Polyurethane (PU) Film Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

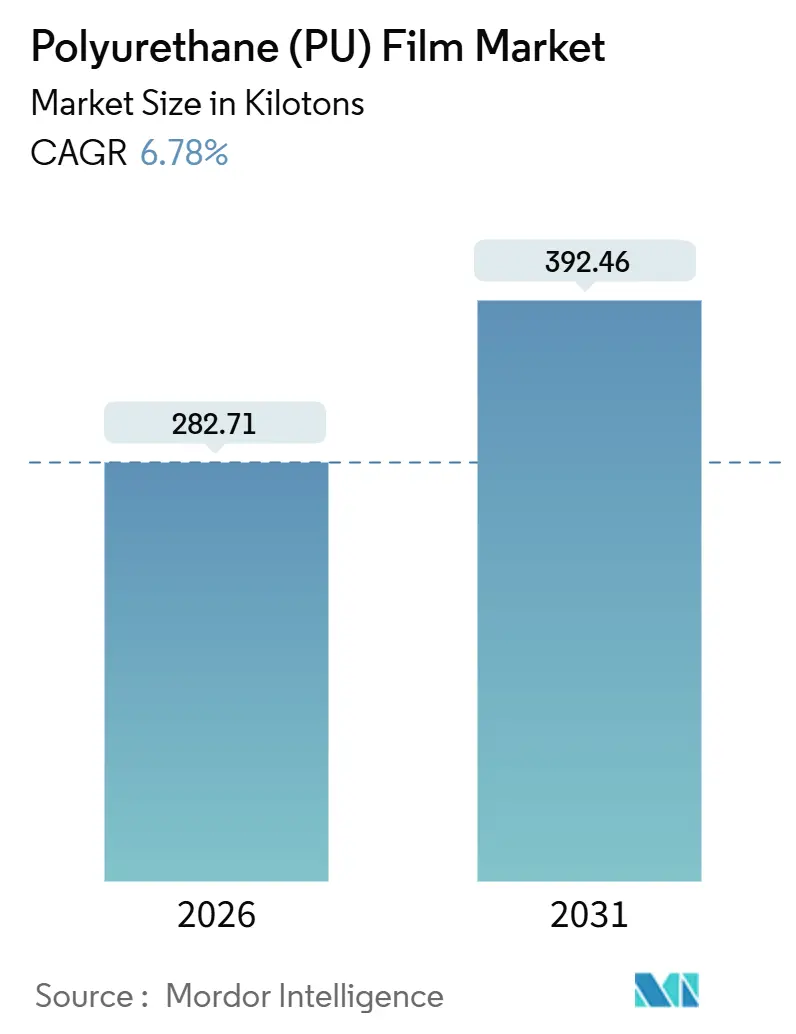

| Market Volume (2026) | 282.71 kilotons |

| Market Volume (2031) | 392.46 kilotons |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurethane (PU) Film Market Analysis by Mordor Intelligence

The Polyurethane Film Market size is estimated at 282.71 kilotons in 2026, and is expected to reach 392.46 kilotons by 2031, at a CAGR of 6.78% during the forecast period (2026-2031). Demand pivots on the phase-out of polyvinyl chloride in regulated applications, rapid uptake of low-VOC coatings for unmanned aerial vehicles, and surging preference for waterproof breathable membranes in premium outdoor apparel. Suppliers are adding specialty‐grade capacity in Asia-Pacific to capture local sourcing mandates, while North American medical-supplies buyers accelerate qualification of polyether grades following tightened FDA leachable limits. Vertical integration, exemplified by ADNOC’s 2025 acquisition of Covestro, hedges feedstock volatility and signals a structural shift toward crude-to-polymer models. At the same time, specialty converters create white space through self-healing topcoats, bio-attributed feedstocks, and ultra-thin optical films for foldable displays. These cross-currents sustain mid-single-digit growth even as margin pressure forces product differentiation through antimicrobial treatments and recycled-content claims.

Key Report Takeaways

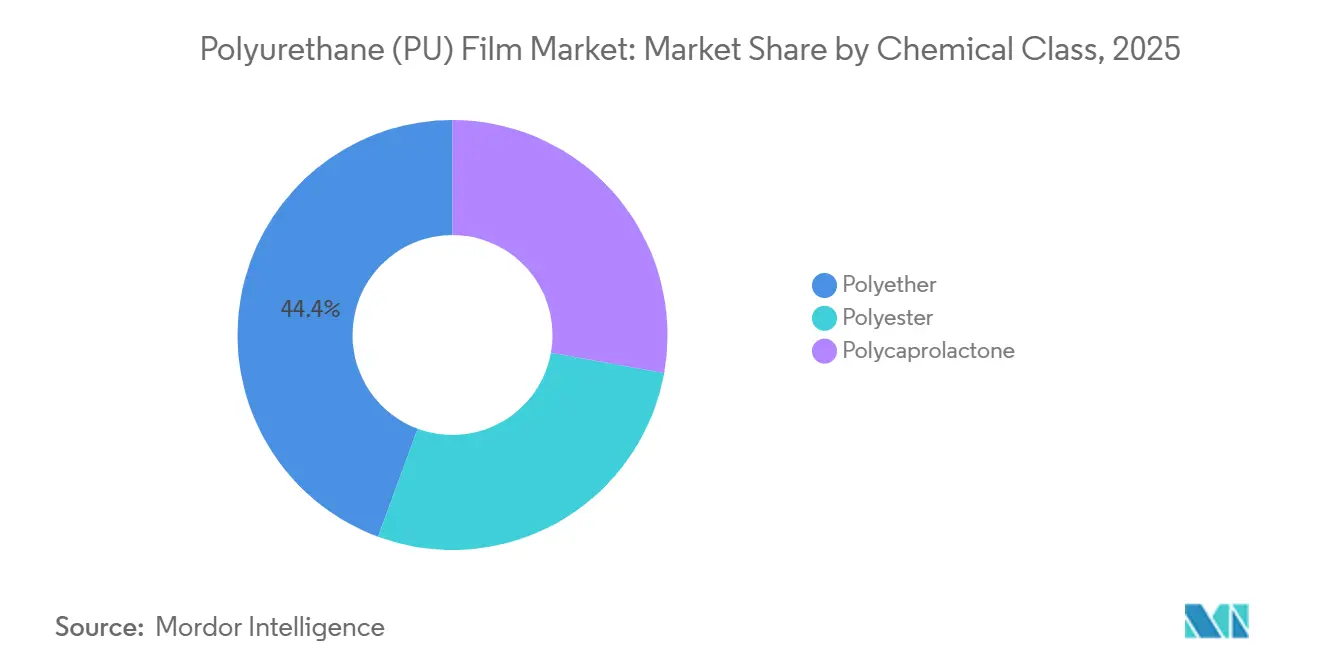

- By chemical class, polyether held 44.36% of the polyurethane film market share in 2025, while polycaprolactone is projected to expand at a 7.01% CAGR through 2031.

- By processing method, cast film extrusion led with a 41.28% share of the polyurethane film market size in 2025, and solution coating is forecast to grow at a 6.94% CAGR to 2031.

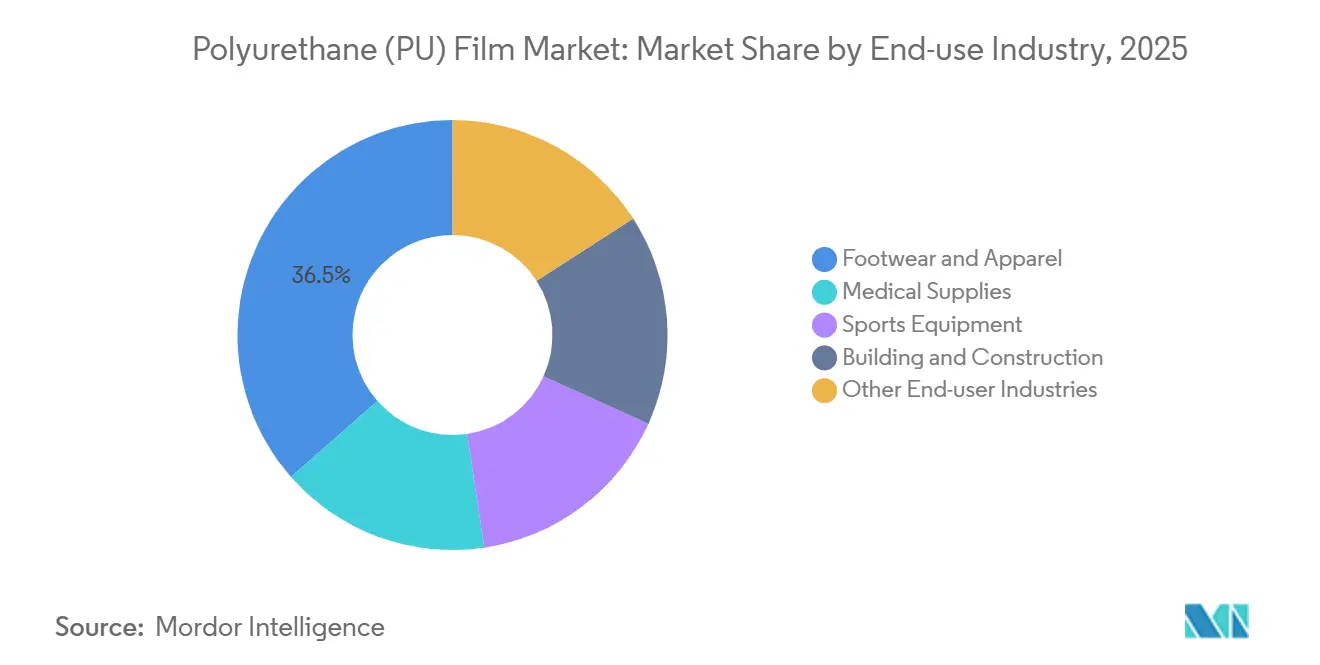

- By end-use industry, footwear and apparel accounted for 36.47% of the polyurethane film market size in 2025; medical supplies represent the fastest segment with a 7.08% CAGR to 2031.

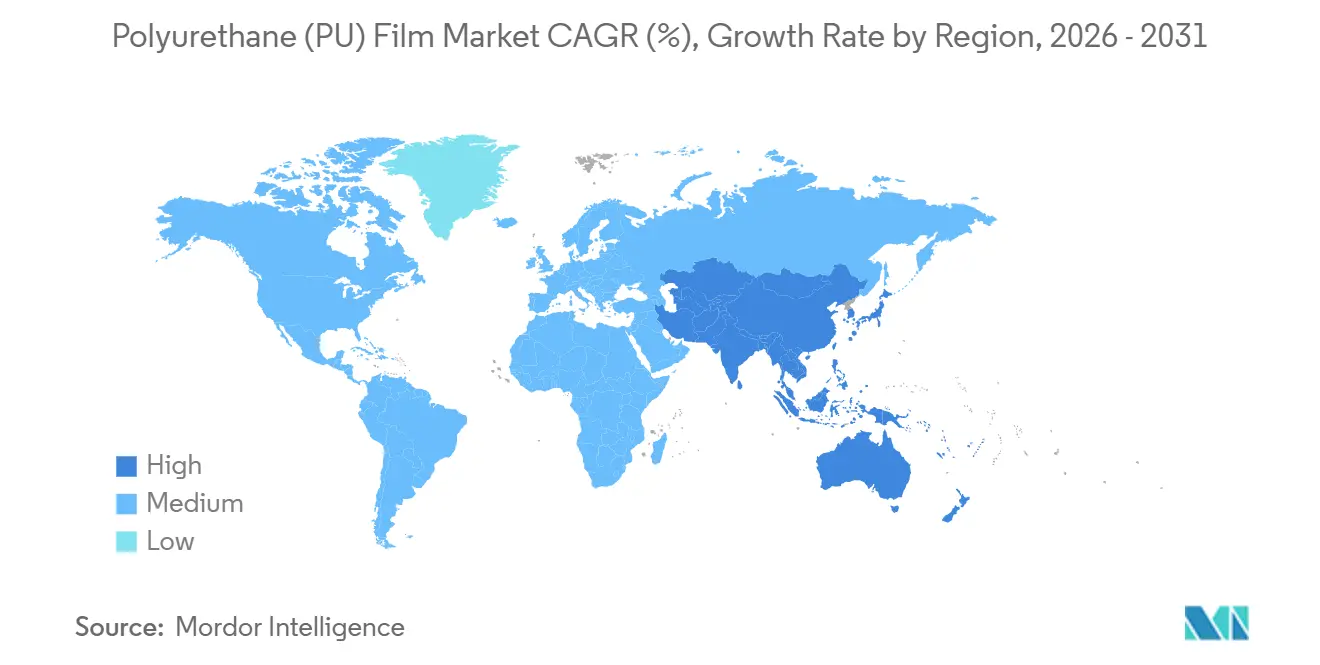

- By geography, Asia-Pacific commanded 49.52% volume in 2025 and is advancing at a 6.93% CAGR through 2031, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyurethane (PU) Film Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waterproof breathable membranes in performance sportswear | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| PVC substitution in medical devices under REACH and FDA scrutiny | +1.5% | North America, EU, Japan | Short term (≤ 2 years) |

| Foldable electronics requiring ultra-thin optical films | +0.9% | South Korea, China, United States | Long term (≥ 4 years) |

| Paint-protection films in used-car refurbishing | +1.3% | United States, EU, China tier-2 cities | Medium term (2-4 years) |

| Low-signature polyurethane coatings for UAV skins | +0.7% | United States, NATO Europe, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Waterproof and Breathable Membranes in High-Performance Sportswear

Outdoor-apparel brands are redesigning membrane stacks as scrutiny of fluorinated chemicals intensifies. GORE-TEX commercialized its ePE membrane with major brands for the 2025 winter collections, replacing fluoropolymer-rich laminates while keeping durability benchmarks[1]W. L. Gore & Associates, “GORE-TEX ePE Membrane Technology,” gore-tex.com. Polyether films dominate because their hydrolytic stability extends product life in humid climates, reducing warranty claims and supporting a 6.78% polyurethane film market CAGR. Converters now graft hydrophobic siloxane groups by plasma treatment, lowering contact angles below 110° without PFAS and maintaining breathability. Investment in Asian coating lines reflects the regional concentration of contract manufacturers that supply global brands. This pull-through effect reinforces demand visibility for 2026-2028 purchase cycles.

Rapid Substitution of PVC Films in Medical Device Components Owing to REACH and FDA Pressure

The European Chemicals Agency banned lead stabilizers in PVC in 2023, and the FDA updated guidance in 2024 to tighten phthalate controls, prompting North American and EU hospitals to migrate to polyether films that meet ISO 10993 without extra extractable testing[2]European Chemicals Agency, “Restriction of Lead in PVC – REACH Annex XVII,” echa.europa.eu. Medical buyers value the reduced gas permeability of polyurethane, which extends IV-bag shelf life, and procurement teams are awarding multiyear contracts that underpin a 7.08% CAGR for the segment. Ease of compliance shortens validation cycles by up to nine months, accelerating conversions across infusion, surgical-drape, and wound-care portfolios. Japanese device manufacturers mirror this trend to secure uninterrupted export certification.

Growth of Foldable and Flexible Electronics Requiring Ultra-Thin Optical-Grade Films

Samsung Display and BOE have successfully tested polyurethane dielectric layers, which reduce operating voltages in organic TFT backplanes. This breakthrough highlights a niche advantage for dielectric constants. South Korean coating lines will be able to handle advanced gauges with minimal haze. However, they face a rejection rate challenge due to a narrow thermoforming window. The crystallization lag of polycaprolactone complicates inline control, leading to a continued reliance on polyether grades, despite their higher cost. As production capacities increase, producers in the APAC region are emphasizing ISO 9001 standards and Class 1000 cleanrooms. This focus not only helps them pass stringent consumer-electronics audits but also solidifies their dominance in the lucrative polyurethane film market.

Mass Adoption of Paint-Protection Films in Used-Car Refurbishing Ecosystems

In North America, installers are now using self-healing 8-mil films that reflow at 60 °C to wrap entire vehicles, achieving a labor time reduction. With a stable U.S. used-car base for 2024, installers have a consistent retrofit pool, unaffected by new-car cycles. XPEL’s DAP software, boasting pre-cut patterns, minimizes fitment errors, driving the demand for solution-coated polyurethane to grow annually. Lubrizol’s expansion of TPU grades tailored for paint protection in Shanghai, set for April 2024, supports this rising demand. Meanwhile, converters are setting themselves apart by introducing antimicrobial and recycled-content variants, which fetch price premiums.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile MDI/TDI feedstock pricing | -1.1% | Global, acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Supply-demand imbalance for specialty diols | -0.8% | North America, EU | Medium term (2-4 years) |

| Narrow processing windows driving high rejection rates | -0.6% | APAC electronics hubs, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile MDI/TDI Feedstock Pricing Linked to Benzene and Crude Swings

Between November 2024 and January 2025, European MDI spot prices surged. This uptick was largely influenced by benzene's alignment with Brent's fluctuations. Additionally, an outage at BASF's cracker led to a reduced supply of aniline, further tightening converter margins. Huntsman initiated a strategic review that highlights the challenges mid-tier producers face in navigating market spikes due to their limited scale. While vertical integration presents a potential solution, ADNOC's acquisition of Covestro stands out as a prime example of the industry's pivot towards securing captive feedstocks, particularly in the polyurethane film sector.

Supply-Demand Imbalance of Specialty Diols After 2024 Capacity Outages

In 2024, a European plant faced an extended outage, disrupting the supply of hydrogenated MDI. This led to spot premiums rising above contract prices and pushed lead times significantly. In response, paint-protection converters turned to lower-UV-resistance aliphatic diols, a move that jeopardized warranty claims due to tightening yellowness limits. Meanwhile, small extruders postponed orders in late 2024. This delay underscored the industry's vulnerability, especially given that lead times for specialty diols can stretch significantly for new capacities. With fresh units not set to commence operations until 2026, procurement risks loom large, tempering the aggressive growth targets in high-clarity applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Class: Polyether Holds Tropical-Climate Edge

Polyether chemistry carried 44.36% of the 2025 volume, bolstered by its hydrolytic stability. This stability has made it a preferred choice for sectors like footwear, outdoor gear, and building membranes, especially in regions where humidity levels soar above 80% for most of the year. The market for polyurethane films, a subset of this category, is poised for growth. This is largely due to the introduction of bio-attributed MDI, which permits renewable content without the need for reformulation. Polycaprolactone variants, however, post a 7.01% CAGR, driven by their use in ISO 10993-approved wound dressings. These dressings offer the advantage of in-situ biodegradation, streamlining clinical removal processes. On the other hand, certain polyester grades are losing market share. This is primarily because paint-protection installers are opting for polyether. Its lower glass-transition temperature makes it more suitable for self-healing topcoats. Additionally, initiatives like Covestro’s glycolysis recycling partnership, which focuses on circular raw materials, further solidify polyether's dominance in the polyurethane film market.

While emerging capacities in the Asia-Pacific region could reshape cost dynamics by 2028, polyether's technical advantages remain formidable. This is true until polycaprolactone reaches cost parity within a competitive margin. Reinforcing this premium pricing power are hospital formularies and sustainability commitments from consumer brands. Vendors are capitalizing on this by highlighting their recycled-content certifications. Such factors bolster resilience in the face of challenges, like the oversupply of commodity TPU, which is exerting pressure on baseline margins throughout the polyurethane film sector.

By Processing Method: Solution Coating Gains on Gauge Flexibility

Cast extrusion retained 41.28% volume in 2025, leveraging its ability to run various gauges at high speeds, thus securing a unique cost-per-ton edge. Yet solution coating grows 6.94% annually. These films boast exceptional surface smoothness and can fold extensively without showing haze. As a result, solution-coated grades have carved out lucrative niches in foldable displays and premium paint protection. This shift has directed capital investments towards multi-zone solvent ovens, predominantly in China and South Korea. Such advancements have positioned producers favorably in the polyurethane film market, especially within electronics supply chains that prioritize minimal defect rates.

Blown extrusion remains confined to agricultural films, where optical clarity isn't a concern. However, with high retrofit costs, shifts in capacity are deterred. While there's pressure to adhere to solvent-emission caps, potentially stunting unchecked solution-coating growth in Europe and North America, the advent of solvent-recovery technology, capable of recapturing a significant portion of DMF, offers a buffer against regulatory challenges. In this dynamic landscape, the polyurethane film market continues to favor processors who align end-use specifications with optimal line architecture for cost efficiency.

By End-Use Industry: Medical Supplies Accelerate Beyond Footwear

Footwear and apparel delivered 36.47% of 2025 volume, leveraging Asia-Pacific’s contract-manufacturing base. Still, medical supplies are forecast to outpace at a 7.08% CAGR through 2031 as polyurethane replaces phthalate-rich PVC in IV bags, drapes, and wound dressings to satisfy updated FDA biocompatibility guidance. Polyurethanes cut validation time by nine months, giving device giants a speed-to-market advantage worth millions in annual sales. Sports equipment and construction use cases grow steadily on abrasion resistance and vapor-permeability benefits, respectively, yet they trail medical in absolute incremental volume.

Margin squeeze in footwear from polyester synthetic leather pushes converters toward antimicrobial and recycled-content claims that secure premiums. Avery Dennison’s Q3 2025 pivot toward PVC-free graphics films underscores this repositioning strategy. Such moves maintain pricing discipline even as commodity TPU spreads narrow in the broader polyurethane film market.

Geography Analysis

Asia-Pacific commanded 49.52% volume in 2025 and will advance at a 6.93% CAGR to 2031 on the back of Chinese TPU expansion and South Korea’s foldable-display surge. In 2025, Covestro bolstered local supply chains by adding dispersion capacity in China and debottlenecking Thailand for footwear grades. Meanwhile, Vietnam and Indonesia, with their humid climates, continue to serve as prime contract-manufacturing hubs, favoring polyether films for waterproof footwear linings and boosting regional consumption.

In North America, the medical-supplies category outpaces other local applications. This growth is largely driven by hospital mandates that exclude phthalate-plasticized PVC. Additionally, the U.S. used-car fleet fuels a surge in paint-protection wraps, contributing to growth as these wraps extend vehicle life cycles. XPEL, capitalizing on this trend, derived a significant portion of its revenue from North American operations, underscoring the region's significance. Furthermore, Mexico's light-vehicle production, spurred by nearshoring, has amplified aftermarket demand.

Europe's polyurethane film market is adapting to REACH Annex XVII regulations, leading to a shift from PVC in medical and building membranes. A consumption bloc comprising Germany, France, the United Kingdom, and Italy accounts for a significant share of the market, with Germany's automotive aftermarket driving the demand for paint protection. Covestro's expansion in Krefeld-Uerdingen in March 2025 bolstered regional supply, and ADNOC's acquisition provides a buffer against European feedstock fluctuations. While Brazil and Argentina lead South American consumption, currency volatility hampers upgrades to specialty grades. Adoption of these grades in the Middle East and Africa remains limited, with the exception of Saudi Arabia and South Africa.

Competitive Landscape

The polyurethane (PU) film market is moderately consolidated. Technology rivalry centers on self-healing chemistries, bio-attributed feedstocks, and optical-grade thinness. Asian coaters investing in solvent-recovery infrastructure hold a cost-to-quality advantage for foldable-display supply, while European producers court sustainability-driven premiums. Long approval lead times under ISO 10993 and ISO 9001 favor incumbents with audit-ready documentation, keeping entry barriers high.

Polyurethane (PU) Film Industry Leaders

Covestro AG

The Lubrizol Corporation

3M

Avery Dennison Corporation

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Covestro AG broadened its portfolio, introducing specialty films designed for enhanced security glazing protection. These thermoplastic polyurethane (TPU) films from Covestro adeptly bond multiple layers of glass, polycarbonate, or acrylic, resulting in durable and transparent laminates.

- January 2025: ADNOC completed its purchase of Covestro AG, merging upstream isocyanate production with downstream polyurethane-film processing. This move establishes a crude-to-polymer vertical integration, shielding the newly formed entity from fluctuations in feedstock prices.

Global Polyurethane (PU) Film Market Report Scope

Polyurethane film is a flexible film with high elongation and properties and characteristics that are superior to most polyolefin films. TPU film also exhibits excellent dynamic flex performance, abrasion resistance, and tear strength.

The polyurethane film market is segmented by chemical class, processing method, end-user industry, and geography. By chemical class, the market is segmented into polyester, polyether, and polycaprolactone. By processing method, the market is segmented into blown film extrusion, cast film extrusion, and solution coating. By end-use industry, the market is segmented into footwear and apparel, medical supplies, sports equipment, building and construction, and other end-user industries. The report also covers the market size and forecasts for the polyurethane films market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Polyester |

| Polyether |

| Polycaprolactone |

| Blown Film Extrusion |

| Cast Film Extrusion |

| Solution Coating |

| Footwear and Apparel |

| Medical Supplies |

| Sports Equipment |

| Building and Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Chemical Class | Polyester | |

| Polyether | ||

| Polycaprolactone | ||

| By Processing Method | Blown Film Extrusion | |

| Cast Film Extrusion | ||

| Solution Coating | ||

| By End-use Industry | Footwear and Apparel | |

| Medical Supplies | ||

| Sports Equipment | ||

| Building and Construction | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is driving the polyurethane film market toward medical applications?

Hospitals in North America and Europe are phasing out phthalate-plasticized PVC, and polyether films meet ISO 10993 biocompatibility tests without extra extractables work, supporting a 7.08% segment CAGR.

Which processing method is gaining the fastest in the polyurethane film market?

Solution coating is growing at 6.94% annually because it can deliver sub-25 µm gauges with optical-grade clarity needed for foldable displays and premium paint-protection wraps.

How large is the Asia-Pacific share in the polyurethane film market?

Asia-Pacific held 49.52% of global volume in 2025 and is set to keep growing at a 6.93% CAGR through 2031.

What competitive strategies dominate among top polyurethane film vendors?

Vertical integration into isocyanates and technology differentiation in self-healing and optical-grade films help majors like Covestro and Lubrizol buffer feedstock swings and win high-margin orders.

What is the value of the polyurethane film market?

The polyurethane film market size is at 282.71 kilotons in 2026 and is expected to reach 392.46 kilotons, registering a CAGR of 6.78%.

Page last updated on: