Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

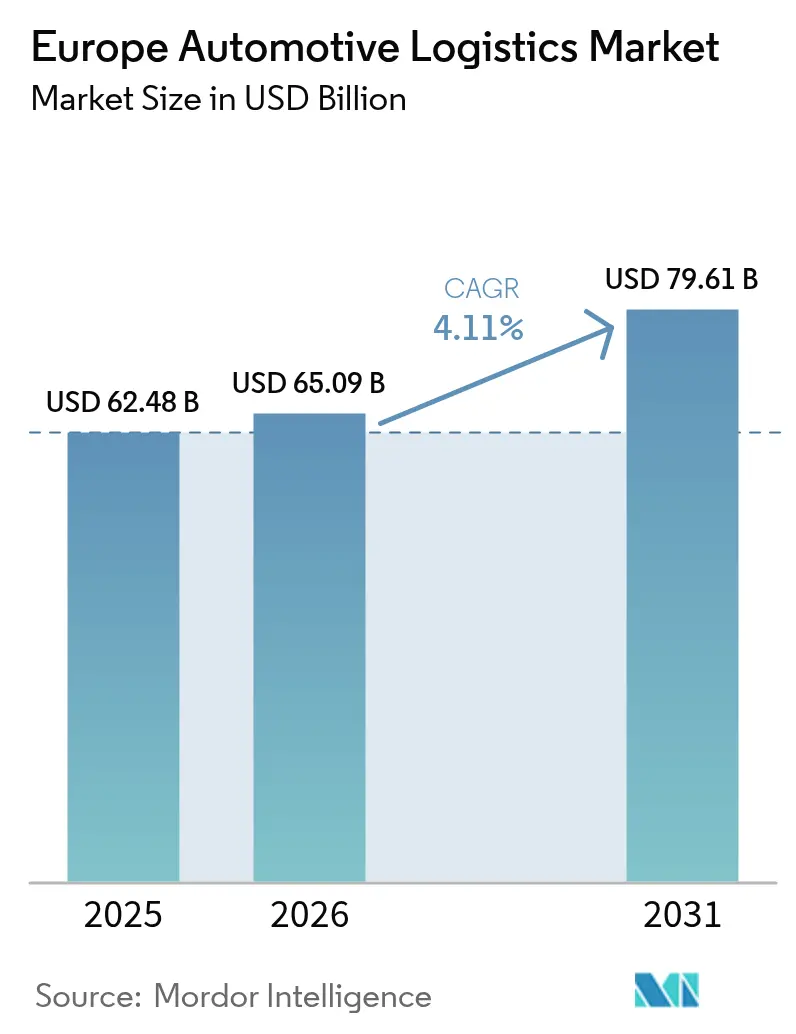

| Base Year Market Size (2025) | USD 62.48 Billion |

| Market Size (2026) | USD 65.09 Billion |

| Market Size (2031) | USD 79.61 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Logistics Market Analysis by Mordor Intelligence

The Europe automotive logistics market size is projected to be USD 62.48 billion in 2025, USD 65.09 billion in 2026, and reach USD 79.61 billion by 2031, growing at a CAGR of 4.11% from 2026 to 2031.

On-shoring incentives created by the EU Carbon Border Adjustment Mechanism, coupled with mandatory Battery Passport rules, are re-routing material flows toward regional suppliers, lifting intra-European freight demand and intensifying pressure on road capacity. Large-scale autonomous-truck pilots along Trans-European Transport Network corridors promise round-the-clock operations but require interoperable digital infrastructure that is still unevenly deployed. Gigafactory clusters in Spain, Italy, and Portugal are generating bulk inbound flows of lithium, cobalt, and manganese, while reverse-logistics loops for end-of-life batteries are opening an entirely new service niche for providers with ADR-certified drivers. Escalating insurance premiums linked to thermal-runaway fire risks squeeze margins, favoring logistics groups with scale to absorb higher compliance costs.

Key Report Takeaways

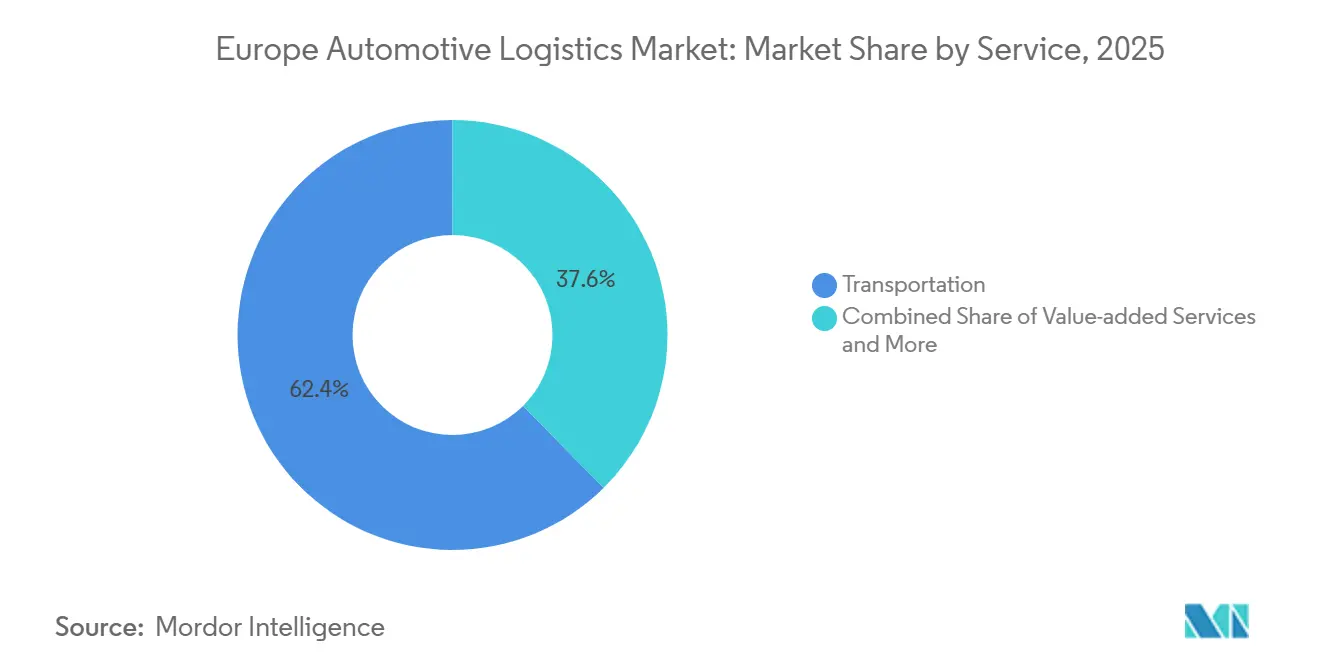

- By service, transportation services led with 62.43% of Europe automotive logistics market share in 2025; value-added services are advancing at a 4.2% CAGR through 2031.

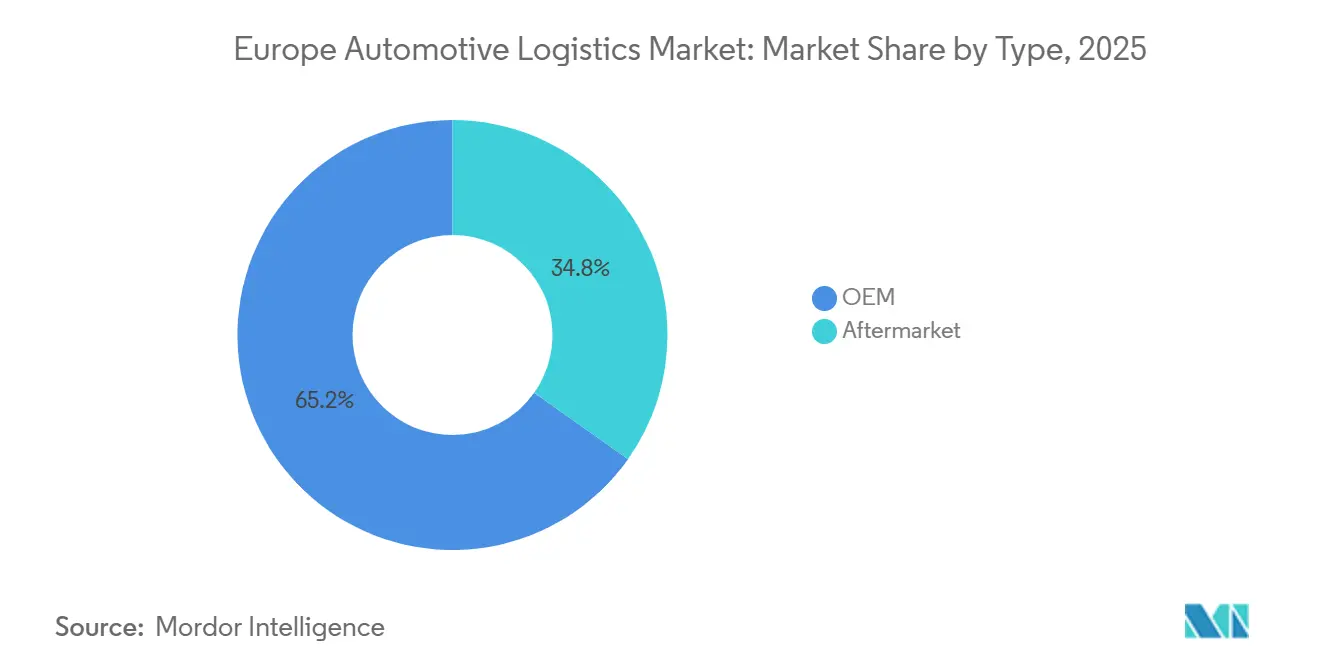

- By type, OEM logistics accounted for 65.2% of the Europe automotive logistics market size in 2025, while aftermarket logistics is expanding at a 4.4% CAGR to 2031.

- By cargo, finished vehicles held 61.3% of Europe automotive logistics market share in 2025; EV batteries and power-electronics are the fastest-growing cargo group at a 4.8%.

- By country, Germany captured 24.3% of the Europe automotive logistics market size in 2025, whereas Poland records the strongest growth with a 4.6% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| On-shoring and friend-shoring of Tier-1/2 component production boosting intra-Europe freight flows | +0.9% | Germany, Poland, Czech Republic | Medium term (2–4 years) |

| EU Carbon Border Adjustment Mechanism accelerating regional supply-chain realignment | +0.7% | EU-27 automotive hubs | Short term (≤ 2 years) |

| Large-scale autonomous truck pilots enabling 24/7 long-haul corridors | +0.5% | Germany, Netherlands, Belgium | Long term (≥ 4 years) |

| Gigafactory megaparks in Southern Europe triggering raw-material and battery-cell freight flows | +0.8% | Spain, Italy, Portugal | Medium term (2–4 years) |

| Mandatory EU Battery Passport regulations creating end-of-life reverse loops | +0.4% | EU-27 early adopters | Long term (≥ 4 years) |

| Deployment of hydrogen-powered heavy-duty fleets spurring green-corridor investments | +0.3% | Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

On-Shoring and Friend-Shoring of Tier-1/2 Component Production Boosting Intra-Europe Freight Flows

Suppliers are relocating manufacturing lines from Asia to Central and Eastern Europe to mitigate geopolitical risk and shorten lead times, a shift that multiplies cross-border truckloads and raises demand for just-in-sequence distribution. Poland and the Czech Republic are securing record foreign direct investment commitments, feeding dense road and intermodal flows into German, Spanish, and French assembly plants. Logistics providers with synchronized multi-modal networks capture share by combining road flexibility with rail speed on high-volume lanes. The trend also elevates the role of regional consolidation hubs that pool parts from multiple suppliers for onward distribution. Higher intra-EU volumes reinforce the strategic value of customs-free borders, yet they strain road capacity and warehouse space in border regions[1]“Carbon Border Adjustment Mechanism,” European Commission, EC.EUROPA.EU .

EU Carbon Border Adjustment Mechanism Accelerating Regional Supply-Chain Realignment

Full carbon tariffs on high-emission imports from 2026 force OEMs to re-source steel and aluminum locally, amplifying demand for certified low-carbon transport lanes. Embedded-emission reporting requirements trigger investment in digital twins that trace shipments from mill to plant, placing a premium on providers with carbon-accounting platforms. The mechanism narrows delivered-cost gaps between European and overseas suppliers, tilting freight flows toward shorter intra-regional hauls. Providers offering intermodal solutions with renewable power traction gain pricing power as OEMs jockey to cut visible Scope 3 emissions. Early adopters have begun bundling emissions data with freight invoices, a service feature likely to become standard as CBAM enforcement tightens[2]“Trans-European Transport Network,” European Commission, EC.EUROPA.EU.

Large-Scale Autonomous Truck Pilots Enabling 24/7 Long-Haul Corridors Across TEN-T Routes

Pilot convoys running Level 4 trucks on the A9 digital test bed in Germany and the Rotterdam–Venlo corridor in the Netherlands show transit-time reductions of 18% versus human-driven operations. Continuous vehicle utilization lowers unit operating cost, yet scaling remains gated by harmonized cross-border driver-out legislation and a shortage of robotics technicians. Early mover fleets enjoy priority access to scarce testing slots, locking in experiential advantages as EU regulators finalize common safety standards. OEMs view autonomy as a hedge against chronic driver deficits, pushing logistics partners to demonstrate near-term roadmaps for autonomous capability. Once nationwide maps, V2X connectivity, and automated yard systems align, autonomous corridors could shift long-haul modal balances away from rail on selected high-density lanes.

Gigafactory Megaparks in Southern Europe Triggering Bulk Raw-Material and Battery-Cell Freight Flows

Battery plants in Valencia, Sagunto, and Turin collectively exceed 200 GWh of announced capacity, generating inbound bulk volumes of spodumene, nickel sulphate, and graphite that move from Mediterranean ports to inland parks. Outbound, temperature-controlled containers shuttle pouch and cylindrical cells to final-assembly lines in Germany and France, requiring dwell times under forty-eight hours. These flows reverse the traditional north-south component gradient and spur investment in specialized container depots, fire-safe interim storage, and sensor-fitted trailers. Spanish ports leverage proximity to North African lithium sources to position themselves as preferred gateways. As production ramps up, additional inland intermodal terminals are slated for upgrade to ADR Class 9 compliance, broadening network redundancy for hazardous cargo routing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented rail interoperability and limited cross-border slots | -0.6% | Germany-Poland, France-Spain borders | Short term (≤ 2 years) |

| Acute shortage of ADR-certified drivers for lithium-ion battery lanes | -0.5% | Germany, France, Poland | Medium term (2–4 years) |

| Shortage of autonomous-systems technicians delaying warehouse automation | -0.3% | Germany, Netherlands, United Kingdom | Long term (≥ 4 years) |

| Escalating insurance premiums for EV-battery freight | -0.4% | High-volume battery corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Rail Interoperability and Limited Cross-Border Slots Constraining Modal-Shift Targets

National signaling systems, divergent electrification voltages, and crew licensing rules force locomotives to change at borders, adding average dwell times of two hours per crossing. Passenger service priority further compresses freight windows, throttling rail capacity on high-volume Germany-Poland and France-Spain sections. Automotive shippers need predictable arrival times, therefore keep critical components on trucks despite sustainability targets. Infrastructure upgrades under the ERTMS program are behind schedule, leaving 46% of core corridors without full deployment. Until harmonization accelerates, rail will struggle to capture a larger share of component traffic[3]“Rail freight transport in the EU: still not on the right track,” European Court of Auditors, ECA.EUROPA.EU .

Acute Shortage of ADR-Certified Drivers for Lithium-Ion Battery Transport Lanes

Class 9 dangerous-goods permits cover less than 14% of the EU driver pool, and annual training throughput cannot match the surge in battery-cell tonnage. Wage premiums have risen above 18% compared with general cargo, inflating cost per lane-meter on critical Valencia–Stuttgart and Breslau–Leipzig lines. OEMs lean on integrated providers that can rotate scarce certified drivers across networks to protect service levels. Some carriers test convoy models pairing one certified lead driver with autonomous follower trucks, yet legal frameworks remain provisional. Persistent undersupply risks capacity crunches as gigafactories reach design output after 2027[4]“ADR 2023 European Agreement,” UNECE, UNECE.ORG .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Outpace Core Transport

Transportation retained 62.43% of Europe automotive logistics market share in 2025 as road freight underpinned just-in-time production schedules. Yet value-added services are growing at a 4.2% CAGR because OEMs outsource battery preconditioning, vehicle software flashing, and reverse-logistics orchestration. Road remains indispensable for high-frequency feeder runs linking parts makers and assembly plants, while rail’s modal share stalls amid interoperability snags. Short-sea and Ro-Ro carriers clear finished vehicles into the United Kingdom and Nordic markets, but vessel capacity constraints at Zeebrugge and Bremerhaven periodically delay sailings. Warehousing demand climbs as spare-part e-commerce pushes fulfillment centers to hold wider SKU ranges closer to end users.

Digitally managed 4PL contracts combine transport, storage, and repair services under outcome-based pricing that rewards delivery performance. Automation projects focus on high-volume cross-dock hubs where robotic pallet movers cut cycle times. Europe Automotive Logistics market size gains also stem from OEM mandates for ISO 14001-certified providers who can evidence carbon-footprint reduction. KPI dashboards integrating telematics and warehouse management systems enable real-time root-cause analysis of network delays. Value-added offerings like digital battery diagnostics and line-side kitting now represent up to 15% of contract value on new tenders, signaling a structural margin uplift for providers able to scale them.

By Type: Aftermarket Acceleration Challenges OEM Dominance

OEM flows occupied 65.2% of Europe automotive logistics market size in 2025, thanks to Europe’s dense vehicle manufacturing footprint. Production networks grow more complex as battery, inverter, and software modules move in parallel to traditional power-train parts. Gigafactory logistics introduces bulk powders and cell shipments that require climate control and ADR oversight, all embedded within the OEM contract scope. Despite scale advantages, OEMs pressure providers for cost relief as they fund electrification capex, compressing margins.

Aftermarket logistics is expanding at a 4.4% CAGR through 2031 in step with rising vehicle age and e-commerce penetration. Direct-to-consumer parcels for maintenance parts balloon urban delivery density, pushing 3PLs to deploy micro-fulfillment nodes near major cities. AI-driven demand forecasting improves SKU availability while holding days-on-hand flattened. Europe Automotive Logistics market share for providers with pan-regional spare-part networks should rise as distributors consolidate and seek fewer, larger partners. Battery warranty returns also flow through aftermarket channels, adding hazardous-goods complexity to a segment once dominated by relatively straightforward pallet moves.

By Cargo Type: Battery Logistics Reshapes Traditional Flows

Finished vehicles accounted for 61.3% of Europe automotive logistics market share in 2025, supported by entrenched Ro-Ro networks and rail auto-racks moving high volumes across Germany, France, and Spain. However, EV batteries and power electronics are registering a 4.8% CAGR, outpacing all other categories. Temperature-controlled reefers fitted with continuous data loggers maintain cell integrity within 15-25 °C on Valencia–Wolfsburg shuttles. Chain-of-custody records feed directly into Battery Passports to prove recycled-content quotas, integrating transport into compliance workflows.

Component flows remain steady as OEMs re-nearshore Tier-2 supply, shortening lead times but increasing shipment frequency. Airfreight is reserved for high-value semiconductors when chip shortages jeopardize assembly-line uptime. Europe Automotive Logistics market size for hazardous cargo services grows as sodium-ion and solid-state chemistries enter pilot production, each bringing new packaging and certification rules. Providers investing early in multi-chemistry handling standards fortify long-term competitiveness.

Geography Analysis

Germany contributed 24.3% of Europe automotive logistics market size in 2025, anchored by Volkswagen, BMW, and Mercedes-Benz assembly clusters and the deep-sea ports of Hamburg and Bremerhaven. Its extensive Autobahn and inland-port network enables fast multimodal transfers, yet labor cost inflation and severe driver shortages cap organic growth. Federal subsidies for hydrogen corridors along the Rhine-Alpine axis support decarbonization pilots that could become procurement differentiators.

Poland posts the fastest 4.6% CAGR as Central Europe’s warehouse pipeline surpasses 3 million m² in annual completions. Special economic zones lure EV battery and e-axle producers, seeding feeder routes into German and French plants that enhance the country’s role as a supply-chain linchpin. Road infrastructure upgrades and EU Cohesion Fund rail projects improve east-west transit times, though border queues at Świecko still impair reliability during peak seasons.

Southern Europe is reshaped by Spanish and Italian gigafactory megaparks that funnel imported spodumene through Valencia and Gioia Tauro. Bulk rail from ports to inland cell plants opens south-north cargo flows that contrast with historic north-south component routes. France maintains a balanced profile combining domestic assembly, finished-vehicle exports, and a growing battery-recycling cluster in the Hauts-de-France region. The United Kingdom grapples with customs re-documentation after Brexit, motivating logistics pairs to embed on-site brokerage teams at Dover and Holyhead. BENELUX nations exploit Rotterdam and Antwerp trans-shipment strength, while Nordic markets lead on green-corridor pilots supported by generous national incentives.

Competitive Landscape

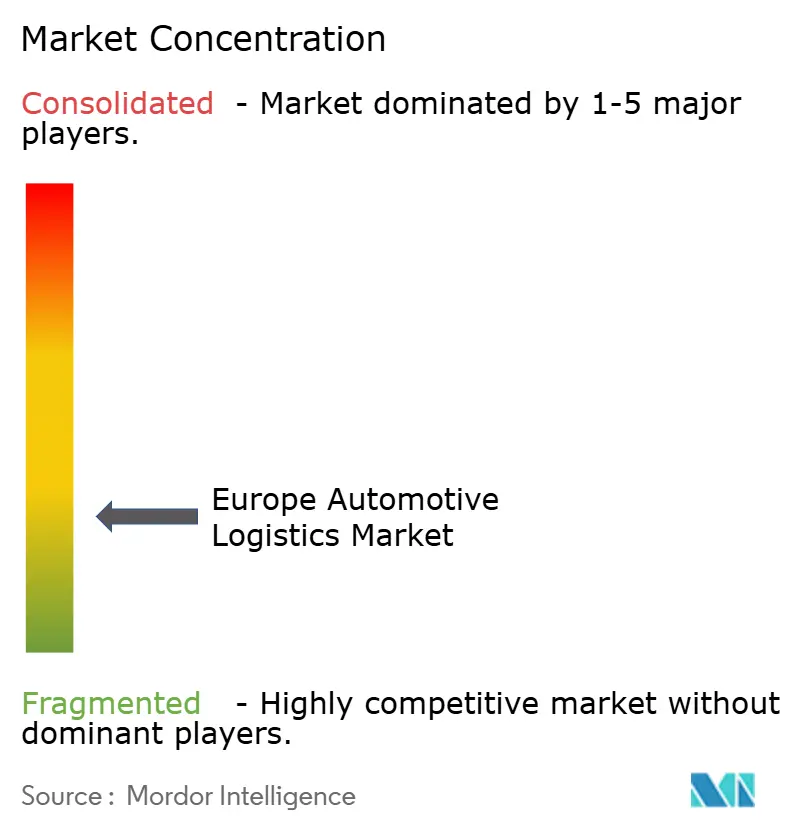

Europe Automotive Logistics market concentration sits at a moderate level, with the top five providers controlling roughly 30% of revenue. DSV’s EUR 14.3 billion (USD 15.8 billion) acquisition of DB Schenker creates a powerhouse with scale across road, rail, and contract logistics. DHL Supply Chain, Kuehne+Nagel, and GEODIS counter through aggressive investment in control-tower technology and specialized battery services. Regional specialists such as BLG Logistics and Schnellecke retain long-standing OEM relationships by offering bespoke line-feeding and in-plant sequencing.

Digital capability becomes the primary battlefield, with AI route optimization trimming empty kilometers and predictive-maintenance algorithms minimizing asset downtime. Providers race to deploy autonomous yard tractors that cut trailer dwell time, yet technician shortages slow rollouts. ADR certification portfolios and ISO 14001 credentials act as critical bid qualifiers, especially for battery logistics. Market entry barriers rise as insurance, regulatory, and data-integration requirements grow more stringent, pushing smaller carriers toward niche subcontracting roles under 4PL umbrellas.

Scale players diversify into reverse logistics and aftermarket fulfillment to capture growth beyond core production flows. Integrated offerings bundle transport with repair, refurbishment, and recycling services, locking customers into multi-year agreements. Financial strength also helps incumbents absorb spiking insurance premiums, a competitive buffer absent in fragmented segments. Consolidation is expected to continue as smaller firms struggle with compliance cost and digital-investment thresholds.

Europe Automotive Logistics Industry Leaders

BLG Logistics

Schnellecke Logistics

GEODIS

DSV A/S

CMA CGM Group (Including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: GXO Logistics was selected by BMW Group to manage car-parts warehousing at Swindon, modernizing in-plant supply for MINI production.

- February 2026: DHL won a contract from NIO to manage storage, distribution, and customs clearance of parts across Northwestern Europe.

- September 2025: CEVA Logistics announced plans for up to 15 Battery Logistics Centers across 10 countries by 2027 to manage EV battery reverse flows.

- September 2025: CEVA Logistics secured a three-year contract with General Motors Europe to handle direct-to-consumer logistics for Cadillac EV models in France and Germany.

Europe Automotive Logistics Market Report Scope

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea / Ro-Ro / Short-Sea | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services |

By Type

| OEM |

| Aftermarket |

By Cargo Type

| Finished Vehicles |

| Auto Components |

| EV Batteries and Power-Electronics |

| Other Cargo |

By Country

| Germany |

| Spain |

| France |

| Italy |

| Poland |

| United Kingdom |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea / Ro-Ro / Short-Sea | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services | ||

| By Type | OEM | |

| Aftermarket | ||

| By Cargo Type | Finished Vehicles | |

| Auto Components | ||

| EV Batteries and Power-Electronics | ||

| Other Cargo | ||

| By Country | Germany | |

| Spain | ||

| France | ||

| Italy | ||

| Poland | ||

| United Kingdom | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe |

Key Questions Answered in the Report

How large will European automotive logistics spending be by 2031?

The Europe Automotive Logistics market size is forecast to reach USD 79.61 billion by 2031 under a 4.11% CAGR.

Which service category is growing the fastest in European automotive logistics?

Value-added services such as battery conditioning and digital control-tower orchestration are expanding at 4.2% CAGR between 2026 and 2031.

Why is Poland gaining share in automotive logistics?

Gigafactory investment, new warehouses, and improving east-west rail links are lifting Poland’s market value at a 4.6% CAGR, the highest in the region.

What is driving the surge in battery-related freight?

Rapid EV adoption and Southern European cell-plant buildouts are accelerating ADR-compliant, temperature-controlled battery shipments at 4.8% CAGR.

How will the EU Battery Passport regulation affect logistics providers?

Providers must offer end-to-end traceability and safe reverse-logistics loops, favoring firms with blockchain tracking, ADR expertise, and specialized storage capacity.

Which companies are leading consolidation in the sector?

DSV, DHL Supply Chain, and Kuehne+Nagel are the key consolidators, leveraging scale and digital platforms to secure large OEM contracts.

Page last updated on: