Butyraldehyde Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

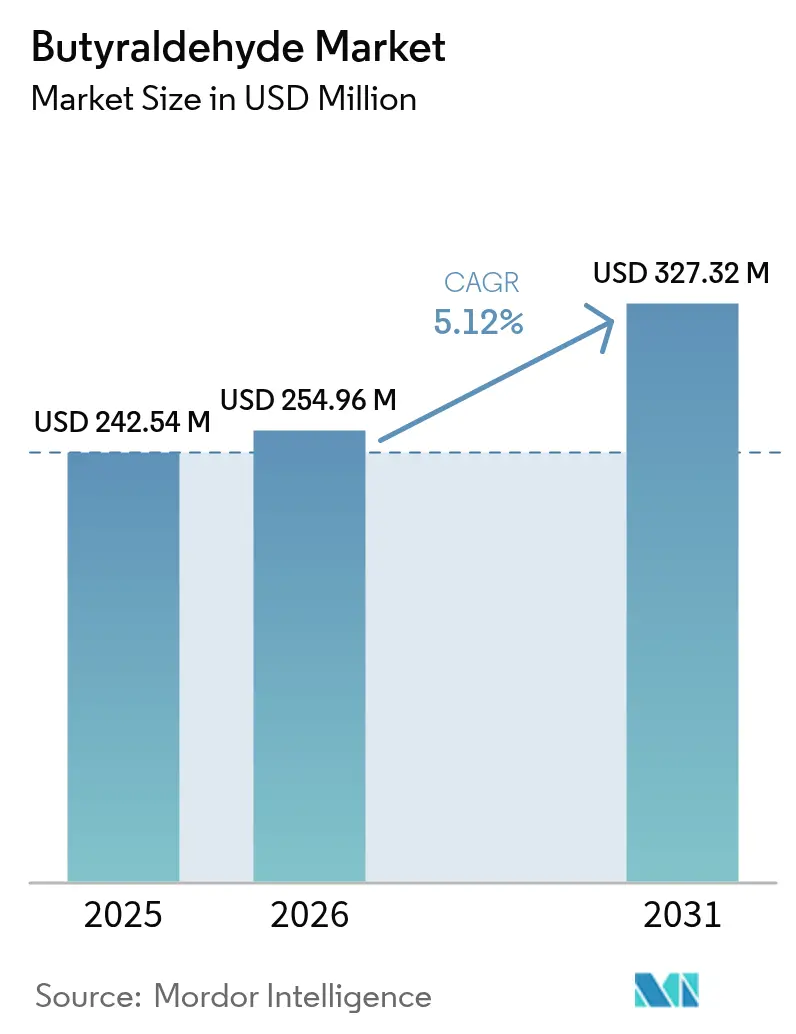

| Market Size (2026) | USD 254.96 Million |

| Market Size (2031) | USD 327.32 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

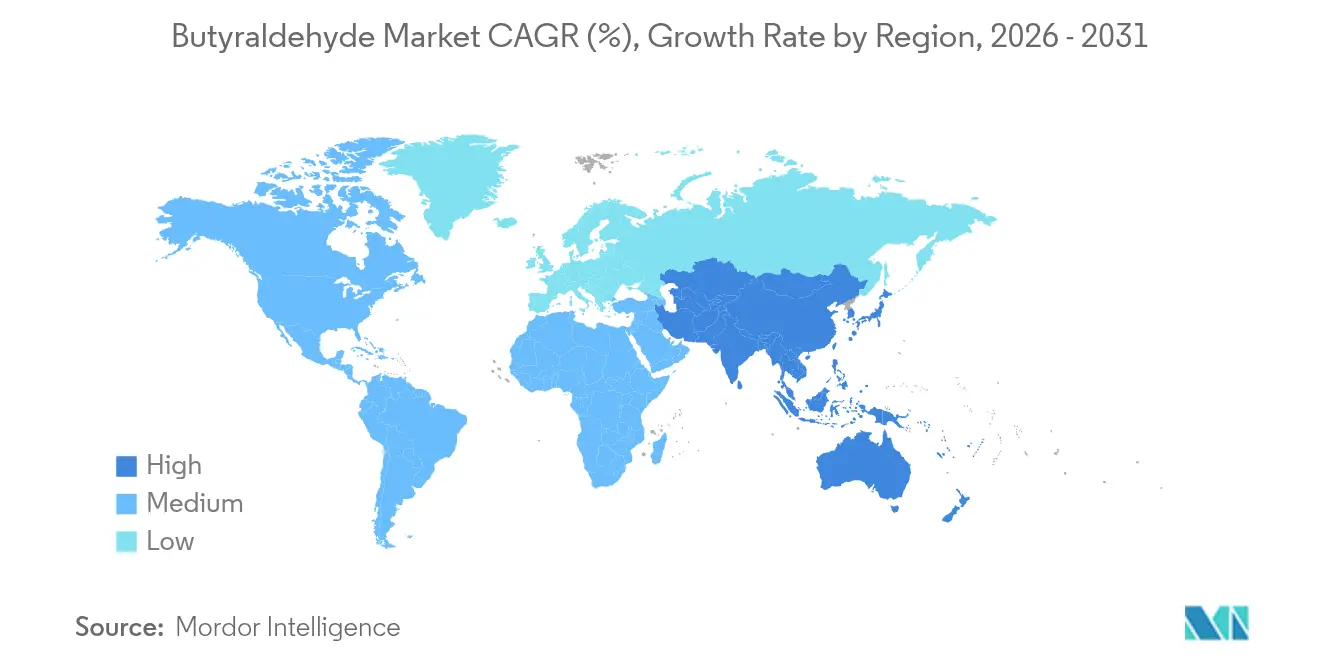

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

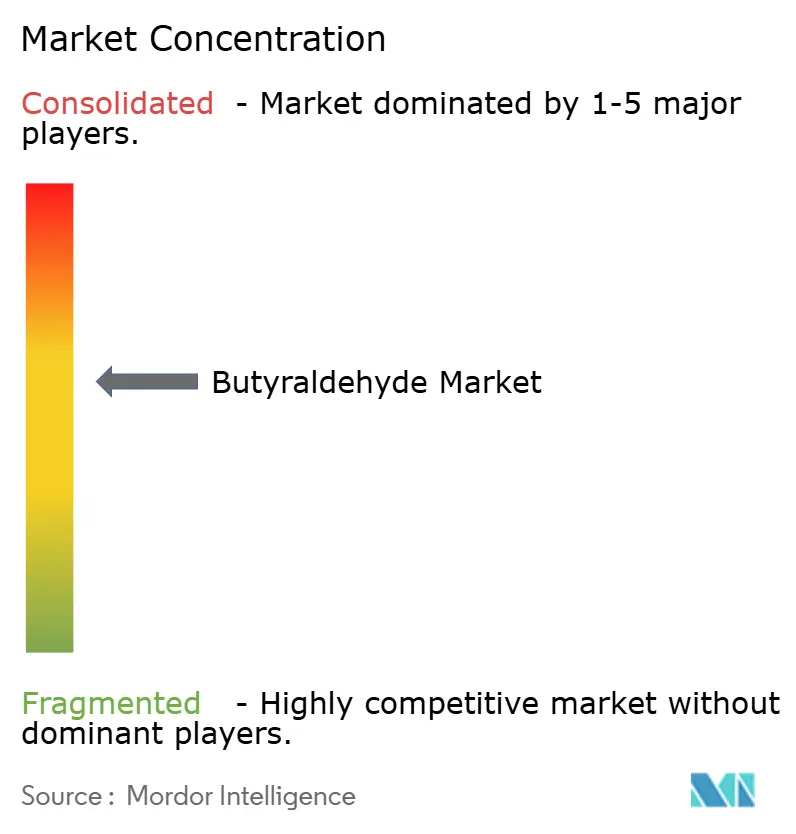

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Butyraldehyde Market Analysis by Mordor Intelligence

Butyraldehyde market size in 2026 is estimated at USD 254.96 million, growing from 2025 value of USD 242.54 million with 2031 projections showing USD 327.32 million, growing at 5.12% CAGR over 2026-2031. Demand growth is anchored in its role as a gateway molecule for n-butanol, 2-ethylhexanol, polyvinyl butyral, and a widening array of downstream intermediates that feed high-value coatings, plastics, and pharmaceutical syntheses. Process innovations—most notably rhodium-zeolite catalysts that push selectivity to n-butanal above 99%—are helping producers lift throughput, curb waste, and navigate cost pressure in an environment where propylene accounts for roughly two-thirds of manufacturing expense. Asia’s chemical build-out, especially in China, underpins more than half of global capacity and remains the principal engine of incremental volume. Short-cycle demand from architectural coatings and medium-cycle pull from flexible PVC, crop-protection actives, and complex APIs combine to keep average plant operating rates healthy despite regulatory headwinds tied to toxicity and volatile organic compounds.

Key Report Takeaways

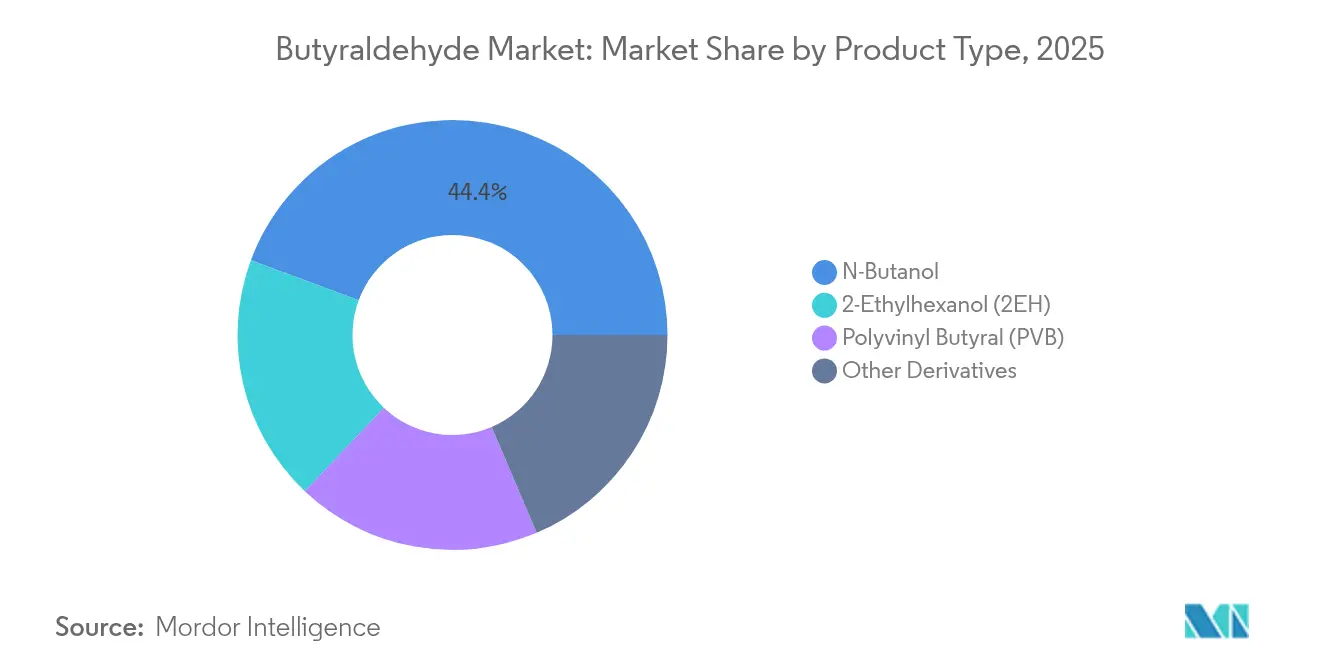

- By product type, n-butanol led with 44.35% of butyraldehyde market share in 2025, while 2-ethylhexanol is forecast to grow at a 5.95% CAGR to 2031.

- By application, paints and coatings held 34.60% of the butyraldehyde market size in 2025; pharmaceuticals are advancing at a 5.85% CAGR through 2031.

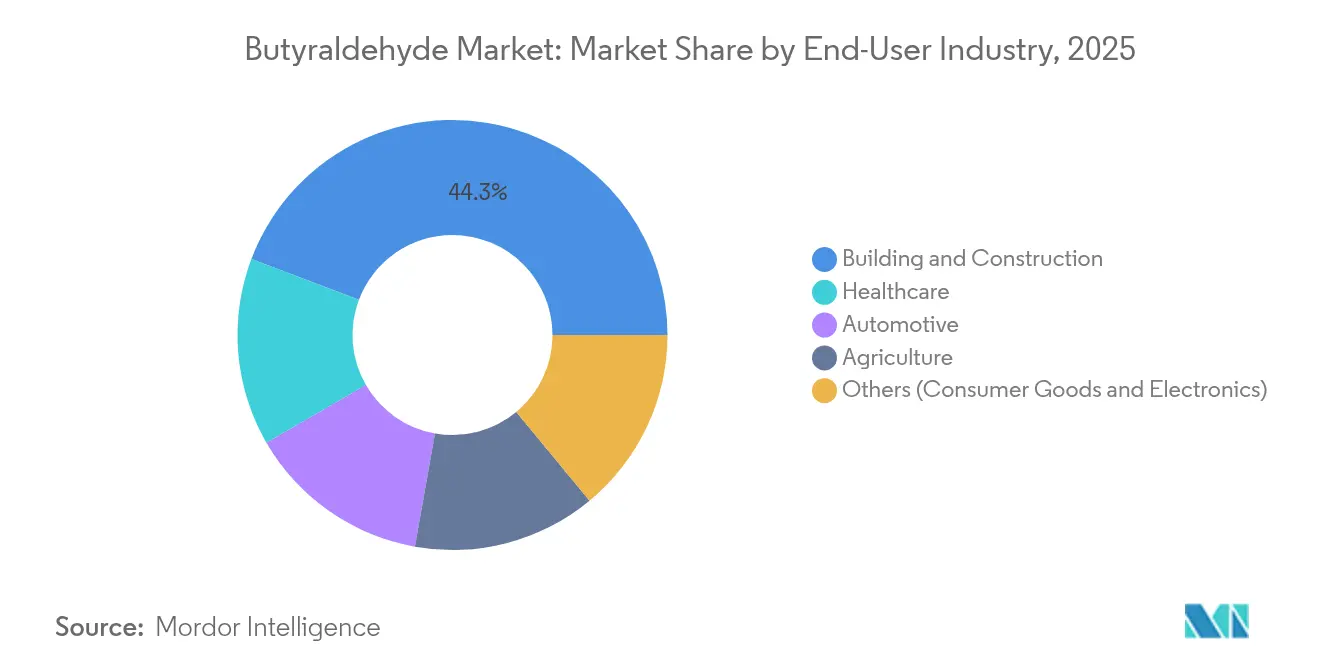

- By end-user industry, building and construction accounted for 44.25% revenue in 2025, whereas healthcare registers the fastest 6.12% CAGR over 2026-2031.

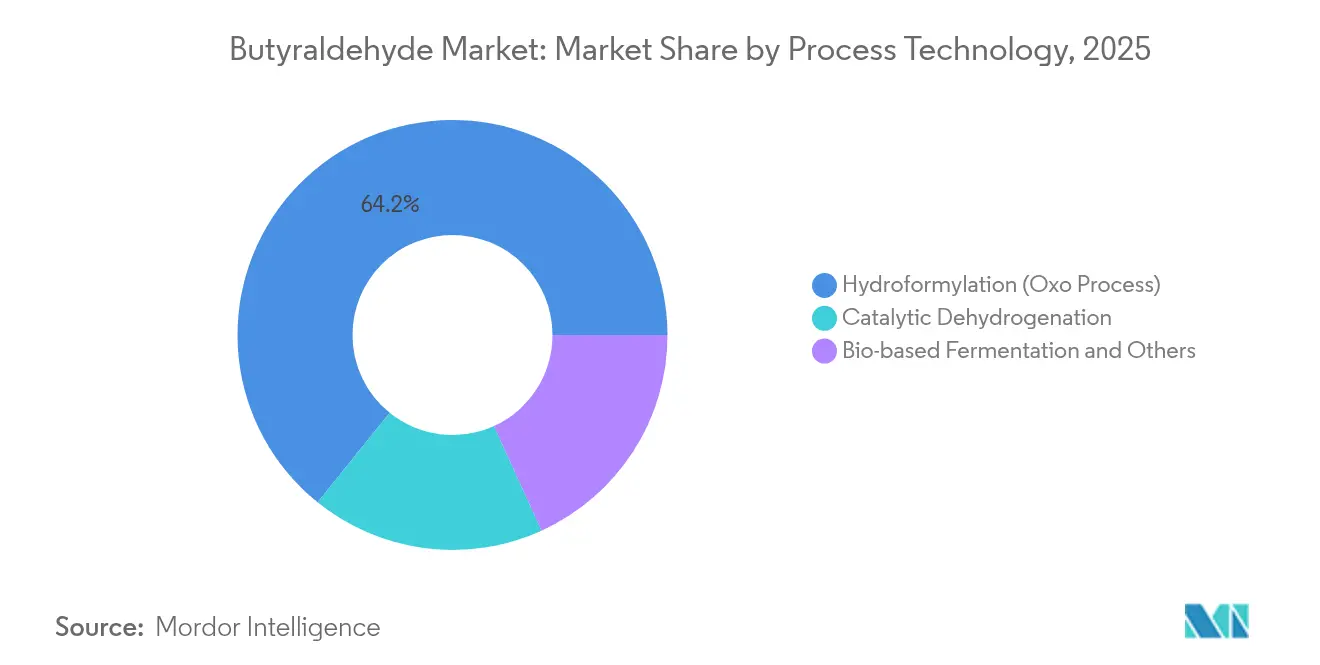

- By process technology, hydroformylation commanded 64.20% of the butyraldehyde market share in 2025; bio-based fermentation is expanding at 6.25% CAGR through 2031.

- By region, Asia captured 54.40% of global value in 2025 and is growing at 6.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Butyraldehyde Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Shift to Low-VOC Water-borne Architectural Coatings | +1.20% | Europe with spill-over to North America | Medium term (2-4 years) |

| Technological Advancements in Production | +0.80% | Global, early adoption in Asia | Short term (≤ 2 years) |

| Expanding Agricultural Industry | +0.70% | Asia, South America | Medium term (2-4 years) |

| Growth in the Pharmaceutical Sector | +1.10% | North America, Europe, Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU shift to low-VOC water-borne architectural coatings

Implementation of the European Green Deal and national statutes that cut allowable VOCs in architectural paints is accelerating the need for n-butanol-rich coalescents and resin modifiers. Producers are reformulating premium exterior and interior coatings to achieve mandated emission reductions of 55% versus 1990 by 2030, and butyraldehyde-derived additives help maintain gloss, hardness, and weatherability in these lower-solvent systems[1]Air Liquide Group, “Green Chemicals & Fuels,” engineering.airliquide.com . Paint makers in Germany, France, Italy, and Spain have published roadmaps calling for 50–65% VOC cuts by 2029, driving early pull-through for butyraldehyde derivatives across resin plants and formulating hubs.

Technological advancements in production catalysis

Novel rhodium-zeolite catalysts deliver over 99% linear aldehyde selectivity and higher turnover frequency than traditional rhodium-phosphine systems, cutting purification steps and improving overall carbon efficiency. Asian producers who retrofit reactors with the new catalyst suite achieve better propylene utilization and can flex feedstocks when olefin pricing becomes volatile. Reduced by-product severity also means smaller wastewater loads, a key advantage in provinces tightening discharge standards.

Expanding agricultural industry

Rising crop-protection spending in China, India, and Brazil is boosting demand for butyraldehyde-based intermediates used to build next-generation herbicides that deliver targeted weed control with lower environmental persistence. The molecule’s facile oxo chemistry enables functionalization pathways for specialty actives where regulators demand lower use rates and better soil degradation profiles, positioning agrochemical formulators to capture yield gains without breaching residue thresholds.

Growth in the pharmaceutical sector

API developers are embracing butyraldehyde as a platform for constructing complex small molecules under green-chemistry guidelines. Pharmaceutical-grade oxidation of butyraldehyde affords 4-hydroxybutyraldehyde, a versatile CNS drug intermediate now in late-stage clinical evaluation for enhanced blood-brain-barrier penetration. Contract manufacturers report improved atom economy and reduced solvent swap steps compared with multi-step alternative routes, underpinning a forecast 6.10% CAGR for pharmaceutical volumes through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Environmental Hazard of Butyraldehyde | -1.00% | Highest impact in Europe and North America | Medium term (2-4 years) |

| Raw Material Volatility | -0.60% | Global | Short term (≤ 2 years) |

| Availability of Substitutes | -0.50% | Global, with higher sensitivity in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health and environmental hazards of butyraldehyde

Classified as a hazardous air pollutant, butyraldehyde emissions face strict limits that compel producers to invest in scrubbers, closed-loop handling, and real-time monitoring. Cities combating smog see heightened scrutiny because aldehyde photochemistry fosters ground-level ozone formation, prompting some downstream users to investigate less-toxic solvents for consumer-facing products[2]U.S. Environmental Protection Agency, “Draft Chemistry, Fate, and Transport Assessment for Formaldehyde,” epa.gov . While industrial customers understand mitigation measures, negative public perception shapes retailer procurement policies.

Raw-material volatility (propylene)

Propylene frequently swings ±20% within a quarter when steam-cracker outages or polypropylene demand spikes absorb available C3. Given that hydroformylation consumes C3 directly, margin compression during price surges can cut average operating rates by 3–5% and slow discretionary maintenance spending, especially at standalone oxo facilities with little integration to downstream derivatives[3]Royal Society of Chemistry, “Green Ethylene Production in the UK by 2035,” pubs.rsc.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: N-Butanol Dominates While 2-Ethylhexanol Accelerates

N-butanol retained a 44.35% revenue share in 2025, making it the anchor product within the butyraldehyde market thanks to its solvent performance in coatings, adhesives, and inks. Regulatory focus on lower-VOC systems has ironically sustained n-butanol because formulators rely on its balanced evaporation rate to tune film formation without sacrificing compliance. The segment’s cost advantage over higher-value derivatives also ensures base-load demand during economic slowdowns.

Momentum now shifts toward 2-ethylhexanol, the fastest-growing derivative at a 5.95% CAGR between 2026 and 2031 as flexible PVC demand rises in construction membranes, wire insulation, and synthetic leather. China’s decision to restrict four conventional phthalates from 2026 spurs the adoption of next-generation plasticizers built on 2-ethylhexanol that meet performance and health criteria. Polyvinyl butyral remains niche but gains from safety-glass uptake in electric vehicles and high-performance architecture as Eastman upgrades its Ghent lines to capture specification-driven orders.

By Application: Paints & Coatings Lead While Pharmaceuticals Expand Rapidly

Paints and coatings absorbed 34.60% of global volume in 2025, anchored in architectural, industrial, and protective finishes that integrate n-butanol as a co-solvent and use oxo-derived resins to balance flow, leveling, and chemical resistance. Tightening emission ceilings reinforce butyraldehyde derivatives’ importance because few alternate solvents match their reactivity in resin esterification while remaining cost-competitive. Construction recovery in Southeast Asia and ongoing US retrofits bolster short-cycle consumption.

Pharmaceutical applications reach just 11.90% of the current volume but post a 5.85% CAGR to 2031, the highest among applications. The butyraldehyde market size tied to pharmaceutical synthesis is expected to increase, assisted by contract manufacturing investment across China, Singapore, and Ireland. Butyraldoximes and other tailored intermediates help medicinal chemists insert functional groups selectively, reducing protecting-group steps and batch cycle times. Agrochemicals, flavors, and personal-care uses together keep the molecule’s demand pattern broad, insulating suppliers from shocks in any single vertical.

By End-User Industry: Building & Construction Maintains Leadership as Healthcare Accelerates

Building and construction absorbed 44.25% of total consumption in 2025, mainly via architectural paints, flooring adhesives, and flexible PVC profiles. Rapid urban migration in India, Indonesia, and Vietnam sustains underlying volume, while European renovation programs that prize energy-efficient façades spur premium coating formulations where butyraldehyde-based resins improve weatherability. Nonetheless, growth moderates as emerging markets pivot toward green-building codes that favor lower-solvent systems.

Healthcare logs a 6.12% CAGR over the forecast horizon, reflecting rising small-molecule API output, medical film demand, and specialized solvent use. Chongqing Xingtaihao Pharmaceutical’s new antitumor drug plant illustrates China’s pivot toward high-value healthcare manufacturing that pulls on butyraldehyde stream chemicals. Automotive, agriculture, and consumer goods remain vital, each respecting different performance levers from impact resistance in dashboard skins to selective herbicide synthesis pathways, preserving a diversified revenue base.

By Process Technology: Hydroformylation Dominates While Bio-Based Routes Gain Momentum

Hydroformylation accounted for 64.20% of global production in 2025, and the segment is projected to hold a still-dominant 58.90% share in 2031 as catalysts upgrade and CO-H₂ ratios optimize energy efficiency. The butyraldehyde market share of hydroformylation, therefore, remains substantial even under aggressive sustainability scenarios because installed assets provide sunk-capital advantages. Linear-selective rhodium-zeolite systems have trimmed separation energy and boosted yields, sustaining the business case for incremental debottlenecks.

Yet bio-based fermentation climbs at 6.25% CAGR, buoyed by life-cycle-assessment benefits and support schemes that reward carbon-intensity cuts. Advances in Clostridium and Zymomonas strains unlock feedstock versatility, letting operators valorize agricultural waste or glycerol into C4 aldehydes with competitive titers. Process risk remains around scale-up kinetics and downstream purification, but leading Asian majors have announced pilot plants to hedge future regulatory shifts away from fossil feedstocks.

Geography Analysis

Asia held 54.40% of global revenue in 2025 and is expected to widen its lead through a 6.35% CAGR to 2031, fueled by multi-billion-dollar oxo complexes in Jiangsu, Shandong, and Gujarat. Evergreen New Material’s USD 1.4 billion fine-chemical park in Taizhou exemplifies capacity build-outs that underpin integrated chains from propylene through oxo derivatives to high-margin plasticizers. Southeast Asian producers gain from duty-free export access into the Regional Comprehensive Economic Partnership bloc, further enhancing regional attractiveness for downstream investors.

Germany and the Netherlands anchor a balanced producer-consumer landscape, highlighting Europe's significant presence in the market. Stringent environmental law accelerates the adoption of compliant derivatives and encourages capital spending on low-emission reactors and solvent-recovery loops. Concurrently, cross-border collaboration between resin houses and coating formulators drives premium specifications that depend on high-purity n-butanol and tailored oxo intermediates.

North America benefits from advantaged shale-based propylene and hosts several world-scale hydroformylation units along the US Gulf Coast. That feedstock edge supports competitive export pricing into Latin America and Europe, even after freight. South America, led by Brazil, sees volume growth alongside soy and sugar-cane-driven agrochemical demand and supportive tax regimes for specialty chemical investment. Middle East & Africa remain smaller but pursue value-chain integration strategies via petrochemical diversification in Saudi Arabia and United Arab Emirates free zones.

Regulatory Landscape

Butyraldehyde is governed through chemicals-management and workplace-safety frameworks that address registration, labeling, storage, and emissions. In the European Union, it falls under REACH (EC) No 1907/2006, with registration obligations for manufacture or import, and it is commonly handled as a transported isolated intermediate under strictly controlled conditions (Article 18(4)); current ECHA registration dossier status does not indicate it is on the REACH SVHC Candidate List or subject to Annex XIV authorization requirements.

In the United States, butyraldehyde is listed on the TSCA Inventory (40 CFR Part 710) and is managed under OSHA Hazard Communication (29 CFR 1910.1200) for hazard classification and communication. Compliance also incorporates transport and handling requirements for flammable liquids (UN 1129), and it can be influenced by state and regional guidance for exposure and air-permitting benchmarks, including New Jersey Right-to-Know materials and Texas TCEQ toxicology reference documentation used in permitting and monitoring programs.

Value Chain Analysis

The value chain starts with upstream propylene supply (from steam crackers and refineries) and synthesis gas (CO and H2), which feed the dominant hydroformylation (oxo) route to produce n- and iso-butyraldehyde using rhodium- or cobalt-based catalysts. Because propylene is a major cost driver, producers often place butyraldehyde units inside integrated petrochemical complexes that secure C3 availability and utilities, then tune n/iso selectivity to reduce separation load and improve downstream yields.

Midstream and downstream, a significant portion of butyraldehyde is consumed captively to make oxo alcohols and derivatives, led by n-butanol and 2-ethylhexanol, followed by intermediates for plasticizers, resins, and PVB interlayers. Finished materials are supplied via bulk distribution into coatings, construction materials, flexible PVC, agrochemical intermediates, and pharmaceutical manufacturing supply chains. Integration across oxo-aldehydes, oxo-alcohols, and derivative plants is the main structural lever for managing feedstock volatility and maintaining specification-grade output for downstream formulators.

Competitive Landscape

The butyraldehyde market is moderately consolidated. BASF, Dow, Eastman Chemical, and Oxea GmbH run vertically integrated assets that secure propylene feed, oxo capacity, and derivative lines. These players use scale economics to maintain cost leadership while steering investment toward high-margin downstream additives. BASF’s decision to expand additives at its Nanjing site highlights a tactical move to blend volume gains with regional proximity to Chinese formulators.

Asian challengers—Luxi Chemical, Petronas Chemicals, and several South Korean firms—are closing technology gaps by licensing best-in-class catalyst systems and commissioning energy-efficient reactors. They benefit from lower capital costs and near-customer logistics in the world’s fastest-growing demand corridor. Western firms respond by marketing low-carbon product ranges and by securing ISCC-Plus certified bio-attributed butyraldehyde to address Scope 3 targets for global brand owners. Collaborations between catalyst developers and plant operators accelerate time-to-market for new selectivity breakthroughs that could shift cost curves.

Strategic moves extend beyond asset debottlenecking. Dow recently outlined pipeline programs to commercialize butyraldehyde-derived aldehyde acrylates for battery binders, signaling a hunt for high-technology applications where early IP can sustain premium margins. Eastman couples its Ghent extrusion upgrade with closed-loop recycling protocols for PVB glass interlayers to lock in OEM loyalty. Looking ahead, the interplay between hydroformylation efficiency gains and bio-based route advances will determine margin spread and ultimately shape competitive rank.

Butyraldehyde Industry Leaders

BASF SE

Dow

Eastman Chemical Company

KH Neochem Co., Ltd.

OXEA GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Most of the near-term opportunity is tied to downstream pull-through from regulated formulation changes and to higher-value derivative integration. In Europe, tighter requirements for lower-VOC architectural and industrial coating systems increase the demand for oxo-derived solvent and resin building blocks that help formulators meet compliant targets, while also raising the premium on plants that can show low-emission operations and tight containment for aldehydes. In plastics, China’s transition away from certain conventional phthalates from 2026 increases the importance of next-generation plasticizer routes based on 2-ethylhexanol, strengthening incentives to align butyraldehyde production with 2-EH supply chains.

On the supply side, catalyst and process upgrades that lift linear selectivity (including rhodium-zeolite systems referenced in the current report context) create space for cost and carbon-efficiency improvements at existing hydroformylation assets, particularly where producers face tightening discharge and VOC constraints. Recent pricing actions also reflect an industry focus on margin protection and pass-through mechanisms during feedstock and utility cost increases, including Perstorp Oxo AB’s global oxo-chemicals and plasticizers price increase effective May 1, 2026, covering butyraldehyde. Together with Asia-centric capacity and downstream build-outs, these factors support investment cases that connect propylene, oxo, and specialty derivatives such as PVB interlayers and tailored intermediates within integrated platforms.

Recent Industry Developments

- May 2026: Perstorp Oxo AB implemented a global selling price increase for oxo chemicals and plasticizers, including butyraldehyde, effective May 1, 2026, citing higher raw material and utility costs. The price move reinforced contract and spot repricing dynamics for a largely captive intermediate and tightened cost pass-through to downstream oxo alcohols and plasticizers. It also underscored the role of integration and energy efficiency in protecting margins during input-cost swings.

- September 2025: BASF reported that Nan Ya Plastics Corporation successfully used BASF SYNSPIRE G1-110 catalyst at its Mailiao 2-ethylhexanol site, reducing annual steam consumption by about 40,000 metric tons and avoiding around 38,000 metric tons of CO2 emissions. Because 2-EH production is directly linked to n-butyraldehyde conversion, this catalyst-enabled utility reduction supports lower conversion costs and improves competitiveness of integrated oxo chains. The announcement also pointed to increasing emphasis on decarbonization and operational efficiency at downstream derivative sites tied to butyraldehyde demand.

- November 2024: Eastman Chemical Company announced plans to invest in upgrading and expanding extrusion capabilities for Saflex polyvinyl butyral interlayers at its Ghent, Belgium facility. PVB interlayers are a key downstream outlet supported by oxo-derived intermediates, so capacity and capability upgrades at a major interlayer site support demand for consistent, specification-grade feedstocks across the chain. The project aligned with higher-performance laminated glass requirements in automotive and architectural applications, where material qualification and supply assurance affect long-term sourcing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from the sale of butyraldehyde (including n and iso grades) used as an intermediate chemical, measured at the point where it is sold into downstream manufacturing and distribution.

Scope exclusions: Captive, in-plant transfers of butyraldehyde that are not priced as third-party sales are excluded from the market value.

Segmentation Overview

- By Product Type

- N-Butanol

- 2-Ethylhexanol (2EH)

- Polyvinyl Butyral (PVB)

- Other Derivatives

- By Application

- Paints and Coatings

- Agrochemicals

- Pharmaceuticals

- Other Applications

- By End-User Industry

- Building and Construction

- Automotive

- Healthcare

- Agriculture

- Others (Consumer Goods and Electronics)

- By Process Technology

- Hydroformylation (Oxo Process)

- Catalytic Dehydrogenation

- Bio-based Fermentation and Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the supply and demand context for oxo chemicals and key derivatives, then narrowing the view to butyraldehyde production and consumption signals. We rely on public, non-paywalled sources such as the US Energy Information Administration for feedstock trends, USGS minerals and industrial statistics for related industrial activity context, and US International Trade Commission data for import and export directionally.

Alongside that, references like Eurostat and UN Comtrade help verify trade flows by region, and peer-reviewed chemistry and catalysis journals are used to understand typical process routes and yield logic that can affect effective supply. Company annual reports, investor presentations, and plant announcements are reviewed for capacity changes, integration levels, and end-use exposure. Paid subscriptions are used selectively for company financials and intelligence, patent databases, and shipment-level trade records where public trade data is not granular enough. This list is not exhaustive, and many other public and paid sources were also used to cross-check data points and clarify assumptions.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk research suggests, especially around operating rates, typical contract versus spot pricing behavior, and where butyraldehyde is converted internally versus sold externally. We speak with producers, distributors, and downstream buyers across key regions, and we also include process and procurement roles so the model reflects real purchasing units and substitution limits.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 50% |

| Mid tier: 54% | Functional/Unit leaders: 26% | EMEA: 32% |

| Smaller Players: 16% | Managers: 58% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where petrochemical and oxo-alcohol value chain signals are reconstructed into a butyraldehyde demand pool by region, followed by application weighting and price normalization. The totals are then cross-checked using selective bottom-up approximations, such as sampled supplier volumes, distributor channel checks, and typical ASP multiplied by estimated consumption volume, to adjust for obvious gaps.

Inputs that matter in this market include propylene and synthesis gas cost direction, announced oxo capacity additions and shutdowns, operating rate ranges at integrated sites, the share of butyraldehyde routed into 2-ethylhexanol and n-butanol chains, and trade intensity for regions that rely on imports. Where data is thin for smaller countries, we fill gaps by mapping end-use exposure to proxy indicators like coatings and plasticizer activity, and then validating the implied numbers with interview feedback.

Forecasts are built using scenario analysis anchored on expected downstream pull and capacity availability, then checked against expert views on price movement and utilization. In the final step, assumptions are tightened so the year-to-year path remains consistent with realistic commissioning timelines and typical chemical cycle behavior.

Data Validation & Update Cycle

Validation is done by triangulating the model output against independent signals like capacity announcements, regional trade direction, and derivative market momentum, which helps flag values that are too high or too low. Outliers are reviewed again at the country and application level, and if a variance cannot be explained through inputs, the relevant assumption is revisited and respondents are re-contacted for clarification.

Before sign-off, the work goes through a multi-step review where another analyst checks formulas, unit conversions, and logic consistency across regions. Reports are refreshed annually, and interim updates are made when material events occur, such as major plant outages, new capacity start-ups, or sharp feedstock shifts. Right before delivery, a final pass is completed so the shared numbers reflect the most current information available.

Mordor Intelligence's Butyraldehyde Market Sizing Compared With Other Published Estimates

Published market values for butyraldehyde can look far apart because each publisher draws the market line in a different place, then uses different price and volume building blocks. Differences also show up when the base year is not aligned, or when the forecast is built from aggressive capacity assumptions without checking actual operating reality.

Captive consumption that never becomes a priced third-party sale is the biggest swing factor, and it sits outside Mordor Intelligence's scope, which is why some larger published values are not directly comparable to this study. Another common gap comes from mixing derivatives like butanol or 2-ethylhexanol into the same revenue pool, and from using constant global average prices without regional adjustments or currency timing checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 254.96 M (2026) | |

| Trade Publication A | USD 887.00 M (2025) | Appears to treat downstream derivative revenue as part of the butyraldehyde value pool, and the base year is different, which can overstate the comparable market size. |

| Industry Analyst B | USD 1.75 B (2024) | Likely includes a broader oxo-chemicals set or multiple aldehydes, and it is not clear how captive transfers and region-level ASP differences were handled. |

The spread across the three figures mainly comes down to what is counted as butyraldehyde revenue versus what is counted as derivative or internal value, and also which year is being referenced. By keeping inputs tied to capacity reality, end-use pull, and region-specific pricing checks, the final number stays traceable to clear variables and can be repeated when new plant or trade signals emerge.

Key Questions Answered in the Report

What is the current size of the butyraldehyde market?

The butyraldehyde market is expected to register USD 254.96 million in 2026 and is projected to grow to USD 327.32 million by 2031.

Which region dominates butyraldehyde demand?

Asia controls 54.40% of global demand and is forecast to rise at a 6.35% CAGR through 2031 on the back of Chinese capacity additions.

Why is n-butanol so important to the butyraldehyde value chain?

N-butanol captures 44.35% of derivative demand because it functions as a workhorse solvent and intermediate in coatings, adhesives, and resin production.

How are environmental rules affecting butyraldehyde consumption?

Stricter VOC regulations in Europe and North America boost demand for compliant derivatives but also raise handling and emission-control costs.

What technology trends could disrupt traditional production routes?

Advances in rhodium-zeolite hydroformylation catalysts and emerging bio-based fermentation platforms promise higher selectivity, lower carbon footprints, and greater feedstock flexibility.

Page last updated on: