Spray Adhesive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spray Adhesive Market Analysis by Mordor Intelligence

The spray adhesive market size was valued at USD 3.30 billion in 2025 and estimated to grow from USD 3.46 billion in 2026 to reach USD 4.37 billion by 2031, at a CAGR of 4.81% during the forecast period (2026-2031). Demand holds firm despite tightening VOC rules because producers continue to refine water-based and hot-melt chemistries that match the bonding strength of legacy solvent products. Growth concentrates in Asia-Pacific, where large-scale infrastructure programs, expanding furniture export hubs, and a deep automotive supply chain all require fast-tack, high-volume bonding solutions. Momentum also comes from global e-commerce logistics, which pushes fulfillment centers to specify aerosol and hot-melt variants that shorten pack-out time. Competitive pressure stays moderate, yet price-sensitive buyers have new choices from regional suppliers that replicate premium chemistries at lower cost while multinational leaders differentiate through sustainable performance upgrades. Structural drivers such as vehicle lightweighting, prefab construction, and hygienic food packaging keep end-use diversity wide, shielding the spray adhesive market from volatility in any single sector.

Key Report Takeaways

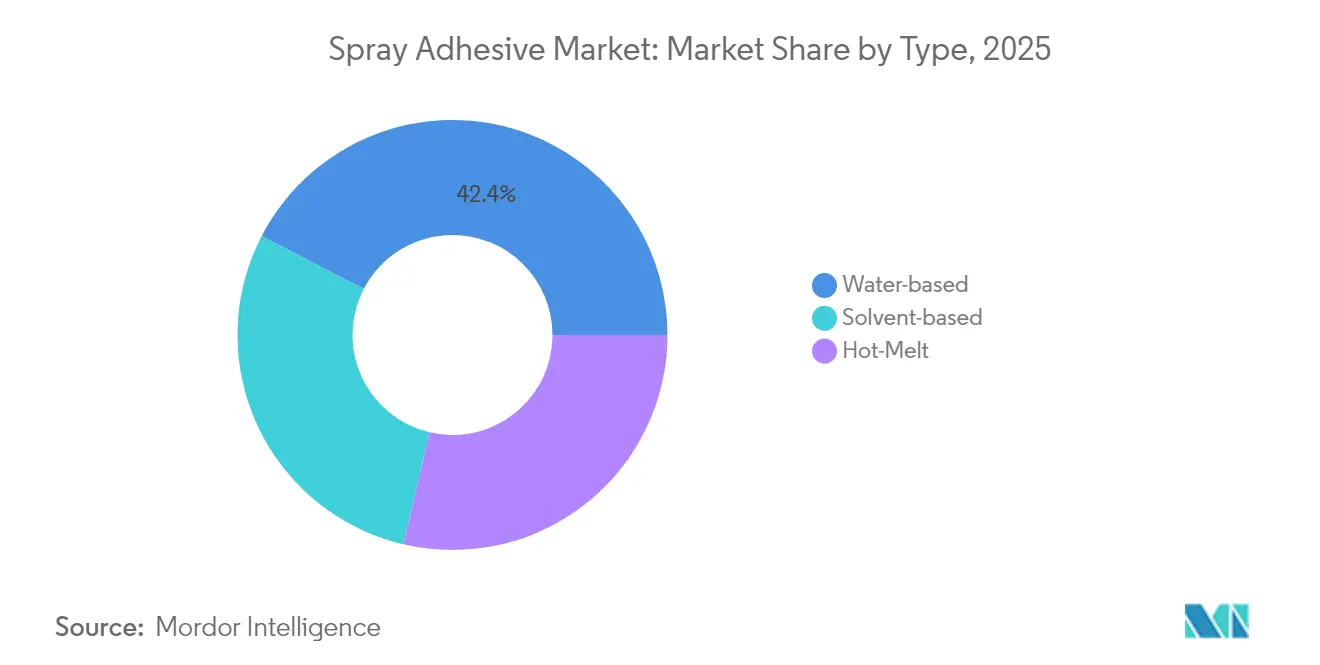

- By type, water-based products led with 42.38% of 2025 spray adhesive market share, while hot-melt grades are projected to expand at a 4.95% CAGR through 2031.

- By resin type, synthetic rubber held 36.35% revenue share in 2025; polyurethane is set to grow fastest at 5.61% CAGR.

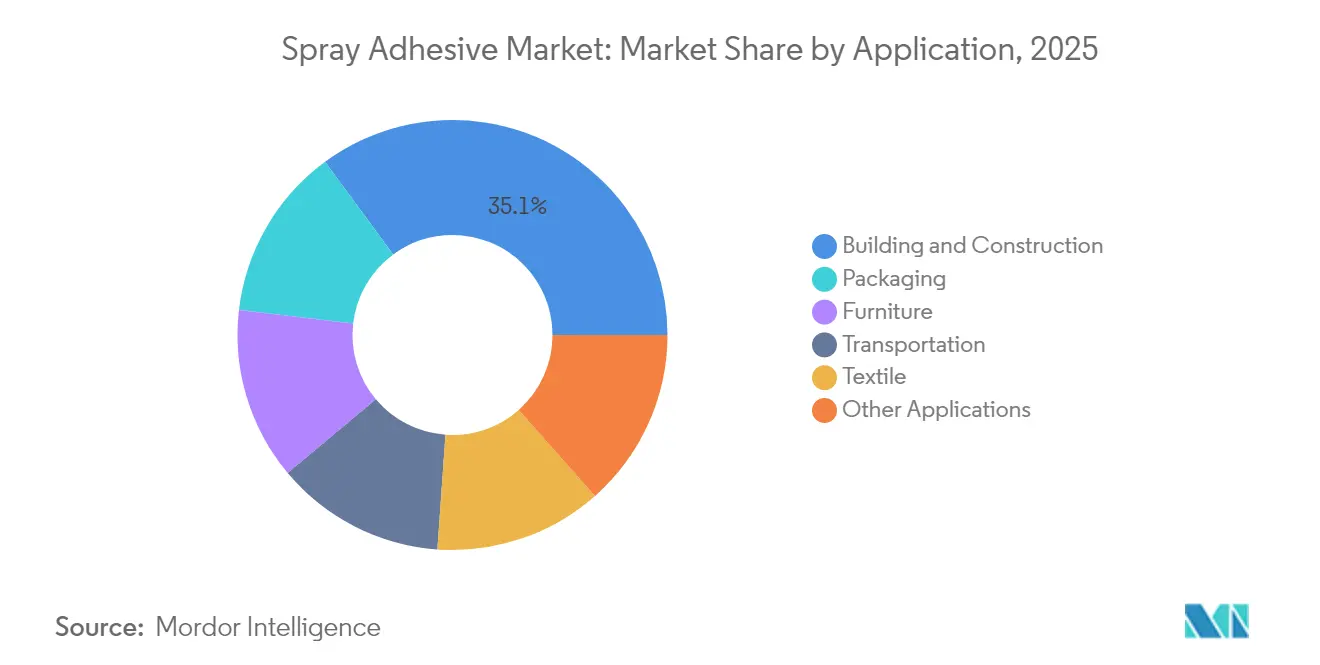

- By application, building and construction captured 35.10% of spray adhesive market size in 2025; furniture is forecast to advance at a 5.06% CAGR to 2031.

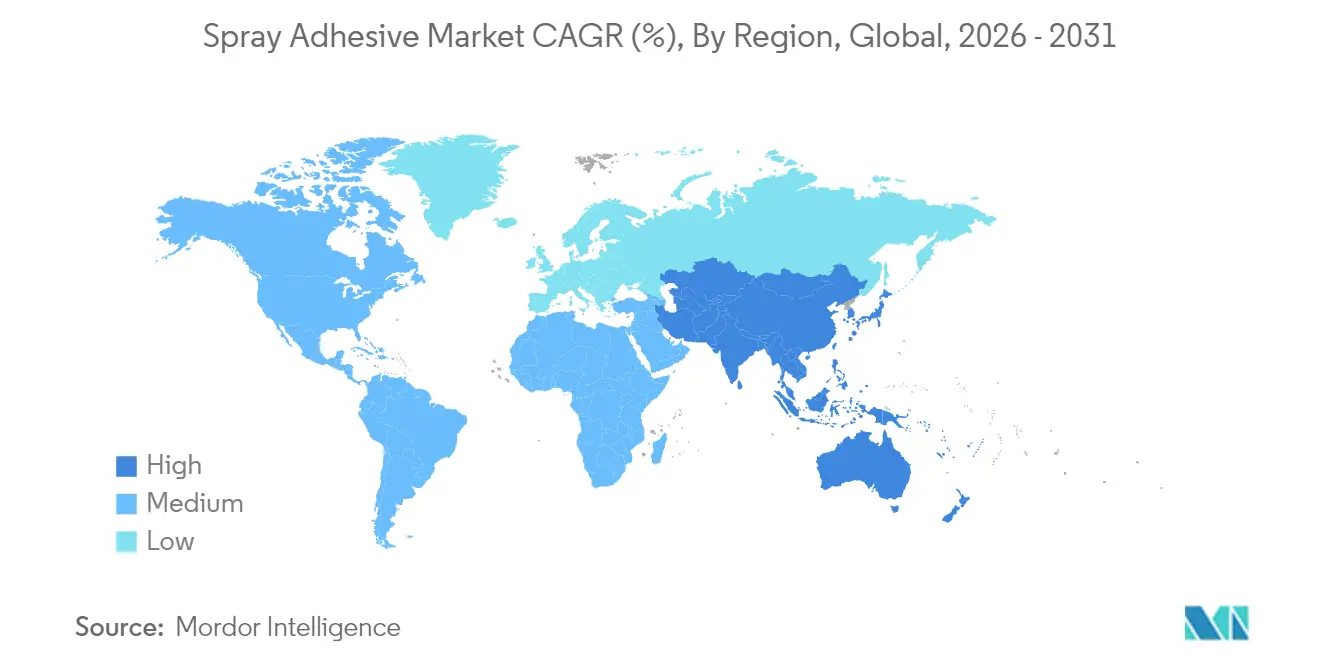

- By region, Asia-Pacific commanded 46.30% of 2025 revenue and is expected to post a 5.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spray Adhesive Market Trends and Insights

Driver Impact Analysis*

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of construction in emerging economies | +1.20% | Asia-Pacific, Middle East and Africa | Medium term (2–4 years) |

| Transition to water-based, low-VOC formulations | +0.90% | North America, Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Increasing utilization in automotive | +0.70% | Europe, North America, China | Medium term (2–4 years) |

| Demand for hygienic food packaging | +0.60% | North America, Europe | Medium term (2–4 years) |

| Expansion of e-commerce fulfillment centers | +0.50% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Construction in Emerging Economies

Surging public and private infrastructure investment across China, India, Indonesia, and the Gulf states is driving relentless volume growth for construction chemicals, including spray adhesives. Prefabricated wall panels, acoustic boards, and insulation sheathing all rely on high-performance bonding to withstand temperature swings and seismic loading. Several municipal housing programs specify low-VOC adhesives to meet green-building codes, nudging contractors toward water-based spray systems. Modular builders favor portable canister rigs that reduce overspray and labor time, increasing throughput on large projects. As urbanization accelerates, local firms adopt hot-melt spray lines that cure instantly, allowing rapid assembly of kitchen cabinets and interior fixtures inside high-rise developments. These combined forces keep the spray adhesive market deeply tied to building activity, particularly in Asia-Pacific’s fast-growing megacities.

Transition to Water-Based, Low-VOC Formulations Adhesives

Regulators on three continents have enacted lower emission ceilings, prompting adhesive formulators to launch waterborne systems with comparable tack and heat resistance to solvent grades. The Texas Commission on Environmental Quality amended rules that will eliminate 3.12 tons per day of VOCs around Houston, while California’s Department of Toxic Substances Control placed spray adhesives on its 2024-2026 priority product work plan[1]Texas Commission on Environmental Quality, “Rule Project No. 2024-024-115-AI,” tceq.texas.gov. Dow’s PRIMAL CA 750 and 3M’s Fastbond 1049 demonstrate that water-based polymers can meet industrial throughput targets without costly ventilation upgrades. Large buyers, especially furniture exporters shipping into the EU, now embed low-VOC requirements in purchase contracts, accelerating penetration of waterborne chemistries. As curing ovens consume less energy with these formulations, users realize direct savings on utility expenses and scope-2 emissions.

Increasing Utilization from the Automotive Industry

Automakers depend on spray adhesives to replace rivets and welds when joining lightweight composites, aluminum, and bio-based interior trims. H.B. Fuller documents that structural bonding can remove up to 10 kg of metal fasteners per vehicle, contributing to fuel-economy and range gains[2]H.B. Fuller, “Choosing the Right Adhesives and Sealants for Automotive Applications,” hbfuller.com. Electric-vehicle battery packs employ flame-retardant spray adhesives that form thermal barriers while adding minimal mass. Henkel’s CoolX line bonds roof-liners at lower oven temperatures, reducing assembly-line energy by as much as 20%. Automotive seating suppliers also specify fast-tack water-based sprays to cut cycle time in foaming operations. With global EV output expected to keep climbing, recurring demand from battery housings, wire harness tapes, and acoustic insulation bolsters long-term volumes in the spray adhesive market.

Increasing Demand for Hygienic Food Packaging

Food brands shift to mono-material and recyclable films that still need robust seal integrity for shelf-life protection. Water-based spray adhesives with FDA and EU food-contact clearances now bond paper-based trays, pouch laminates, and fiber lids, eliminating solvent residuals that can migrate. Dow, Saint-Gobain, and specialty converters collaborate on adhesives that permit in-plant recycling of edge-trim waste. Bio-based polymer dispersions appeal to premium organic brands seeking carbon-neutral certifications. Equipment retrofits remain limited because many spray lines only require nozzle changes when upgrading to water-borne chemistry, speeding adoption. Rising regulatory scrutiny over per- and polyfluoroalkyl substances (PFAS) in food wraps heightens the value proposition of new spray adhesive formulations that exclude fluorinated additives.

Restraint Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over VOC emissions | –0.8% | North America, Europe | Short term (≤ 2 years) |

| High production costs of advanced formulations | –0.6% | Global, emphasis on emerging markets | Medium term (2–4 years) |

| Competition from alternative bonding methods | –0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns Due to VOC Emissions

Air-quality agencies have tightened product-category caps, placing immediate compliance burdens on brands that still rely on strong-solvent carriers. The California Air Resources Board lowered limits on web-spray and special-purpose formulations. New Jersey’s draft rule aims to cut allowable VOCs in construction adhesives by more than half. Every new limit triggers relabeling, re-qualification, and sometimes forklift upgrades for explosive-atmosphere zones. Global producers must juggle multiple jurisdictional thresholds, fragmenting volume runs and trimming economies of scale. Firms unable to finance rapid reformulation risk losing shelf space, temporarily suppressing growth in the spray adhesive market.

Competition from Alternative Products

Mechanically applied pressure-sensitive films and advanced ultrasonic welding systems now vie for the same roles as spray adhesives in furniture edge-banding and automotive upholstery. These substitutes offer solvent-free credentials but often require costly capital equipment. As more manufacturers weigh total cost of ownership versus operational flexibility, competition intensifies. Nevertheless, spray application retains an edge in versatility and retro-fit simplicity, preserving its relevance but capping runaway market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Water-Based Leads the Environmental Transition

Water-based grades held the largest 42.38% portion of 2025 revenue, confirming industry commitment to low-emission chemistries. The segment benefits from regulatory support and from upgrades in polymer design that give water dispersions heat resistance above 120 °C, widening their application window. Asia-Pacific converters adopted canister spray systems that minimize cleaning downtime, advancing penetration across plywood lamination lines. In parallel, the hot-melt category is charting the quickest 4.95% CAGR, driven by automated furniture lines that value instant handling strength and zero drying ovens. Solvent products still occupy niche spaces such as aerospace composite repair, but their spray adhesive market size is set to shrink as environmental levies rise.

A second boost to water-based adoption comes from portable equipment developments that extend pot life and reduce overspray. Worthington Enterprises collaborated with 3M to deliver lightweight pressurized canisters that maintain uniform spray patterns for the full charge, lifting in-plant transfer efficiency to 80%. These improvements help the category defend its spray adhesive market share against entrenched solvent users, positioning water-based lines for sustained leadership through 2030.

By Resin Type: Synthetic Rubber Maintains Dominance

Synthetic rubber chemistries secured 36.35% of 2025 revenue and remain popular for their balanced tack, flexibility, and cost control. Their resilience across –20 °C to 80 °C operating shelves is critical for HVAC insulation wraps and commercial roofing. Developers continue to blend styrene-block copolymers with bio-based plasticizers, trimming carbon content without sacrificing peel strength. During 2026-2031, polyurethane grades will grow the fastest at 5.61% CAGR, favored in demanding automation, aerospace interiors, and panel laminations that need high green strength. Huntsman posted USD 3.9 billion polyurethane sales in 2024, reflecting continued appetite for these chemistries.

Epoxy variants occupy a smaller yet vital niche bonding metals in rail rolling stock and wind-turbine root joints, where chemical resistance overrides cure speed. Vinyl acetate-ethylene is rallying in baby-furniture and toy assembly because VAE emulsions generate negligible odor. Hybrid systems that marry silicone or acrylic blocks into polyurethane backbones are emerging, allowing formulators to tailor heat resistance while keeping atomization behavior suitable for spray guns. This diversified resin toolkit fuels innovation, sustaining healthy competition within the spray adhesive market.

By Application: Building and Construction Drives Volume Growth

Building and construction absorbed 35.10% of global shipments in 2025, validating spray technology’s role in modern site logistics. Prefab insulation boards, drywall, and composite siding arrive on-site bonded with factory-sprayed adhesives that cut install time. New green-building codes encourage low-VOC formulas, expanding water-based uptake in facade elements. Spray adhesive market size for furniture is advancing at a 5.06% CAGR as mass-customization software prompts short production runs that rely on quick-change adhesive spray stations. Packaging lines demand clean nozzles and fast set-time, attributes available from recent hot-melt aerosol products.

Transportation keeps absorbing advanced chemistries that bond acoustic mats, headliners, and battery cell spacers. Aerospace seat makers specify fire-retardant water-based sprays that meet FAR 25.853 vertical burn tests, highlighting the sector’s trust in modern formulations. Textile mills employ repositionable sprays to stabilize fabrics during cutting, trimming waste by 15%. Electronics and medical-device makers trial low-fogging, antimony-free systems for sensitive assemblies, representing future niches that could yield premium margins inside the spray adhesive market.

Geography Analysis

Asia-Pacific dominates with 46.30% revenue in 2025 and exhibits the fastest 5.64% CAGR outlook. China’s stimulus for affordable housing and India’s highway corridor projects ensure consistent demand for panel lamination sprays and tile adhesives. Local converters boost capacity to satisfy furniture export orders to the United States and the European Union, embedding low-VOC metrics that align with destination regulations. Japan’s electronics assemblers champion high-solids water-based sprays that reduce condensation risk on printed-circuit boards, spurring local compounders to scale formulations for subcontract partners. South Korea’s battery vertical integrates polyurethane spray lines to secure vibration isolation in high-density EV packs.

North America relies on strong residential remodeling, commercial reroofing, and resurgent domestic auto production. The Utah Department of Environmental Quality estimates a potential 4,000-ton annual VOC cuts once its consumer-product rule takes effect. This sets a compliance clock that already shifts purchase preference toward water-based canisters. Mexico’s export-oriented upholstery factories invest in automated hot-melt spray booths that boost throughput for theater seating and hospitality furniture destined for the United States. Canadian prefab home plants specify flame-retardant sprays that meet stringent provincial codes, underpinning regional diversification within the spray adhesive market.

Europe shows a mature yet innovation-driven profile. Germany’s premium auto OEMs require odor-free cockpit adhesives, steering suppliers to tailor monomer-free polyurethane dispersions. The United Kingdom’s retrofit insulation drive deploys low-emission spray foam panels secured with construction-grade water-based sprays. Sika’s CHF 11.8 billion global sales, with 7.3% growth in EMEA construction chemicals, evidence adhesive demand resilience. Italian and Polish furniture clusters automate spray lines to meet shorter lead-time expectations from online retailers. EU Green Deal policies accelerate solvent replacement, ensuring that Europe remains a reference market for sustainability in the spray adhesive market.

Competitive Landscape

The market is moderately fragmented. Top players invest heavily in polymer research and development, scaling pilot plants for bio-based feedstocks and employing digital process controls that curb energy use. Henkel reports water-based lines capable of cutting production CO₂ by 30% compared with legacy systems. Dow’s Edison-award-winning PRIMAL CA 750 exemplifies how performance parity and allergen-free claims win orders in upholstery and foam bonding. These firms also license spray-canister technology to applicator OEMs, safeguarding downstream compatibility.

Spray Adhesive Industry Leaders

3M

Henkel AG & Co. KGaA

H.B. Fuller Company

Arkema Group (Bostik)

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sika AG acquired Cromar Building Products Ltd. to strengthen its UK roofing channel, adding spray contact adhesives to its portfolio.

- October 2024: 3M introduced Fastbond Pressure Sensitive Adhesive 1049 with a water-based formula that lowers VOCs without sacrificing tack.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the spray adhesive market comprises all single and two-component adhesive formulations that are dispensed through pressurized canisters or automated guns to create a fine mist, forming an immediate tack bond on substrates such as wood, foam, fabric, metal, and engineered plastics. The study values only factory-produced sprayable liquids or melts sold in bulk drums, intermediate returnable cylinders, and aerosol cans.

Scope exclusion: We do not count manual contact cements or roll-on laminating glues that cannot be atomized.

Segmentation Overview

- By Type

- Solvent-based

- Water-based

- Hot-Melt

- By Resin Type

- Epoxy

- Polyurethane

- Synthetic Rubber

- Vinyl Acetate-Ethylene

- By Application

- Building and Construction

- Packaging

- Furniture

- Transportation

- Textile

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interview product managers at adhesive formulators, procurement leads in furniture, packaging, and vehicle interiors, plus distributors across Asia-Pacific, North America, and Europe. Their insights on canister refill cycles, average spread rates, and price pass-throughs let us stress-test desk findings and refine adoption curves.

Desk Research

Our analysts begin with public domain datasets that anchor volume flows, customs shipment codes for HS 3506, national production surveys from the U.S. Census and Eurostat, housing start series from the U.S. Federal Reserve, and automotive seating output from OICA. They enrich these with regulatory feeds such as U.S. EPA and ECHA VOC cap updates, technical bulletins from The Adhesive and Sealant Council, and peer-reviewed polymer journals that track water-based and hot-melt conversion rates. Subscription content from Dow Jones Factiva and D&B Hoovers supplies company revenue splits and capacity disclosures, giving early clues on regional shifts. This list is illustrative; many additional sources underpin model checkpoints.

Market-Sizing & Forecasting

A top-down production-plus-trade build starts with domestic output, adds net imports, then applies typical sprayable share factors by resin. Select bottom-up tests, supplier roll-ups and sampled average selling price multiplied by regional canister volumes, confirm totals before adjustments. Key drivers modeled include new floor space completions, corrugated board consumption, furniture production indices, vehicle seat builds, and tightening VOC thresholds that shift chemistry mix. A multivariate regression blended with ARIMA projections translates these indicators into 2025-2030 demand; scenario analysis captures slower construction or faster e-commerce cases. Data gaps on informal refill sales are bridged using calibrated penetration ratios validated by interviewees.

Data Validation & Update Cycle

Outputs pass three-layer review: automated variance checks, senior analyst sign-off, and a final refresh just before publication. Our market is revisited every twelve months, with mid-cycle revisions triggered by material regulatory or capacity events.

Why Mordor's Spray Adhesive Baseline Commands Reliability

Published figures often diverge because firms choose different chemistries, delivery formats, and refresh cadences. We anchor on clearly defined sprayable products, update yearly, and align exchange rates to the study year average.

Key gap drivers include: (a) some publishers fold wider aerosol sealants into their total, inflating value; (b) others apply global average selling prices that ignore Asia's lower ASPs; (c) legacy studies freeze supply bases at publication, whereas our analysts refresh plant lists every cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.30 B (2025) | Mordor Intelligence | |

| USD 7.25 B (2024) | Global Consultancy A | Bundles non-spray contact cements and counts equipment revenue |

| USD 3.76 B (2024) | Industry Research B | Uses partial regional coverage and historic ASP uplift without currency normalization |

| USD 4.77 B (2025) | Regional Consultancy C | Applies aggressive uptake multipliers for hot-melt grades and omits gray-market imports |

Taken together, the comparison shows that Mordor's disciplined scope, dual-check modeling, and timely refresh offer decision-makers a balanced, transparent baseline they can replicate and trust.

Key Questions Answered in the Report

What is the current size of the spray adhesive market?

The spray adhesive market stands at USD 3.46 billion in 2026 and is projected to reach USD 4.37 billion by 2031 on a 4.81% CAGR.

Which region leads global demand for spray adhesives?

Asia-Pacific holds 46.30% of 2025 revenue and is expected to grow at 5.64% CAGR through 2031, driven by construction, furniture, and automotive output.

Why are water-based spray adhesives gaining share?

Stricter VOC limits and advancements in polymer chemistry allow water-based grades to match solvent performance while helping manufacturers comply with air-quality regulations.

Which resin is growing fastest in spray applications?

Polyurethane formulations are forecast to expand at a 5.61% CAGR from 2026-2031 due to superior bonding strength in automotive and high-temperature settings.

How do e-commerce trends influence adhesive demand?

Fulfillment centers seek fast-tack aerosol and hot-melt sprays that cut carton-sealing time, lifting operational throughput and stimulating steady adhesive consumption.

Page last updated on: