Sports Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.33 Billion |

| Market Size (2031) | USD 19.15 Billion |

| Growth Rate (2026 - 2031) | 11.07% CAGR |

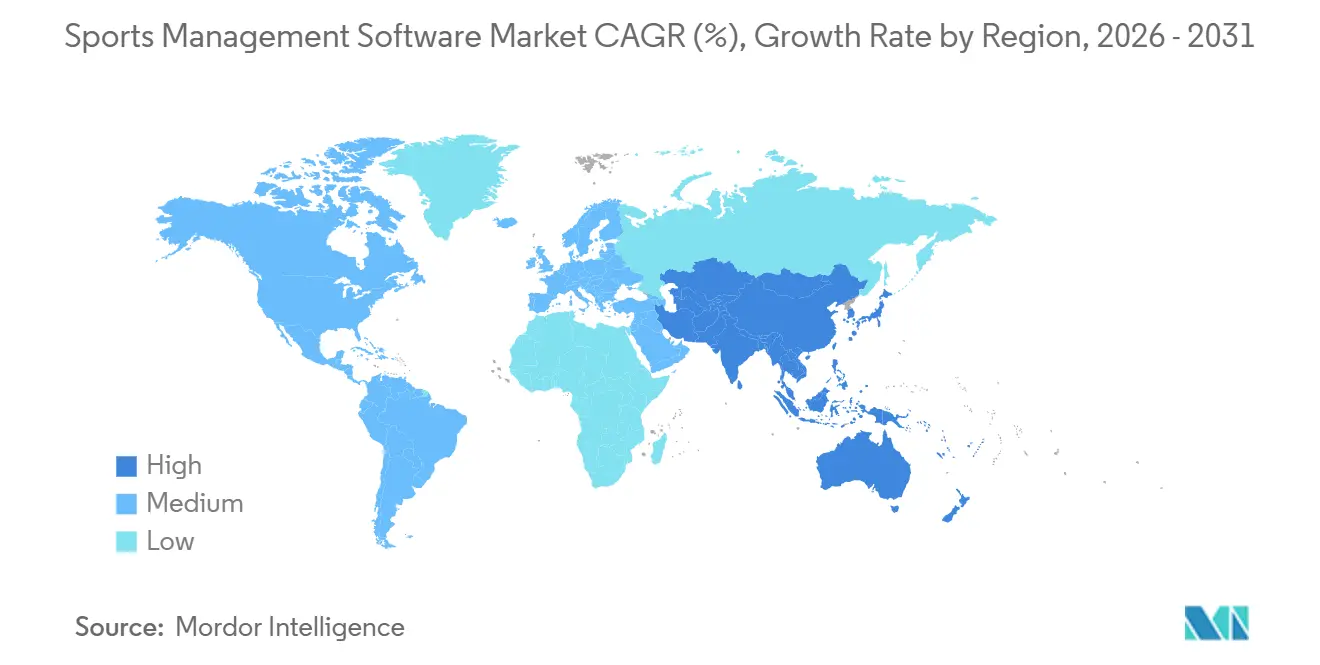

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Management Software Market Analysis by Mordor Intelligence

The sports management software market size was valued at USD 10.84 billion in 2025 and was estimated to grow from USD 11.33 billion in 2026 to reach USD 19.15 billion by 2031, at a CAGR of 11.07% during the forecast period (2026-2031). Three structural shifts are driving this expansion:,franchises and grassroots clubs are moving administrative workflows to cloud-native platforms, embedded-finance modules are eliminating third-party payment friction, and generative-AI scheduling engines are compressing labor costs by as much as 60%. Accelerating investment in women’s professional leagues, rising adoption of predictive analytics across mature North American users, and rapid growth among esports operators together extend the addressable base for the sports management software market. Vendors are responding with API-first architectures and SOC 2-audited cloud deployments, while investors funnel record capital into platform aggregators and performance analytics specialists. At the same time, tightening data-privacy regulations in Europe and Australia are forcing software providers to hard-wire consent management and local hosting into product roadmaps.

Key Report Takeaways

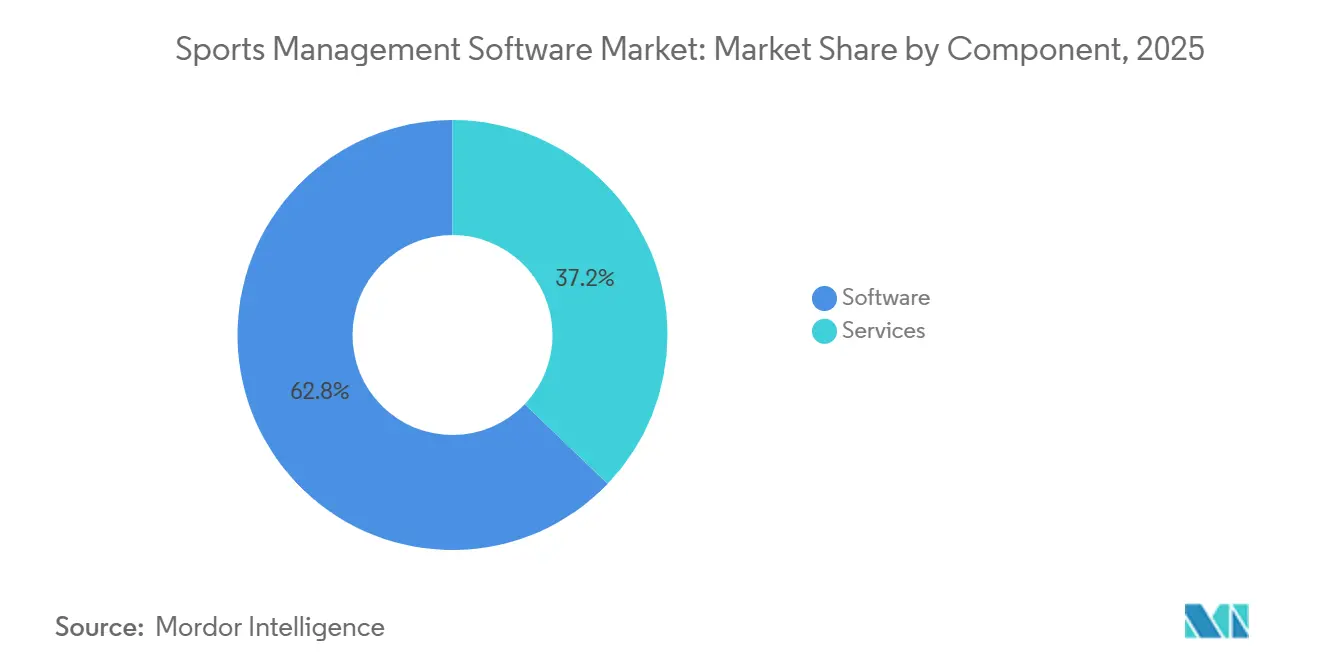

- By component, software licenses captured 62.83% of sports management software market share in 2025, while professional services are projected to expand at an 11.33% CAGR through 2031.

- By deployment model, cloud platforms accounted for 59.64% of the sports management software market size in 2025 and are forecast to advance at a 12.05% CAGR between 2026 and 2031.

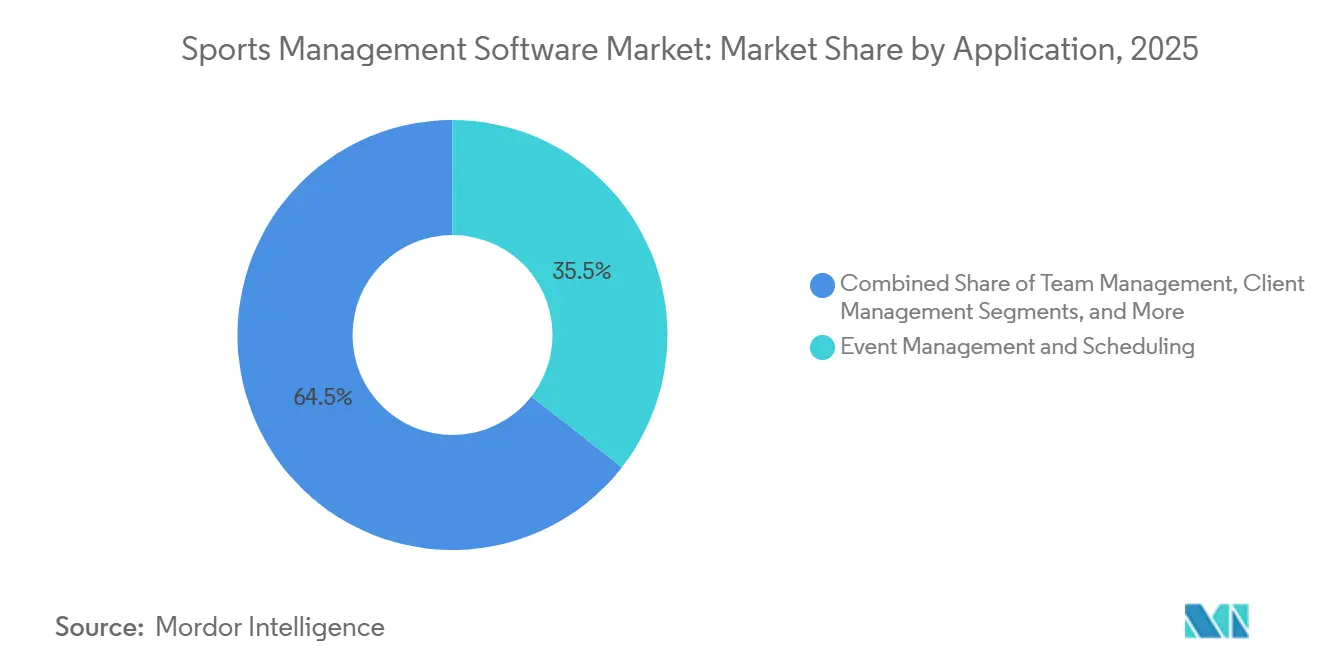

- By application, event management and scheduling led with 35.47% revenue share in 2025; client management is the fastest-growing use case at an 11.67% CAGR to 2031.

- By end-user, professional sports clubs and franchises held 40.91% share of the sports management software market size in 2025, whereas esports organizations are set to grow at an 11.96% CAGR through 2031.

- By geography, North America commanded 44.84% sports management software market share in 2025, while Asia Pacific is projected to post the highest regional CAGR of 12.42% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sports Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing investment in professional and grassroots sports facilities | +2.1% | Global, with concentration in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Rapid shift toward cloud-first SaaS subscription models | +2.8% | Global, led by North America and Europe, accelerating in Asia Pacific | Short term (≤ 2 years) |

| Integration of mobile payments and embedded finance modules | +1.6% | North America, Europe, and urban centers in Asia Pacific | Medium term (2-4 years) |

| AI-driven automated scheduling and communications | +2.3% | North America and Europe core, spill-over to Asia Pacific and Middle East | Short term (≤ 2 years) |

| Government-backed digital transformation grants for community clubs | +1.4% | Europe (UK, EU), Australia, Canada, selective Asia Pacific markets | Long term (≥ 4 years) |

| Growth of women's leagues demanding dedicated management platforms | +1.2% | North America, Europe, Australia, emerging in Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Cloud-First SaaS Subscription Models

Cloud penetration reached 70% of sports entities in 2025, cutting IT outlays by up to 40% compared with on-premise builds.[1]PwC, “Digital Transformation in Sports Organizations,” pwc.com Monthly SaaS fees as low as USD 50 widened access for community clubs that previously faced upfront license costs of USD 50,000. European organizations increasingly distribute workloads across AWS and Microsoft Azure to satisfy GDPR data-residency rules, while hybrid deployments persist in regions with unreliable bandwidth. The new economics favor platform consolidation: TeamSnap ONE folded 12 SKUs into a tiered plan in 2025, trimming customer-acquisition costs by 22%.[2]SchedulOpt, “Reinforcement-Learning Scheduler Cuts Manual Changes,” schedulopt.com ISO 27001 has become a universal checkpoint, anchoring buyer trust in a cloud-dominated sports management software market.

AI-Driven Automated Scheduling and Communications

Generative-AI engines now resolve fixture clashes, official availability, and weather disruptions with 30-60% less human input. A Texas youth league cut manual interventions by 52% after installing a reinforcement-learning scheduler in 2025. Multilingual GPT-powered messaging raised email open rates to 61% among non-English households, improving inclusivity for grassroots clubs. Energy-aware AI modules even time HVAC shutdowns to slash municipal utility bills by 19%. Regulatory scrutiny is rising, with California mandating transparency on algorithmic decisions that affect youth playing time.

Growing Investment in Professional and Grassroots Sports Facilities

Public and private capital inflows are tying facility grants to digital-readiness. Sport England disbursed GBP 230 million during 2025, with clauses requiring cloud adoption. Australia awarded AUD 200 million under similar terms, compelling clubs to implement software within 18 months. Saudi Arabia’s Vision 2030 invested USD 2 billion in venue upgrades that require AI-enabled booking systems. The NBA forced every G League affiliate onto unified management platforms by the 2025-2026 season, tightening vendor selection cycles. As a result, the sports management software market sees faster conversions and larger deal scopes.

Integration of Mobile Payments and Embedded-Finance Modules

Platforms now embed wallets that capture membership dues, merchandise sales, and rental fees in one transaction flow. Teamworks Wallet enabled direct NIL stipend payouts for collegiate athletes in 2025, erasing payroll intermediaries. Buy-now-pay-later options reduced youth-sports registration abandonment by 18% among families with annual incomes below USD 75,000. Clubs that switched to embedded finance posted a 27% boost in ancillary revenue, backed by one-click upsells. Compliance hurdles remain, PCI-DSS Level 1 audits can add USD 150,000 in annual costs, forcing smaller clubs to adopt white-label gateways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data-security and privacy compliance costs | -1.8% | Global, acute in Europe (GDPR), California (CCPA), and Australia (Privacy Act) | Short term (≤ 2 years) |

| Budget constraints at amateur and community clubs | -1.3% | Global, concentrated in emerging markets and rural areas of developed economies | Long term (≥ 4 years) |

| Vendor lock-in fears limiting long-term contracts | -0.9% | Europe and North America, moderate in Asia Pacific | Medium term (2-4 years) |

| Fragmented legacy systems hampering interoperability | -1.1% | North America and Europe, selective impact in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Data-Security and Privacy Compliance Costs

Remediation of a sports data breach averaged USD 4.88 million in 2024, a bill that mid-tier organizations struggle to meet. GDPR penalties reached EUR 251 million for Meta’s sports-related profiling violations, while Australia now levies up to AUD 50 million for late disclosures. Certification expenses, such as ISO 27001 and PCI DSS audits, drain budgets that could fund feature improvements, slowing platform upgrades in the sports management software market.

Budget Constraints at Amateur and Community Clubs

Median grassroots budgets range from AUD 50,000 to AUD 150,000, yet full-featured software can cost USD 6,000 annually, plus USD 25,000 in one-time services. In the United Kingdom, 40% of community clubs still rely on volunteers for manual administration.[3]Sport England, “Grassroots Funding and Digital Barriers,” sportengland.org Although Canada earmarked CAD 28 million of its 2025 grants for technology, complex applications and staggered payouts dampen uptake. Freemium tiers partially bridge the gap but convert only 18% of users to paid plans, slowing the penetration rate in the sports management software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge as Integration Complexity Mounts

Professional services grew at an 11.33% CAGR through 2031, outpacing software as clubs outsource data migration, API wiring, and staff training. Software still supplied 62.83% of the sports management software market revenue in 2025, anchored by recurring subscriptions for scheduling, payments, and member databases. Yet 60% of buyers report tangled legacy stacks, pushing deployment cycles past six months and elevating service invoices to as much as USD 75,000.

An API-first architecture now defines competitive advantage. Vendors fund headcount expansion in consulting and managed services units, with Teamworks adding 120 specialists after a USD 235 million raise. Self-service video modules and AI chatbots are shaving 31% off ticket volumes, while managed-service retainers priced at 25% of subscription fees attract resource-strapped community clubs. As these trends accelerate, the sports management software market sees professional services both reinforcing vendor lock-in and unlocking deeper platform adoption.

By Deployment Model: Cloud Dominance Accelerates Amid Hybrid Holdouts

Cloud platforms held 59.64% sports management software market share in 2025 and are forecast to climb at a 12.05% CAGR through 2031. Subscription economics eliminate six-figure up-front licensing costs, allowing small clubs to deploy enterprise-grade tools. European data-sovereignty rules nurture multi-cloud adoption, whereas South African rugby outfits still sync on-premise databases during low-connectivity hours.

Hybrid setups persist among franchises that store sensitive contract data locally but shift fan-facing workflows to the cloud. Edge nodes deployed by Genius Sports at Premier League stadiums trimmed latency from 120 milliseconds to 18 milliseconds in 2025. Despite the momentum, 45% of European prospects hesitate on multi-year deals because data portability under GDPR increases switching friction. Accordingly, the sports management software market rewards providers that publish clear exit APIs and pricing caps on data exports.

By Application: Client Management Ascends as Retention Trumps Acquisition

Event management retained 35.47% of application revenue in 2025, yet client management posted the fastest CAGR at 11.67%, signaling a pivot from one-off scheduling to lifetime-value optimization. Integrated CRM modules cut churn by 20% through automated win-back campaigns and milestone-based offers.

Personalization engines recommend programs based on behavior, raising cross-sell conversions by 27%. AI churn predictors that flag absentee members saved clubs an average of 23% in lost dues. With embedded wallets, platforms upsell coaching sessions at checkout, elevating average revenue per member and expanding the sports management software market share tied to CRM functions.

By End-User: Esports Organizations Redefine Growth Benchmarks

Professional franchises delivered 40.91% of spending in 2025, but esports organizations are on track for the highest CAGR at 11.96% through 2031. Global esports revenue is expected to touch USD 2.3 billion in 2025, bolstering demand for tournament-management software that standardizes player contracts and prize disbursements.

Collegiate programs seek compliance features to align with NCAA rules on practice time and recruiting. Community recreation departments lean on freemium scheduling but upgrade for payment processing once government grants land. Fitness chains integrate booking systems with wearables via Apple Watch, lifting engagement 42%. These trends diversify the sports management software market but also heighten the need for configurable workflows that serve audiences from municipal parks to cloud-gaming arenas.

Geography Analysis

North America led the sports management software market with a 44.84% share in 2025, driven by deep penetration across professional leagues and youth sports ecosystems. The region drew USD 52 billion in disclosed sports-tech deals during H1 2025, highlighted by Genius Sports’ USD 1.2 billion Legend purchase in 2026. State-level grant programs in California, Texas, and New York allocated USD 120 million to community digitalization, while Canada’s CAD 80 million Sport-for-All initiative earmarked 35% for software procurement. Maturity now forces vendors to layer predictive analytics and AI schedulers to differentiate beyond core functionality.

Asia Pacific is the fastest-growing region, with a 12.42% CAGR through 2031. China’s 500 million sports participants and India’s 25-30% annual growth in sports tech underpin explosive demand. Beijing has ordered all provincial bureaus to move onto cloud platforms by 2027, cementing domestic giants Alibaba Cloud and Tencent Sports as keystones. Indian Premier League teams each spend up to USD 15 million on integrated analytics, while Seoul’s esports venues stress-test real-time tournament software. Government grants in Australia inject AUD 200 million into community migration, further expanding the regional sports management software market.

Europe’s growth is shaped by GDPR compliance. Twenty-eight percent of clubs migrated to EU-hosted data centers in 2025, and Sport England linked GBP 230 million in grassroots funding to digital readiness. Bundesliga teams deploy AI fan-experience platforms that lifted per-capita spending 19%, showing revenue-side justification for ongoing investments. The Middle East leverages Vision 2030’s USD 2 billion facility program to mandate AI booking tools, while Africa remains nascent, concentrated in South Africa, Nigeria, and Kenya. South America sees Brazil driving adoption among football academies despite currency volatility, leaving ample headroom for future sports management software market penetration.

Competitive Landscape

The sports management software market remains moderately fragmented. The top five providers-TeamSnap, SportsEngine, Stack Sports, Active Network, and collectively held a prominent share in 2025. Platform aggregators pursue horizontal scale by rolling up adjacent modules, as seen in Teamworks’ Sportlogiq acquisition and Stack Sports’ PlayMetrics deal. Performance analytics specialists such as Hudl and Catapult Sports add AI vision and wearable tech to retain elite customers. Vertical newcomers like CourtReserve target racquet facilities with purpose-built reservation engines, exploiting incumbents’ one-size-fits-all approach.

Capital inflows reinforce consolidation. Teamworks’ USD 235 million Series E funded a 120-person services expansion, while ScorePlay raised USD 13 million to automate media-rights distribution. Edge computing patents from Genius Sports and biomechanics IP from Catapult broaden moats that hinge on data ownership.

Patent filings reveal strategic priorities. Catapult Sports secured 14 wearable-sensor patents in 2024-2025, covering real-time biomechanical analysis, while Genius Sports filed 8 patents related to low-latency sports-betting data feeds that integrate with league-management platforms, USPTO. ISO 27001 certification and SOC 2 Type II attestations have become table stakes, as data-security concerns drive 67% of enterprise buyers to mandate third-party audits during vendor evaluation ISO. As API openness and embedded finance mature, vendors that bridge interoperability without heavy custom coding stand to gain share in the sports management software market.

Sports Management Software Industry Leaders

Sports Engine Inc.

Jonas Club Software

Active Network LLC

Stack Sports Holdings

TeamSnap Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Genius Sports completed its USD 1.2 billion acquisition of Legend, adding ticketing and fan-engagement to its data management stack.

- January 2026: Teamworks bought Sportlogiq, integrating real-time hockey analytics into its communication suite.

- November 2025: eamSnap launched TeamSnap ONE, unifying 12 products into tiered plans that cut acquisition costs by 22%.

- November 2025: NBC Sports Next put SportsEngine up for sale with an estimated valuation up to USD 200 million, inviting private-equity bids.

Global Sports Management Software Market Report Scope

In sports management, software became a key differentiator to gaining a competitive advantage for the stakeholders in the sports industry. Hence, many sports associations, clubs, and their coaches are adopting the all-in-one integrated software solution, driving the global sports management software market growth.

The Sports Management Software Market Report is Segmented by Component (Software and Services), Deployment Model (On-Premise and Cloud), Application (Event Management and Scheduling, Team Management, Marketing Management, Client Management, League and Competition Management, Membership and Payment Processing), End-User (Professional Sports Clubs and Franchises, Colleges and Universities, Schools and Academies, Community Recreation Organizations, Gyms and Fitness Centers, and Esports Organizations), and Geography (North America, South America, Europe, Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premise |

| Cloud |

| Event Management and Scheduling |

| Team Management |

| Marketing Management |

| Client Management |

| League and Competition Management |

| Membership and Payment Processing |

| Professional Sports Clubs and Franchises |

| Colleges and Universities |

| Schools and Academies |

| Community Recreation Organizations |

| Gyms and Fitness Centers |

| Esports Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| By Application | Event Management and Scheduling | |

| Team Management | ||

| Marketing Management | ||

| Client Management | ||

| League and Competition Management | ||

| Membership and Payment Processing | ||

| By End-user | Professional Sports Clubs and Franchises | |

| Colleges and Universities | ||

| Schools and Academies | ||

| Community Recreation Organizations | ||

| Gyms and Fitness Centers | ||

| Esports Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the sports management software market by 2031?

The market is expected to reach USD 19.15 billion by 2031, expanding at an 11.07% CAGR from 2026-2031.

Which deployment model grows the fastest in sports management software?

Cloud platforms lead growth with a 12.05% CAGR, driven by lower upfront costs and automatic updates.

Why are esports organizations important to software vendors?

Esports teams are forecast to post the highest end-user CAGR at 11.96%, adopting club-style workflows for tournaments and prize payouts.

How large is the services opportunity within the market?

Professional services revenues are rising at 11.33% CAGR as clubs outsource data migration, API integration, and training.

Which region is expected to post the strongest growth through 2031?

Asia Pacific is projected to lead with a 12.42% CAGR, propelled by China’s vast participant base and India’s rapid tech adoption.

Page last updated on: