Specialty Enzymes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

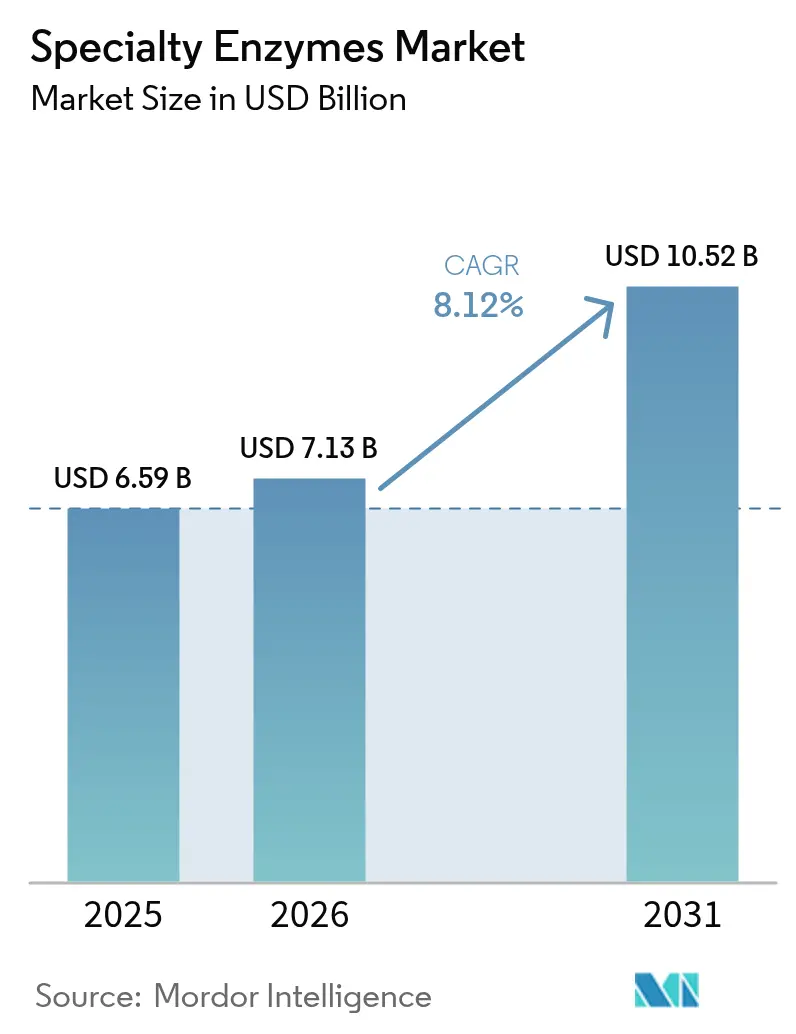

| Market Size (2026) | USD 7.13 Billion |

| Market Size (2031) | USD 10.52 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Enzymes Market Analysis by Mordor Intelligence

Specialty enzymes market size in 2026 is estimated at USD 7.13 billion, growing from 2025 value of USD 6.59 billion with 2031 projections showing USD 10.52 billion, growing at 8.12% CAGR over 2026-2031. Market growth is underpinned by the wider use of biocatalysts in pharmaceutical production, growing demand for sustainable industrial processes, and the expanding acceptance of enzyme-based therapeutics. Ongoing advances in enzyme design are allowing manufacturers to respond faster to shifting industry needs while keeping production costs competitive. Investments in AI-guided enzyme engineering have shortened development cycles from years to months, facilitating quicker commercialization and reducing cost barriers. These advancements are enabling manufacturers to meet evolving industry demands while maintaining cost efficiency. Supportive environmental policies and consumer interest in natural products are prompting manufacturers to favor recombinant and plant-based enzyme sources. Breakthroughs like the CelOCE metalloenzyme, which can double cellulose conversion efficiency, highlight the transformative potential of enzyme innovation in biofuels and other resource-intensive industries. Such innovations are expected to significantly enhance sustainability and operational efficiency across various applications.

Key Report Takeaways

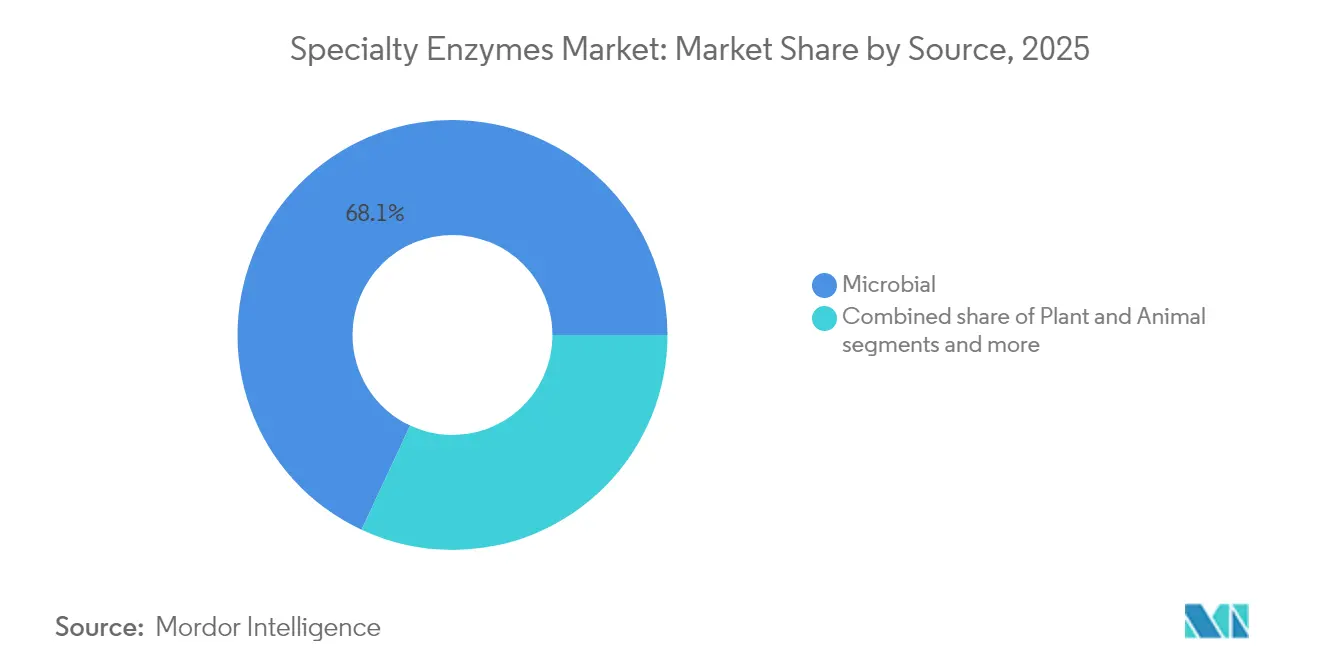

- By source, microbial enzymes commanded 68.05% of the specialty enzymes market share in 2025, while plant sources are forecast to grow at 9.35% CAGR to 2031.

- By form, liquid formulations led with 56.60% revenue share in 2025 and are projected to expand at 9.98% CAGR through 2031.

- By enzyme type, carbohydrases held 35.70% of the specialty enzymes market size in 2025 and are projected to maintain the fastest 9.84% CAGR between 2026-2031.

- By application, pharmaceuticals accounted for 42.10% of the specialty enzymes market size in 2025 and are advancing at a 9.28% CAGR to 2031.

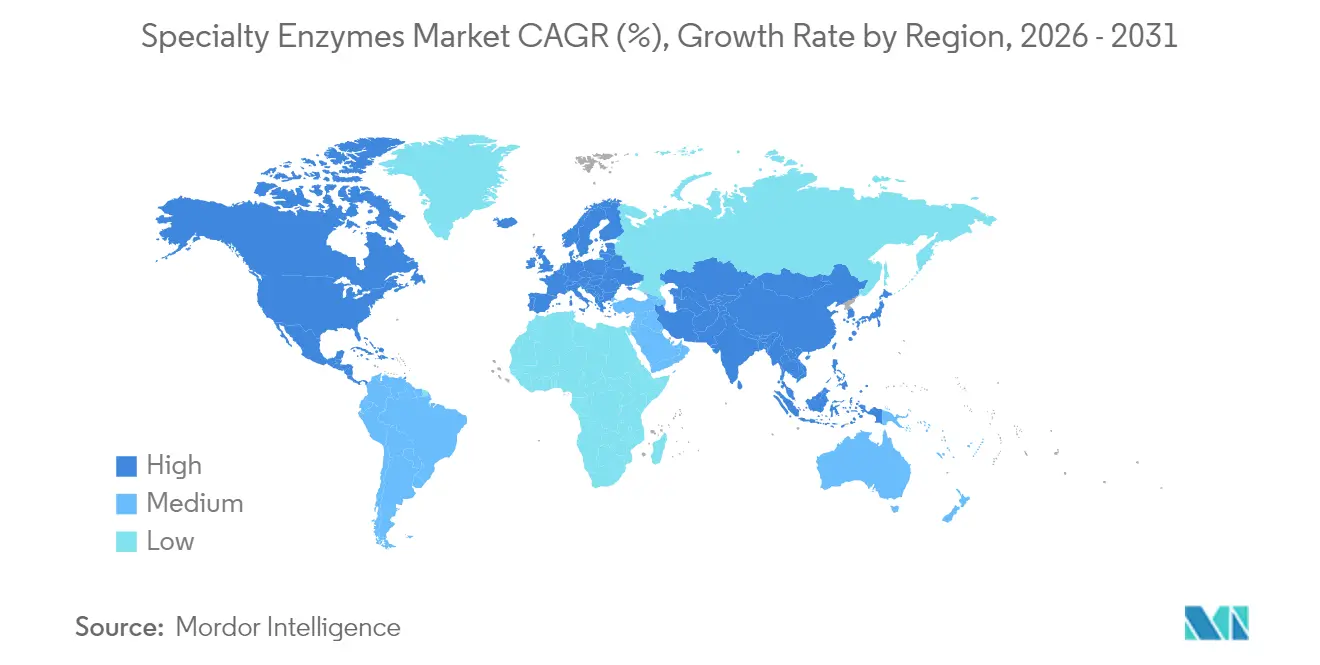

- By geography, North America captured 32.78% of the specialty enzymes market share in 2025, while Asia-Pacific is set to register a 9.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specialty Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of eco-friendly biocatalysts in pharmaceutical manufacturing | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Government support drives market growth through policy and funding | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Advancement in enzyme engineering and directed evolution | +1.5% | Global | Short term (≤ 2 years) |

| Demand from cosmetic and dermatology sectors for enzymatic peels | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Surge in demand for enzymatic wound debridement products | +0.7% | Global, led by North America | Short term (≤ 2 years) |

| Growing focus on green chemistry and sustainable industrial process | +1.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing adoption of eco-friendly biocatalysts in pharmaceutical manufacturing

Pharmaceutical producers are increasingly replacing chemical catalysts with biocatalysts to reduce environmental impact and improve process efficiency. This shift is particularly valuable in biologics, where enzyme precision minimizes the need for complex purification steps. The Food and Drug Administration (FDA)'s regulatory review periods for biologics, including POMBILITI and EPKINLY in 2025, indicate streamlined approval processes for enzyme-based therapeutics [1]Source: Federal Register, “Determination of regulatory review periods for biologics,” federalregister.gov. Engineered enzymes enable the production of chiral pharmaceutical intermediates with improved selectivity and reduced waste compared to traditional methods. Computational design tools have shortened enzyme development cycles, enabling pharmaceutical companies to develop biocatalysts for specific drug synthesis routes more efficiently. Enzyme applications now extend to advanced drug delivery systems and therapies for genetic disorders, broadening opportunities for manufacturers in the specialty enzyme space.

Government support drives market growth through policy and funding

Government initiatives are accelerating the growth of the specialty enzymes market through policy frameworks and direct funding that support research, commercialization, and industrial adoption. Governments are actively funding enzyme innovation through grants, tax benefits, and PPP collaborations that bridge academia and industry. India's BioE3 policy represents a major government intervention in biotechnology, with an allocation of INR 9,197 crore (USD 1.1 billion) to establish biomanufacturing hubs for bio-based chemicals and enzymes. The policy aims to achieve a USD 300 billion bioeconomy by 2030, identifying enzymes as essential components across six areas, including precision biotherapeutics and climate-resilient agriculture [2]Source: Ministry of Science and Technology India, “BioE3 policy highlights,” dst.gov.in. China's updated food safety regulatory system has created opportunities for enzyme manufacturers through mandatory registration procedures that benefit established companies with proven safety records [3]Source: United States Department of Agriculture, “China feed additive export guidelines,” usda.gov. The European Union's pre-market approval requirements for food enzymes have standardized safety assessments, reducing market entry barriers for compliant manufacturers.

Advancement in enzyme engineering and directed evolution

The integration of artificial intelligence, robotics, and enzyme engineering has made custom biocatalysts more accessible, reducing development costs. Directed evolution techniques have progressed beyond traditional random mutagenesis to incorporate rational design principles, allowing researchers to engineer enzymes with new catalytic functions. High-throughput screening platforms enable the simultaneous processing of thousands of enzyme variants, accelerating the identification of effective biocatalysts for industrial applications. Computational workflows integrate protein structure prediction with machine learning models to design enzymes for specific chemical transformations, particularly in pharmaceutical synthesis, where selectivity is crucial. The integration of artificial intelligence, robotics, and enzyme engineering has made custom biocatalysts more accessible, allowing smaller biotechnology companies to compete with established enzyme manufacturers. Companies in the global specialty enzyme market are implementing advanced engineering techniques, including machine learning and directed evolution, to develop more efficient, robust, and novel enzymes. In May 2025, Isomerase launched EvoSelect, a machine learning-powered enzyme engineering platform that uses evolutionary data to design optimized enzyme sequences.

Demand from cosmetic and dermatology sectors for enzymatic peels

Proteolytic enzymes, including papain, bromelain, and ficin, are replacing chemical exfoliants in skincare products due to their ability to selectively remove dead skin cells while preserving healthy tissue. Clinical research shows that proteolytic enzymes can improve skin texture and firmness as effectively as higher-strength chemical exfoliants, but with far less irritation. The market growth aligns with sustainability initiatives, as manufacturers extract active compounds from fruit by-products, reducing waste while meeting clean beauty requirements. However, the absence of regulations requiring manufacturers to disclose enzyme activity levels creates quality inconsistencies that may affect market growth. The integration of enzyme technology with encapsulation and slow-release systems is expanding its role beyond exfoliation into anti-aging and treatment-based skincare products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost for customized enzymes | -1.1% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Short shelf life and stability challenges | -0.8% | Global, with higher impact in tropical regions | Short term (≤ 2 years) |

| Risk of allergic reaction and immunogenicity in enzyme therapy | -0.6% | Global, regulatory focus in North America and Europe | Long term (≥ 4 years) |

| Ethical concern in use of animal-derived enzymes | -0.4% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High production cost for customized enzymes

The complex processes involved in designing, engineering, and scaling up tailored enzymes require substantial investment in advanced technologies, skilled labor, and quality control measures. The need for specialized raw materials and stringent regulatory compliance increases production costs. Tailoring enzymes for specialized industrial processes requires heavy research and developments investment, often taking two to three years before the product reaches commercial readiness. Small and medium-sized biotechnology companies encounter significant challenges in scaling production from laboratory to commercial quantities. The required fermentation infrastructure demands substantial capital investment and specialized expertise. The pricing difference between industrial and pharmaceutical enzymes reflects their distinct value propositions, with pharmaceutical proteins priced at higher end compared to industrial applications. Manufacturing economics are impacted by the requirement for specialized purification processes and quality control systems that comply with regulatory standards for different end-use applications.

Short shelf life and stability challenges

Maintaining enzyme stability remains a key challenge, especially for liquid formulations, which tend to degrade faster under normal storage temperatures. This challenge is most significant in tropical regions, where temperature fluctuations and humidity can reduce enzyme activity by 20-30% within months of production. While protein engineering has enabled the development of thermostable enzymes to address stability concerns, this often compromises catalytic efficiency or substrate specificity. Cold chain logistics requirements for maintaining enzyme activity increase distribution costs by 15-25%, creating particular challenges for companies serving emerging markets with limited refrigeration infrastructure. The industry is addressing these challenges through innovations in enzyme formulation, including stabilizing additives and protective coatings that extend shelf life while maintaining biological activity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Dominance Drives Cost Efficiency

Microbial sources hold a 68.05% market share in 2025, due to the scalability and cost advantages of recombinant DNA technology for enzyme production. Plant-derived enzymes are growing at 9.35% CAGR (2026-2031), driven by consumer demand for natural ingredients and sustainability requirements in food and cosmetic applications. Animal-derived enzymes experience declining demand due to ethical concerns and regulatory restrictions, especially in European markets where alternative sources are increasingly required.

Microbial enzymes dominate because they can be produced under controlled fermentation conditions, ensuring consistent quality and minimizing contamination risks. Microbial production systems leverage advances in synthetic biology to develop production strains with improved enzyme secretion and minimized by-product formation. The growth in plant sources is supported by new enzyme extraction methods from agricultural waste, which create circular economy opportunities and lower raw material costs.

By Form: Liquid Formulations Lead Innovation

Liquid formulations dominate the market with a 56.60% share in 2025 and are projected to grow at a CAGR of 9.98% through 2031, driven by their superior performance characteristics and application versatility. Dry enzyme formulations maintain their position in specialized applications where extended shelf life and reduced shipping costs are essential, particularly in animal feed and industrial cleaning sectors. The market preference for liquid formulations stems from their immediate bioavailability and seamless integration into manufacturing processes without dissolution requirements. New stabilization technologies have helped extend the shelf life of liquid enzymes, overcoming one of their main historical drawbacks.

Non-aqueous liquid systems are increasing in adoption for applications that require better substrate solubility and reduced feedback inhibition. Concentrated liquid formulations offer reduced storage and transportation costs while maintaining enzyme activity. Dry formulations continue to improve through advanced spray-drying and freeze-drying techniques that maintain enzyme structure and activity during dehydration.

By Enzyme Type: Carbohydrases Maintain Dual Leadership

Carbohydrases dominate the market with a 35.70% share in 2025 and are projected to grow at a CAGR of 9.84% during 2026-2031. This dominance is driven by their extensive use in food processing, biofuel production, and pharmaceutical applications. Proteases maintain a significant market presence through their essential role in detergent manufacturing and pharmaceutical synthesis, while lipases continue to expand in biodiesel production and food processing applications. Additional enzyme categories, including oxidoreductases and transferases, are becoming increasingly important in pharmaceutical manufacturing and environmental solutions.

The carbohydrase segment's market demand is reinforced by increasing demand for plant-based foods and biofuel production, as these enzymes effectively break down complex carbohydrates. Multi-enzyme formulations, such as Ronozyme® Multigrain, which combines endo-1,4-beta-xylanase, endo-1, 3(4)-beta-glucanase, and endo-1,4-beta-glucanase, enhance processing efficiency and reduce operational costs. The development of enzyme cocktails creates synergistic effects that improve performance in complex substrate breakdown applications.

By Application: Pharmaceutical Sector Drives Innovation

The pharmaceutical application segment holds a dominant 42.10% market share in 2025 and is projected to grow at 9.28% CAGR through 2031. This leadership position stems from established enzyme usage in pharmaceutical manufacturing and ongoing research developments. Food and beverage applications represent a substantial market segment, utilizing enzymes for processing, preservation, and quality improvement. The animal feed segment expands through regulatory-approved enzyme additives that enhance nutrient absorption and reduce environmental effects.

Additional applications in industrial cleaning, textile processing, and environmental remediation provide market diversification. The pharmaceutical segment's growth is further driven by enzyme-based drug delivery systems and enzyme replacement therapies for genetic disorders. Enhanced enzyme engineering capabilities enable the development of more efficient biocatalysts for pharmaceutical production, resulting in reduced manufacturing costs and environmental impact.

Geography Analysis

In 2025, North America clinched a commanding 32.78% share of the specialty enzymes market, supported by strong research and development capabilities and streamlined regulatory pathways for enzyme therapeutics. Leading universities in the region spearhead AI-driven enzyme design, propelling domestic innovation. Furthermore, tax incentives championing sustainable manufacturing have amplified enzyme utilization across various industrial processes, solidifying North America's preeminence. The region's strong focus on technological advancements and partnerships between academia and industry further strengthens its competitive edge in the global market.

Asia-Pacific is emerging as the fastest-growing region, driven by supportive government initiatives, cost advantages, and a skilled workforce, with a projected 9.62% CAGR. Supportive policies and inherent cost advantages underpin this growth. India's BioE3 strategy, coupled with China's revised food enzyme regulations, has smoothed the path for market entry. Moreover, the region's affordable production costs, a reservoir of skilled talent, and state-of-the-art infrastructure are luring global enzyme manufacturers. The region's growing focus on biotechnology and government-backed initiatives to enhance enzyme production capacity further contribute to its rapid growth.

Europe, South America, the Middle East, and the Africa region are also making strides. In Europe, strict safety standards and a sustainability-focused regulatory environment continue to foster innovation and consumer confidence. Additionally, the region's emphasis on green chemistry and eco-friendly enzyme applications aligns with its sustainability goals, driving further market expansion. Meanwhile, in South America, biotech ventures in Brazil and Argentina, buoyed by favorable trade agreements and bioeconomy initiatives, are driving growth in the food and agriculture sectors. The Middle East and Africa region is witnessing advancements, owing to healthcare enhancements and initiatives aimed at food security.

Regulatory Landscape

Specialty enzymes used in food and beverage applications operate under multi-track regulatory pathways that vary by jurisdiction and intended use (processing aid, food additive, or ingredient), while pharma- and industrial-grade enzymes must also meet sector-specific quality and safety requirements. In the United States, the FDA regulates food enzyme preparations through the food additive framework (including applicable provisions under 21 CFR Part 170 and related sections) or via the voluntary GRAS notification route, which influences the evidence expected for identity, manufacturing controls, and toxicology. Internationally, FAO/WHO bodies such as Codex Alimentarius and JECFA provide specifications and safety guidance that often function as reference points in cross-border trade, even though they do not constitute a single binding standard.

In the European Union, Regulation (EC) No 1332/2008 harmonizes rules for food enzymes, with EFSA conducting pre-market safety evaluations as inputs to authorization. Market access depends on compliance with EU requirements as the Union List process advances, and the European Commission update to the Register of food enzymes in February 2026 reflects continued administrative progress toward the future positive list. Companies also manage different oversight regimes for enzymes used in feed or technical applications (for example, national feed additive rules or EU chemicals requirements such as REACH), which increases the importance of regulatory science, traceability, and documentation aligned to each end-use category.

Value Chain Analysis

The specialty enzymes value chain begins with feedstock and strain inputs, moves through discovery and engineering (screening, directed evolution, and application development), then proceeds to scale-up fermentation, downstream recovery and purification, and final formulation into liquid or dry products. Manufacturing often includes quality control labs and process analytics alongside fermentation and formulation to support traceability and consistent activity levels, which is especially relevant for high-value pharmaceutical and food-grade enzymes. Firms such as Novonesis, Kerry, IFF, AB Enzymes, Advanced Enzyme Technologies, and c-LEcta reflect a blend of large-scale producers and specialists, with c-LEcta’s ENESYZ platform used to tailor enzymes for targeted applications.

Go-to-market typically combines direct sales to large FMCG, dairy, baking, and industrial customers with distributors and regional technical service teams that support customer trials, line commissioning, and optimization. Key friction points include fermentation capacity availability, raw material and media cost volatility, and stability and cold-chain constraints for activity-sensitive products, particularly in warm climates. To reduce lead times and improve resilience, manufacturers increasingly use a mix of in-house production, regional hubs, and application labs that speed customer qualification and adapt formulations to local processing conditions.

Competitive Landscape

The specialty enzymes market exhibits moderate consolidation. Major companies dominate the specialty enzymes market, controlling a significant portion of global revenue. This dominance, however, leaves room for niche specialists to thrive by targeting specific high-margin applications and addressing unmet needs in specialized industries. These niches often focus on industries such as pharmaceuticals, food and beverages, and biofuels, where tailored enzyme solutions are in high demand. Key players include DSM-Firmenich AG, Kerry Group plc, BASF SE, International Flavors & Fragrances, and Associated British Foods plc.

Many leading manufactuerers are adopting vertical integration managing everything from enzyme production to technical support to strengthen client relationships and secure steady revenue flows. These strategies also enable firms to offer end-to-end solutions, strengthening their value proposition in the market. Additionally, vertical integration helps companies maintain tighter control over quality and costs, ensuring a competitive edge.

Companies with comprehensive regulatory knowledge use this advantage to fast-track market approvals, setting up barriers for newer competitors. In this evolving landscape, technology rather than pricing has become the key differentiator, driving continuous innovation and opening new opportunities for specialized enzyme developers. The emphasis on innovation ensures that companies remain agile in addressing evolving customer demands and regulatory requirements.

Specialty Enzymes Industry Leaders

International Flavors & Fragrances

Kerry Group plc

BASF SE

Associated British Foods plc

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A central opportunity area is supply chain localization and capacity additions for food and nutrition enzymes, supported by 2026 investments and site upgrades that expand regional availability and shorten lead times. Kerry’s expanded biotechnology manufacturing hub in Carrigaline, Co. Cork, Ireland (announced January 2026) targets higher lactase production capacity for dairy applications, supporting lactose-free and sugar-reduction product development. IFF’s March 2026 effort to transform its Arroyito site in Argentina into a fermentation-based enzyme production hub also points to regionally anchored manufacturing and application support for Latin American food and bio-industrial customers.

Another near-term whitespace is application-led enzyme systems that drive measurable processing and label outcomes, rather than operating only as formulation aids. This is most evident in brewing, dairy, and emerging alternative-protein processing, where enzyme performance connects to throughput, calorie or carbohydrate reduction, and waste minimization. Regulatory gating remains a key condition: EU access depends on EFSA safety evaluations under Regulation (EC) No 1332/2008, while US commercialization often requires FDA GRAS positioning or food additive compliance. This dynamic increases the value of companies that combine enzyme engineering and performance validation with dossier-ready documentation and region-specific technical support to accelerate customer adoption across geographies.

Recent Industry Developments

- May 2026: Kerry launched AlphaGal Ultra, a multi-enzyme solution for animal feed aimed at improving nutrient availability and feed conversion. The introduction expands Kerry’s specialty enzyme positioning beyond food processing into performance-driven feed applications and reinforces its portfolio in regulated livestock and aquaculture value chains.

- March 2026: IFF announced the transformation of its Arroyito site in Argentina into a full fermentation-based enzyme production hub serving food, animal nutrition, and bio-industrial markets. The site upgrade supports faster regional fulfillment and application collaboration in Latin America, reducing dependence on longer global supply routes for enzyme intermediates and finished products.

- June 2024: BASF completed the sale of its bioenergy enzymes business to Lallemand, including the Spartec product portfolio. The divestment signaled a sharper focus on other biosolutions and higher-value biological platforms, while transferring bioenergy enzyme continuity and customer relationships to a specialist fermentation player.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers specialty enzymes that are manufactured and sold for use in targeted end uses such as food and beverages, pharmaceuticals, and animal nutrition, and it is measured as revenue generated from enzyme products sold into these applications.

Scope exclusions: Excludes basic or commodity enzymes that are primarily produced for broad, low-differentiation industrial processing where specialty performance claims are not the main purchase driver.

Segmentation Overview

- By Source

- Plant

- Microbial

- Animal

- By Form

- Liquid

- Dry

- By Type

- Carbohydrases

- Proteases

- Lipases

- Others

- By Application

- Food and Beverages

- Pharmaceutical

- Animal Feed

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, align definitions, and build the initial demand and pricing logic before interviews started. We relied on public, non-paywalled references such as enzyme and biotech publications in peer-reviewed journals, trade and tariff statistics from UN Comtrade, government sources such as the US FDA and the European Medicines Agency for enzyme related approvals and usage contexts, and food safety references from Codex Alimentarius and related national food agencies.

To translate those signals into a usable model, we also reviewed company annual reports, investor presentations, product catalogs, and reputable press coverage to map where specialty enzymes are actually being commercialized. In parallel, a paid subscription for company financials and a patent database were used to cross-check supplier activity, product pipelines, and ownership changes that can distort market totals in a given year. The desk sources named here are illustrative, and we referenced additional public materials and paid datasets for validation and clarification as the analysis progressed.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with enzyme manufacturers, distributors, and downstream users in food processing, pharma formulation, and animal nutrition, so the model assumptions could be stress-tested against real buying and selling behavior. We also checked regional differences across APAC, EMEA, and the Americas to validate adoption patterns, typical pricing moves, and how regulatory and quality requirements shape demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 39% |

| Mid tier: 57% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 16% | Managers: 48% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where industry production, trade flows, and end-use demand indicators are used to reconstruct the addressable specialty enzyme demand pool by region, and then the value is derived using observed price bands. To keep it practical, results are corroborated with selective bottom-up approximations like sampled supplier revenue splits, channel checks for high-volume applications, and a volume times ASP sanity test for enzyme types where pricing is more stable.

Key inputs used in the model include enzyme type mix across carbohydrases, proteases, and lipases, the application split across food and beverages, pharmaceuticals, and animal nutrition, typical dosage and formulation patterns that influence volume consumption, and observed ASP movements tied to quality grades and supply tightness. Where direct volume signals are weak, gaps are handled by using proxy indicators such as downstream output trends and a conservative penetration curve, which are then reviewed during interviews.

Forecasting is done using scenario analysis supported by short regression checks on a few drivers that respondents consistently linked to demand, such as processed food production trends, pharmaceutical manufacturing activity, and shifts toward higher-performance formulations. Assumptions are kept transparent so the same steps can be repeated when new public statistics or refreshed interview inputs become available.

Data Validation & Update Cycle

Validation is done by triangulating the modeled totals against independent signals such as supplier expansion announcements, patenting intensity, and regional trade movements for relevant enzyme categories. When a region or application shows a jump that is not supported by those checks, the inputs are re-opened, and follow-up calls are triggered to understand whether the change is real or a data artifact.

Before sign-off, the model goes through multi-step analyst reviews where assumptions, unit conversions, and currency treatment are checked for consistency. Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity additions, major regulatory changes, or meaningful shifts in pricing. Right before delivery, we do a fresh pass on the latest public releases so clients receive an up-to-date view.

Mordor Intelligence's Specialty Enzymes Market Size Versus Other Published Estimates

Published market sizes for specialty enzymes can differ even when the topic sounds identical, because the included enzyme set, end-use coverage, and the year used for pricing and currency conversion are not always aligned. Differences also show up when one publisher relies more on broad industry ratios, while another leans more on application demand signals and interview validation.

Food-grade enzyme products used in mainstream industrial processing often get included in some estimates, and that item sits outside Mordor Intelligence's scope when it is not sold as a specialty performance-driven enzyme into the defined applications. Another common gap comes from how ASP progression is handled, since some figures apply a single inflation uplift, whereas our checks use application-level price bands discussed with buyers and sellers. Update cadence also shifts comparability, because M&A, capacity additions, and regulatory changes can affect how revenue is attributed, especially across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.13 B (2026) | |

| Global Consultancy A | USD 6.05 B (2024) | Uses an earlier base year and a broader definition that emphasizes product splits, which can shift value between specialty and adjacent enzyme categories when pricing is averaged at a higher level. |

| Industry Publisher B | USD 6.58 B (2025) | Long-horizon forecasting to 2035 increases sensitivity to assumed CAGR and price escalation, and the scope language is less specific on what is excluded, which can lead to wider inclusion of industrial enzyme use cases. |

Overall, the spread is largely explained by scope edges and base-year alignment, followed by how pricing is carried forward through the forecast period. By tying the model to clear application demand signals and then cross-checking with supplier and channel feedback, we keep the estimate traceable to inputs that can be re-tested when the market shifts.

Key Questions Answered in the Report

What is the current specialty enzymes market size?

The specialty enzymes market size stands at USD 7.13 billion in 2026, with expectations to reach USD 10.52 billion by 2031.

Which application segment is growing fastest?

Pharmaceuticals lead both in 2025 share at 42.10% and in growth, posting a 9.28% CAGR through 2031.

Which geographic region shows the highest growth potential?

Asia-Pacific is projected to expand at 9.62% CAGR, supported by India’s BioE3 policy and evolving Chinese regulations.

Why are liquid formulations preferred?

Liquid enzymes offer immediate bioavailability and easier integration into manufacturing lines, helping the form maintain 56.60% share and the fastest 9.98% CAGR.

Page last updated on: