Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.10 Billion |

| Market Size (2026) | USD 9.51 Billion |

| Market Size (2031) | USD 11.86 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

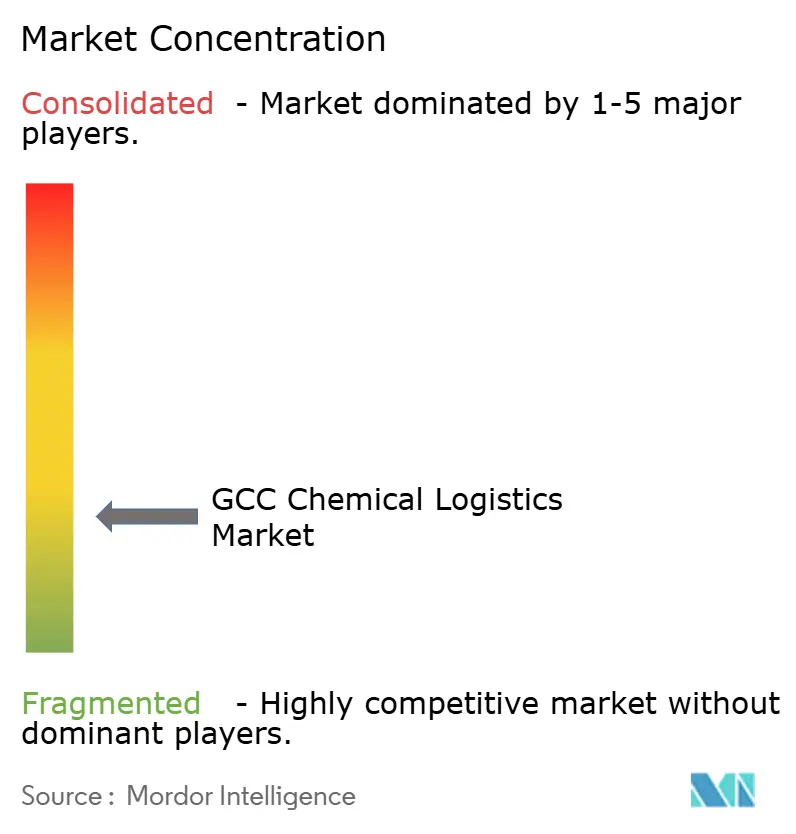

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Chemical Logistics Market Analysis by Mordor Intelligence

The GCC Chemical Logistics market size is expected to grow from USD 9.10 billion in 2025 to USD 9.51 billion in 2026 and is forecast to reach USD 11.86 billion by 2031 at 4.52% CAGR over 2026-2031.

The region’s positioning as a global petrochemical hub, combined with large‐scale capacity additions and integrated industrial zones, is stimulating long-term demand for multimodal logistics services. Continuous investment in ports, rail, and near-terminal clusters is improving connectivity, while tightening health, safety, and environmental (HSE) rules are pushing manufacturers toward specialist third-party providers. Demand for GDP-compliant cold-chain transport is accelerating as pharmaceutical imports rise, and digital platforms are gaining traction as operators pursue real-time visibility and predictive control of hazardous cargo flows. Geopolitical transit risks through the Strait of Hormuz and the Red Sea are simultaneously driving investment in alternative corridors and advanced contingency routing solutions.

Key Report Takeaways

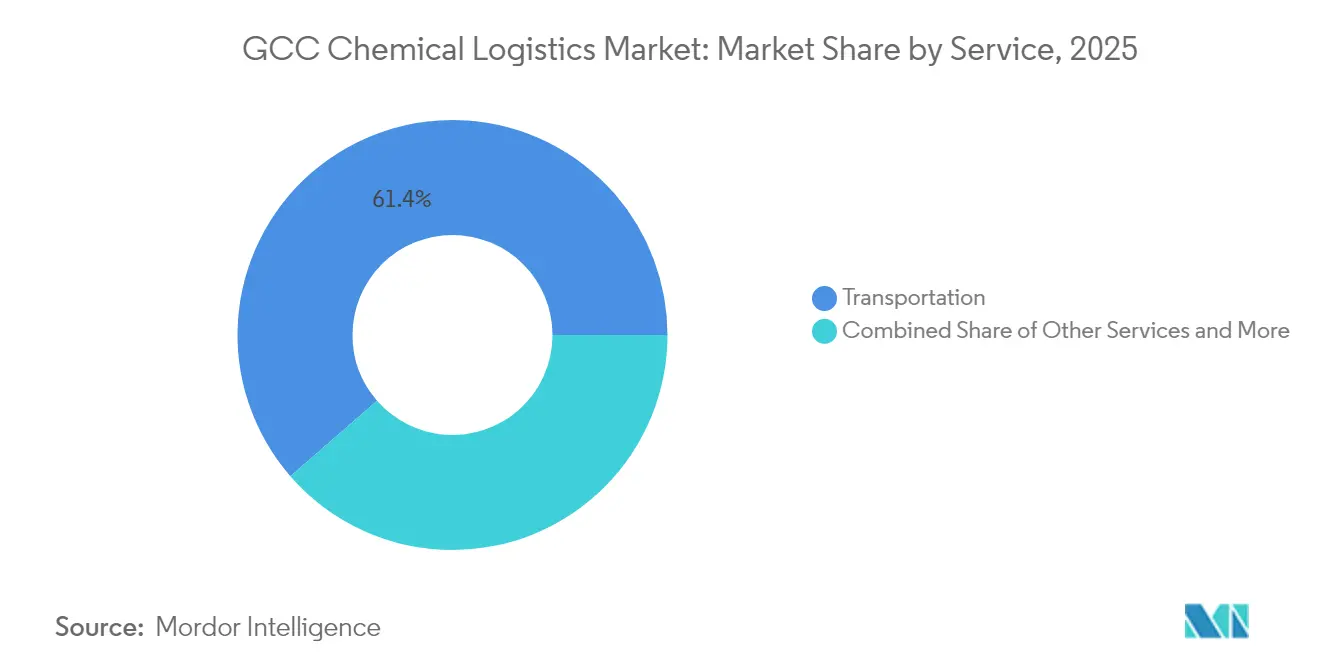

- By service, transportation commanded 61.40% of GCC chemical logistics market share in 2025, whereas warehousing, distribution, and inventory management are advancing at a 4.05% CAGR through 2031.

- By end-user industry, oil & gas held 35.60% of the GCC chemical logistics market size in 2025, while pharmaceuticals is the fastest-growing segment at a 4.70% CAGR to 2031.

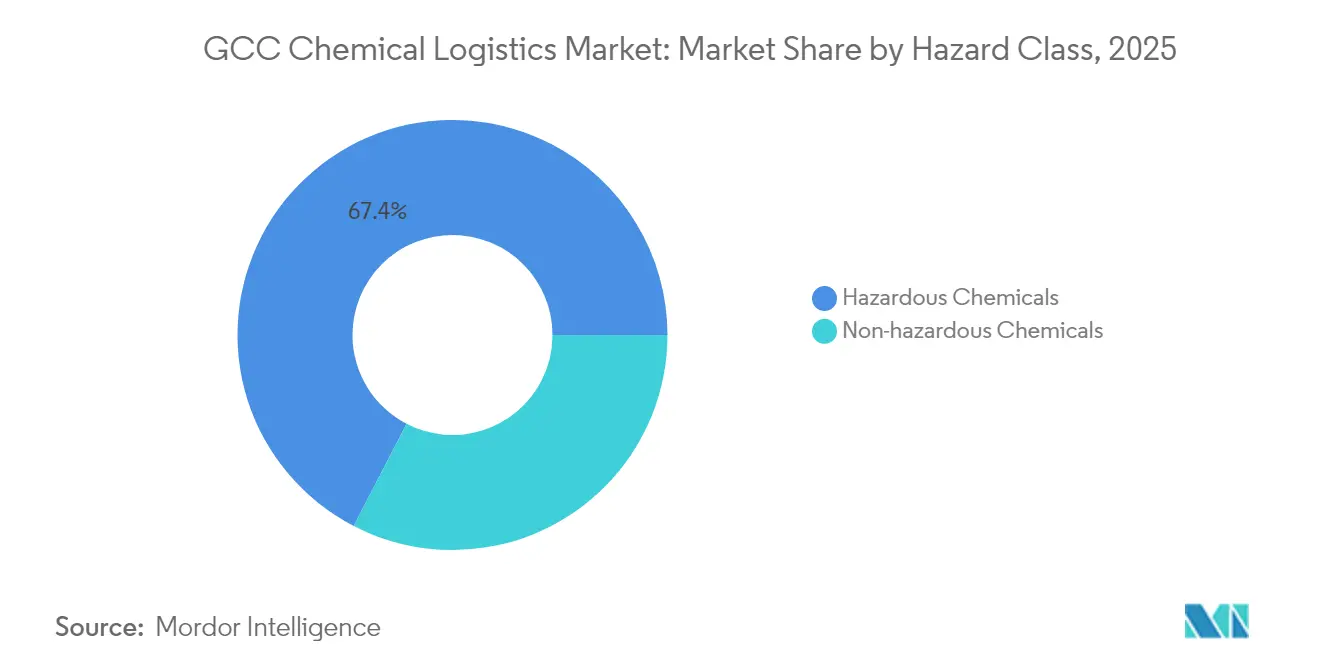

- By hazard class, hazardous chemicals captured 67.40% of the GCC chemical logistics market share in 2025; non-hazardous cargo is projected to expand at a 3.62% CAGR between 2026 and 2031.

- By temperature control, non-temperature-controlled cargo dominated with an 80.70% share in 2025 and is projected to expand at a 4.18% CAGR.

- By country, Saudi Arabia accounted for 40.70% of the GCC chemical logistics market size in 2025; the United Arab Emirates is set to rise at a 3.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Chemical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in petrochemical production capacity expansions | +1.8% | Saudi Arabia, Qatar, UAE with spillover to Kuwait, Oman | Medium term (2-4 years) |

| Massive multimodal-infrastructure investments (ports, rail & land-bridge) | +1.2% | Global GCC, concentrated in Saudi Arabia and UAE | Long term (≥ 4 years) |

| Tightening HSE regulations fuelling 3PL outsourcing | +0.9% | Global GCC with early adoption in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Booming pharma & specialty-chemical imports needing GDP-compliant transport | +0.7% | Regional, with premium demand in UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| SEZ-linked "near-terminal" chemical clusters driving onsite logistics demand | +0.5% | Saudi Arabia (Jubail, Yanbu), UAE (JAFZA), Qatar (Ras Laffan) | Long term (≥ 4 years) |

| Adoption of forward-hubbing & digital-twin control towers to bypass route shocks | +0.4% | Global GCC with technology leaders in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Petrochemical Production Capacity Expansions

Major projects such as Saudi Aramco’s USD 7.7 billion Fadhili Gas Plant expansion will raise feedstock output and create new flows for ethane, naphtha, and mixed-feed cracker derivatives[1]Gulf Cooperation Council Standardization Organization, “Draft Technical Regulation on GHS Alignment,” gso.org.sa. Growing output diversity obliges logistics providers to manage multiple hazard classes and temperature bands within the same network. Integrated complexes located at Jubail, Yanbu, and Ras Laffan require synchronized inbound feedstock and outbound product scheduling, prompting investment in specialized tank fleets, vapor-recovery terminals, and port handling systems. The resulting jump in throughput volumes underpins steady growth in the GCC chemical logistics market as producers seek assured capacity and regulatory compliance.

Massive Multimodal Infrastructure Investments

Saudi Arabia’s Logisti 2 platform and DP World’s USD 2.5 billion regional program are improving modal shifts across road, rail, and sea. New community systems cut clearance times, while inland logistics parks bring storage closer to chemical clusters. Etihad Rail is enhancing inter-emirate connectivity, and the Gulf Railway concept promises cross-border block-train services for bulk liquids. Infrastructure upgrades expand corridor choices, lower handling costs, and support the scalability required by the GCC chemical logistics market.

Tightening HSE Regulations Fueling 3PL Outsourcing

The Gulf Cooperation Council’s alignment with UN GHS Rev. 5 obliges bilingual labeling, standardized pictograms, and harmonized emergency response rules. Compliance demands certified drivers, ADR-equipped fleets, and segregated storage. Many producers lack the time or scale to internalize these requirements and are increasingly outsourcing to specialist providers equipped with digital documentation systems and 24/7 control towers. Outsourcing supports the growth trajectory of the GCC chemical logistics market and lifts service-level benchmarks.

Booming Pharma & Specialty-Chemical Imports Needing GDP-Compliant Transport

Dubai Municipality’s 2024 guidelines mandate continuous temperature monitoring from 2-8 °C and 15-25 °C for healthcare products[2]Dubai Municipality Health & Safety Department, “Technical Guidelines for Consumer Products Storage Requirements,” dm.gov.ae. WHO guidelines reinforce end-to-end risk management. These standards are enlarging the footprint of GDP-ready warehouses and dedicated reefer fleets, fueling premium-rate demand and driving a distinct cold-chain sub-segment within the GCC chemical logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for ADR-compliant fleets & warehouses | -1.1% | Global GCC with acute impact in Saudi Arabia and UAE | Medium term (2-4 years) |

| Geopolitical choke-points increasing transit-time risk | -0.8% | Global GCC with severe exposure via Strait of Hormuz and Red Sea routes | Short term (≤ 2 years) |

| Shortage of ADR/IMO-certified labour | -0.6% | Regional, most severe in Saudi Arabia and Qatar | Long term (≥ 4 years) |

| Energy-transition volatility in bulk chemical flows | -0.4% | Global GCC with transition leaders UAE and Saudi Arabia most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for ADR-Compliant Fleets & Warehouses

Explosion-proof wiring, vapor-control systems, and specialized fire suppression raise fleet and facility costs well above general cargo benchmarks. Continuous recertification and crew training obligations add to operating expenditure and deter smaller entrants. Capital hurdles slow network expansion and temper competitive intensity in the GCC chemical logistics market.

Geopolitical Chokepoints Increasing Transit-Time Risk

More than 20% of global seaborne oil transits the Strait of Hormuz, yet bypass pipeline capacity is only 2.6 million b/d[3]U.S. Energy Information Administration, “World Oil Transit Chokepoints,” eia.gov. Red Sea diversions around the Cape of Good Hope lengthen voyages by 10–14 days. Longer voyage times escalate charter rates and product inventory costs, compelling operators to maintain buffer stocks and explore alternative rail or pipeline options. This risk weighs on growth prospects in the GCC chemical logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Amid Digital Transformation

Transportation retained a 61.40% share of the GCC chemical logistics market in 2025, supported by extensive highway links from petrochemical clusters to export terminals. Road tankers remain the workhorse for regional moves, yet investments in Etihad Rail and proposed Gulf Railway corridors will gradually divert heavy bulk flows onto rail. Sea transport governs export revenue, and chemical tanker availability is a critical capacity lever. Airfreight caters to specialty and pharma cargo where transit time is critical.

Warehousing, distribution, and inventory management is the fastest-growing service at a 4.05% CAGR through 2031, buoyed by demand for digital-twin warehouses and pick-to-light systems that lift productivity. Continuous value-added services such as labeling and repackaging are also rising, reinforcing integrated solutions in the GCC chemical logistics market.

By End-User Industry: Oil & Gas Leadership with Pharmaceutical Acceleration

Oil & gas contributed 35.60% to the GCC chemical logistics market size in 2025, reflecting feedstock flows within vertically integrated complexes. Reliance on long-term contracts cushions volatility and provides stable base volumes for fleet deployment.

Pharmaceutical cargo, though smaller, is expanding at a 4.70% CAGR, propelled by regional health spending and mandatory GDP compliance. Specialty chemicals serve downstream conversion industries, and cosmetics retain a niche share yet benefit from rising disposable incomes. Diversification trends sustain demand diversity and underpin resilience in the GCC chemical logistics market.

By Hazard Class: Hazardous Cargo Challenges Dominate

Hazardous chemicals controlled 67.40% of GCC chemical logistics market share in 2025, encompassing flammable liquids, corrosives, and toxics under ADR and IMO codes. High hazard concentration necessitates specialist assets, incident response protocols, and recurring safety audits.

Non-hazardous volumes, although lower at 32.60%, include temperature-sensitive pharmaceutical ingredients, driving premium yield opportunities. Balanced growth across both classes supports network optimization and capacity utilization within the GCC chemical logistics market.

By Temperature Control: Ambient Cargo Leads, Cold Chain Grows

Non-temperature-controlled flows accounted for 80.70% of the GCC chemical logistics market in 2025, mirroring the dominance of petrochemical commodities moved at ambient conditions.

Temperature-controlled cargo holds 19.30% but is growing due to pharmaceutical and specialty chemical inflows that demand 2-8 °C and 15-25 °C compliance. Cold-chain investments generate higher returns but require robust monitoring and validated processes, reinforcing barriers to entry and service differentiation across the GCC chemical logistics industry.

Geography Analysis

Saudi Arabia held 40.70% of the GCC chemical logistics market in 2025, anchored by integrated hubs at Jubail and Yanbu, which generate dense inbound and outbound flows. The USD 240 million Jeddah Logistics Park and multiple Special Economic Zones are broadening multimodal corridors and attracting foreign logistics operators. Vast domestic demand, coupled with upcoming green-hydrogen and ammonia projects, will widen service needs and sustain investment momentum in the GCC chemical logistics market.

The United Arab Emirates is the fastest-growing geography, advancing at a 3.95% CAGR to 2031. Jebel Ali Free Zone and Khalifa Port offer state-of-the-art tank farms, ADR warehouses, and automated clearance systems that reduce dwell time and attract re-export business. Tristar Group’s purchase of a Shell Chemicals terminal expanded capacity by 5,505 CBM and illustrates the ongoing private-sector commitment. The UAE’s position as an airfreight and transshipment hub amplifies its importance within the GCC chemical logistics market.

Competitive Landscape

The GCC chemical logistics market is moderately fragmented but trending toward consolidation. DHL Supply Chain and Saudi Aramco’s ASMO platform aggregates procurement and logistics spend across the energy value chain, creating a multi-billion-dollar buyer with negotiating leverage on assets and technology. CEVA Logistics and Almajdouie’s joint venture combines 2,000 assets and extensive local facilities, elevating service scale and geographic reach.

Strategic emphasis has shifted toward digital twins, control-tower visibility, and AI-assisted routing that anticipates port congestion and weather disruptions. Operators are also investing in cryogenic tanks and ISO containers designed for liquid hydrogen and ammonia, anticipating future export corridors.

White-space opportunities exist in pharma cold chain, onsite SEZ logistics, and last-mile hazardous waste retrieval, where current capacity is limited. Regional specialists such as RSA-TALKE, Den Hartogh, and Bahri Logistics defend market share through niche fleet configurations and local knowledge, while global players bring standardized processes and broader service portfolios. The resulting mix enriches the competitive dynamics of the GCC chemical logistics market.

GCC Chemical Logistics Industry Leaders

Al-Futtaim Logistics

RSA-TALKE

BDP International (PSA BDP)

Bahri Logistics

Kanoo Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DHL announced a EUR 500 million (USD 520 million) allocation for new gateways, warehouses, and fleet upgrades across Saudi Arabia and the UAE.

- April 2025: DSV agreed to buy Schenker for EUR 14.3 billion (USD 14.9 billion), boosting regional capacity and automotive sector coverage.

- November 2024: Gulf Warehousing Company and GFH Financial Group signed heads of terms to build 200,000 m² of grade-A facilities in Riyadh, Jeddah, and Dammam.

- October 2024: CEVA Logistics and Almajdouie finalized a joint venture that forms one of the largest integrated logistics platforms in Saudi Arabia.

GCC Chemical Logistics Market Report Scope

Chemical logistics comprises the transportation of products, many of which require special care in handling and storing to prevent safety hazards such as combustion, contamination, and spoilage.

The GCC chemical logistics market covers the growing trends, a complete background analysis of the chemical logistics market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and logistics spending by the end-user industries, and the impact of COVID - 19 on the market.

The GCC chemical logistics market is segmented by service (transportation, warehousing, distribution, and inventory management, and other value-added services), end user (pharmaceutical industry, cosmetic industry, oil and gas industry, specialty chemicals industry, and other end users), and geography (United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Oman, and Bahrain).

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing, Distribution & Inventory Management | |

| Other Services |

By End-User Industry

| Pharmaceutical |

| Cosmetic |

| Oil & Gas |

| Specialty Chemicals |

| Other End-Users |

By Hazard Class

| Hazardous Chemicals |

| Non-hazardous Chemicals |

By Temperature Control

| Temperature-Controlled (Refrigerated/Heated) |

| Non-Temperature-Controlled |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing, Distribution & Inventory Management | ||

| Other Services | ||

| By End-User Industry | Pharmaceutical | |

| Cosmetic | ||

| Oil & Gas | ||

| Specialty Chemicals | ||

| Other End-Users | ||

| By Hazard Class | Hazardous Chemicals | |

| Non-hazardous Chemicals | ||

| By Temperature Control | Temperature-Controlled (Refrigerated/Heated) | |

| Non-Temperature-Controlled | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Oman |

Key Questions Answered in the Report

What is the projected value of the GCC chemical logistics market by 2031?

The GCC chemical logistics market is forecast to reach USD 11.86 billion by 2031, growing at a 4.52% CAGR.

Which service segment is growing fastest within GCC chemical logistics?

Warehousing, distribution, and inventory management is expanding at a 4.05% CAGR through 2031 due to rising demand for value-added and digital-twin services.

How much market share does Saudi Arabia hold in GCC chemical logistics?

Saudi Arabia accounted for 40.70% of the GCC chemical logistics market in 2025, anchored by integrated petrochemical hubs.

Why is pharmaceutical logistics gaining traction in the GCC?

Stringent GDP rules and rising healthcare spending are driving a 4.70% CAGR in pharma cargo, boosting demand for temperature-controlled transport and storage.

What are the key risks affecting chemical cargo transit in the region?

Geopolitical chokepoints at the Strait of Hormuz and the Red Sea elevate transit-time risk and prompt contingency routing and buffer inventories.

Which technology trends are shaping competitive advantage?

Digital twins, real-time control towers, and cryogenic handling systems for emerging hydrogen and ammonia cargoes are differentiating leading providers.

Page last updated on: