological standards for new entrants. African processors, on the other hand, continue to focus on low-cost thermal cracking. However, as European and U.S. customers increasingly audit supply chains for carbon footprint, there is a growing preference for traceable and higher-purity feedstock.

Emerging opportunities include bio-lubricants leveraging cardanol's oxidative stability and low-temperature fluidity, as well as carbon materials for supercapacitors. Start-ups are collaborating with university consortia to develop recyclable wind-blade resins and anacardic-acid-based biopesticides, though large-scale commercialization remains several years away. High intellectual-property intensity and stringent regulatory compliance create significant entry barriers, favoring incumbents with robust research and development (R&D) capabilities and global logistics networks.

Cashew Nut Shell Liquid Industry Leaders

Cardolite Corporation

GHW (VIETNAM) CO., LTD

Palmer International

Golden Cashew Products Pvt. Ltd.

LC BUFFALO CO., LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Element Solutions Inc. completed the acquisitions of Micromax for USD 500 million and Enthone Functional Coatings (EFC) for USD 369 million. These acquisitions have strengthened its specialty chemical portfolio by incorporating surfactants and additives derived from cashew nut shell liquid, a renewable resource widely used in industrial applications.

- May 2025: Cardolite Corporation expanded its production capacity in Mangalore and introduced LITE 514HP, a high-bio phenalkamine derived from cashew nut shell liquid. This product is designed to cure at temperatures below 5 degrees Celsius and provides over 3,000 hours of resistance under ASTM B117 salt-spray testing.

Global Cashew Nut Shell Liquid Market Report Scope

Cashew Nut Shell Liquid, also known as cashew nut shell oil, is a dark reddish-brown, viscous liquid extracted from the honeycomb structure of the cashew nut shell. It is a by-product of the cashew industry, previously considered agricultural waste but now utilized as a bio-based alternative to petroleum-derived chemicals.

The cashew nut shell liquid market is segmented by product type, grade, extraction method, application, end-user industry, and geography. By product type, the market is segmented into technical cnsl (tcnsl), cardanol, cardol, phenalkamine resins, and anacardic acid and other derivatives. By grade, the market is segmented into technical grade, acid grade, and distilled/refined grade. By the extraction method, the market is segmented into mechanical press, solvent extraction, distillation and vacuum distillation, super-critical co₂ extraction, and thermal cracking. By application, the market is segmented into friction materials, paints and coatings, adhesives and laminates, surfactants and plasticizers, polymer and composites, chemical intermediates, and other niche uses (bio-lubricants, carbon materials). By end-user industry, the market is segmented into automotive and transportation, building and construction, industrial chemicals, personal care and cosmetics, oil and gas, agriculture, and others. The report also covers the market size and forecasts for cashew nut shell in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Technical CNSL (TCNSL) |

| Cardanol |

| Cardol |

| Phenalkamine Resins |

| Anacardic Acid and Other Derivatives |

| Technical Grade |

| Acid Grade |

| Distilled / Refined Grade |

| Mechanical Press |

| Solvent Extraction |

| Distillation and Vacuum Distillation |

| Super-critical CO₂ Extraction |

| Thermal Cracking |

| Friction Materials |

| Paints and Coatings |

| Adhesives and Laminates |

| Surfactants and Plasticizers |

| Polymer and Composites |

| Chemical Intermediates |

| Other Niche Uses (Bio-lubricants, Carbon Materials) |

| Automotive and Transportation |

| Building and Construction |

| Industrial Chemicals |

| Personal Care and Cosmetics |

| Oil and Gas |

| Agriculture |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Technical CNSL (TCNSL) | |

| Cardanol | ||

| Cardol | ||

| Phenalkamine Resins | ||

| Anacardic Acid and Other Derivatives | ||

| By Grade | Technical Grade | |

| Acid Grade | ||

| Distilled / Refined Grade | ||

| By Extraction Method | Mechanical Press | |

| Solvent Extraction | ||

| Distillation and Vacuum Distillation | ||

| Super-critical CO₂ Extraction | ||

| Thermal Cracking | ||

| By Application | Friction Materials | |

| Paints and Coatings | ||

| Adhesives and Laminates | ||

| Surfactants and Plasticizers | ||

| Polymer and Composites | ||

| Chemical Intermediates | ||

| Other Niche Uses (Bio-lubricants, Carbon Materials) | ||

| By End-User Industry | Automotive and Transportation | |

| Building and Construction | ||

| Industrial Chemicals | ||

| Personal Care and Cosmetics | ||

| Oil and Gas | ||

| Agriculture | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current market size of Cashew Nut Shell Liquid Market?

The Cashew Nut Shell Liquid Market size was valued at 1.06 million tons in 2025 and is estimated to grow from 1.11 million tons in 2026 to reach 1.41 million tons by 2031, at a CAGR of 4.90% during the forecast period (2026-2031).

What application area is growing fastest for CNSL derivatives?

Paints and coatings, especially marine and wind-energy systems, are projected to rise at a 5.21% CAGR as phenalkamine technology displaces conventional curing agents.

Why is Asia-Pacific the dominant regional market?

India and Vietnam process more than 60% of global shells, and regional end-use sectors, automotive, construction, and export-oriented coatings, drive sustained demand.

Which CNSL grade commands the highest premium?

Distilled and refined cardanol, meeting Gardner less than or equal to 1 and potassium less than 10 ppm, earns up to 20% more than technical grade due to stringent OEM quality standards.

Page last updated on: