Polyurethane for Footwear Applications Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

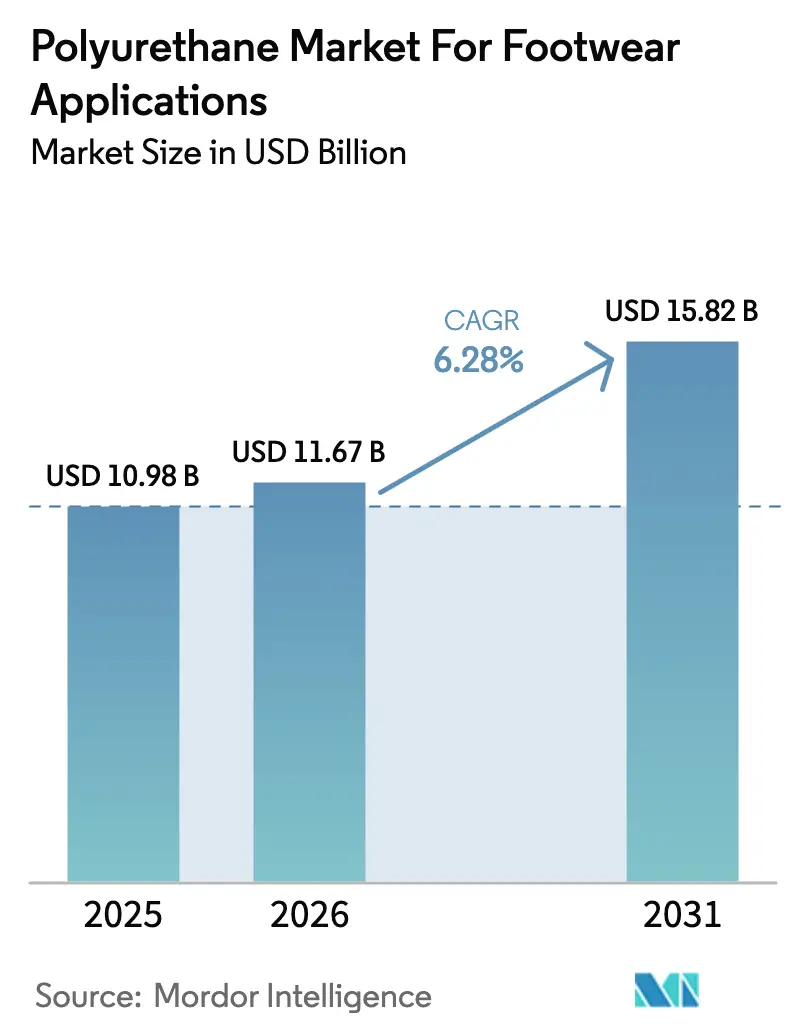

| Market Size (2026) | USD 11.67 Billion |

| Market Size (2031) | USD 15.82 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

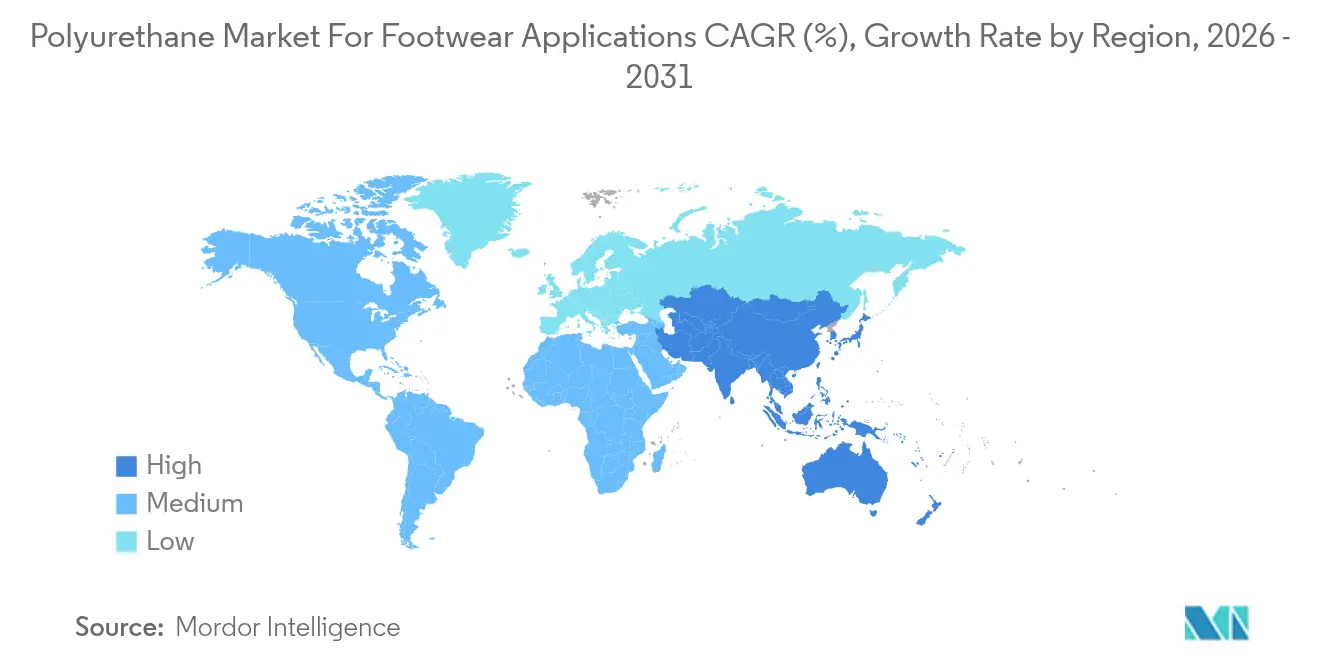

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurethane for Footwear Applications Market Analysis by Mordor Intelligence

The Polyurethane Market size For Footwear Applications market is expected to grow from USD 10.98 billion in 2025 to USD 11.67 billion in 2026 and is forecast to reach USD 15.82 billion by 2031 at 6.28% CAGR over 2026-2031. Robust demand for light yet durable soling solutions, mainstreaming of athleisure, and stringent sustainability targets are combining to keep the polyurethane sole footwear market on a steady upward path. Rising disposable incomes in emerging economies, coupled with rapid manufacturing automation, are shortening lead times and further supporting volume growth. Producers that master lightweight cushioning technologies and circular-ready chemistries are winning orders from global brands that are under pressure to phase out heavier, less durable materials. Volatile feedstock prices remain an overhang, yet supply-chain integration and long-term procurement contracts are helping leading manufacturers preserve margins while ensuring stable customer deliveries.

Key Report Takeaways

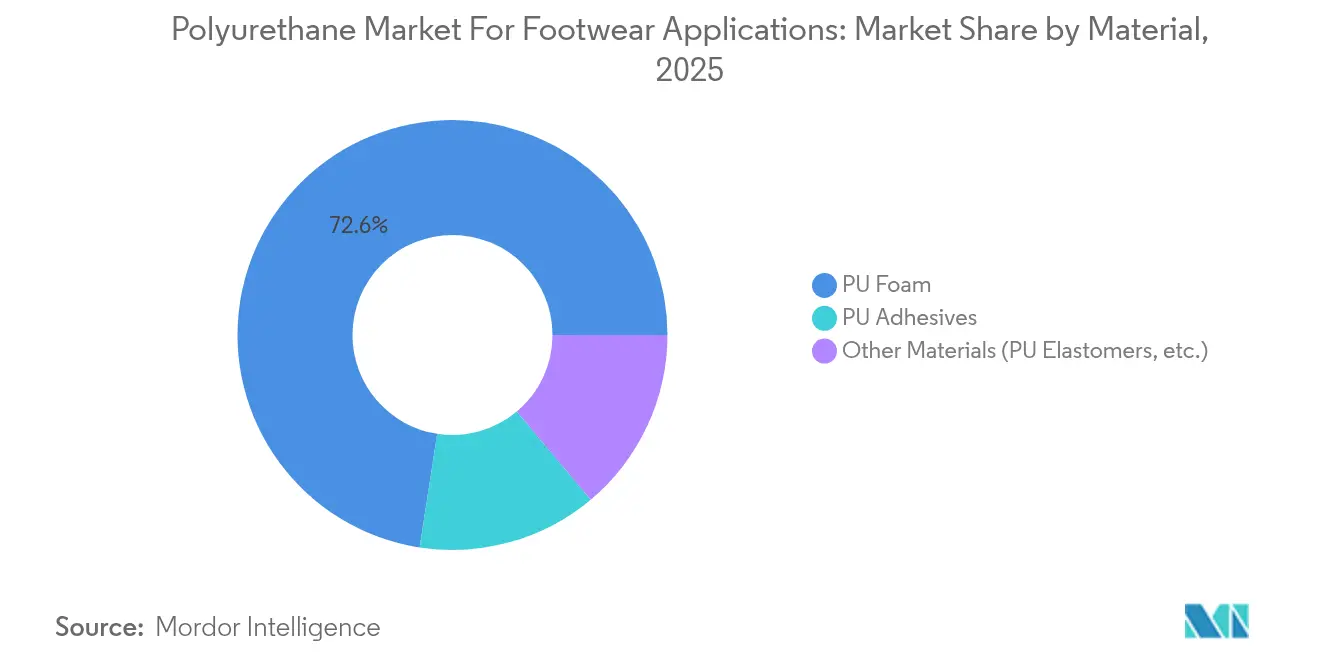

- By material, PU foam led with a 72.56% revenue share of the polyurethane sole footwear market in 2025, while Other Materials are forecast to expand at a 6.92% CAGR through 2031.

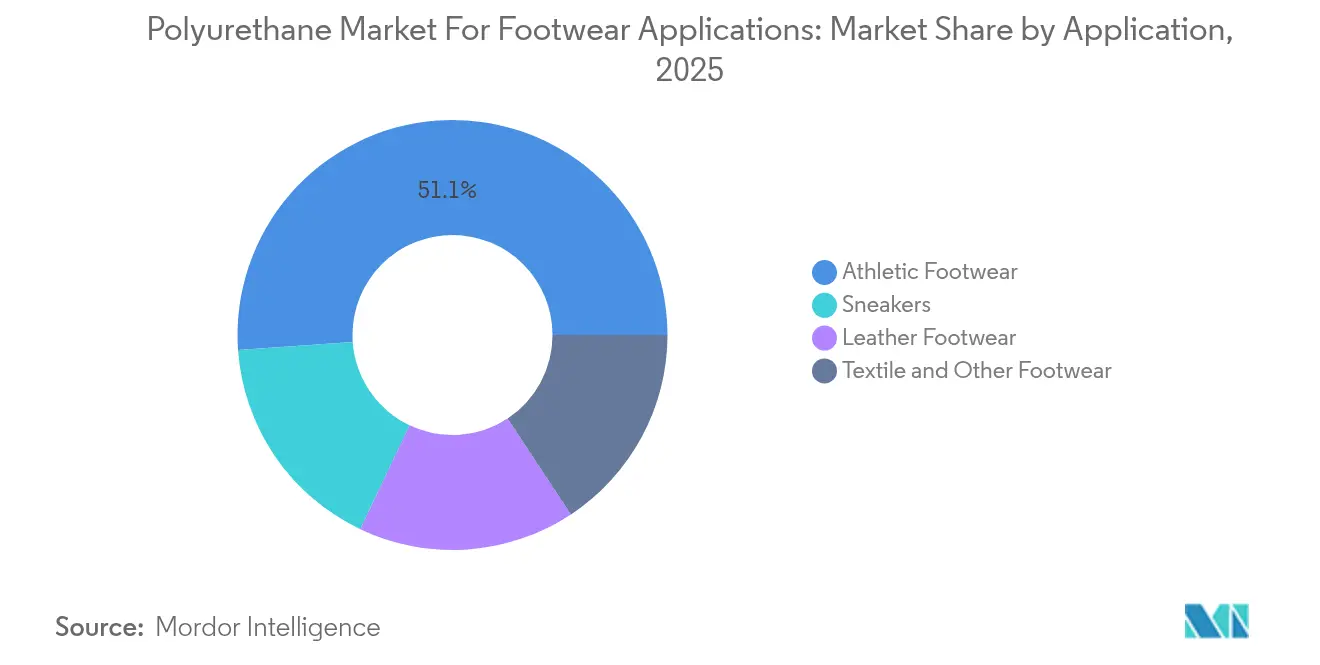

- By application, athletic footwear commanded 51.12% of the polyurethane sole footwear market size in 2025; the sneakers segment is poised to grow at a 7.18% CAGR to 2031.

- By geography, Asia-Pacific accounted for 48.62% of the polyurethane sole footwear market share in 2025 and is projected to post the fastest regional CAGR of 6.79% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Polyurethane for Footwear Applications Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global footwear production volumes | +1.80% | Global, concentrated in APAC hubs | Medium term (2-4 years) |

| Superior lightweight cushioning properties of PU soles | +1.50% | North America & Europe premium tier | Long term (≥ 4 years) |

| Shift toward athleisure & performance footwear in emerging markets | +1.20% | Core APAC, spill-over to LATAM | Short term (≤ 2 years) |

| Automation of PU sole injection molding in low or mid tier factories | +0.90% | APAC, expanding to Mexico | Medium term (2-4 years) |

| Adoption of bio-based polyols to lower PU carbon footprint | +0.70% | Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising global footwear production volumes

Escalating factory output in Vietnam, India, and coastal China continues to support the Polyurethane for Footwear Applications Market by widening the installed base of direct-injection lines. Producers like ZhongJie-KY are scaling capacity targets to 80 million pairs annually, funded by USD 60 million in multi-country capex programs. High-volume runs improve fixed-cost absorption, letting suppliers buffer MDI and TDI price swings without sacrificing margins. Vietnam’s supportive tax holidays and cluster-driven infrastructure upgrades enhance its appeal as brands look to diversify beyond single-country sourcing models.

Superior lightweight cushioning properties of PU soles

Polyurethane rebounds efficiently after compression, retains structural integrity over 11 million flexes, and delivers higher energy return than EVA. Brooks Running switched half of its lineup to DNA AMP polyurethane midsoles, citing longer-lasting responsiveness that appeals to serious runners[1]Brooks Running, “DNA AMP Technology Overview,” basf.com . In premium European markets, consumers increasingly equate durability with value, reinforcing demand for PU-based cushioning that outperforms legacy foams over time.

Shift toward athleisure & performance footwear in emerging markets

Middle-class consumers in Asia now want shoes that look casual yet perform like trainers. That trend is why sneakers, though smaller in absolute revenue, are accelerating faster than classic running shoes within the polyurethane sole footwear market. PUMA’s Emerge model integrates 35% sugarcane-derived foam while maintaining gym-worthy bounce. Such lifestyle-performance hybrids support higher average selling prices, rewarding suppliers that can fine-tune density, rebound, and surface finish.

Adoption of bio-based polyols to lower PU carbon footprint

Polyols derived from algae oils and agricultural residue can cut cradle-to-gate emissions by up to 50%. UC San Diego research teams have demonstrated 100% bio-based polyurethane foams that avoid phosgene and retain commercial-grade tensile strength. Huntsman’s tie-up with BLUMAKA delivers midsoles containing 75% recycled content for surf-lifestyle brand Sanuk[2]Huntsman, “BLUMAKA Partnership on Recycled Foam,” huntsman.com . Early adoption remains concentrated in Europe, yet brand-level net-zero targets signal global scale-up later this decade.

Restraints Impact Analysis of Polyurethane for Footwear Applications Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile MDI orTDI feedstock prices tightening margins | -1.10% | Global, acute in APAC | Short term (≤ 2 years) |

| Stringent EU & US regulations on di-isocyanate exposure | -0.80% | Europe & North America | Medium term (2-4 years) |

| Collection & recycling challenges for post-consumer PU soles | -0.40% | Developed circular-economy markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU & US regulations on di-isocyanate exposure

New training and workplace labeling rules in the European Union, in force since 2024, add compliance costs for companies still operating legacy “free” monomer lines. LANXESS already markets low-free prepolymers that satisfy the directive and has highlighted regulatory readiness as a post-sale advantage after transferring its urethanes unit to UBE. U.S. OSHA is reviewing similar exposure thresholds, signaling higher overhead for converters that postpone upgrading ventilation and monitoring systems.

Collection & recycling challenges for post-consumer PU soles

Polyurethane’s cross-linked structure complicates end-of-life recovery. While closed-loop demonstrations such as Adidas Futurecraft Loop shoes prove technical feasibility, commercial networks to retrieve, separate, and process waste remain nascent[3]Adidas, “Futurecraft Loop Phase 3 Update,” adidas-group.com . In regions where extended-producer-responsibility rules tighten, inability to certify recycling volumes could expose brands to eco-fees that dampen demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Polyurethane for Footwear Applications Market Segment Analysis

By Material:

PU foam maintains lead yet specialty alternatives gain groundPU foam generated 72.56% of the Polyurethane for Footwear Applications Market revenue in 2025 and is forecast to advance in lock-step with total footwear output. The segment benefits from massive installed capacity, extensive operator know-how, and well-understood injection parameters that keep defect rates low.

However, thermoplastic polyurethanes and bio-based variants within the Other Materials grouping are expanding at a 6.92% CAGR. These materials attract brands that want transparent end-of-life recyclability, solvent-free bonding, or enhanced slip resistance in wet conditions. BASF’s Elastollan TPU delivers both recyclability and wet-grip advantages, positioning specialty grades to nibble share where occupational safety rules are tightening. With brand roadmaps increasingly linking material selection to public carbon disclosures, specialty resins are expected to secure incremental contracts in high-visibility product lines even as PU foam remains the industry workhorse.

By Application:

Sneakers outpace athletic-only designs in growth momentumAthletic footwear accounted for 51.12% of the Polyurethane for Footwear Applications Market in 2025, underpinned by running, basketball, and cross-training models that rely on resilient midsole foam. The segment’s scale ensures consistent offtake for full-truckload deliveries of MDI-based systems, anchoring many suppliers’ production plans.

Sneakers, though contributing a smaller revenue base, are set to grow at 7.18% annually thanks to the lifestyle-performance crossover. Consumers now expect the same cushioned ride in casual silhouettes, and direct-injection polyurethane lets brands maintain slim profiles without sacrificing underfoot comfort. Leather footwear also absorbs polyurethane upgrades, notably through fully recyclable synthetic leather overlays that bond seamlessly to PU midsoles and simplify future de-manufacturing.

Geography Analysis

APAC Polyurethane for Footwear Applications Market

Asia-Pacific controlled 48.62% of global revenue in 2025 and is projected to advance at 6.79% through 2031, ensuring that the Polyurethane for Footwear Applications Market continues to gravitate toward its manufacturing heartland. Policy-backed industrial parks in Tamil Nadu, India, are creating integrated clusters that cut outbound logistics costs and compress prototype-to-launch timelines for global brands. China retains the broadest tooling base, yet labor-intensive shops in Fujian and Guangdong are automating to offset rising wage floors and power-supply constraints.

North America Polyurethane for Footwear Applications Market

North America remains integral for innovation pilots and limited-run releases. Reebok’s Liquid Factory concept uses polyurethane drawn by multi-axis robots to build midsoles without aluminum molds, slashing tooling cost and enabling domestic production at consumer-accepted price points. Brands leverage such projects to test hyper-personalized fits and then shift mature designs to Asia for scale manufacture once demand stabilizes.

Europe Polyurethane for Footwear Applications Market

Europe exerts global influence through regulatory leadership. The region’s push for circular economy legislation encourages suppliers to introduce take-back schemes and mono-material constructions. Covestro’s INSQIN waterborne, partly bio-based PU coatings help European tanneries comply with VOC limits while unlocking breathable, chrome-free laminates. Although operating costs are higher than in Asia, brand-owned factories in Portugal, Germany, and Italy keep select production local to showcase rapid design-turn speeds and high craft quality.

Competitive Landscape

Competition is moderately fragmented, with chemical multinationals supplying the bulk of pre-polymer systems, and a growing tier of sustainability-focused specialists. LANXESS offloaded its Urethane Systems division to UBE for EUR 460 million in 2024, signaling continued portfolio pruning among diversified groups seeking to sharpen strategic focus. The deal hands UBE a ready-made customer base in footwear adhesives and elastomers while freeing LANXESS to channel capital toward higher-margin segments.

BASF leads in breadth of supply, offering Elastopan PU, Elastollan TPU, and Infinergy expanded TPU, enabling brand customers to mix and match rebound levels without switching vendors. Covestro amplifies competitive pressure through INSQIN’s solvent-free coating suite, which delivers color-fast finishes compatible with recycled fabrics. Huntsman invests in field-service engineering, installing dosing equipment at customer plants so small converters can switch from manual mixes to automated metering with minimal downtime.

Disruptors such as Algenesis, whose Soleic biopolyurethane midsoles fully compost in soil, keep incumbents alert to step-change sustainability. Despite scale hurdles, such innovations secure pilot contracts from eco-driven labels, nudging mainstream suppliers to accelerate their own bio-feedstock programs. Overall, no single company holds more than 15% of world revenue, yet the top five capture close to half, placing market concentration at mid-level.

Polyurethane for Footwear Applications Industry Leaders

BASF SE

Covestro AG

Huntsman International LLC

Dow

Wanhua

- *Disclaimer: Major Players sorted in no particular order

Polyurethane for Footwear Applications Market Companies Covered in this Report

- BASF SE

- Coim Group

- Covestro AG

- Dow

- Era Polymers Pty Ltd

- Huafeng Group

- Huntsman International LLC

- INOAC Corporation

- LANXESS

- Manali Petrochemicals Ltd

- NUI

- OrthoLite

- Rogers Corporation

- The Lubrizol Corporation

- Trelleborg

- Wanhua

Read Analysis of Polyurethane for Footwear Applications Companies

Recent Industry Developments in Polyurethane for Footwear Applications Market

- April 2025: KPR King Power (KPR), one of the key player in the safety footwear industry, has partnered with BASF to produce safety shoes utilizing Elastopan Loop. This advanced material is a recycled polyurethane (PU) solution that incorporates recycled PU components.

- November 2024: Dow introduced a low-carbon material portfolio for the footwear market, featuring bio-circular materials, post-consumer recycled resins, and polyolefin elastomers. Dow partnered with Porto Indonesia Sejahtera to integrate REVOLOOP recycled resins into premium sandals and flip-flops, advancing circular footwear solutions.

Polyurethane for Footwear Applications Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the polyurethane market for footwear applications as the value of virgin PU resins, flexible foams, elastomers, thermoplastic grades, and related pre-polymers sold to produce shoe outsoles, midsoles, insoles, and bonded uppers across athletic, casual, work-safety, and fashion categories worldwide. According to Mordor Intelligence, ancillary PU used as contact adhesives or surface coatings is counted only when directly consumed inside footwear manufacturing plants.

Scope exclusions include reworked scrap, post-consumer recycled PU, and any PU captured in complete shoe retail sales, which are outside scope.

Segments Covered in This Report

- By Material

- PU Foam

- PU Adhesives

- Other Materials (PU Elastomers, etc.)

- By Application

- Athletic Footwear

- Leather Footwear

- Sneakers

- Textile and Other Footwear

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

Multiple touchpoints, including raw-material suppliers, outsole molders, contract shoe manufacturers, and regional brands across Asia, Europe, and the Americas, validated demand hotspots, ASP progressions, and bio-based uptake. Interviews also helped us stress-test duty-driven trade shifts and seasonality before locking model assumptions.

Desk Research

We began with trade statistics from UN Comtrade, Eurostat, and China Customs, which reveal import-export flows of MDI, TDI, and finished PU soles that anchor the consumption pool. Industry associations such as Plastics Europe, the Footwear Distributors & Retailers of America, and the World Footwear Yearbook supplied production, cost, and pair-per-capita trends. Company 10-Ks, investor decks, and environmental disclosures let us derive average selling prices and plant utilizations. To cross-check volumes, our analysts pulled shipment traces from Volza and patent trends from Questel. These sources illustrate market mechanics, yet they are not exhaustive; many additional public and paid materials informed the desk phase.

Market-Sizing & Forecasting

We applied a top-down and bottom-up blend. Global footwear pair output and regional PU-per-pair coefficients framed the demand pool, which was then balanced against export-adjusted PU resin shipments and sampled ASP × volume roll-ups from key suppliers. Drivers such as athletic-footwear penetration, average outsole weight, MDI price index, disposable income growth, and regulatory caps on di-isocyanate exposure feed our multivariate-regression forecast. Where plant-level data were thin, proxy ratios from comparable facilities bridged gaps, and findings were re-benchmarked with expert consensus before finalization.

Data Validation & Update Cycle

Every quarter, our team scans trade prints, PU feedstock moves, and footwear production surveys to flag variances. Models undergo peer review, anomaly checks, and management sign-off; full refreshes publish annually, with mid-cycle tweaks when material events arise.

How Mordor Intelligence's Polyurethane for Footwear Applications Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick different material sets, convert currencies on assorted dates, and refresh at uneven cadences.

Key gap drivers include narrower raw-material inclusion, limited Asia primary checks, and one-off inflation adjustments used by other publishers, whereas our analysts keep a live watch on PU resin shifts and recalibrate coefficients each year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.98 B (2025) | Mordor Intelligence | - |

| USD 5.90 B (2024) | Global Consultancy A | Omits PU adhesives; older base year and static FX rates |

| USD 6.37 B (2024) | Trade Journal B | Focuses only on flexible foam; relies on desk data with ad-hoc updates |

The comparison shows that when scope breadth, timely field inputs, and recurrent audits converge, Mordor delivers a balanced, transparent baseline that decision-makers can replicate and trust. We believe this disciplined approach lets clients act with greater certainty in fast-moving footwear value chains.

Key Questions Answered in the Report

What is the current value of the Polyurethane for Footwear Applications Market?

The Polyurethane for Footwear Applications Market size stands at USD 11.67 billion in 2026 and is forecast to reach USD 15.82 billion by 2031.

Which region dominates global demand?

Asia-Pacific leads with a 48.62% revenue share in 2025 and is projected to post the fastest regional CAGR of 6.79% through 2031.

Which material category grows fastest?

Within material category, other materials grow at 6.92% annually, outpacing traditional PU foam.

Why are sneakers growing faster than classic athletic shoes?

Consumers favor versatile silhouettes that merge casual aesthetics with performance cushioning, driving a 7.18% CAGR for sneakers against the mature athletic segment.

How are manufacturers lowering polyurethane’s carbon footprint?

Producers are incorporating bio-based polyols, recycled foam granules, and solvent-free coatings, with early adopters already offering midsoles containing up to 75% recycled content.

What risk do feedstock price swings pose?

MDI and TDI volatility can compress converter margins by more than 1 percentage point, especially for factories lacking long-term supply contracts or captive upstream capacity.

Page last updated on: