Protein Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

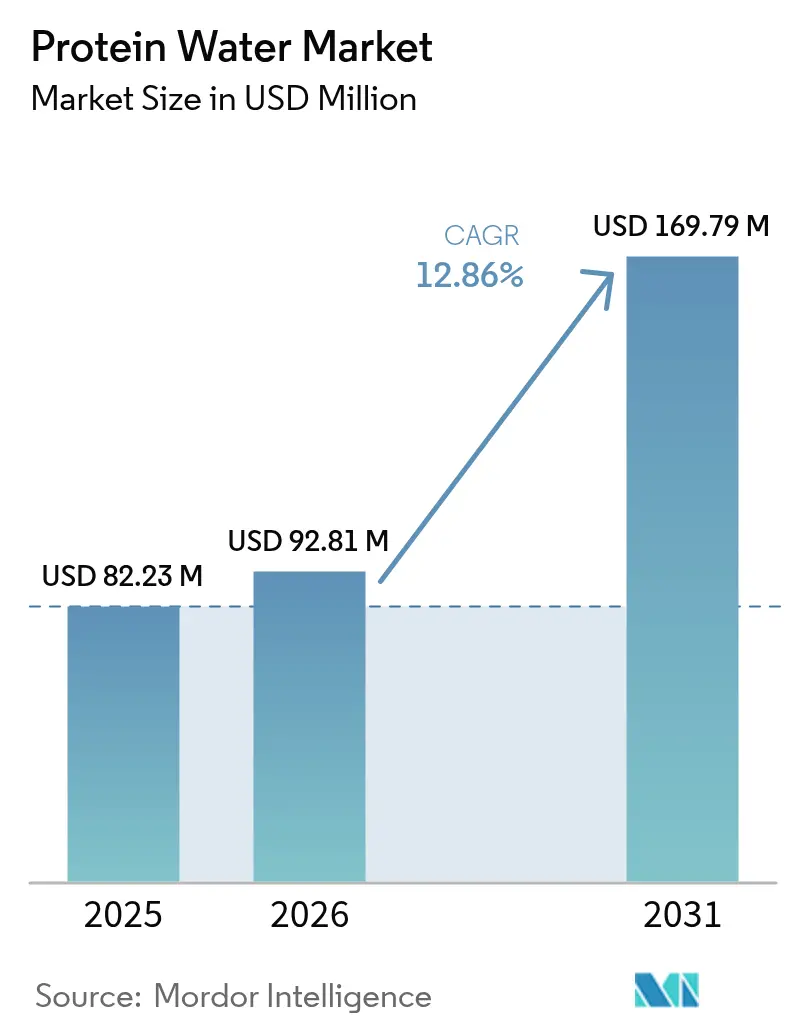

| Market Size (2026) | USD 92.81 Million |

| Market Size (2031) | USD 169.79 Million |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

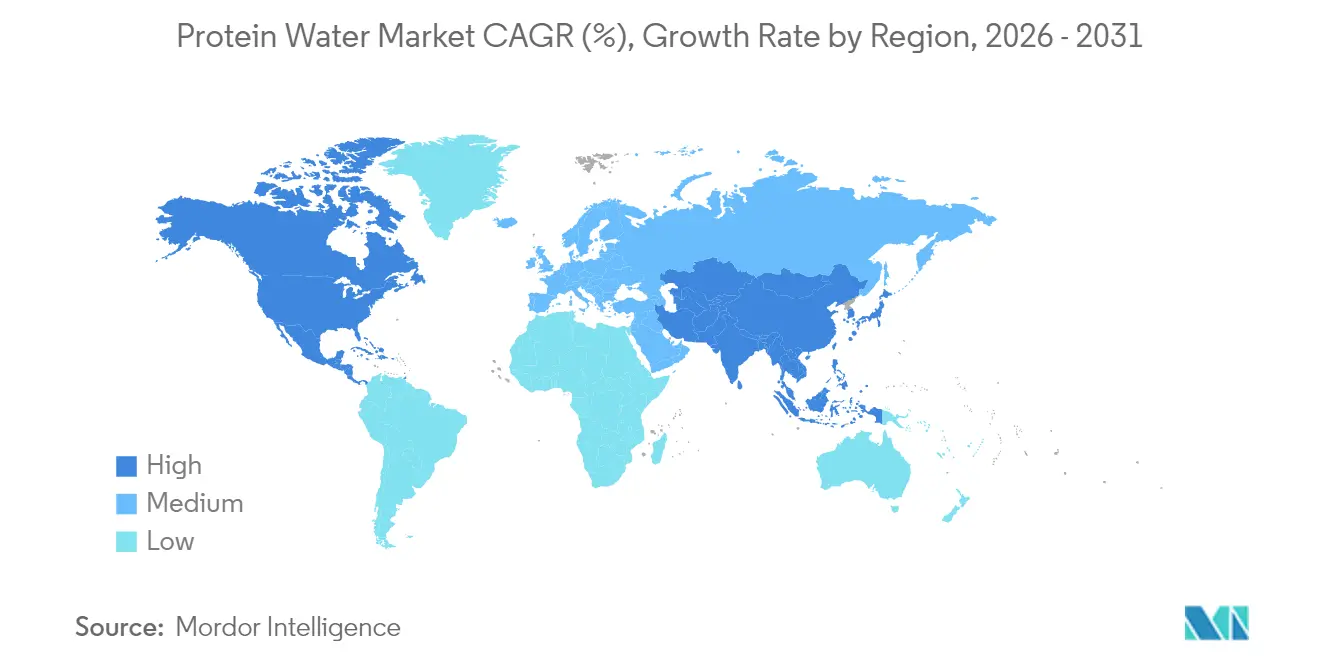

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protein Water Market Analysis by Mordor Intelligence

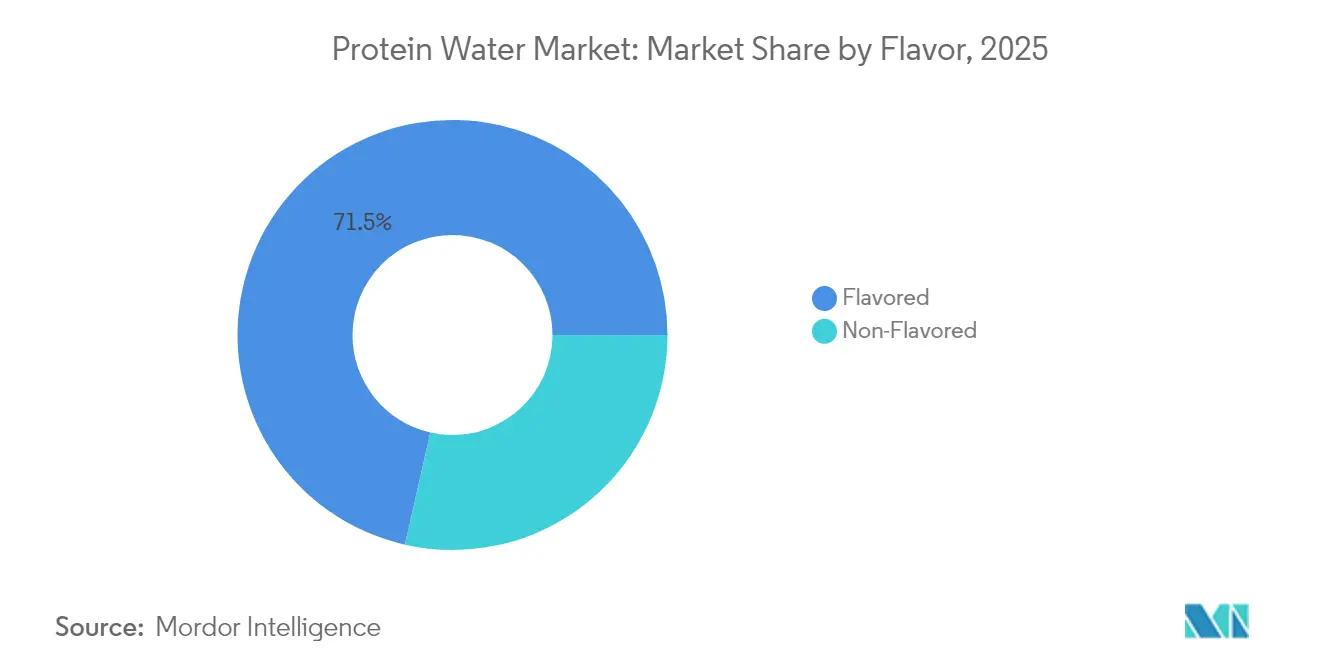

The protein water market size is expected to grow from USD 82.23 million in 2025 to USD 92.81 million in 2026 and is forecast to reach USD 169.79 million by 2031 at 12.86% CAGR over 2026-2031. Regulatory advancements, increasing consumer focus on health, and the transformation of distribution channels are driving protein water's positioning as a hybrid product between traditional hydration and functional nutrition. With rising urbanization and higher disposable incomes, the demand for premium products is experiencing significant growth globally. Protein water, fortified with protein, is gaining traction among consumers due to its convenience, perceived health benefits, and superior taste compared to tap water. Growing health concerns, such as digestive issues and weight management, are prompting consumers to opt for healthier alternatives like protein water. North America currently dominates revenue generation, supported by a well-established sports-nutrition culture and advanced distribution infrastructure. In contrast, the Asia-Pacific region is emerging as the fastest-growing market, driven by increasing affluence and the rapid adoption of e-commerce. In 2024, flavored protein water products lead sales; however, non-flavored minimalist options are witnessing the fastest growth. The competitive landscape remains moderately intense, with major beverage companies and specialized brands competing for market share across physical and digital channels.

Key Report Takeaways

- By flavor, flavored products accounted for 71.45% revenue share in 2025, whereas non-flavored options are forecast to grow at a 14.78% CAGR to 2031.

- By packaging, PET bottles dominated with 74.10% of the protein water market share in 2025, while cans are projected to expand at a 13.94% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 44.85% of the protein water market size in 2025; online retail shows the highest CAGR at 17.62% between 2026 and 2031.

- By geography, North America commanded 37.78% of 2025 revenues, and Asia-Pacific is advancing at a 13.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health And Wellness Trends Are Pushing Consumers Toward Clean-Label Hydration Options | +3.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Growth In Fitness and Sports Nutrition Markets Supports Protein Water Consumption | +2.8% | North America and Asia-Pacific core, spill-over to Europe | Short term (≤ 2 years) |

| Innovation In Flavors and Plant-Based Proteins Expands Consumer Appeal | +2.1% | Global, with early adoption in North America | Medium term (2-4 years) |

| Busy Lifestyles Are Driving the Popularity of On-The-Go Consumption of Ready-To-Drink Protein Beverages | +2.4% | Global, particularly urban centers in North America and Asia-Pacific | Short term (≤ 2 years) |

| Social media and Influencer Marketing Are Increasing Product Visibility | +1.8% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Expanding Online and Specialty Health Retail Channels Enhance Market Access | +2.2% | Global, with accelerated growth in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health And Wellness Trends Are Pushing Consumers Toward Clean-Label Hydration Options

The FDA's updated "healthy" labeling framework, effective February 2025, fundamentally reshapes how protein water can position itself in the marketplace by allowing water-based beverages with 5 calories or fewer to qualify for health claims[1]Source: U.S. Food and Drug Administration, “Food Labeling: Nutrient Content Claims; ‘Healthy’,” fda.gov. This regulatory change aligns with evolving consumer preferences, as 71% of Americans in 2024 actively seeked higher protein intake, a significant rise compared to previous years. This shift expands the addressable market beyond the traditional sports nutrition segment[2]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org. The combination of regulatory clarity and growing consumer demand enables protein water brands to capitalize on health-focused positioning, previously dominated by more complex nutritional products. Additionally, the FDA's emphasis on reducing added sugars, saturated fats, and sodium in products eligible for healthy claims bolsters the appeal of clean-label formulations. Clear protein formulations address consumer demand for transparency while avoiding the sensory challenges associated with traditional protein supplements. Protein water, with its minimal ingredient profile, is well-positioned to benefit from this trend, offering manufacturers a competitive edge through transparency and simplicity rather than relying on intricate functional claims.

Growth In Fitness and Sports Nutrition Markets Supports Protein Water Consumption

The sports nutrition market is expanding its reach from traditional athlete demographics to a broader base of health-conscious consumers. This shift creates a conducive environment for the growth of protein water, reflecting increasing consumer acceptance of protein-enhanced beverages. As sports nutrition becomes more accessible, protein water offers a functional hydration solution for consumers seeking simpler, lower-calorie alternatives to conventional protein shakes. The convenience and portability of protein water make it particularly appealing to busy urban consumers who prioritize on-the-go nutrition. Additionally, the clear, refreshing format of protein water addresses common barriers to protein supplement consumption, such as thick textures and chalky aftertastes associated with traditional protein drinks. The normalization of gym attendance and home fitness post-pandemic, coupled with the wellness economy's robust annual growth, further supports this trend. The shift toward "holistic hydration" concepts, combining electrolytes with protein for comprehensive recovery, positions protein water as a strategic bridge between hydration and performance nutrition categories.

Innovation In Flavors and Plant-Based Proteins Expands Consumer Appeal

The growing demand for plant-based proteins presents a strategic opportunity for protein water manufacturers to differentiate their offerings by addressing both protein delivery and sustainability priorities. Consumer trust in plant-based proteins significantly surpasses that of alternative protein sources, indicating that plant-based protein water formulations are well-positioned for broader market acceptance compared to animal-derived alternatives. Plant-based protein innovations are addressing historical formulation challenges, with protein soft drinks featuring plant proteins, primarily pea protein isolate, indicating significant expansion potential. Advanced processing techniques, including protein hydrolysis and microencapsulation, are improving taste profiles and solubility characteristics that previously limited plant protein adoption in clear beverage applications. Flavor innovation extends beyond traditional fruit profiles to include sophisticated combinations like protein coffee enhancers and matcha lattes, as demonstrated by The EVERY Company's FERMY line launch in June 2024. The development of hybrid protein systems, combining plant and dairy proteins, optimizes both nutritional profiles and taste characteristics, addressing consumer preferences for both sustainability and performance.

Busy Lifestyles Are Driving the Popularity of On-The-Go Consumption of Ready-To-Drink Protein Beverages

Workplace food and beverage consumption trends reveal that 23.4% of working adults acquire meals at work, consuming an average of 1,292 calories per week, primarily from high-calorie, low-nutrition options[3]Source: Centers for Disease Control and Prevention, “Foods Obtained at Work Site Study,” cdc.gov. These trends create a market opportunity for protein water as a healthier workplace hydration solution, addressing both convenience and nutritional requirements. The shift toward on-the-go consumption highlights protein water's portability advantage over powder-based alternatives, which require preparation and additional equipment. This growth trajectory is further supported by the expansion of e-commerce in the food and beverage sector. Protein water's positioning as a meal replacement or between-meal solution addresses the consumers who prioritize hydration-focused beverages while simultaneously meeting protein intake goals. The format's convenience advantage over traditional protein powders eliminates preparation time and equipment requirements, making it accessible for workplace consumption and travel scenarios. Packaging innovations, including single-serve formats and resealable options, optimize portability while maintaining product stability and shelf life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Costs Limit Affordability for Mass-Market Consumers | -1.9% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Limited Awareness in Emerging Markets Restricts Adoption | -1.4% | Asia-Pacific emerging markets, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Intense Competition from Protein Shakes, Bars, And Other Beverages Affects Market Share | -1.7% | Global, particularly in North America and Europe | Short term (≤ 2 years) |

| Limited Differentiation Across Brands Makes Standing Out Difficult | -1.2% | Global, with highest impact in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Product Costs Limit Affordability for Mass-Market Consumers

Premium pricing strategies, while supporting brand positioning and margin objectives, create accessibility barriers that limit market penetration beyond affluent consumer segments. Protein ingredient costs, particularly for high-quality whey protein isolates and plant-based alternatives, represent significant input cost pressures that manufacturers typically pass through to consumers via retail pricing. The US Department of Commerce's anti-dumping determination on Chinese pea protein, with margins reaching 280.31%, further constrains cost-effective plant protein sourcing options and may accelerate domestic ingredient development initiatives Federal Register [4]Source: Federal Register, "Certain Pea Protein from the People's Republic of China", federalregister.gov. Manufacturing complexity associated with clear protein formulations, including specialized processing equipment and quality control requirements, adds operational costs that smaller brands struggle to absorb. The challenge intensifies in emerging markets where disposable income constraints limit willingness to pay premium prices for functional beverages, potentially slowing geographic expansion and volume growth. Small and medium enterprises struggle to achieve profitable operations while matching market price expectations, leading to consolidation pressures.

Limited Awareness in Emerging Markets Restricts Adoption

Consumer acceptance of functional beverages across markets is heavily influenced by cultural factors and product familiarity. Regulatory frameworks in countries such as Australia, New Zealand, China, and Japan vary significantly, creating fragmented regulations that act as barriers to market entry. These barriers hinder protein water brands from achieving economies of scale across the region. Also, regulatory frameworks in emerging markets often lag behind developed regions in establishing clear guidelines for functional beverage claims, creating uncertainty for manufacturers seeking to communicate product benefits effectively. Additionally, limited consumer awareness of protein water's benefits compared to traditional hydration options further complicates market penetration. In emerging markets, consumers often associate protein supplementation with traditional food sources, necessitating substantial marketing investments to build category awareness before focusing on brand differentiation. Moreover, inadequate retail infrastructure in many emerging markets restricts distribution channels, forcing protein water brands to rely on premium outlets, which limits their mass-market reach and reduces opportunities for building consumer awareness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Clear Formulations Drive Premium Positioning

The non-flavored segment's accelerated growth at 14.78% CAGR through 2031 reflects sophisticated consumer preferences for minimalist formulations that prioritize functional benefits over taste masking. Despite flavored variants commanding 71.45% market share in 2025, the trajectory toward unflavored options indicates maturation of consumer palates and increased confidence in protein water's inherent taste profile. Clear whey protein isolate technology, which enables transparent formulations without compromising protein content, addresses consumer demand for "clean" visual presentation while maintaining nutritional efficacy. The shift parallels broader beverage industry trends toward reduced sugar content and artificial ingredient elimination, supported by the FDA's updated "healthy" labeling criteria that favor nutrient-dense formulations FDA.

Flavored segment dominance reflects mainstream consumer preferences for familiar taste profiles that ease transition from traditional sports drinks and flavored waters. Fruit-based flavors, particularly citrus and berry combinations, leverage established consumer acceptance while masking potential protein aftertastes that could limit repeat purchase behavior. Innovation in natural flavoring systems, including botanical extracts and fruit essences, addresses clean-label requirements while maintaining sensory appeal. The emergence of sophisticated flavor profiles, such as protein coffee enhancers and adaptogenic blends, targets specific consumer segments seeking functional benefits beyond basic protein supplementation

By Packaging: Sustainability Reshapes Container Innovation

PET bottles dominated with 74.10% of 2025 volume owing to entrenched manufacturing lines and light-weight logistics. However, cans are forecast to expand at a 13.94% CAGR to 2031 as climate-conscious millennials favor infinitely recyclable packaging. Early adopters tout lower greenhouse-gas footprints, while retailers appreciate can-friendly logistics and stackable displays that maximize shelf density. The protein water market size for can formats is likely to jump significantly as beverage fillers retrofit lines originally designed for flavored sparkling water. PET remains cost-efficient, particularly for clear-bottle shelf appeal and single-serve variants targeted at gyms and convenience stores. Yet corporate net-zero goals drive research into bio-PET, plant-derived caps, and tethered closures that align with forthcoming EU packaging rules.

Glass remains niche due to weight and shatter risk. Pouches appear in limited travel-friendly runs but face perception hurdles on recyclability. Ultimately, container differentiation complements flavor and functional stories, helping brands stand out in congested beverage coolers. Other packaging formats, including pouches and tetrapack, serve niche applications but face adoption barriers related to consumer perception and technical limitations in maintaining protein stability. The industry's movement toward sustainable PET alternatives, including bio-based and recycled content options, may bridge the gap between cost efficiency and environmental responsibility.

By Distribution Channel: Digital Commerce Accelerates Access

Supermarkets and hypermarkets contributed 44.85% of 2025 revenues, leveraging shopper trust and impulse-purchase visibility. Nonetheless, online retail posts an 17.62% CAGR through 2031, reflecting structural migration toward e-grocery and direct-to-consumer models. The protein water market size attributable to digital channels will expand steadily as auto-replenishment subscriptions shrink friction for repeat buyers who view the drink as a daily ritual. Social-media retargeting funnels shoppers to brand sites offering mixed-flavor bundles, personalized starter kits, and loyalty points redeemable for fitness accessories, thereby deepening engagement beyond price promotions. Brick-and-mortar chains respond with click-and-collect services, dedicated functional-beverage bays, and data-sharing partnerships that improve on-shelf assortment.

Secondary channels reinforce brand ubiquity. University dining programs test pilot contracts to compensate for often-criticized sugary drink portfolios, framing protein water as a better-for-you alternative. Convenience and grocery stores serve as important secondary channels for on-the-go consumption occasions, though their limited refrigerated space constrains SKU proliferation and brand visibility. The emergence of specialty health retail channels, including nutrition stores and fitness centers, targets core consumer segments with higher engagement levels and willingness to pay premium prices. Vending solutions in corporate campuses and transport hubs target white-collar commuters who seek light, refreshing fuel. Specialty health-food stores curate high protein SKUs alongside collagen bars and keto snacks, benefiting from aggregator foot traffic of label-conscious consumers.

Geography Analysis

North America's market leadership with 37.78% share in 2025 reflects mature protein supplementation culture and established functional beverage infrastructure that supports category development. The region benefits from sophisticated retail networks, including specialty nutrition stores and premium grocery chains, that provide optimal product placement and consumer education opportunities. Regulatory clarity from the FDA's updated "healthy" labeling guidelines, effective February 2025, creates favorable conditions for health claim communication and mainstream marketing strategies. Consumer willingness to pay premium prices for functional benefits, combined with high disposable income levels, supports sustainable business models for protein water brands.

Asia-Pacific emerges as the fastest-growing region at 13.67% CAGR through 2031, driven by expanding middle-class demographics, rising health consciousness, and government initiatives promoting functional foods. Japan's regulatory sophistication, demonstrated by the Consumer Affairs Agency's proposed revisions to functional food labeling requirements in June 2024, signals market maturation that could accelerate category legitimacy and consumer acceptance according to Food Compliance International. The region's preference for local flavors, such as yuzu and lychee, supports the launch of region-specific products, avoiding the negative perception of "Western protein shakes." The rapid adoption of mobile commerce in the region facilitates product sampling and consumer feedback, enabling agile start-ups to quickly refine their product offerings.

Europe and other regions represent emerging opportunities with varying regulatory landscapes and consumer acceptance levels that require localized market entry strategies. The region's emphasis on sustainability and clean-label formulations aligns with protein water positioning, though price sensitivity and established beverage preferences create adoption challenges. South America and Middle East and Africa markets remain nascent but offer long-term growth potential as economic development and urbanization drive functional beverage adoption. The global nature of protein water's appeal, combined with standardized manufacturing processes, enables scalable international expansion strategies for established brands with sufficient capital resources.

Regulatory Landscape

Protein water sits between packaged water, functional beverages, and sports nutrition, so compliance depends on ingredient status, fortification rules, and labeling or claims. In the United States, the FDA regulates protein-fortified beverages under the Federal Food, Drug, and Cosmetic Act, with formulation relying on permitted food additives or GRAS substances (as reflected in 21 CFR Parts 170-172) and mandatory Nutrition Facts labeling under 21 CFR Part 101. The FDA's updated "healthy" nutrient content claim framework, effective February 2025, acts as a commercialization anchor for lower-calorie, low-sugar protein water positioning, tightening the link between formulation variables (calories, added sugars, sodium, saturated fat) and on-pack claim eligibility.

In Europe, manufacturers work under harmonized fortification rules via Regulation (EC) No 1925/2006 (as amended), which governs the voluntary addition of vitamins, minerals, and certain other substances, while maintaining safety and compositional scrutiny when adding nutrients to beverages. Canada continues to manage fortification via Health Canada policies and the Food and Drug Regulations, and an industry compliance deadline of January 1, 2026 tied to updated vitamin D fortification requirements in specific milk and beverage categories highlights how changing fortification expectations can drive reformulation and relabeling work for protein water products using dairy-derived ingredients or vitamin-added positioning.

Competitive Landscape

The protein water market exhibits moderate fragmentation, creating opportunities for both established beverage conglomerates and specialized nutrition brands to capture market share through differentiated positioning strategies. The globally renowned companies in the market include Arla Foods amba, Protein2o, among others. The key players competing for major market shares and small regional players are catering to a small region, to gain market shares on the other end. Key players are scattered across all the regions, with the majority of them based in North America and Europe. The key strategies adopted by the players to maintain competitiveness in the market are expansions, innovations, and new product launches.

New market entrants are differentiating themselves by focusing on plant-based formulations, sustainable packaging solutions, and direct community engagement strategies. Some are collaborating with co-manufacturers to maintain asset-light financial models while reallocating resources toward digital marketing initiatives and influencer partnerships. Regional brands are capitalizing on local flavor preferences, such as mango-chili in Mexico and blackcurrant in Scandinavia, while utilizing small-batch storytelling to appeal to consumers seeking authenticity. Intellectual property efforts are concentrated on innovations like micro-filtration for protein clarity, proprietary flavor-masking technologies, and patented cold-fill processes that enhance shelf life without relying on preservatives.

Strategic approaches are diverging: large conglomerates are incorporating protein water into comprehensive “total hydration” portfolios, which include sports drinks, electrolyte beverages, and flavored waters, leveraging bundled promotions to drive sales. On the other hand, niche players are strengthening their brand communities by sponsoring boutique fitness studios and organizing interactive workout challenges to convert participants into long-term subscribers. The mergers and acquisitions (M&A) landscape remains active, with major beverage companies pursuing bolt-on acquisitions to enhance formulation expertise and build credibility with early-adopter demographics.

Protein Water Industry Leaders

-

Arla Foods amba

-

Protein2o

-

Agropur

-

Athlex Beverages Private Limited

-

Anand Milk Union Limited (AMUL)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product whitespace is forming around multifunctional hydration formats that extend beyond "protein-only" by combining clear protein with electrolytes, fiber, and sugar-free positioning. In May 2026, H2Pro+ introduced a functional protein water in New York built around whey protein isolate, prebiotic fiber, and electrolytes in a low-calorie format, while Not Rocket Science launched an RTD protein water in India combining 100% whey protein isolate with an electrolyte blend. Together, these launches reflect active premiumization around ingredient stacks that support both hydration and nutrition use cases, with faster concept-to-shelf cycles in channels that favor trial, including fitness, specialty retail, and e-commerce.

Manufacturing and formulation opportunities are also increasingly tied to ingredient and process technologies that support clarity, solubility, and shelf stability. Advances in plant protein solubility and clarity (for example, clear plant protein ingredients referenced in the market) expand the formulation toolkit for brands seeking dairy-free positioning while keeping a water-like sensory profile. In parallel, packaging and processing choices are improving retail flexibility. Partnerships such as SIG and Oobli, combining aseptic filling with sweet-protein based sugar reduction, point to how shelf-stable packaging concepts can reduce cold-chain dependence and support broader retail placements. Retail-led range expansion remains a near-term scale path, shown by Nichols and THG announcing a Myprotein Clear Whey Protein Water range for the UK (September 2026 launch window), positioned around a high-protein-per-serving proposition for mainstream consumers.

Recent Industry Developments

- July 2026: Nichols and THG announced a partnership to launch a new range of Myprotein Clear Whey Protein Water in the UK, timed for a September 2026 rollout. The partnership extends clear, water-like protein formats into a broader retail audience through an established sports-nutrition brand, supporting category normalization beyond niche fitness channels.

- June 2025: Amul launched a protein water in India in a clear 500 ml bottle, positioned around whey protein, zero sugar, and added electrolytes with a low-calorie profile. This release shows how large dairy players are using existing whey streams to enter ready-to-drink functional hydration and accelerate mass awareness for protein water in emerging markets.

- November 2024: Applied Nutrition introduced Sparkling Protein Water, formulated with protein, no sugar, electrolyte-rich coconut water powder, and added vitamin C in a canned format. The launch reinforced sparkling and can-packaged variants as a differentiation route in protein water, aligning the category with on-the-go consumption and broader functional beverage sets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers beverages sold as protein water, where protein (commonly isolates) is added to water and marketed for hydration plus protein intake. We size the market in value terms using retail and online sales of products positioned and labeled as protein water.

Scope exclusions: This sizing does not count ready-to-mix protein powders, standard RTD protein shakes, or broader functional waters that do not position as protein water.

Segmentation Overview

-

By Flavor

- Flavored

- Non-Flavored

-

By Packaging

- PET Bottle

- Can

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first market structure, especially what qualifies as protein water, how these products are sold, and where demand is showing up fastest. We referenced public sources such as U.S. FDA labeling guidance, USDA food and beverage context data, the European Commission food information rules, and consumption indicators from agencies such as WHO and OECD.

To make the model practical, we also reviewed company filings, investor presentations, retailer announcements, and press coverage to understand typical pack formats and pricing behavior across channels. In addition, a paid subscription for company financials and news was used selectively to sanity check revenue direction for key brands, plus a patent database scan helped validate activity around formulations and protein sources. These sources are illustrative only, and we used other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured questionnaires with beverage brands, ingredient and packaging participants, distributors, and channel-facing roles who see pricing and velocity changes early. For a global view, we kept coverage balanced across APAC, EMEA, and the Americas so assumptions on online growth, shelf expansion, and flavor mix could be challenged and then refined.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 18% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where category demand is reconstructed using regional functional beverage consumption signals, channel expansion patterns, and observed price bands for protein water. The totals are then corroborated with selective bottom-up approximations, such as sampled SKU-level ASPs multiplied by estimated volumes and channel checks, which helps adjust for undercounting in smaller online-led brands.

Key model inputs include average selling price by pack type (PET bottle, can, and other packs), share split between flavored and non-flavored products, distribution channel mix shifts (especially online retail versus grocery), and regional growth signals tied to health positioning and convenience formats. For forecasting, we used scenario analysis supported by expert consensus, where the base case is anchored to expected shelf space gains, online penetration, and steady pricing progression rather than a single aggressive adoption curve. When direct volume signals are missing for niche packs, we use conservative proxy assumptions, then pressure-test them in interviews until the implied growth stays realistic.

Data Validation & Update Cycle

Validation is handled through multiple checks, where modeled outputs are compared against independent indicators such as pricing spreads, channel mix direction, and regional demand momentum. Outliers are reviewed in detail, and when a variance cannot be explained by scope or timing, we recheck assumptions and trigger a follow-up conversation with relevant participants.

Before sign-off, the full dataset and calculations go through a multi-step analyst review so arithmetic, unit conversions, and logic consistency are confirmed. The report is refreshed annually, and interim updates are made when major events shift pricing, distribution access, or category definitions. Right before delivery, a final pass is completed so clients get the latest view aligned with the most recent public signals.

Mordor Intelligence's Protein Water Market Estimate Compared With Other Published Estimates

Published market sizes for protein water can look far apart even when the topic sounds the same, because the boundaries and the counted product forms are not always consistent. Differences also come from how prices are treated, whether the base year is aligned, and how aggressively adoption is projected in newer channels.

By tracking channel-by-channel pricing and refreshing scope checks annually, Mordor Intelligence keeps the count limited to protein water beverages and avoids mixing in ready-to-mix powders or broader functional drink pools, which can lift totals quickly. Another common gap driver is currency timing and regional weighting, since fast growth in one region can change the global curve when assumptions are not validated with local channel feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 92.81 M (2026) | |

| Global Consultancy A | USD 848.60 M (2024) | Uses a broader revenue pool that can include adjacent functional drink interpretations and wider product definitions, with a different base year, which makes direct alignment with a protein-water-only boundary difficult. |

| Industry Publisher B | USD 1.38 B (2025) | Explicitly includes ready-to-mix powder formats and wider packaging and channel structures, so the scope expands beyond beverages sold strictly as protein water, which pushes the stated value higher. |

The comparison shows that most of the spread is created by scope choices first, and then by base-year timing and pricing treatment. When definitions are held steady and assumptions are checked against channel realities, the resulting market size becomes easier to trace, replicate, and use for planning.

Key Questions Answered in the Report

What is the current size of the protein water market?

The protein water market is valued at USD 92.81 million in 2026 and is forecast to hit USD 169.79 million by 2031, reflecting a 12.86% CAGR.

Which region leads protein water revenues today?

North America leads with 37.78% of 2025 sales owing to mature sports-nutrition culture and clear regulatory guidance.

Which flavor segment is growing fastest?

Non-flavored SKUs grow at a 14.78% CAGR to 2031 as consumers gravitate toward minimalist ingredient lists.

How important is online retail for protein water?

Online retail is the fastest-expanding channel, projected to post an 17.62% CAGR through 2031 as shoppers favor subscription and direct-to-consumer convenience.

Page last updated on: