Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

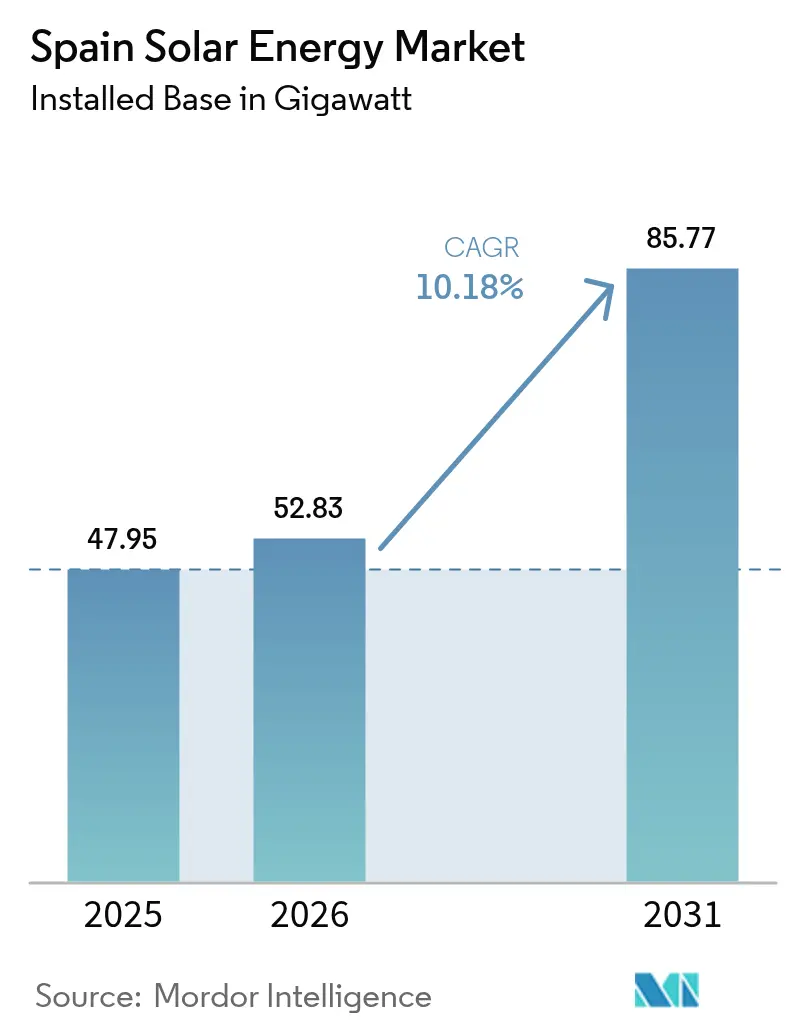

| Base Year Market Size (2025) | 47.95 gigawatt |

| Market Volume (2026) | 52.83 gigawatt |

| Market Volume (2031) | 85.77 gigawatt |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Solar Energy Market Analysis by Mordor Intelligence

The Spain Solar Energy Market size was valued at 47.95 gigawatt in 2025 and estimated to grow from 52.83 gigawatt in 2026 to reach 85.77 gigawatt by 2031, at a CAGR of 10.18% during the forecast period (2026-2031).

Rapid capacity growth already lifts solar to 21% of national electricity generation, well ahead of the European Union average, and places the country on a clear trajectory to meet its 76 GW solar PV target under the revised National Energy and Climate Plan. Declining module prices, accelerated permitting aligned with EU Fit-for-55 mandates, and strong corporate PPA appetite underpin momentum across the Spain solar energy market. Hybrid solar-and-storage configurations, especially in high-irradiance provinces, are emerging as a hedge against curtailment and price cannibalization. International developers are deepening commitments, as illustrated by TotalEnergies’ 263 MW Sevilla cluster and Plenitude’s 330 MW Renopool project, while grid congestion and Natura-2000 land constraints temper short-term volumes.

Key Report Takeaways

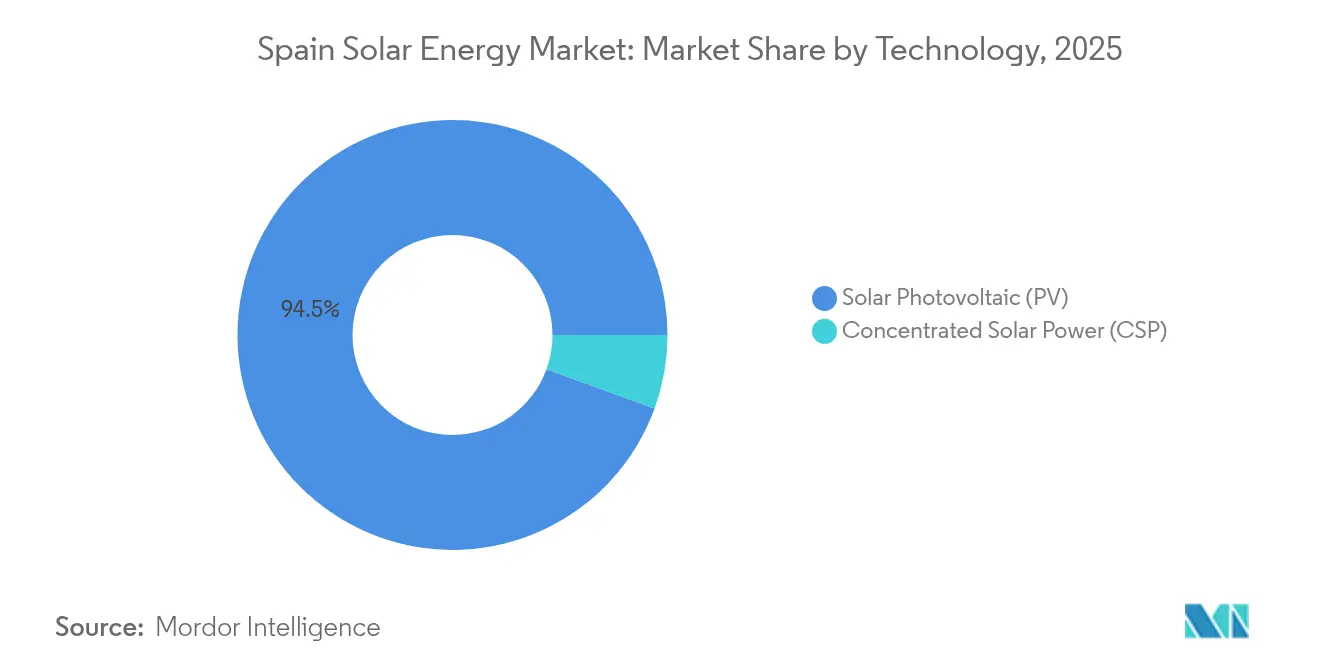

- By technology, solar photovoltaic captured 94.45% of Spain's solar energy market share in 2025, while concentrated solar power is set to grow at only 2.3% through 2031 as thermal storage loses competitiveness.

- By grid type, on-grid systems held 96.85% of the Spain solar energy market size in 2025; off-grid installations are advancing at a 34.2% CAGR to 2031, the fastest of any segment.

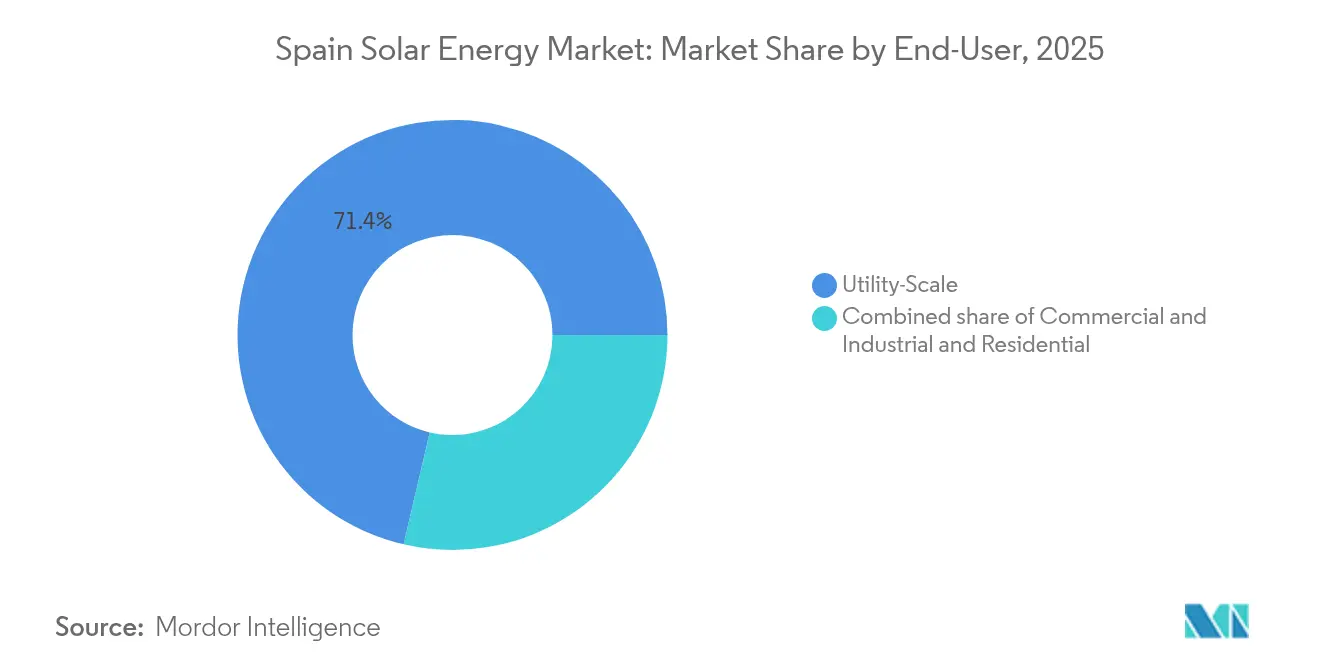

- By end user, utility-scale plants controlled 71.35% of 2025 capacity and are posting a 13.05% CAGR through 2031 as integrated utilities absorb distressed merchant assets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining cost of utility-scale PV modules | +1.8% | National, procurement clusters in Extremadura and Andalucía | Short term (≤ 2 years) |

| EU Fit-for-55 and REPowerEU deadlines | +2.1% | National, aligned with PNIEC 76 GW target | Medium term (2-4 years) |

| Corporate PPA boom among IBEX-35 firms | +1.5% | Madrid and Barcelona industrial corridors | Medium term (2-4 years) |

| Grid-connected battery hybrids | +1.2% | High-curtailment zones in Extremadura and Castilla-La Mancha | Long term (≥ 4 years) |

| Agri-PV incentives in drought regions | +0.8% | Andalucía, Castilla-La Mancha, Murcia | Medium term (2-4 years) |

| Surge in self-consumption cooperatives | +0.9% | Urban peripheries of Madrid, Valencia, Sevilla | Short term (≤ 2 years) |

| AI-optimised dispatch | +0.6% | National, early adoption by Iberdrola and Acciona | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining cost of utility-scale PV modules

Module prices continue to fall due to global oversupply, allowing projects in Castilla-La Mancha and Extremadura to reach competitive levelized costs even on lower-grade land.[1]TotalEnergies, “TotalEnergies Inaugurates Largest Solar Site in Europe,” totalenergies.com Bifacial panels paired with single-axis trackers now achieve capacity factors above 25%, widening the economic envelope for large ground-mounted plants. International utilities such as TotalEnergies cite capex savings of up to 15% compared with 2023 figures. Cost parity encourages hybridization with battery storage because freed capital can be reallocated to balance-of-system upgrades and energy management software. Local engineering firms report a notable shift toward 1,500 VDC system designs that cut cable losses and labor inputs. The net effect is an enlarged Spain solar energy market pipeline in regions previously on the economic margin.

EU Fit-for-55 & REPowerEU Compliance Deadlines

Binding 2030 decarbonization targets give developers regulatory certainty, accelerating auction participation and bankability. Spain authorized 22,326 MW of PV construction in 2024 and cleared an additional 3,019 MW in Q1 2025.[2]PV Magazine, “Spain Authorizes 3 GW of PV in Q1 2025,” pv-magazine.com Regulatory alignment extends to storage: behind-the-meter batteries now qualify for capacity revenues, improving cash flows for distributed assets. Regional authorities echo the national stance; the Junta de Andalucía fast-tracked grid interconnection for 1.4 GW of projects in 2025. Clear policy timelines minimize merchant-price risk, drawing foreign direct investment into the Spain solar energy market.

Corporate PPA Boom Among IBEX-35 Firms

Long-term power purchase agreements are now a standard risk-mitigation tool for Spanish multinationals. Iberdrola signed a 553 MW solar PPA with Burger King in 2025, while Bloomberg contracted 40 MW to supply its European data centers.[3]Iberdrola, “Burger King and Iberdrola Sign 553 MW Solar PPA,” iberdrola.com Standardized tenors, simplified credit evaluations, and competitive strike prices, often within 5% of day-ahead averages, support gigawatt-scale transaction pipelines. Bank lenders increasingly treat PPA-backed projects as quasi-utility risk. The growing corporate offtake pool broadens demand for the Spain solar energy market outside regulated auctions.

Grid-Connected Battery Hybrids Enhancing Project IRR

Spain announced 820 MW of large-scale storage for commissioning in Q4 2024. Hybrids mitigate curtailment that reached double-digit percentages in Andalucía during the March 2024 low-demand weekends. Enlight financed USD 310 million to hybridize 554 MW of wind capacity, showcasing cross-technology synergies. Storage arbitrage raises blended revenues by shifting solar output into evening peaks when prices averaged EUR 120/MWh in summer 2024. Hybrids also qualify for capacity-market premiums, further lifting internal rates of return for new entrants to the Spain solar energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-use conflicts with Natura-2000 areas | -1.3% | Extremadura, Andalucía, Castilla-La Mancha | Medium term (2-4 years) |

| Curtailment from inverter saturation | -1.8% | Cáceres, Badajoz, Ciudad Real, Murcia | Short term (≤ 2 years) |

| Day-ahead price cannibalisation | -2.2% | National high-solar hours 11:00 to 15:00 | Short term (≤ 2 years) |

| Lengthy municipal permitting for two-axis trackers | -0.9% | Small municipalities nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land-Use Conflicts with Natura-2000 Conservation Areas

Protected zones cover about 30% of Spain and trigger full environmental impact studies for any project footprint larger than 5 hectares. Murcia alone plans 30,000 ha of PV by 2030, yet 60% lies on former cropland that faces organized opposition from farm cooperatives. Developers increasingly target brownfield sites such as disused mines, adding EUR 50,000-100,000/MW in remediation costs. Concentration in low-conflict land funnels capacity into regions already constrained by weak transmission, thereby amplifying curtailment risk.

Curtailment Risk from Inverter Saturation

National curtailment averaged 10.7% in July 2025 and peaked at 43.07% at the Merida node in Badajoz. Spain’s grid upgrade plan allocates EUR 6.9 billion for 2024-2029, but most reinforcements conclude after 2027, so curtailment is unlikely to dip below 8% before then. Developers now deduct 8-12% from revenue forecasts in high-irradiance provinces, which materially lowers project NPV and encourages hybrid storage solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Photovoltaic capacity outpaces CSP as thermal storage loses ground

Solar photovoltaic commanded 94.45% of the Spain solar energy market in 2025 and is expanding at a 10.45% CAGR to 2031, whereas CSP’s PNIEC target has fallen to 4.8 GW. Lithium-ion batteries cost below USD 140/kWh in 2024 and enable two-to-four-hour storage at half the cost of molten-salt systems, so developers prioritise PV-plus-battery hybrids. Spain's solar energy market size for photovoltaic additions will therefore increase by more than 31 GW between 2025 and 2030.

CSP still offers industrial process heat at EUR 20-50/MWh, cheaper than volatile natural gas prices, and Spain hosts 2.3 GW of operating plants. Yet no new utility-scale CSP projects reached financial close in 2024. As utilities redeploy capital into bifacial PV with n-type cells that lift yield by 10-15%, CSP’s share will shrink further.

By Grid Type: Off-grid growth bypasses transmission bottlenecks

On-grid systems held 96.85% of capacity in 2025, but off-grid installations are scaling at 34.2% CAGR because they avoid curtailment penalties and grid access fees. Mining operators in Extremadura now install solar-plus-storage islands to guarantee supply during negative-price events that hurt merchant revenues. Spain's solar energy market share for off-grid systems is therefore small today, yet strategically important.

On-grid deployment continues because corporate PPAs require certified renewable output, and utility projects larger than 100 MW still achieve LCOE as low as EUR 25-30/MWh in high-irradiance provinces. However, developers in curtailment hot-spots are re-permitting stalled on-grid sites as microgrids, a sign that the grid barrier is reshaping the Spain solar energy market landscape.

By End User: Utility-scale portfolios soak up merchant volatility

Utility-scale plants accounted for 71.35% of the Spain solar energy market size in 2025 and will grow at a 13.05% CAGR because integrated utilities can diversify geographic risk across gigawatt portfolios. PPAs totaling 4.66 GW in 2024 highlight robust demand from IBEX-35 offtakers, although prices have reached record lows.

Commercial and industrial self-consumption slowed after subsidies expired, and residential additions fell 26.3% in 2024. The 5 km sharing rule set in 2025 should revive neighborhood cooperatives, yet these will still supply only a fraction of incremental demand out to 2030. As a result, the Spain solar energy market will remain dominated by utility assets that can absorb 2-3 years of sub-economic pool prices.

Geography Analysis

Regional deployment is heavily skewed toward southern provinces. Extremadura tops capacity tables with 2,842 MW of Iberdrola-operated assets. High irradiance, low land prices, and supportive regional permits create a virtuous loop that draws both domestic and foreign capital. Andalucía hosts TotalEnergies’ 263 MW Sevilla cluster, the company’s largest European solar plant, proof of global investor confidence. Castilla-La Mancha exhibits hybrid agri-PV leadership, leveraging flat terrain to blend renewable power and crop resilience.

Aragón and Castilla y León are emerging nodes due to land banks outside Natura-2000 zones, yet more complex environmental approvals slow timelines. Northern industrial regions such as the Basque Country gravitate toward rooftop and mixed-use builds; Iberdrola recently secured the area’s largest photovoltaic permit near Bilbao. Transmission congestion in the south drives incremental value for projects closer to Madrid and Barcelona load centers. Cross-zonal trading within the Iberian market mitigates some curtailment, but full benefit awaits 2028 line expansions.

Regional governments compete through incentives. The Junta de Andalucía labels large solar projects as strategic for job creation, cutting red tape to under six months. Extremadura reimburses grid-access fees for projects above 50 MW that include battery storage, sharpening cost competitiveness. Castilian provinces test agronomic partnerships with universities to scale agri-PV suited for drought resistance. Diverse policy approaches shape a multifaceted Spain solar energy market that grows in clusters rather than a uniform national wave.

Regulatory Landscape

Spain’s solar framework is anchored in the updated PNIEC 2023-2030 approved in September 2024, which sets a 76 GW solar PV target by 2030 and positions self-consumption as a named pillar, including a 19 GW self-consumption ambition within the national PV goal. Grid access and connection rules continue to evolve under the oversight of the Comisión Nacional de los Mercados y la Competencia (CNMC), including CNMC Circular 1/2024 (published October 2024) governing access and connection for demand facilities and a June 2025 CNMC resolution detailing technical specifications to determine demand access capacity on distribution networks.

For remuneration and administrative processing, MITECO updates underpin the operating environment, including the start of the 2026-2031 regulatory period on January 1, 2026 for relevant compensation parameters. In mid-2026, legislative activity focused on streamlining and sequencing authorizations, and a draft Royal Decree circulated in July 2026 proposes modifications to existing decrees on authorization procedures. The stated intent is to accelerate renewable buildout while keeping environmental compliance requirements in place.

Competitive Landscape

The Spain solar energy market shows moderate concentration. Iberdrola, Endesa, and Acciona lead domestic volume, together accounting for more than half of the operating capacity. Iberdrola earmarks EUR 15.5 billion for renewables through 2026, balancing merchant plants with long-dated PPAs. Endesa monetized part of its pipeline by selling 49.99% of select assets to Masdar for EUR 817 million while retaining operational control, illustrating capital-light scaling.

International entrants intensify rivalry. TotalEnergies, Plenitude, and Enlight finance multi-hundred-MW campuses, often bundled with storage to differentiate on grid services. Technology moves to the forefront: AI-driven dispatch, two-axis trackers, and 1,500 V architectures are competitive levers rather than pure scale. Smaller specialists such as Q-Energy and Solaria focus on mid-scale clusters and industrial rooftops, exploiting faster paybacks and lower development risk.

M&A remains active as utilities refocus on core geographies. Private equity funds hunt for de-risked yet sub-100 MW portfolios to aggregate into yield platforms. Equipment suppliers, including PV Hardware, localize tracker production to reduce logistics exposure, mirroring broader supply-chain diversification. Over 2025-2030, competitive pressure is expected to compress IRRs by 75-125 basis points, pushing players toward value-added services and hybrid assets.

Spain Solar Energy Industry Leaders

Iberdrola SA

Endesa (Enel Group)

Acciona Energía

Naturgy Renovables

Solaria Energía y Medio Ambiente SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Curtailment and grid congestion in high-irradiance nodes are creating a practical opening for hybridization and flexibility solutions. That is already showing up in how projects are being structured and contracted: Zelestra and EDP signed a PPA in June 2026 to hybridize an operational 50 MW solar plant in Caceres with a 160 MWh BESS, and Grenergy signed a 12-year financial tolling agreement in April 2026 for the battery system linked to its Escuderos solar hybrid project. Together, these deals point to a monetization pathway for storage using contracted structures rather than relying only on merchant spreads, which supports demand for integrators, EPCs, and software providers focused on energy management, dispatch optimization, and grid services.

A second opportunity is tightening evacuation and development pathways by pairing new solar with existing grid nodes and industrial infrastructure. Iberdrola’s Aceca project in Toledo received an Environmental Impact Statement approval in June 2026 and is designed to hybridize PV with an existing combined cycle plant, using established interconnection and operating footprints. On the demand side, long-duration offtake remains a driver for new build and repowering. The July 2026 Solaria and Merlin Properties agreement tied solar supply to data center demand in the Community of Madrid, combining a long-term PPA with a storage component, which signals broader corporate energy solutions that bundle generation with firming and capacity attributes aligned with PNIEC’s solar scale-up objectives.

Recent Industry Developments

- July 2026: Solaria and Merlin Properties signed a 213 MW solar supply agreement linked to data center demand in the Community of Madrid, structured around a long-term PPA and an accompanying storage arrangement. The deal highlights how hyperscale and colocation loads are driving utility-scale procurement with firming features, reinforcing the shift toward solar-plus-storage contracting.

- June 2026: Repsol and Masdar announced a transaction for Masdar to acquire a 49.99% stake in a EUR 849 million, 705 MW operational renewable portfolio in Spain. The partnership illustrates continued capital recycling into operating assets, supporting balance-sheet funding for additional solar and hybrid projects while bringing in long-term infrastructure capital.

- May 2026: Recurrent Energy inaugurated the 426 MWp Rey Solar photovoltaic plant in Carmona (Seville), which reached commercial operation in December 2025. Commissioning at this scale reinforces Andalucia’s position as a utility-scale PV hub and adds to the installed base that is increasingly shaping grid planning and flexibility needs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as solar power capacity installed in Spain, counted in gigawatts, covering new additions and the operating base across utility and distributed projects.

Scope exclusions: We exclude broader power market assets and non-solar renewables, and we do not size the full value of EPC services, financing, or grid infrastructure beyond solar-related capacity.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first structure of the model and keep assumptions aligned with how Spain tracks solar deployment. The model relied mainly on public energy and grid publications, so capacity definitions, commissioning timing, and the technology split stayed consistent year to year.

Key inputs were taken from sources such as Spain's energy ministry and official statistical releases, the national transmission operator and grid connection updates, IEA PVPS and other IEA publications, Eurostat energy balances, and IRENA renewable capacity statistics. We also reviewed company annual reports, investor presentations, and trusted industry press to monitor project pipelines, module and inverter pricing direction, and policy signals. For gap-filling, we referenced paid subscriptions that compile company financials and news, along with patent databases and shipment level trade data for directional import trends. These are illustrative examples only, and other sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how fast projects move from announcement to grid connection in Spain, and stress-testing the technology and end-user mix used in the model. We spoke with a balanced set of stakeholders across utility developers, installers, equipment suppliers, financiers, and electricity sector experts, and then checked responses for consistency across the main regions of Spain where solar build-out is concentrated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 18% | |

| Mid tier: 46% | Functional/Unit leaders: 35% | |

| Smaller Players: 20% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach in which national installed solar capacity is reconstructed from commissioning activity, grid connection signals, and official capacity publications, then split into consistent solar technology buckets for reporting. After setting that total, we used selective bottom-up checks to keep totals realistic, including sampled project counts by size band, typical capacity per project type, and cross-checks against announced and under-construction pipelines.

Inputs that shaped the model included yearly commissioned capacity (GW), grid connection and permitting progress, the shift between utility-scale and distributed systems, solar PV versus CSP mix, and the direction of equipment pricing that influences build pace and repowering decisions. For forecasting, scenario analysis was used, since policy targets, interconnection timelines, and financing conditions can change the slope of additions quickly. Where bottom-up signals were incomplete, the gap was handled through penetration and uptake rates that were validated in interviews, then applied back to the demand pool.

Data Validation & Update Cycle

Results were triangulated across multiple checkpoints, including official capacity totals, project commissioning announcements, and grid and policy milestones that can explain step changes. When large variance appeared, we reran the assumptions, then completed a peer review to ensure definitions and year cutoffs were applied consistently.

The report is refreshed annually, with interim updates when material events occur, including major policy revisions, permitting changes, or unusually large commissioning waves. Before delivery, a final review is completed so the latest public statistics and market signals are reflected in both the numbers and the narrative.

Mordor Intelligence's Spain Solar Energy Market Size Compared Against Other Published Estimates

It is common to see different published market sizes for Spain solar, mainly because some sources measure capacity while others measure revenue, and they also differ on which parts of the value chain are counted. Timing differences also matter because solar additions can be lumpy within a year, and some publishers use different cutoffs for what they treat as commissioned.

Grid-connected commissioning records and official installed capacity totals are the main checks that anchor Mordor Intelligence's 2025 estimate to operating solar capacity in Spain, which is why this report presents the market in gigawatts rather than mixing in equipment and service revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 47.95 B (2025) | |

| Regional Consultancy A | USD 13.00 B (2024) | This figure is presented as a revenue valuation, so it can include spending on equipment, installation, and related services, which is not comparable to installed capacity in GW. It may also reflect a different year cutoff and pipeline treatment for projects not yet commissioned. |

| Trade Journal B | USD 1.63 B (2024) | This estimate is scoped as photovoltaic market revenue, which typically excludes CSP and often narrows the definition to certain system types or sales channels. Differences in currency timing and assumptions on average selling prices can further compress the stated value versus broader solar definitions. |

The spread between these numbers is mostly explained by units and scope, since capacity based sizing tracks installed GW, while revenue based sizing depends on pricing and what parts of the supply chain are included. By keeping the model tied to commissioning and installed-base signals, and using interviews to adjust for pipeline conversion and rooftop uptake, the final view stays transparent and repeatable.

Key Questions Answered in the Report

How large is the Spain solar energy market in 2026?

Installed capacity reaches 52.83 GW in 2026, and the Spain solar energy market is on track to hit 85.77 GW by 2031.

What CAGR is expected for Spanish solar additions through 2031?

The Spain solar energy market is projected to expand at a 10.18% CAGR between 2026 and 2031.

Which technology leads today's capacity mix?

Photovoltaic systems hold 94.45% of installed capacity and remain the fastest-growing technology segment.

Why are battery hybrids gaining traction?

Batteries capture intraday spreads that reached EUR 150/MWh during negative-price events, boosting project IRR by several percentage points.

How severe is curtailment risk in southern Spain?

Curtailment averaged 10.7% nationally in July 2025 and exceeded 40% at the Merida node in Badajoz due to transmission congestion.

What role do corporate PPAs play?

Spain signed 4.66 GW of solar PPAs in 2024, with volume-only structures now common as offtakers accept price risk to secure renewable certificates.

Page last updated on: