Geofoams Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

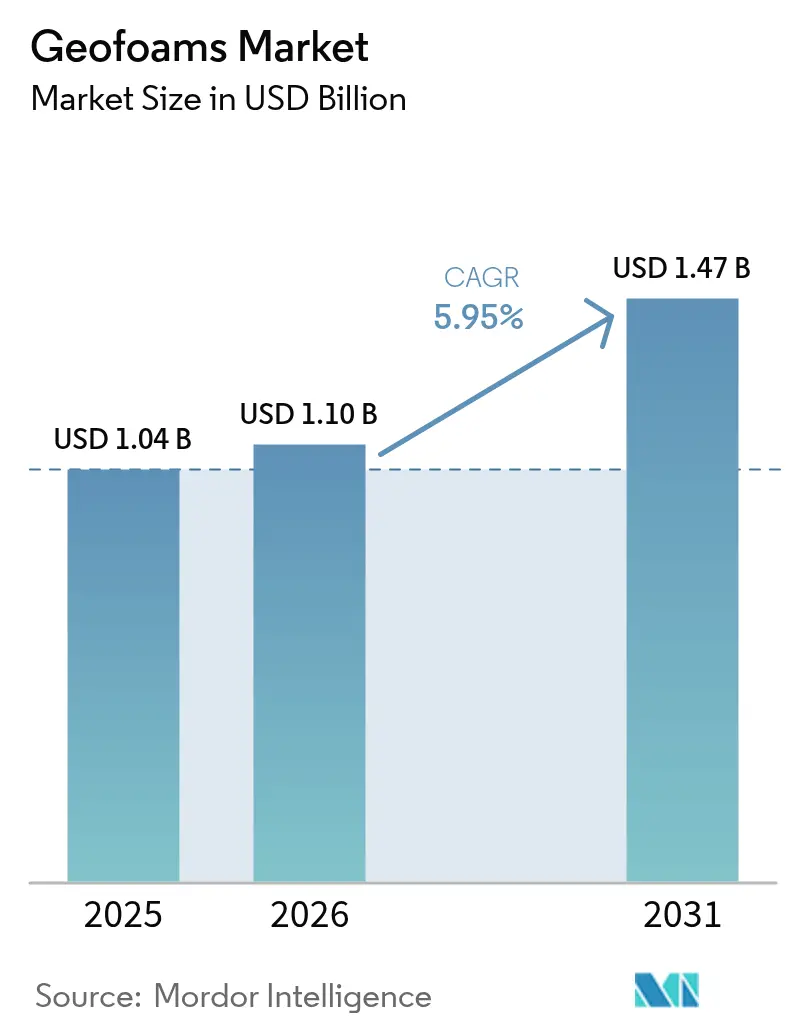

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

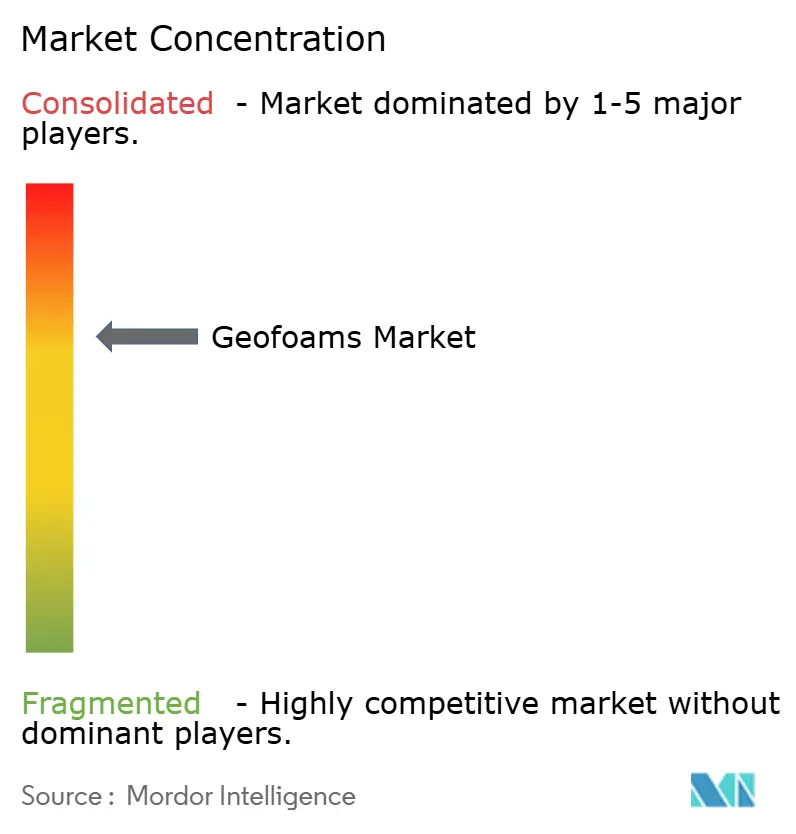

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geofoams Market Analysis by Mordor Intelligence

The Geofoams Market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.10 billion in 2026 to reach USD 1.47 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031). Infrastructure renewal, lightweight construction trends and growing sustainability mandates collectively underpin demand, while expanded and extruded polystyrene technologies redefine conventional earth-fill approaches. Accelerated capital expenditure on highways, bridges and urban transit systems in Asia-Pacific and North America is translating directly into larger bid volumes for geofoam blocks, especially where weak soils or seismic risk constrain traditional backfills. Design‐build contractors increasingly value geofoam’s factory-controlled consistency and fast installation times, reducing lane-closure periods on heavily trafficked corridors. Meanwhile, heightened regulatory interest in embodied-carbon disclosure is elevating the material’s lifecycle cost advantages relative to granular fills. Competitive differentiation now hinges on vertical integration into polystyrene supply, recycled-content development and fire-retardant chemistry.

Key Report Takeaways

- By material technology, expanded polystyrene commanded 64.54% of geofoams market share in 2025. Extruded polystyrene is projected to register the fastest 6.37% CAGR through 2031.

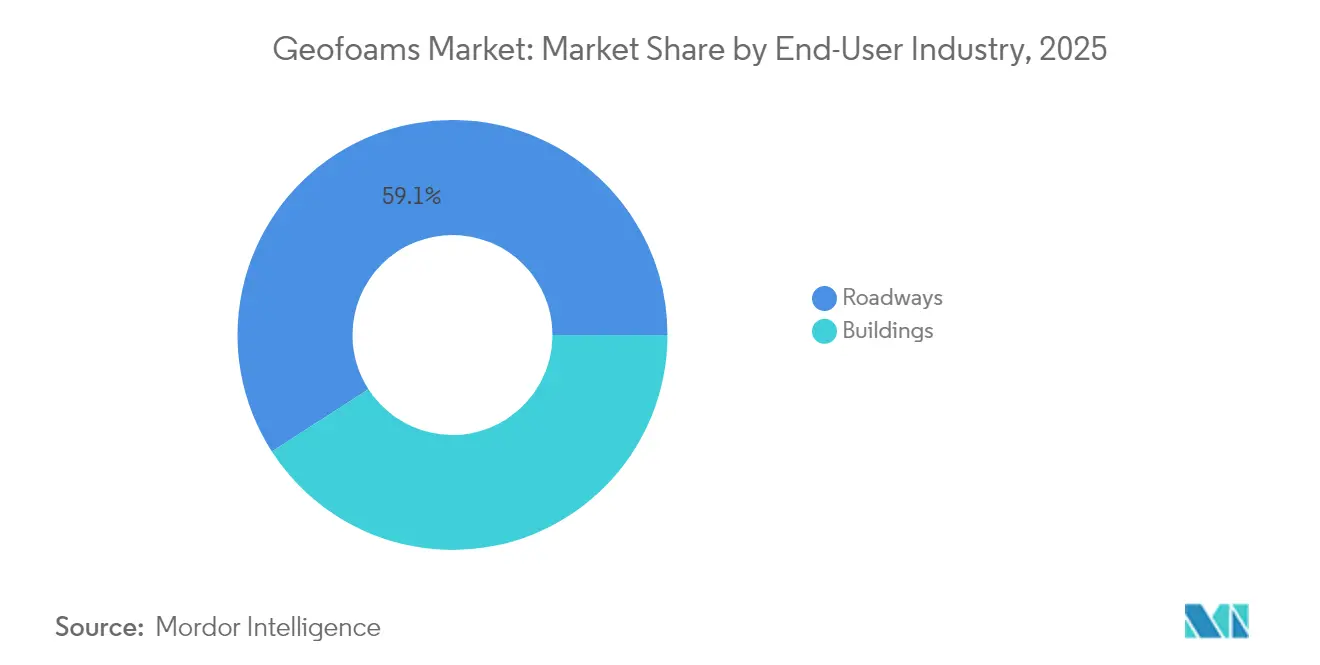

- By end-user industry, roadways held 59.12% share of the geofoams market size in 2025. The buildings segment is expected to expand at a 6.72% CAGR between 2026-2031.

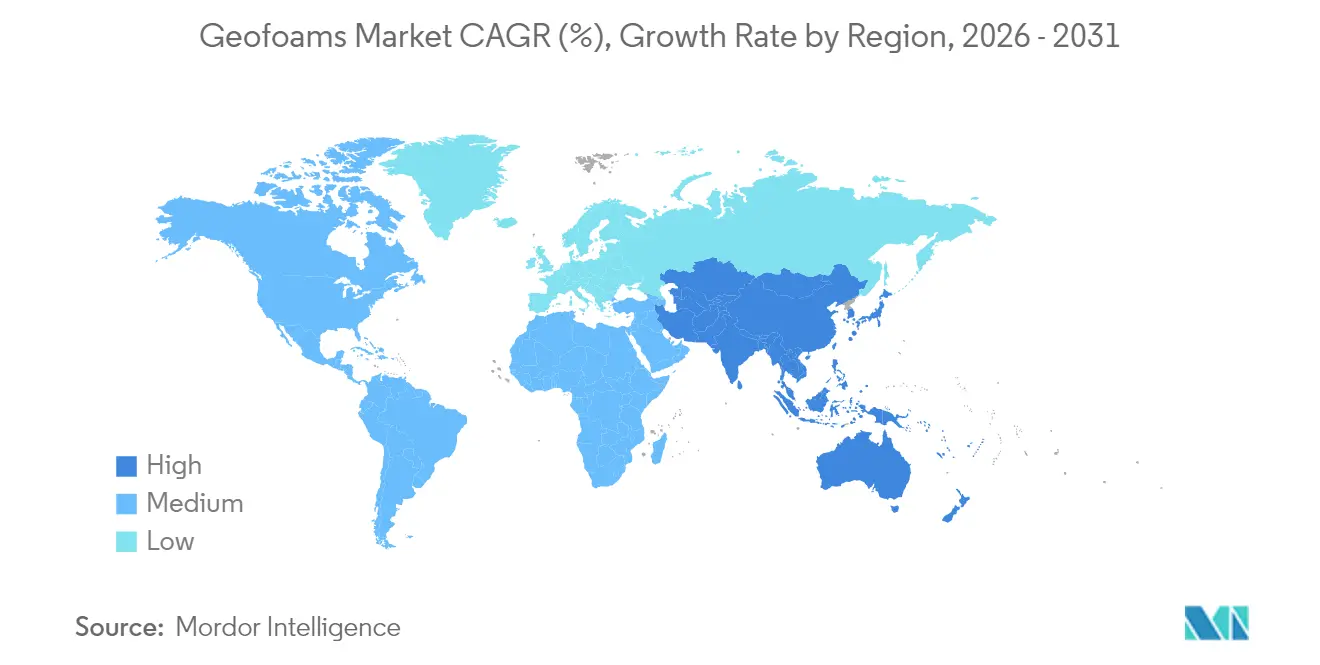

- By Geography, North America led with 34.86% revenue share in 2025, while Asia-Pacific is set to post the highest 6.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geofoams Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from roadway & bridge embankments | +1.70% | Global, with concentration in North America & Asia-Pacific | Medium term (2-4 years) |

| Cost-effective alternative to traditional lightweight fills | +1.20% | Global | Short term (≤ 2 years) |

| Surging infrastructure CAPEX in Asia-Pacific | +0.80% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Accelerated modular bridge programs using EPS geofoam blocks | +0.60% | North America & EU | Medium term (2-4 years) |

| Circular-economy push for recycled-EPS geofoam reuse | +0.40% | EU & North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Roadway & Bridge Embankments

Transportation agencies are turning to geofoam blocks to mitigate differential settlement, shorten construction schedules and avoid costly ground-improvement programs. Colorado’s emergency highway repair demonstrated 30% schedule compression when geofoam replaced traditional earthwork[1]Harelson, Stephen, “Geofoam: Colorado's Innovative Answer to an Emergency Highway Repair,” trb.org . Norwegian highway projects show 100-year durability across 350 installations, proving the material’s resilience under freeze-thaw cycles. Bridge approach ramps gain particular benefit, maintaining geometry over weak soils without deep foundations. The 1% density versus soil allows traffic to reopen days, not weeks, after placement. Long-term monitoring confirms load distribution that matches design models during seismic and thermal events.

Cost-Effective Alternative to Traditional Lightweight Fills

Geofoam’s attraction extends beyond unit price. Prefabricated blocks bypass on-site mixing and curing, trimming labor hours by up to 40% in slope repair works[2]New York State Department of Transportation, “Guidelines for Design and Construction of Expanded Polystyrene Fill as a Lightweight Soil Replacement,” dot.ny.gov . Transport savings are pronounced where aggregate sources lie hundreds of kilometers away. Because blocks can be manually maneuvered, smaller crews and lighter equipment reduce fuel and rental costs. Factory-controlled density and compressive strength slash quality-assurance outlays tied to field-mixed solutions. Together, these attributes reposition project budgets, freeing capital for ancillary scope such as drainage upgrades.

Surging Infrastructure CAPEX in Asia-Pacific

Government-backed programs like China’s Belt and Road Initiative and India’s National Infrastructure Pipeline underpin sustained geofoam procurement through 2030. The Asian Development Bank pegs the region’s annual infrastructure requirement at USD 1.7 trillion, 50% allocated to transport networks where lightweight fills solve challenging ground conditions. Rapid urbanization demands fast-track construction; geofoam’s modularity supports aggressive timelines without compromising quality. Seismic design criteria in Japan and Indonesia further boost demand for low-density fills that dampen inertial forces. Monsoon-prone climates appreciate the closed-cell moisture resistance of extruded polystyrene, protecting embankments against seasonal inundation.

Accelerated Modular Bridge Programs Using EPS Geofoam Blocks

Urban congestion leaves minimal tolerance for prolonged lane closures. Agencies are adopting modular bridge systems where factory-cut geofoam forms the approach transition. Standardized block geometries integrate seamlessly with prefabricated decks, reducing on-site assembly from weeks to days. Predictable stiffness and creep characteristics simplify structural modeling, encouraging template-based design that speeds procurement. In emergency restorations, lightweight blocks can be air-lifted to remote sites, restoring connectivity after floods or earthquakes. Consistency of supply through vertically integrated manufacturers lowers schedule risk for design-build teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High vulnerability to petroleum solvents & hydrocarbons | -0.90% | Global, particularly in industrial & transportation applications | Short term (≤ 2 years) |

| Limited design know-how in emerging economies | -0.50% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Stricter fire-resistance standards driving cost up | -0.70% | North America & EU, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Vulnerability to Petroleum Solvents & Hydrocarbons

Polystyrene’s affinity for hydrocarbon solvents constrains deployment near fuel handling zones. NOAA’s chemical database cites rapid volumetric loss when EPS contacts gasoline, necessitating HDPE geomembrane barriers that add 5-10% to installed cost[3]NOAA Office of Response and Restoration, “Polystyrene Beads, Expandable,” cameochemicals.noaa.gov . Roadways with high spill risk must incorporate monitoring wells and contingency liners, complicating designs. Industrial storage yards face similar exposure, pushing specifiers toward alternative fills or composite encapsulation systems. Although coating technologies are advancing, long-term field validation remains limited, keeping designers cautious in critical facilities.

Stricter Fire-Resistance Standards Driving Cost Up

Updated ANSI FM 4880-2024 test protocols have tightened flame-spread and smoke-developed limits for insulating block assemblies. Achieving compliance requires brominated or phosphorus-based retardants that increase resin cost 8-12% and can slightly lower compressive strength. European façade guidelines now mandate non-combustible barriers above certain heights, driving hybrid wall systems that dilute geofoam content. Manufacturers must balance additive loading against mechanical performance and recyclability. Research into halogen-free chemistries is promising but commercialization faces regulatory certification timelines of three to four years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: XPS Growth Challenges EPS Dominance

Expanded polystyrene retained 64.54% of geofoams market share in 2025, while extruded polystyrene is forecast to grow at a 6.37% CAGR to 2031. EPS thrives in cost-sensitive roadway embankments where volume rules procurement strategies, sustaining the overall geofoams market. Yet XPS’s lower water absorption and superior compressive strength satisfy bridge, tunnel and cold-climate foundations demanding long service life. DuPont tests reveal XPS can deliver the same thermal R-value with 30-40% thinner sections, appealing to designers seeking subgrade insulation without over-excavation.

Production economics illustrate why EPS dominates volume: steam expansion uses less energy and input styrene, keeping unit costs 15-20% below XPS. Conversely, XPS’s continuous extrusion yields uniform cell size that resists creep, supporting premium applications where design life exceeds 75 years. Recycling infrastructure favors EPS because block off-cuts can be readily granulated and steamed into new beads, whereas XPS re-extrusion demands stricter melt-filtering. Looking forward, municipalities with aggressive green-building codes may tilt share further toward XPS as moisture durability lessens maintenance budgets, but EPS will stay entrenched in large-scale bulk fills owing to its price advantage.

By End-User Industry: Buildings Segment Accelerates

Roadways represented 59.12% of geofoams market size in 2025, reflecting decades of adoption in embankment stabilization. However, building construction is on track to post a brisk 6.72% CAGR through 2031, gradually narrowing the volume gap. Architects specify geofoam under slabs-on-grade and green roofs to cut dead load and improve thermal performance, aligning with net-zero energy objectives. In high-rise podiums, lightweight fill relieves lateral earth pressure on retaining walls, allowing slimmer concrete sections and lowering rebar tonnage.

Roadway demand will continue to anchor the geofoams market through state and federal bridge-rehabilitation funding that values speed and reduced traffic disruption. Conversely, building applications open new channels for specialty fabricators offering block-in-block shapes and flame-retardant grades tuned for IBC code compliance. Synergies with modular construction emerge, where factory-cut void formers integrate with offsite-built floor cassettes, further enhancing installation productivity. Combined, these dynamics reposition geofoam from a niche embankment material to a holistic lightweight solution across civil and architectural sectors.

Geography Analysis

North America accounted for 34.86% of global revenue in 2025, underpinned by extensive highway rehabilitation and stringent settlement-control criteria in bridge approaches. Projects in Colorado, Minnesota and Ontario testify to lifecycle cost savings once differential settlement is curtailed. Canadian Arctic corridors leverage geofoam’s insulating value to stabilize permafrost, preventing thaw settlement beneath runways and pipelines.

Asia-Pacific is projected to expand at a 6.66% CAGR to 2031, the fastest globally, on the back of USD 1.7 trillion yearly infrastructure needs. Mega-rail corridors in China and India favor geofoam to manage weak alluvial soils without deep excavation. Japanese seismic codes reward lightweight fills that reduce inertial loads, while South Korean expressways have standardized EPS blocks for ramp widening projects.

Europe demonstrates steady adoption driven by circular-economy mandates and coastal climate challenges. Germany and France integrate recycled-content geofoam into flood-defense works, aligning with EU waste-reduction targets. The United Kingdom’s smart-motorway upgrades specify geofoam to minimize closure times, supporting contractor incentives tied to user delay cost savings. Nordic countries capitalize on three decades of field data validating geofoam resilience in sub-zero conditions, reinforcing public trust and regulatory approval for expanded use.

Regulatory Landscape

Geofoam specification is anchored to ASTM standards for rigid cellular polystyrene used in geotechnical works, notably ASTM D6817/D6817M for material types and physical-property and dimensional requirements, and ASTM D7180/D7180M as a guide for use in geotechnical projects. Public works procurement commonly references these standards, which tends to push suppliers toward documented third-party test data and consistent QA/QC practices to meet DOT and contractor submittal requirements.

For building-related applications, foam-plastics provisions in model codes such as the International Building Code (IBC) elevate fire-safety compliance. These provisions often require third-party agency listings and surface-burning testing (ASTM E84 or UL 723) depending on the assembly and use location. A concrete example is Iowa DOT's SP-230302 (implemented March 2025), which mandates EPS type categories per ASTM D6817 and requires UL Certification of Classification for fire performance on contracted EPS fill projects, increasing the importance of certified flame-retardant grades and compliant documentation in bids.

Value Chain Analysis

The value chain begins upstream with polystyrene resin supply (EPS beads and XPS feedstocks) and flame-retardant additive packages, followed by conversion at dedicated block-molding or extrusion facilities. For EPS geofoam, producers typically pre-expand beads with steam, mold them into large blocks, cure the blocks (commonly 24 to 48 hours), and then precision-cut and kit them to project shop drawings. For XPS, continuous extrusion delivers boards or blocks with tighter cell uniformity for moisture-sensitive applications. ASTM D6817 (material specification) and ASTM D7180 (use guidance) influence acceptance and submittals across the chain by defining minimum property expectations and application practices.

Midstream differentiation centers on fabrication capability (CNC cutting, numbering, packaging, and custom geometries), engineering support (layout, staging, and handling plans), and the ability to provide certified test documentation aligned to DOT and code requirements. Downstream, distribution is logistics-driven because blocks are bulky and low-density. That favors regional manufacturing footprints, just-in-time delivery, and coordination with civil contractors to reduce on-site storage and damage risk. Transport and handling constraints, along with curing time for EPS blocks, remain recurring bottlenecks that shape lead times and total installed cost.

Competitive Landscape

The geofoams market remains moderately consolidated, with the top five players controlling roughly 60% of global shipments. Vertical integration is accelerating as polymer majors seek downstream margin capture. Carlisle’s USD 259.5 million purchase of Plasti-Fab in October 2024 added block-molding capability to its insulation portfolio, reinforcing supply security amid resin volatility. BASF’s 50,000 tpa Neopor expansion at Ludwigshafen signals confidence in demand growth and supports customers bidding long-term infrastructure frameworks.

Strategic differentiation centers on flame-retardant chemistry, recycled-content innovation and pre-cut kitting services that shrink on-site labor. Regional specialists, particularly in Scandinavia and Japan, carve niches via project engineering support and logistics networks tackling remote worksites. Barriers to entry include capital-intensive block-molding presses, ASTM D6817 audit requirements and relationship-driven specification channels within transport agencies. Mergers and joint ventures are expected in Asia as domestic resin suppliers vie for downstream market share, while North American players pursue distribution alliances to service fast-growing Gulf Coast and Mountain states.

Emergent competition could stem from bio-foamed polymers under development at universities, but commercial readiness remains beyond 2030. In the interim, incumbents will likely pursue incremental process efficiencies, for example low-pressure steam cycles that cut energy by 15%, enhancing ESG credentials and improving bid competitiveness on public tenders weighted toward carbon scoring.

Geofoams Industry Leaders

Alleguard

ARCAT, Inc.

Atlas Roofing Corporation

Beaver Plastics Ltd.

Carlisle Construction Materials LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space exists where transport agencies and design-build teams prioritize rapid schedule recovery and minimized lane-closure windows, since geofoam installation shifts work from field compaction to factory-controlled block placement. In the United States, DOT design guidance and specifications support repeatable adoption pathways, with documented use cases such as New York State DOT guidance for EPS fill as lightweight soil replacement helping normalize procurement and design submittals for roadway and bridge-approach projects.

Another opportunity is broader penetration in building and mixed-use projects that need lightweight fill for podiums, slabs, and retrofit works, but must satisfy stricter fire-performance compliance. The tightening focus on fire test protocols and listings, for example UL classification requirements embedded in Iowa DOT's March 2025 SP-230302 and foam-plastics provisions in IBC frameworks, encourages suppliers to expand certified flame-retardant and assembly-tested offerings, along with kitted, traceable documentation packages. On the supply side, polymer and EPS capacity investments that support higher-quality expandable polystyrene inputs, such as BASF's planned 50,000 metric tons per year Neopor capacity expansion at Ludwigshafen (announced October 2024, startup targeted in early 2027), underpin a pathway for more consistent raw-material availability for converters serving infrastructure frameworks.

Recent Industry Developments

- April 2026: Beaver Thermal Solutions highlighted its geotechnical EPS solutions, including geofoam, supported by manufacturing operations in Alberta and British Columbia. The continued emphasis on custom geofoam solutions and technical support strengthens regional supply coverage for transportation and ground-improvement projects that value short lead times and fabrication services.

- February 2025: Carlisle Companies Incorporated announced the acquisition of ThermaFoam, expanding its expanded polystyrene insulation footprint. The deal deepens vertically aligned access to EPS products and can improve supply assurance for contractors specifying geofoam alongside broader insulation systems.

- August 2024: Alleguard, backed by Wynnchurch Capital, acquired Harbor Foam, LLC, an EPS products manufacturer based in Grandville, Michigan. The acquisition expands Alleguards EPS platform and broadens manufacturing and distribution capacity that can be leveraged for geofoam and related construction applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the geofoams market is defined as the value of engineered foam blocks used as lightweight fill and insulation in geotechnical and civil construction works, where demand is tied to project activity and specified material volumes.

Scope exclusions: We exclude general-purpose packaging foams and non-geofoam construction plastics that are not supplied and specified as geofoam blocks for civil or geotechnical use.

Segmentation Overview

- By Type

- Expanded Polystyrene (EPS)

- Extruded Polystyrene (XPS)

- By End-user Industry

- Roadways

- Buildings

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear fact base around construction output and where lightweight fill is being used. We referenced public sources such as national statistics offices for construction spending, transportation and public works agencies for road programs, and customs portals for polymer and foam-related trade flows where relevant.

To keep assumptions practical, we also reviewed building and geotechnical standards and guidance notes, such as from transportation departments and engineering bodies, plus peer-reviewed papers on EPS/XPS performance in embankments and settlement control. Company annual reports, product technical datasheets, investor presentations, and credible press releases helped us understand typical application mixes and pricing logic. A paid subscription covering company financials and a patent database were used selectively to confirm capacity signals and technology direction. The desk sources listed here are illustrative and not exhaustive, and many other public references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to stress-test the model assumptions that are hard to see in public data, especially how projects specify geofoam, how often it is substituted for other fill, and how pricing moves with resin and freight. We spoke with a balanced mix of manufacturers, converters, distributors, contractors, and engineering consultants across major regions so we could match demand signals with supply-side realities before finalizing the numbers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 20% | APAC: 44% |

| Mid tier: 41% | Functional/Unit leaders: 39% | EMEA: 36% |

| Smaller Players: 20% | Managers: 41% | Americas: 20% |

Market-Sizing & Forecasting

Sizing follows a top-down and bottom-up logic, where we first reconstruct the demand pool from construction and infrastructure activity, and then corroborate it using supplier-side and channel checks. In practice, the top-down build uses indicators like road and bridge project pipelines, embankment and slope-stabilization activity, building foundation works in soft-soil areas, and the typical adoption of geofoam in these jobs. These are then translated into value using observed price ranges that reflect EPS versus XPS usage and local cost drivers.

To keep the estimate realistic, we also run selective bottom-up approximations using sampled capacity and utilization signals, distributor throughput discussions, and typical project order sizes, which helps adjust totals where public statistics are thin. Gaps in smaller countries are handled by using proxy metrics such as construction spend growth, import reliance for foam blocks, and similar project profiles, before being normalized through interview feedback.

Forecasts are built using scenario analysis supported by a multivariate view of the main drivers, including infrastructure budgets, residential and commercial starts, resin price direction, and logistics costs. Assumptions are reviewed with primary respondents so the forecast reflects how quickly adoption shifts and how price changes are passed through.

Data Validation & Update Cycle

Outputs are checked against independent signals, including construction spending trends, infrastructure award activity, and directional movement in polymer inputs, and then reviewed for outliers by a second analyst before sign-off. When a region shows a jump that cannot be explained by project timing or pricing, we re-check the conversion logic and re-contact selected respondents to confirm whether the change is real.

The report is refreshed annually, and interim updates are made when material events occur, such as sharp resin price moves, major infrastructure announcements, or meaningful capacity additions. Before delivery, a fresh review pass is completed so the client receives the most current view supported by consistent assumptions and documented checks.

Mordor Intelligence's Geofoams Market Estimate Compared With Other Published Estimates

Published geofoam market values can vary even when they seem to cover the same product, because the counted applications, timing year, and pricing approach are not always aligned. Differences also come from how each study treats EPS versus XPS mixes and whether it ties demand to real project activity or uses broad construction growth as a shortcut.

By tracking project-linked demand indicators and refreshing EPS and XPS price ranges through interview validation, Mordor Intelligence keeps the geofoams total focused on blocks specified for roadways and buildings, instead of counting adjacent foam uses in packaging or general insulation boards.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.10 B (2026) | |

| Global Consultancy A | USD 1.14 B (2024) | Uses an earlier base year and a broader application set that can include slope stabilization and retaining structure jobs more explicitly, which shifts totals when project cycles are uneven. |

| Industry Publisher B | USD 1.19 B (2025) | Uses a different base year and applies higher average pricing and faster pass-through assumptions, which can lift the value even if physical volumes are similar. |

The spread in the table is mostly explained by base-year selection, how strictly end uses are filtered to geofoam block demand, and how price updates are applied across regions. When these items are set clearly and checked consistently, the resulting market size stays easier to reproduce and compare over time.

Key Questions Answered in the Report

What is the current size of the geofoams market?

The geofoams market size is USD 1.10 billion in 2026 and is projected to reach USD 1.47 billion by 2031.

Which region is expected to grow fastest through 2031?

Asia-Pacific is forecast to record the highest 6.66% CAGR, buoyed by USD 1.7 trillion in annual infrastructure investment needs.

Why do designers choose extruded polystyrene over expanded polystyrene?

XPS offers lower water absorption and higher compressive strength, making it preferable in moisture-prone or long-life applications despite its higher cost.

How does geofoam improve bridge approach performance?

Its density is roughly 1% of soil, which minimizes differential settlement and accelerates construction schedules, reducing traffic disruption.

What regulatory trends shape future geofoam demand?

Circular-economy directives promoting recycled content, and stricter fire-resistance standards that require advanced retardant chemistry, are expected to influence product specification.

Page last updated on: