Spay And Neuter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

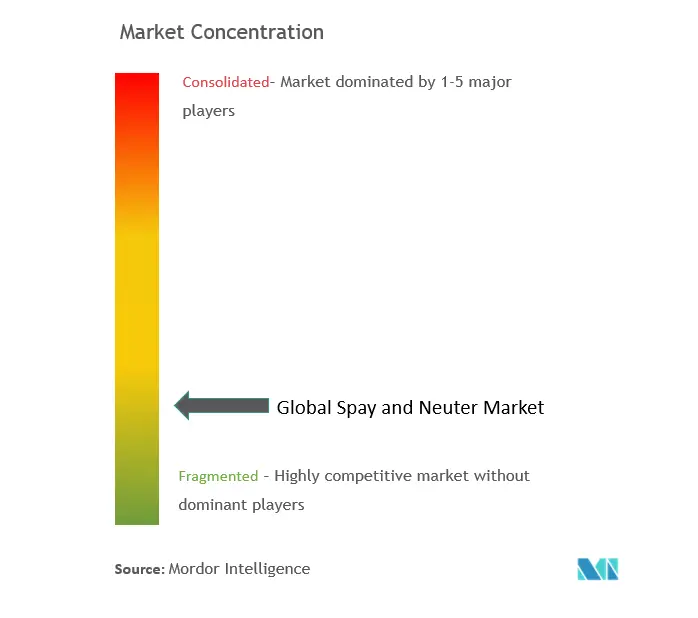

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spay And Neuter Market Analysis by Mordor Intelligence

The spay and neuter market size in 2026 is estimated at USD 2.83 billion, growing from 2025 value of USD 2.70 billion with 2031 projections showing USD 3.54 billion, growing at 4.63% CAGR over 2026-2031. Robust demand for elective sterilization, the rise of premium preventive-care bundles, and early adoption of non-surgical products are set to keep the global spay and neuter market on a steady growth curve. Persistent pet-humanization trends have elevated sterilization from a population-control tactic to a core element of companion-animal wellness plans. Public and private subsidy programs, mandatory municipal ordinances, and large-scale NGO campaigns integrate affordable access with social responsibility, further sustaining procedure volumes. In parallel, corporate consolidation has increased pricing transparency and protocol standardization, while nascent non-surgical technologies promise to widen access in cost-sensitive regions.

Key Report Takeaways

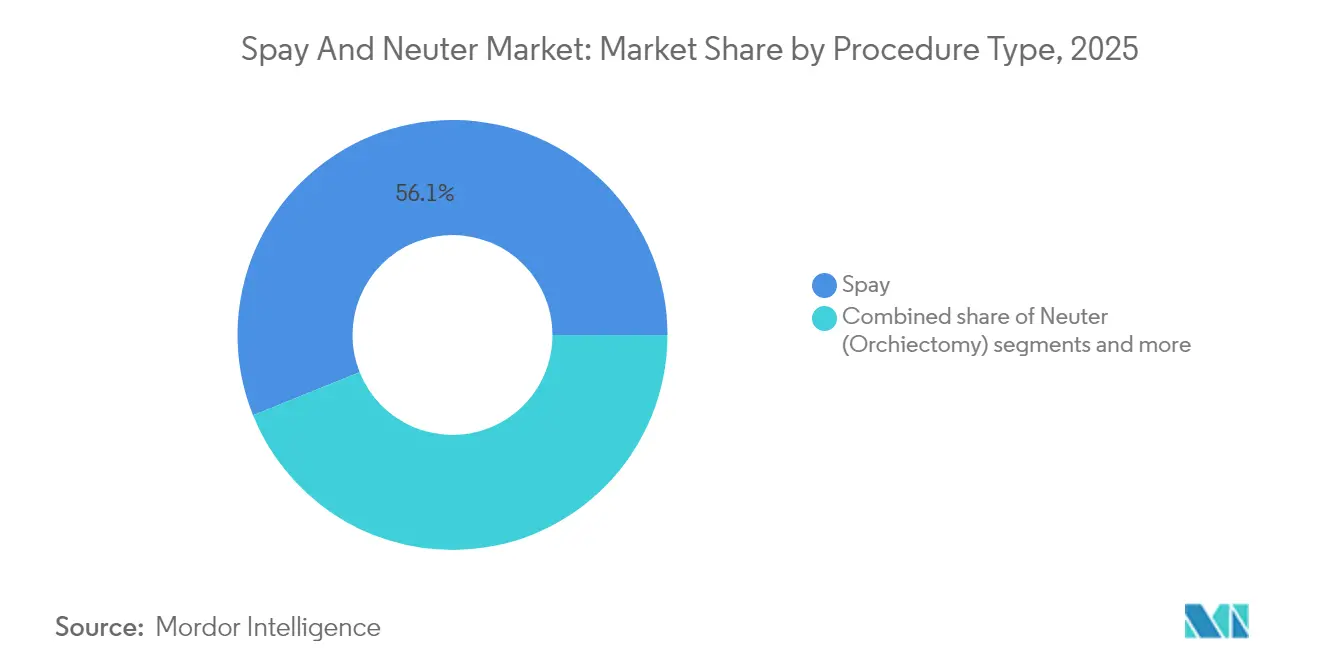

- By procedure type, spay operations commanded 56.08% of the spay and neuter market share in 2025; non-surgical sterilization is projected to expand at a 5.30% CAGR through 2031.

- By animal type, dogs led with a 64.62% revenue share of the spay and neuter market size in 2025, whereas cats are poised to record the fastest 6.05% CAGR to 2031.

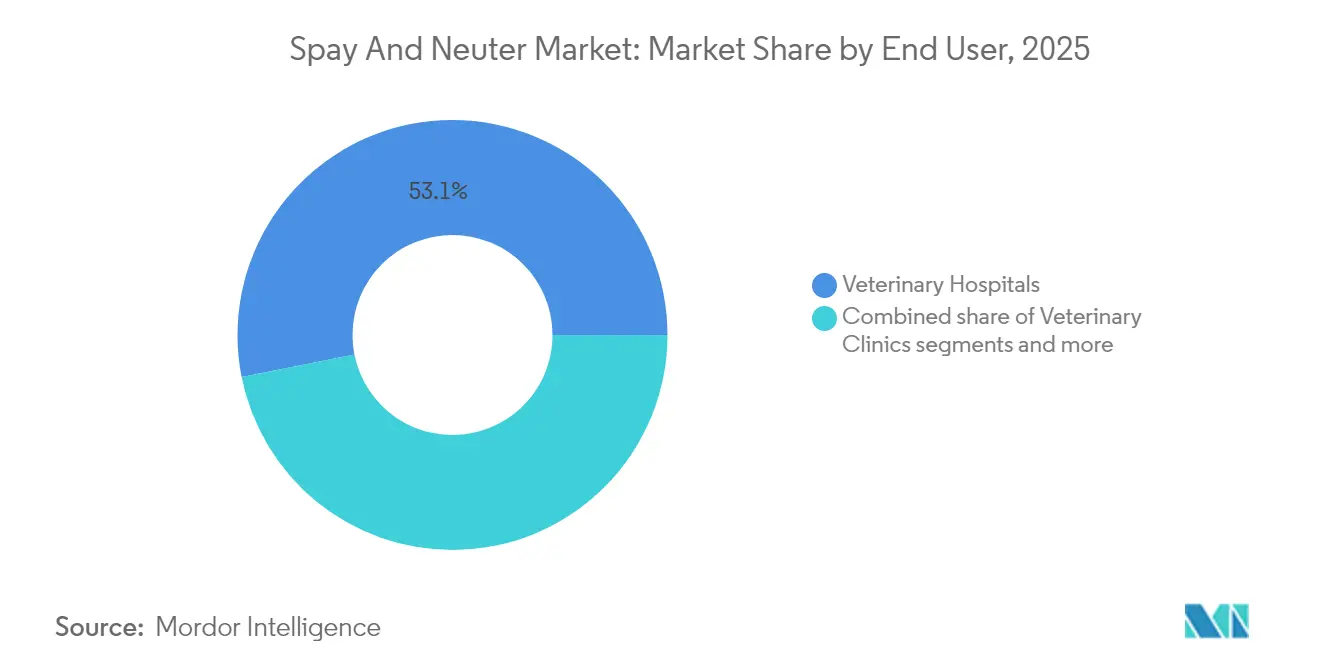

- By end user, veterinary hospitals held 53.12% share of the spay and neuter market size in 2025, while mobile/community programs are forecast to progress at 6.92% CAGR through 2031.

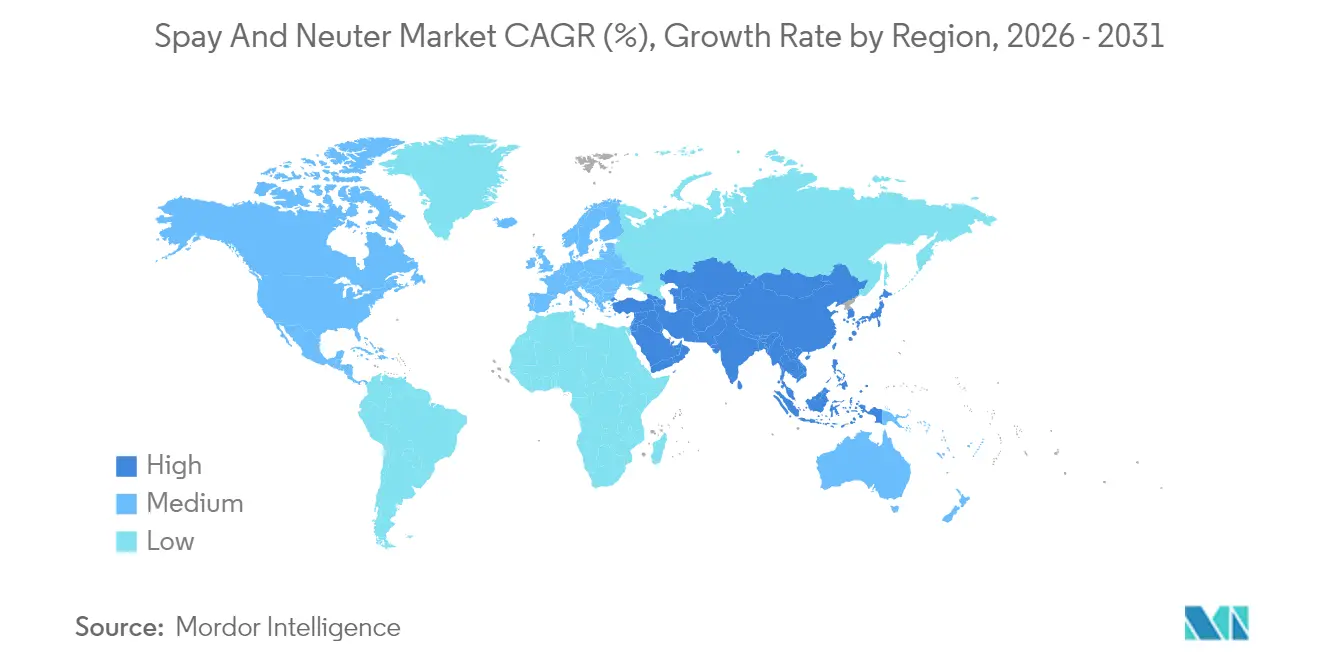

- By geography, North America dominated with a 41.74% spay and neuter market share in 2025; Asia-Pacific is expected to post the highest 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spay And Neuter Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising companion animal ownership & pet-humanization | +1.2% | Global; strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Government & NGO subsidized spay-neuter campaigns | +0.8% | North America core; expanding to Latin America | Short term (≤ 2 years) |

| Mandatory municipal sterilization ordinances | +0.6% | North America & Europe; emerging in APAC | Long term (≥ 4 years) |

| Rising veterinary healthcare expenditure | +1.0% | Global; led by developed markets | Medium term (2-4 years) |

| Breakthrough non-surgical sterilant pipelines | +0.4% | Global; regulatory approval dependent | Long term (≥ 4 years) |

| Corporate chain bundled low-cost surgery packages | +0.7% | North America & Europe; expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Ownership & Pet-Humanization

Youthful urban households are choosing pets over larger families, turning sterilization into a routine wellness milestone rather than a one-off public-health duty. China’s pet economy touched billions in 2024, with veterinary spending at 28%, while India’s dog population almost tripled over the last decade, pushing corporate entrants to scale multi-clinic networks. Higher disposable incomes drive owner willingness to select laparoscopic techniques, laser surgery, and longer-acting analgesics, raising average invoice values and lifting profitability across the spay and neuter market.

Government & NGO Subsidized Spay-Neuter Campaigns

Voucher programs, free-day clinics, and traveling surgical units have become critical volume drivers, particularly for low-income zip codes. Best Friends Animal Society's #SpayTogether initiative has deployed over USD 2 million in funding with the goal of supporting 50,000 spay/neuter surgeries across eight US states, while the organization directly performed 20,673 spay/neuter procedures in 2024[1]. These initiatives also generate predictable case loads that underpin capacity-expansion investments by private practices.

Mandatory Municipal Sterilization Ordinances

Thirty-two US states require shelter adoptions to be sterilized before release, while counties such as King County, Washington, impose differential licensing fees that double for intact animals. Such statutes embed a structural floor under annual procedure volumes. In Europe, similar mandates(applied in Germany, Spain, and parts of Italy) sustain clinic throughput and have encouraged mobile units to schedule recurring routes in suburban and rural districts.

Rising Veterinary Healthcare Expenditure

Average household spending on companion-animal medical care surpassed USD 1,732 in the United States during 2024, with sterilization now bundled into “silver” or “gold” wellness packages at corporate chains such as Banfield Pet Hospital. Value-based pricing and extended credit options have increased client uptake of pre-operative bloodwork, IV-fluid therapy, and post-operative analgesia, raising both ticket size and perceived quality. Similar dynamics play out in the United Kingdom and Australia, where pet-insurance riders reimburse elective surgeries, pushing premium procedure adoption and fortifying the spay and neuter market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled veterinary surgeons (rural) | -0.9% | Global; acute in rural North America & Europe | Medium term (2-4 years) |

| Cultural & religious opposition to sterilization | -0.5% | Asia-Pacific, Middle East, selective global regions | Long term (≥ 4 years) |

| Post-operative complication concerns among owners | -0.3% | Global; higher in developing markets | Short term (≤ 2 years) |

| COVID-19 backlog delaying elective procedures | -0.4% | Global; recovery phase ongoing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Veterinary Surgeons (Rural)

Shelter surveys show 73% of facilities delaying surgeries because of veterinarian shortages, with 18,648 animals on waiting lists as of 2024. Economic disincentives and lifestyle preferences steer new graduates toward urban posts, creating “veterinary deserts” where travel distances inflate owner drop-off rates. Europe reports 78.5% of its rural areas under-served, compelling NGOs to deploy mobile teams and tele-mentoring to preserve procedure volumes[2]Source: NVA Communications, “EQT to Acquire VetPartners,” nva.com.

Cultural & Religious Opposition to Sterilization

Thailand’s semi-owned dog population posts sterilization rates below 20%, influenced by Buddhist beliefs framing neutering as interference with karma. In Nordic nations, a traditional view of intact dogs remains prevalent, while nuanced interpretations of Islamic jurisprudence influence attitudes across the Middle East. These sensibilities dampen uptake, forcing campaigns to focus on education and voluntary compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Surgical Dominance Faces Innovation Pressure

Spay surgeries represented 56.08% of the spay and neuter market size in 2025, reflecting higher pricing for ovariohysterectomies and longer theater time. Neuter procedures contribute steady volume but lower revenue per case, enabling high-throughput clinics to balance margins. Surgical protocols are standardized across corporate chains, allowing predictable inventory management and consistent quality in the spay and neuter market.

Non-surgical alternatives account for a small but rapidly growing share, propelled by Suprelorin implants that provide 6-12 months of reversible infertility with 99% efficacy in field trials. Pipeline innovations in immunocontraceptive vaccines promise single-visit solutions appealing to owners concerned about anesthesia risk. As these options scale, surgical dominance may erode, prompting practices to diversify service menus and retrain staff—yet the spay and neuter market is expected to keep surgical services at its core through 2031.

By Animal Type: Canine Leadership with Feline Growth Acceleration

Dogs held 64.62% of the overall revenue in 2025, reflecting larger body size, higher anesthesia dosages, and owner preference for bundled upgrades such as laser incision and extended pain control. Large-breed spays can cost 2.2× more than a feline ovariohysterectomy, anchoring margins for full-service hospitals and specialty chains.

Cats, however, are forecast to grow at 6.05% CAGR, buoyed by municipal TNR grants that underwrite high-volume sterilization days and by rising urban adoption rates of companion cats in Asia-Pacific cities. Enhanced trap designs, feral-friendly anesthesia protocols, and bulk-price suture packs collectively compress costs, keeping the spay and neuter market competitive for shelters and NGOs.

By End User: Hospital Dominance Challenged by Mobile Innovation

Veterinary hospitals commanded 53.12% of 2025 revenue, leveraging multi-disciplinary teams, advanced diagnostic suites, and in-house pharmacies to deliver integrated experiences within the spay and neuter industry. Corporate operators negotiate national drug contracts, deploy centralized HR, and run call-center scheduling that lifts utilization rates.

Mobile/community programs, expanding at a 6.92% CAGR, directly address access gaps. Best Friends’ Navajo Nation van, outfitted with two surgical tables and autoclave, performed 3,000 procedures in its inaugural year, cutting owner travel time by 80%. Municipalities and NGOs increasingly co-fund similar units, bringing the spay and neuter market to parking lots, grange halls, and tribal lands otherwise devoid of care.

Geography Analysis

North America retained 41.74% of global revenue in 2025, fortified by uniform shelter-neuter requirements across 32 states and an extensive corporate clinic footprint. Mars Petcare’s 3,000-plus locations in Banfield and VCA networks have standardized post-operative pain protocols and broadened financing options, accelerating premium uptake. Public-private voucher schemes in Texas and California further buttress procedure volumes among price-sensitive demographics.

Asia-Pacific registers the highest 7.86% CAGR, attributed to rising middle-class ownership and government incentives to reduce stray populations. China’s veterinary-school enrollment has nearly doubled since 2020, yet supply lags demand, pushing procedure prices upward and sustaining strong profitability for early entrants. In India, Mars Inc.’s stake in Crown Veterinary Services channels capital into modern surgical suites and structured internships, elevating clinical standards and advancing the spay and neuter market.

Europe maintains mature uptake supported by embedded animal-welfare legislation, although procedure growth is incremental. Germany’s federal law requiring shelter sterilization pre-adoption stabilizes demand, while Spain’s “One Health” strategy bundles sterilization subsidies with rabies-vaccination campaigns, ensuring steady clinic throughput. Latin America and the Middle East/Africa show mixed progress; urban hubs such as São Paulo and Johannesburg implement voucher programs, yet rural penetration remains modest due to clinician shortages and cultural hesitancy.

Competitive Landscape

The spay and neuter market displays moderate concentration: the top five corporate chains control an estimated half of US companion-animal revenue.. Mission Veterinary Partners’ pending merger with Southern Veterinary Partners will create a 730-hospital entity, magnifying purchasing power and data-analytics reach. Mars Petcare retains the lead with roughly 45% share of US corporate outlets, integrating primary, specialty, and diagnostics across Banfield, BluePearl, and VCA platforms.

Private-equity ownership fuels roll-up activity across Europe and Oceania. EQT’s acquisition of VetPartners’ 267 clinics in Australia and New Zealand earmarks capital for imaging equipment and staff education, reinforcing competitive capabilities[2]Best Friends Animal Society. "Spay/Neuter Stimulus Funding." May 1, 2025. bestfriends.org . New entrants exploit geographic white spaces: nonprofit Emancipet grows via low-fee urban clinics, while tele-scheduling startups match part-time surgeons with rural shelters on surgery days, shaving backlog wait times. Pharmaceutical players are also active: Boehringer Ingelheim’s purchase of Saiba Animal Health signals intent to integrate therapeutic vaccines into broader wellness offerings, potentially opening cross-selling channels within hospital chains.

Spay And Neuter Industry Leaders

-

Companions Spay & Neuter

-

Petco Animal Supplies, Inc.

-

Naoi Animal Hospital

-

Houston Humane Society

-

East Valley Veterinary Clinics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Chilean scientists unveiled a reversible neuter vaccine for dogs, heralding a potential paradigm shift toward single-visit, low-risk sterilization

- December 2024: Mars Inc. acquired a strategic stake in India-based Crown Veterinary Services to scale clinical capacity and training programs amid surging pet ownership

Global Spay And Neuter Market Report Scope

As per the scope of this report, spaying and neutering are birth control techniques for male and female companion animals, which also assist in a longer life cycle for them.

The spay and neuter market is segmented by species, providers, and geography. By species, the market is segmented into dogs, cats, and others. By providers, the market is segmented into veterinary hospitals and veterinary clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.

| Spay (Ovariohysterectomy) |

| Neuter (Orchiectomy) |

| Non-surgical Sterilization |

| Dogs |

| Cats |

| Other Companion Animals |

| Veterinary Hospitals |

| Veterinary Clinics |

| Animal Shelters & NGOs |

| Mobile / Community Programs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| APAC | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Procedure Type | Spay (Ovariohysterectomy) | |

| Neuter (Orchiectomy) | ||

| Non-surgical Sterilization | ||

| By Animal Type | Dogs | |

| Cats | ||

| Other Companion Animals | ||

| By End User | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Animal Shelters & NGOs | ||

| Mobile / Community Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| APAC | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global value of the spay and neuter market in 2026?

The spay and neuter market size is valued at USD 2.83 billion in 2026 and is projected to reach USD 3.54 billion by 2031.

Which region holds the largest share of the spay and neuter market?

North America leads with 41.74% market share due to mature legislation and dense clinic networks.

Which procedure type grows the fastest through 2031?

Non-surgical sterilization registers the highest 5.30% CAGR, driven by implants and pipeline vaccines.

Why is Asia-Pacific the fastest-growing regional market?

Rapid pet-ownership growth, rising disposable income, and new veterinary investments propel a 7.86% CAGR through 2031.

Page last updated on: