Specimen Collection Cards Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

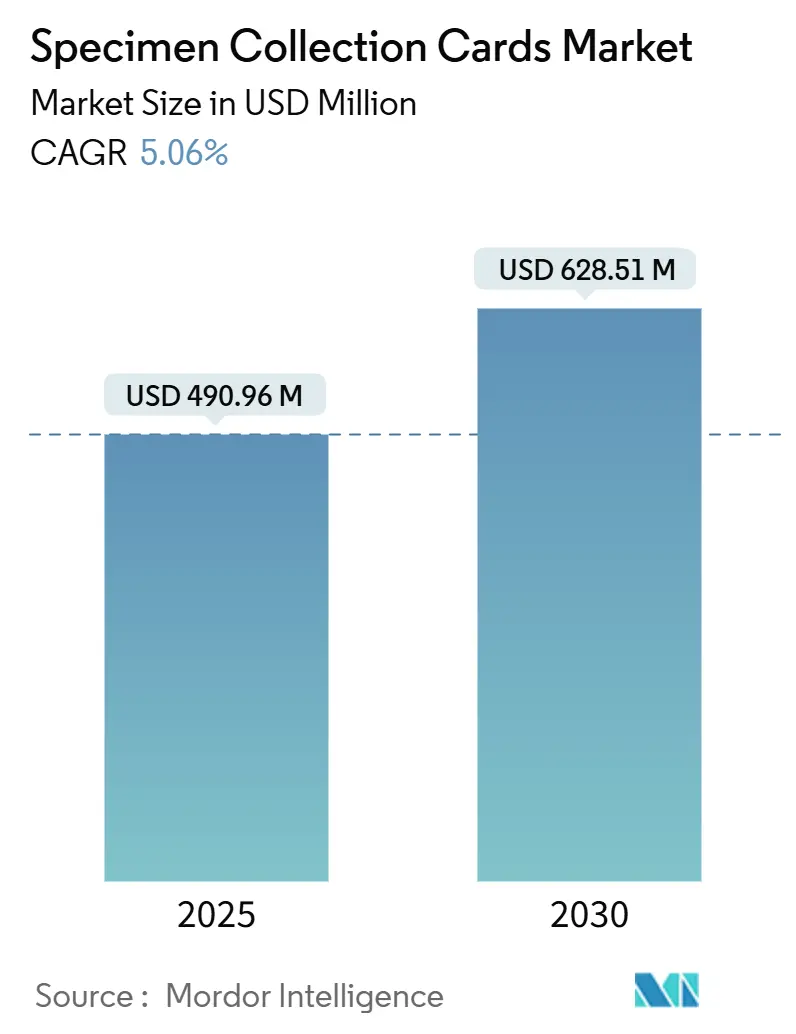

| Market Size (2025) | USD 490.96 Million |

| Market Size (2030) | USD 628.51 Million |

| Growth Rate (2025 - 2030) | 5.06% CAGR |

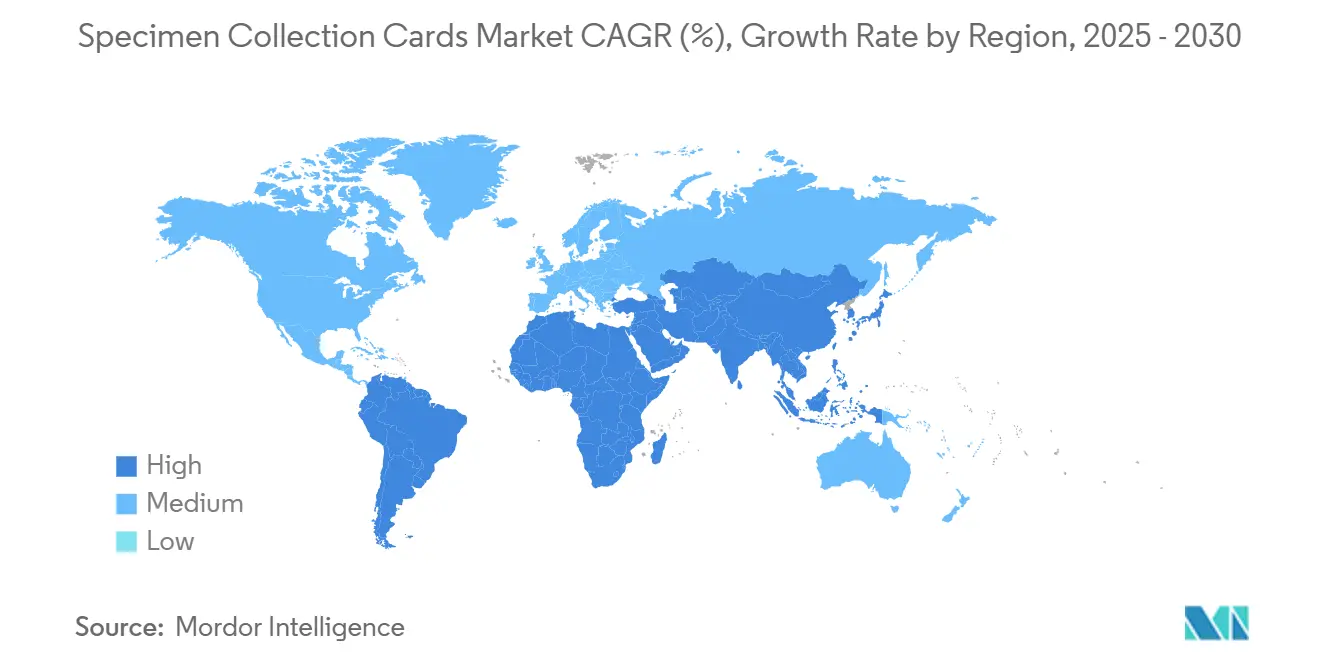

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specimen Collection Cards Market Analysis by Mordor Intelligence

The specimen collection cards market size was USD 490.96 million in 2025 and is projected to reach USD 628.51 million by 2030, growing at a 5.06% CAGR. Strong demand for remote biosampling, the momentum of decentralized clinical trials, and the rapid expansion of newborn screening programs are reinforcing steady growth. Pandemic-era reliance on dried blood spot (DBS) logistics proved the practical value of cards in cold-chain-constrained environments, spurring continued adoption across infectious-disease surveillance and at-home test kits. Volumetric microsampling innovations, while challenging legacy DBS methods, are also expanding the technical frontier, encouraging incumbents to upgrade filter substrates and microfluidic features. North America remains the anchor for regulatory clarity and large-scale newborn programs; however, Asia-Pacific’s hospital investments and public-health initiatives are converting latent demand into rapid installations. Competitive intensity is moderate, with global diagnostics conglomerates acquiring niche technology start-ups to protect positions and cross-sell broader assay portfolios.

Key Report Takeaways

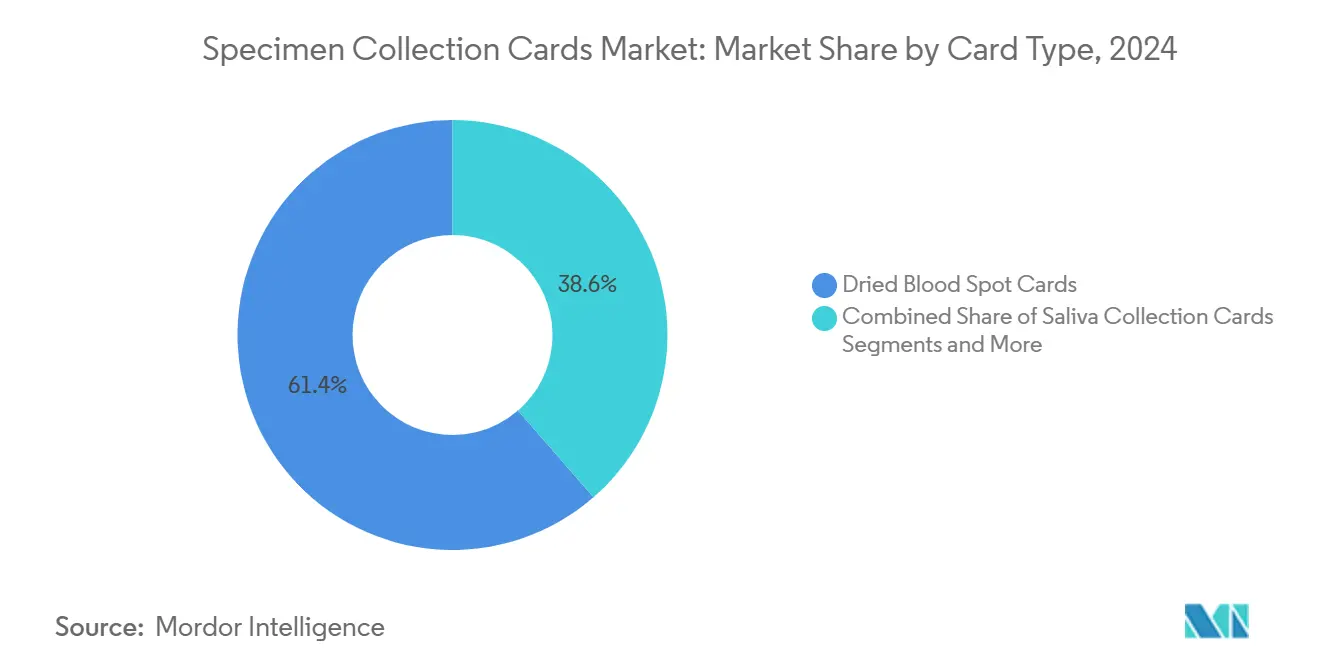

- By card type, dried blood spot cards led with a 61.38% specimen collection cards market share in 2024, while saliva collection cards are forecast to expand at a 9.42% CAGR through 2030.

- By sample type, blood accounted for 76.42% of the specimen collection cards market size in 2024, and saliva is projected to grow at an 8.89% CAGR to 2030.

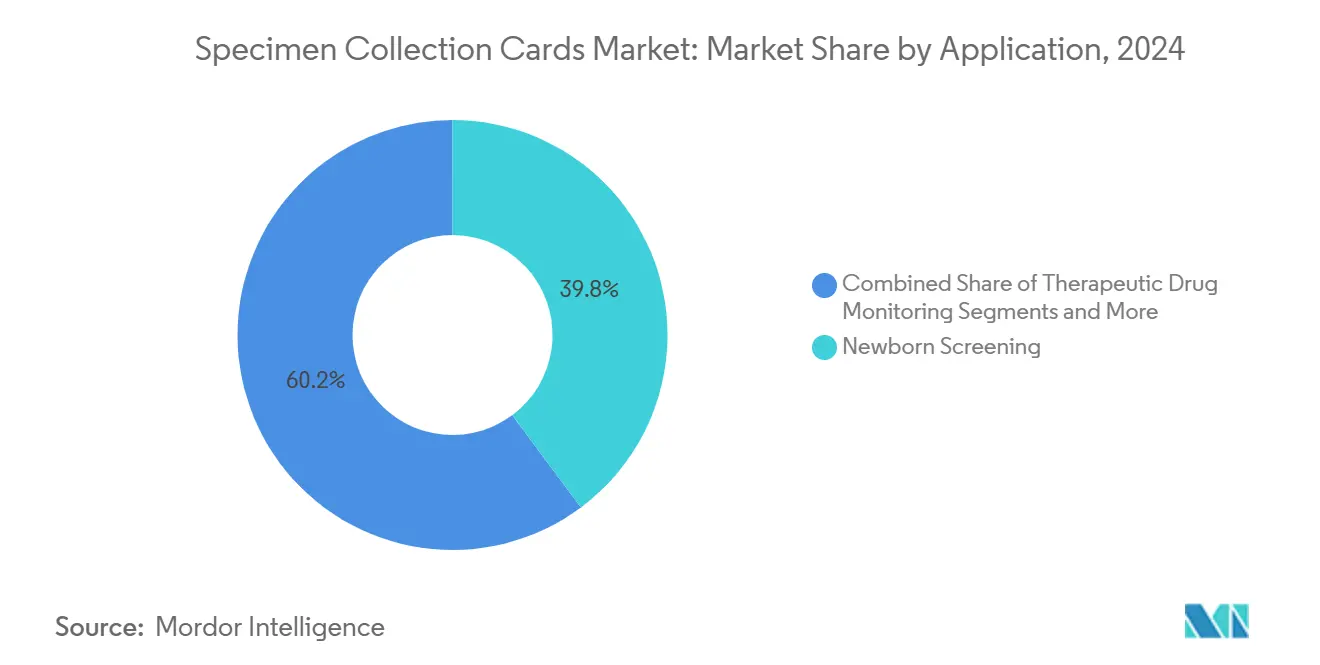

- By application, newborn screening held 39.81% of 2024 revenue; infectious-disease diagnostics is set to record an 8.12% CAGR during the forecast window.

- By end user, hospitals and clinics controlled 44.31% of 2024 spending, whereas home and tele-health testing services are poised to rise at 9.74% CAGR.

- By geography, North America commanded 36.43% revenue share in 2024, and Asia-Pacific is anticipated to deliver a 7.33% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Specimen Collection Cards Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Newborn Screening Programs | +1.2% | Global, with strongest growth in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Expansion Of Infectious-Disease Surveillance Using DBS Cards | +0.8% | Global, particularly in LMIC regions and post-pandemic recovery areas | Short term (≤ 2 years) |

| Growth In At-Home/Telehealth Sample-Collection Kits | +1.1% | North America & EU leading, expanding to APAC urban centers | Medium term (2-4 years) |

| Decentralized Clinical Trials Demanding Remote Biosampling | +0.9% | Global pharmaceutical hubs, with concentration in US, EU, and emerging Asian markets | Long term (≥ 4 years) |

| Integration Of Microfluidics Enabling Multi-Omics Analysis | +0.7% | Advanced healthcare markets in North America, Western Europe, and select APAC regions | Long term (≥ 4 years) |

| Cold-Chain Cost-Savings Driving Uptake In LMIC Laboratories | +0.5% | LMIC regions globally, particularly Sub-Saharan Africa and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Newborn Screening Programs

More governments are financing expanded newborn screening, positioning DBS cards as the primary interface between public-health policy and precision medicine. India is advancing cystic-fibrosis screening pilots that could uncover thousands of undiagnosed cases annually.[1]Rashi Arora, “India: The Last and Best Frontier for Cystic Fibrosis Newborn Screening with Perspectives on Special Challenges,” International Journal of Neonatal Screening, mdpi.com Thailand’s rural e-platform reached 98.6% coverage for 123,692 births, proving that web-based logistics can support high-volume card flows in resource-limited settings. Japan’s inclusion of lysosomal storage disorders confirmed 101 positives among 733,000 newborns, validating the clinical value of broader panels.[2]Shunsuke Kobayashi, “Japanese Experience of Newborn Screening for Lysosomal Storage Diseases and Adrenoleukodystrophy,” Orphanet Journal of Rare Diseases, bmcjournals.onlinelibrary.wiley.comDutch trials showed next-generation sequencing can process DBS DNA in five days, linking high-throughput genomics to existing card workflows. Collectively, these initiatives continue to lift baseline demand for specimen collection cards market volumes.

Expansion of Infectious-Disease Surveillance Using DBS Cards

School-based surveillance in Missouri used self-collected DBS to detect Mycoplasma pneumoniae, reinforcing decentralized outbreak monitoring.[3]Matthew Payne, “Notes from the Field: School-Based Surveillance of Mycoplasma pneumoniae Trends and Impact on School Attendance — Missouri, Fall 2024,” Morbidity and Mortality Weekly Report, cdc.govThe WHO program in Cambodia flagged 12.5% extensively drug-resistant gonorrhea, illustrating how standardized card sampling uncovers resistance trends. DBS assays now quantitate neutralizing antibodies to SARS-CoV-2, providing population immunity snapshots without venipuncture. Dried matrix spots are also tracking neglected tropical diseases where refrigeration is scarce.[4]Dora Buonfrate, “The Use of Dried Matrix Spots as an Alternative Sampling Technique for Monitoring Neglected Tropical Diseases,” Frontiers in Microbiology, pmc.ncbi.nlm.nih.gov Together, these developments sustain a durable volume stream for the specimen collection cards market.

Growth in At-Home/Telehealth Sample-Collection Kits

Consumer acceptance of mailbox-ready test kits is normalizing fingertip and saliva collection outside clinics. Cardinal Health ships more than 50 million specimen kits yearly, underpinning retail diagnostics expansion. BD’s MiniDraw earned FDA clearance by matching venous-draw accuracy in pharmacy settings. Labcorp’s Lab-in-an-Envelope service integrates finger-stick cards with national courier returns, widening chronic-disease monitoring reach. FDA emergency authorization of at-home monkeypox PCR sampling showed regulators now trust self-collection when validated protocols exist. This customer-centric shift supports persistent double-digit growth for the specimen collection cards market in direct-to-consumer channels.

Decentralized Clinical Trials Demanding Remote Biosampling

Industry adoption of hybrid and fully virtual trial designs hinges on reliable dry-card logistics. IQVIA’s mobile teams now collect specimens in participant homes across multiple countries, cutting site-visit burdens. Tasso+ self-collection demonstrated strong venous correlation for safety labs, removing centrifugation hurdles. European guidance within the Health Data Space is aligning privacy compliance with remote sampling, improving sponsor confidence. As under 5% of U.S. cancer patients enrolled in trials historically, remote sampling is widening eligibility and boosting recruitment diversity. These pressures elevate recurring demand across the specimen collection cards market.

Restraints Impact Analysis of Specimen Collection Cards Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Analytical-Sensitivity Limitations Of Low-Volume Spots | -0.8% | Global, particularly affecting advanced diagnostics in developed markets | Short term (≤ 2 years) |

| Regulatory Uncertainty For Self-Collection Devices | -0.6% | North America & EU regulatory jurisdictions, with spillover to global markets | Medium term (2-4 years) |

| Supply Constraints For High-Grade Cotton-Linter Filter Paper | -0.4% | Global manufacturing centers, concentrated impact in Asia-Pacific production hubs | Short term (≤ 2 years) |

| Competition From Volumetric Micro-Sampling Devices | -1.1% | Advanced healthcare markets with high R&D spending, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Analytical-Sensitivity Limitations of Low-Volume Spots

Detection of low-abundance biomarkers remains challenging when cards capture only a few microliters. Cardiometabolic research found lipid panels underperform relative to venous draws, implicating volume and matrix effects. Multicountry quality audits reported that 46% of patient DBS cards failed acceptance criteria, often due to incorrect fill patterns and poor drying environments. Pediatric drug monitoring struggles with sub-microliter draws, forcing rigorous validation to avoid dosing errors. Interlaboratory proficiency studies revealed wide CV ranges versus whole blood, underscoring the need for harmonized protocols. These limitations temper unrealistically high expectations within the specimen collection cards market.

Regulatory Uncertainty for Self-Collection Devices

Although FDA has cleared several self-collection platforms, policy remains fluid. Proposed LDT reforms include backup enforcement via specimen-collection-kit oversight, injecting ambiguity into future submissions. EU regulators likewise adjust IVDR transition pathways, leaving innovators to pre-emptively design to evolving standards. Start-ups must fund additional studies to satisfy home-use labeling, elevating time-to-market costs. Global distributors watch U.S. and EU precedents, delaying large procurement deals until clarity emerges. This stop-start environment slows some revenue capture for the specimen collection cards market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Specimen Collection Cards Market Segment Analysis

By Card Type:

DBS Dominance Faces Saliva InnovationDried blood spot formats generated the largest revenue, holding 61.38% of the specimen collection cards market size in 2024 as decades of validation across newborn screening and therapeutic monitoring cemented clinical confidence. Still, saliva cards are rising swiftly at a 9.42% CAGR as patient-friendly self-collection aligns with telehealth models. Protein saver and FTA nucleic-acid cards address research niches that demand DNA stabilization for genomics assays, while dried plasma spot designs appeal to virology labs needing hematocrit-free analytes. Ongoing enhancements, such as patterned plasma separation layers and lipid-specific coatings, reveal how incumbents protect territory against volumetric absorptive devices. The segment’s innovation cadence signals that traditional paper-based DBS will coexist with newer polymers rather than disappear, preserving a robust revenue core for the specimen collection cards market.

The competitive axis tilts toward value-added features. Patterned dried plasma spot cards demonstrated higher HIV viral-load precision compared with standard separation kits. Ahlstrom’s Lipid Saver extended into fatty-acid analytics, giving nutrition researchers a turnkey option. Manufacturers are blending cellulose with synthetic fibers to withstand high-throughput automation punches, catering to laboratories chasing labor efficiency. Such product proliferation refreshes reorder cycles and keeps pricing resilient, underpinning long-term value in the specimen collection cards market.

By Sample Type:

Blood Supremacy Challenged by Saliva GrowthBlood accounted for 76.42% of 2024 sales, reflecting its unmatched biomarker breadth and entrenched clinical protocols. Saliva’s 8.89% CAGR underscores momentum for painless collection in infectious-disease and genetic-risk screening. Urine remains a specialist option in metabolic and environmental testing where analytes are excreted rather than circulating, while cerebrospinal or synovial fluid cards serve ultra-niche research domains. COVID-19 accelerated saliva’s acceptance; validated containers from Sarstedt simplified logistics for molecular assays. Nutrition-science studies now quantify dietary lipid signatures from DBS, broadening blood applications into public-health nutrition. As research uncovers extracellular vesicles within dried blood, high-value oncology and prenatal diagnostics may further elevate blood’s share, though saliva will keep chipping away volume in consumer kits, sustaining healthy internal competition within the specimen collection cards market.

Segment participants differentiate by sample-type versatility. Card platforms offering modular matrices or dual-sample zones win multi-omics grants and CRO contracts. Pharma sponsors favor sample-agnostic designs to future-proof trial biobanks. Vendors able to engineer cross-compatible formats will capture incremental share as standard-of-care evolves, creating overlapping revenue layers across the specimen collection cards market.

By Application:

Newborn Screening Leads, Infectious Disease AcceleratesNewborn screening delivered 39.81% of 2024 value, propelled by universal mandates in developed countries and expanding pilots across Asia and Latin America. Infectious-disease diagnostics, with an 8.12% CAGR, is catching up through antibiotic-resistance surveillance and pandemic-preparedness budgets. Forensic and law-enforcement labs rely on DNA-stable cards to maintain chain-of-custody integrity. Drug discovery and decentralized clinical-trial protocols leverage remote cards to streamline patient engagement. Therapeutic drug monitoring gains from home dosing adherence programs, lowering clinic visits for chronic conditions.

Genomic newborn pilots like BeginNGS show rapid diagnostic turnarounds and healthcare savings, supporting policy adoption. Machine-learning-enhanced metabolic screening improved sensitivity to 93.42%, minimizing recall anxiety. FDA classification of multiplex nucleic-acid tests now references prerequisite card validation, embedding regulatory pull-through. These converging trends lift recurring reagent and card consumption, locking in multiyear upside for the specimen collection cards market.

By End User:

Hospitals Lead, Home Testing SurgesHospitals and clinics absorbed 44.31% of 2024 procurement, reflecting entrenched laboratory networks and reimbursement familiarity. Home and tele-health testing services lead growth at 9.74% CAGR as insurers reimburse chronic-disease panels mailed from patient homes. Diagnostic reference labs serve as processing backbones, while academic centers pioneer next-gen analytics that subsequently trickle into commercial kits.

Pharmaceutical and biotech sponsors employ cards in adaptive trials, shrinking geographic enrollment barriers. Forensic institutions standardize body-swab DNA cards in death investigations, reinforcing demand for robust chain-of-custody materials. NIST’s roadmap highlights AI-assisted evidence workflows, signaling future card requirements for digital traceability. Collectively, these actors assure steady unit turnover throughout the specimen collection cards market.

Geography Analysis

North America Specimen Collection Cards Market

North America delivered a 36.43% revenue share in 2024 as robust newborn mandates, high decentralized-trial density, and clear FDA pathways reinforced procurement cycles. The National Academies’ 2025 roadmap urges continued excellence, maintaining >98% newborn coverage through DBS protocols. Canada and Mexico add incremental volumes via regional screening expansions, though reimbursement heterogeneity tempers uniform penetration. FDA oversight of specimen-collection kits under broader LDT reform introduces short-term compliance costs yet ultimately promotes product standardization, solidifying confidence in the specimen collection cards market.

APAC Specimen Collection Cards Market

Asia-Pacific is the fastest-growing territory, advancing at 7.33% CAGR as India, China, and Japan fund broad screening and digital health platforms. India’s cystic-fibrosis initiatives and Thailand’s near-universal rural coverage highlight scale potential. China’s urban hospitals invest in microfluidic DBS automation to tackle rising non-communicable disease burdens. Japan’s lysosomal-disorder screening underscores advanced multicondition protocols that pull high-margin card variants. Pharmaceutical outsourcing hubs in the region drive demand for remote biosampling in multicountry oncology and metabolic trials, reinforcing future upside for the specimen collection cards market.

EMEA and LATAM Specimen Collection Cards Market

Europe exhibits steady replacement demand, with Italy’s five-year program screening 343,507 newborns and the Netherlands pioneering NGS workflows for DBS DNA. The European Health Data Space smooths cross-border virtual-trial operations, spurring card purchases for pan-EU studies. Middle East and Africa markets gradually expand, typified by Saudi Arabia’s 18-disorder panel roll-out. Latin America, with Mexico’s renewed policy focus, offers latent upside contingent on funding stability. Together, these geographies ensure globally diversified growth for the specimen collection cards market.

Competitive Landscape

The market remains moderately fragmented. Revvity, Danaher, and Thermo Fisher Scientific anchor the high-volume tier, using global distribution and assay portfolios to protect share. Thermo Fisher’s USD 3.1 billion acquisition of Olink in 2024 bolstered proteomics integration, illustrating vertical deepening. Danaher opened two CLIA-certified innovation centers to accelerate companion-diagnostic co-development, aligning specimen cards with precision medicine roadmaps. Specialized firms such as Neoteryx and Capitainer AB capitalize on VAMS precision to penetrate decentralized-trial contracts. DBS System SA and Ahlstrom carve niches through substrate engineering and lipid-specific coatings, respectively.

Strategic consolidation cycles every few years as large players fill technology gaps. Regeneron’s 2025 purchase of 23andMe assets exemplifies genomic-infrastructure expansion, though the acquisition landscape mainly revolves around platform convergence rather than pure volume grabs. Vendors increasingly bundle analytics, cloud portals, and logistics, creating stickier customer relationships. White-space opportunities lie in AI-augmented image analysis of card saturation, blockchain traceability for forensic custody, and smartphone-assisted self-collection coaching. Successful innovators will harmonize these digital layers with robust regulatory dossiers, a prerequisite for capturing premium pricing inside the specimen collection cards market.

Pricing dynamics favor differentiated technologies. Legacy plain-paper DBS cards face moderate commodity pressure, yet tailored chemistries command premiums in multi-omics applications. VAMS providers justify higher ASPs through quantitative accuracy and low sample rejection rates, resonating with pharmaceutical CROs. Regional distributors in LMICs leverage cost-efficient bundles to penetrate public-health tenders, occasionally private-labeling generic cards. Despite rising competition, diversified incumbents sustain margins by cross-selling reagents and analytical instruments, securing durable earnings streams across the specimen collection cards market.

Specimen Collection Cards Industry Leaders

Revvity

Danaher

Qiagen

Thermo Fisher Scientific

Ahlstrom

- *Disclaimer: Major Players sorted in no particular order

Specimen Collection Cards Market Companies Covered in this Report

- Agilent Technologies

- Ahlstrom

- Bio-Rad Laboratories

- Capitainer AB

- Danaher

- DBS System SA

- Eastern Business Forms

- Roche

- GE Healthcare

- Merck

- Neoteryx

- QIAGEN

- Revvity

- Sarstedt AG & Co.

- Shimadzu Diagnostics

- Spot On Sciences

- Thermo Fisher Scientific

- U-Bio Meditech

- West Pharmaceutical Services

Recent Industry Developments in Specimen Collection Cards Market

- February 2025: Ahlstrom’s Lipid Saver and related biological sample collection cards received FDA Class I listing, validating product safety and compliance.

- September 2024: Agilent opened its Biopharma CDx Services Lab in California to support drug-developer companion-diagnostic pipelines.

Global Specimen Collection Cards Market Report Scope

Segmentation Overview

| Dried Blood Spot (DBS) Cards |

| FTA Nucleic-acid Cards |

| Protein Saver Cards |

| Dried Plasma Spot Cards |

| Saliva Collection Cards |

| Urine Collection Cards |

| Other Specialty Cards |

| Blood |

| Saliva |

| Urine |

| Other Biofluids |

| Newborn Screening |

| Infectious-Disease Diagnostics |

| Forensic & Law-Enforcement |

| Drug Discovery & Clinical Trials |

| Therapeutic Drug Monitoring |

| Genomic & Proteomic Research |

| Environmental & Veterinary Diagnostics |

| Other Applications |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Research & Academic Institutes |

| Forensic Laboratories |

| Pharmaceutical & Biotech Companies |

| Home & Tele-health Testing Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Card Type | Dried Blood Spot (DBS) Cards | |

| FTA Nucleic-acid Cards | ||

| Protein Saver Cards | ||

| Dried Plasma Spot Cards | ||

| Saliva Collection Cards | ||

| Urine Collection Cards | ||

| Other Specialty Cards | ||

| By Sample Type | Blood | |

| Saliva | ||

| Urine | ||

| Other Biofluids | ||

| By Application | Newborn Screening | |

| Infectious-Disease Diagnostics | ||

| Forensic & Law-Enforcement | ||

| Drug Discovery & Clinical Trials | ||

| Therapeutic Drug Monitoring | ||

| Genomic & Proteomic Research | ||

| Environmental & Veterinary Diagnostics | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Research & Academic Institutes | ||

| Forensic Laboratories | ||

| Pharmaceutical & Biotech Companies | ||

| Home & Tele-health Testing Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the specimen collection cards market in 2025?

The specimen collection cards market size reached USD 490.96 million in 2025 and is projected to hit USD 628.51 million by 2030.

Which card type generates the most revenue?

Dried blood spot formats contributed 61.38% of 2024 revenue, making them the leading card type.

Why is Asia-Pacific growing the fastest?

Government-funded newborn screening roll-outs and pharmaceutical investment in decentralized trials are propelling a 7.33% CAGR through 2030.

What technology is challenging traditional DBS cards?

Volumetric absorptive microsampling offers standardized volumes and higher quantitative accuracy, drawing interest from pharmaceutical sponsors.

Which end-user segment is advancing the quickest?

Home and tele-health testing services are forecast to expand at 9.74% CAGR as consumers adopt convenience-focused self-collection kits.

What is the main restraint confronting market growth?

Analytical-sensitivity limits of low-volume spots can hinder detection of rare biomarkers, particularly in advanced precision-medicine assays.

Page last updated on: