Spain Digital X-Ray Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

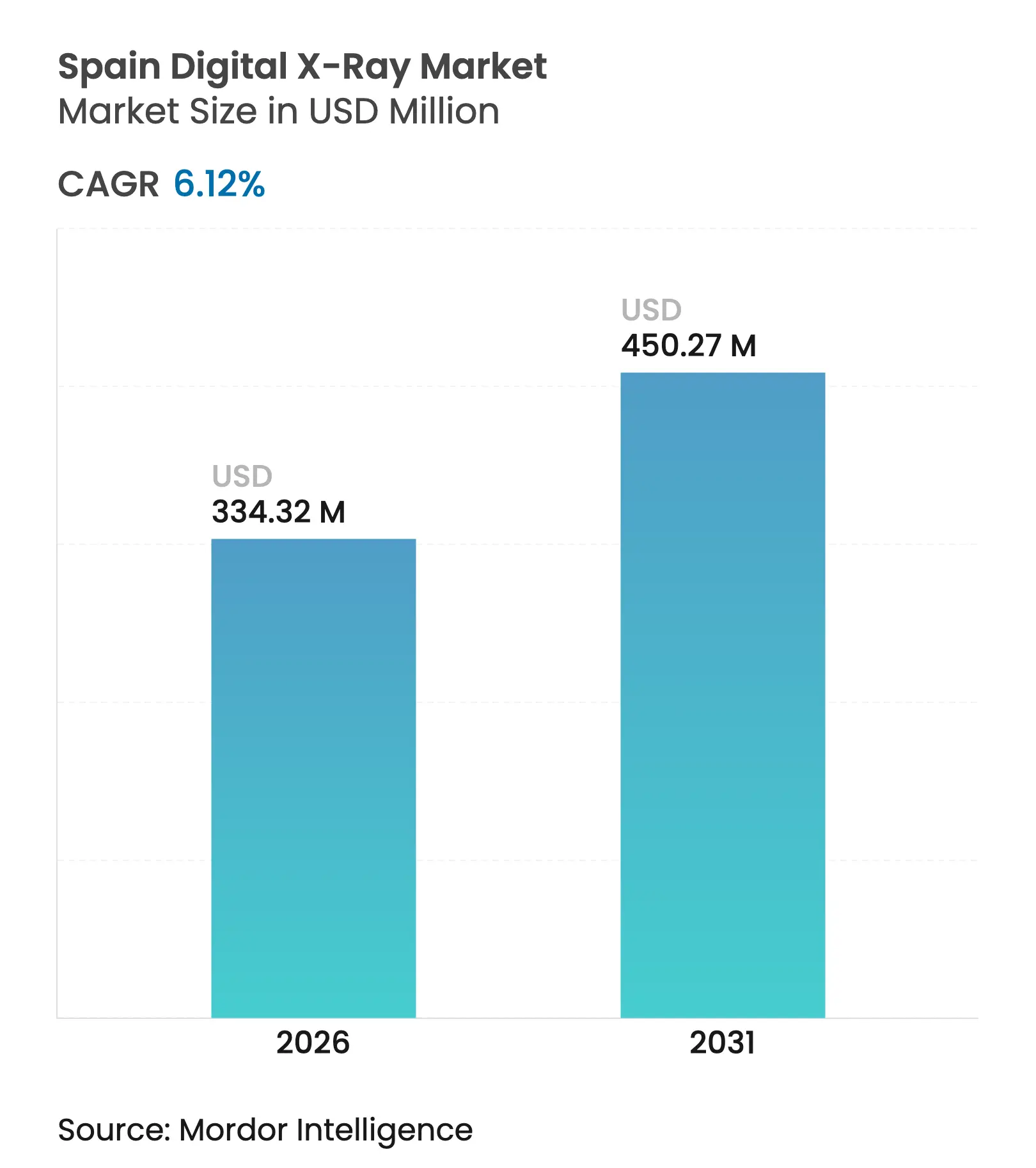

| Market Size (2026) | USD 334.32 Million |

| Market Size (2031) | USD 450.27 Million |

| Growth Rate (2026 - 2031) | 6.12 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Spain Digital X-Ray Market Analysis by Mordor Intelligence

Spain digital X-ray market size in 2026 is estimated at USD 334.32 million, growing from 2025 value of USD 315.02 million with 2031 projections showing USD 450.27 million, growing at 6.12% CAGR over 2026-2031. Demand strengthens as the PERTE Salud de Vanguardia program channels EUR 1.469 billion toward medical technology, while the National Oncology Plan expands radiology budgets and accelerates early-detection protocols. Purchasers increasingly favor cassette-less direct radiography that trims 30-40% off examination times and lowers dose exposure by up to 50%. Stable reimbursement for outpatient diagnostics supports steady replacement of film and computed radiography infrastructure, and flexible detector panels widen adoption in mobile units that serve rural communities. Competitive pressure rises as international vendors promote AI-integrated systems to offset aggressive local pricing, and hospitals prioritize platforms that mitigate workforce shortages through automated positioning and triage support.

Key Report Takeaways

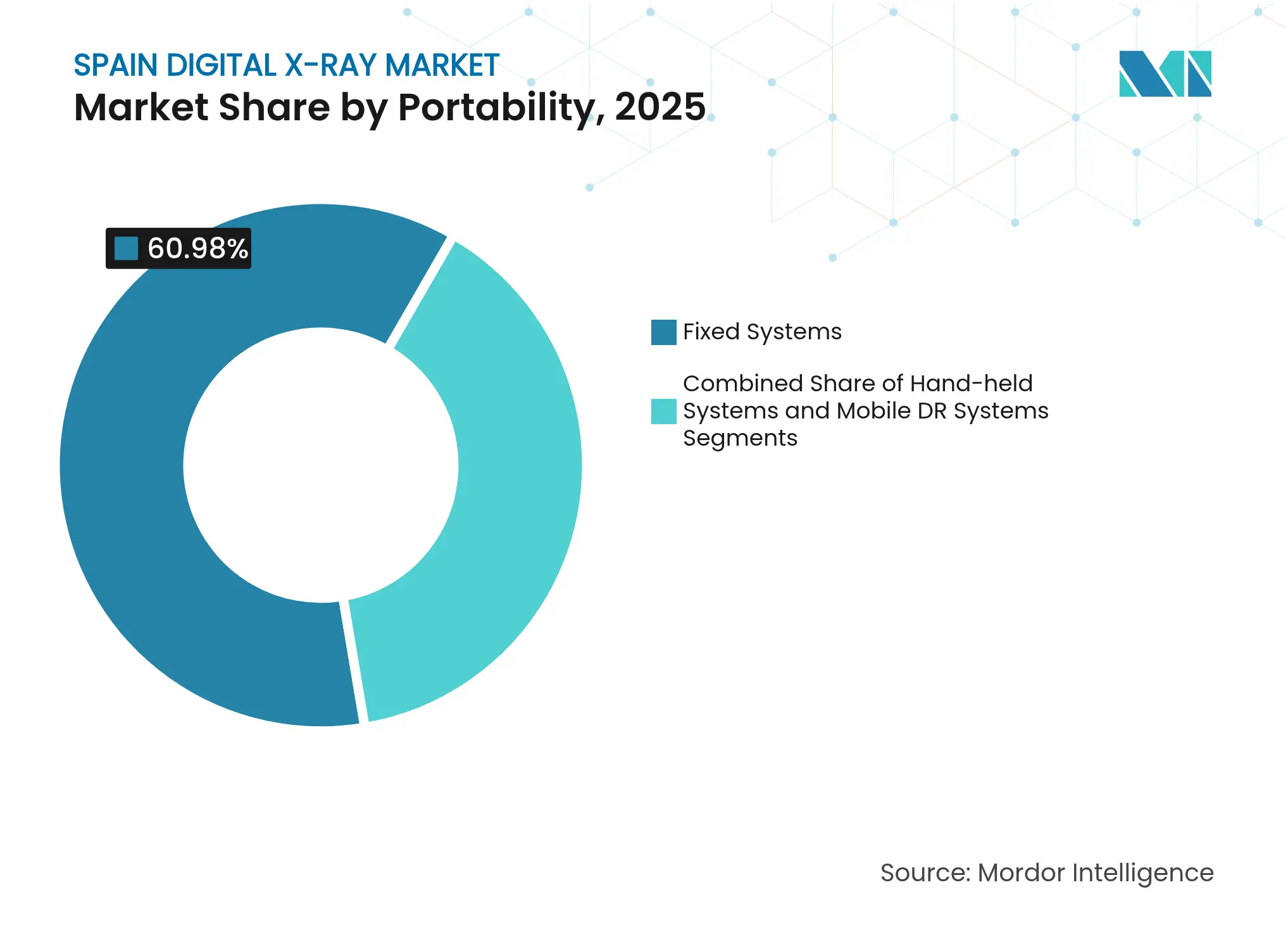

- By portability, fixed systems held 60.98% of Spain digital X-ray market share in 2025, while hand-held systems are forecast to expand at a 8.9% CAGR to 2031.

- By detector type, amorphous silicon panels accounted for 44.10% of Spain digital X-ray market share in 2025, whereas flexible panels lead growth at a 9.42% CAGR through 2031.

- By application, orthopedic imaging captured 38.21% revenue share in 2025, and chest imaging is advancing at a 9.5% CAGR between 2026 and 2031.

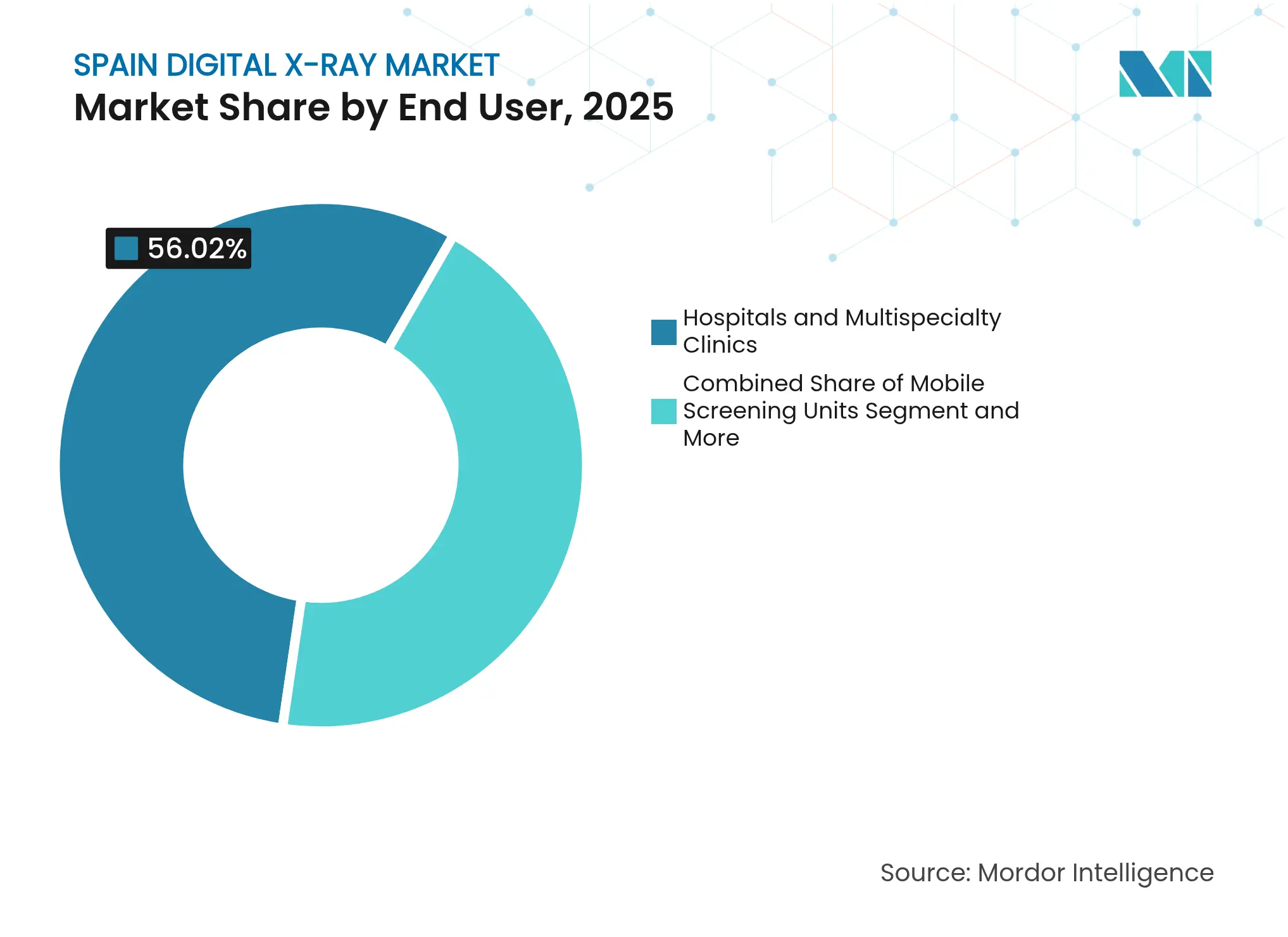

- By end user, hospitals and multispecialty clinics commanded 56.02% of Spain digital X-ray market share in 2025, while mobile screening units are set to climb at a 9.72% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Digital X-Ray Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Age-Ing Population Driving Musculoskeletal Imaging Demand

Age-Ing Population Driving Musculoskeletal Imaging Demand

| +1.8% | National, with concentration in Galicia, Asturias, Castilla y León | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

| Geographic Relevance:

National, with concentration in Galicia, Asturias,

Castilla y León

| Impact Timeline:

Long term (≥ 4 years)

|

National Oncology Plan Expanding Radiology Budgets

National Oncology Plan Expanding Radiology Budgets

| +1.2% | National, with early gains in Madrid, Catalonia, Andalusia | Medium term (2-4 years) | |||

Hospital Switch-Outs from CR To Cassette-Less DR to Cut

Dose & Workflow Time

Hospital Switch-Outs from CR To Cassette-Less DR to Cut

Dose & Workflow Time

| +0.9% | National, led by major hospital networks in Madrid, Barcelona, Valencia | Short term (≤ 2 years) | |||

Portable DR For Ambulance & Rural Care Roll-Outs

Portable DR For Ambulance & Rural Care Roll-Outs

| +0.7% | Rural regions: Extremadura, Castilla-La Mancha, Aragón, Galicia | Medium term (2-4 years) | |||

AI-Based Triage Mandates in Castilla-La Mancha &

Catalonia

AI-Based Triage Mandates in Castilla-La Mancha &

Catalonia

| +0.6% | Regional pilots expanding to Valencia, Madrid, Andalusia | Medium term (2-4 years) | |||

EU-Funded Green Hospital Retrofits Favour Low-Power DR

Units

EU-Funded Green Hospital Retrofits Favour Low-Power DR

Units

| +0.5% | National, concentrated in major urban hospitals | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Age-ing Population Driving Musculoskeletal Imaging Demand

Spain’s share of residents aged 65+ rises to 20.1% in 2025 and is projected to reach 25.6% by 2035, fueling a persistent need for orthopedic and chest examinations[1]Instituto Nacional de Estadística, “Proyecciones de Población 2022-2072,” ine.es. Orthopedic imaging already represents 38.63% of overall procedures, and Galicia, where 27.8% of citizens are seniors, records utilization rates 15-20% above the national average. The Plan AMAT-I earmarks EUR 400 million for high-throughput equipment capable of managing these larger patient cohorts. Hospitals favor dual-detector rooms and AI-assisted workflow tools that safeguard quality while cutting waiting times.

National Oncology Plan Expanding Radiology Budgets

The National Oncology Plan assigns EUR 2.5 billion to cancer infrastructure through 2030, dedicating one-quarter to imaging upgrades. Early-detection protocols emphasize low-dose chest X-ray screening for high-risk groups, pushing orders for digital systems with embedded nodule-detection algorithms. Catalonia’s pilot sites report 40% higher detection rates versus legacy film technology, and Madrid’s Hospital Universitario 12 de Octubre secured EUR 15 million to modernize 12 radiography rooms. Multidisciplinary tumor boards require seamless data exchange, strengthening demand for fully integrated imaging platforms.

Hospital Switch-Outs from CR to Cassette-Less DR to Cut Dose and Workflow Time

Spanish hospitals accelerate CR-to-DR conversions, achieving 30-40% faster examinations and 25-50% lower dose[2]Spanish Society of Medical Physics, “Guía de Radioprotección en Radiología Digital 2024,” sefm.es. Aragón completed system-wide upgrades across 15 hospitals in 2024, lifting throughput by 35% and slashing repeat scans by 60% due to fewer positioning errors. Motion-detection technology at Hospital Clínico San Carlos reduced retakes by 45% and underpins Spain’s environmental goals, as DR eliminates chemical waste and lowers energy use by 40% compared with CR processors.

Portable DR for Ambulance and Rural Care Roll-Outs

Mobile programs extend diagnostic reach to under-served rural regions, with Castilla y León deploying 25 mobile units that cut average travel times by 85% for basic X-rays. Hand-held systems integrated in ambulances enable on-site trauma assessment, trimming emergency department processing by about 20 minutes. EU structural funds reimburse up to 75% of acquisition costs when localities face radiology access gaps over 30 kilometers. These incentives underpin double-digit growth in battery-powered systems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Tight

Regional CAPEX Ceilings Post Nextgen EU Grants Run-Off

Tight

Regional CAPEX Ceilings Post Nextgen EU Grants Run-Off

| -0.8% | National, acute in Andalusia, Valencia, Castilla-La Mancha | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.8%

| Geographic Relevance:

National,

acute in Andalusia, Valencia, Castilla-La Mancha

| Impact Timeline:

Short

term (≤ 2 years)

|

Shortage

Of Radiographers Slows Utilisation Ramp-Up

Shortage

Of Radiographers Slows Utilisation Ramp-Up

| -0.6% | National, severe in Catalonia, Madrid, Basque Country | Medium term (2-4 years) | |||

GDPR-Driven

Cloud-Migration Hesitancy for Image Archives

GDPR-Driven

Cloud-Migration Hesitancy for Image Archives

| -0.4% | National, concentrated in public hospitals with legacy systems | Medium term (2-4 years) | |||

Competitive

Tender Pricing Pressure from Local OEM Sedecal

Competitive

Tender Pricing Pressure from Local OEM Sedecal

| -0.3% | National, most pronounced in public sector procurement | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Tight Regional CAPEX Ceilings Post NextGen EU Grants Run-Off

As COVID-era grants decline, regional health budgets fall 15-25%, prompting Andalusia and Valencia to defer EUR 45 million in planned radiology purchases[3]Spanish Court of Auditors, “Informe 1516 — Fondos NextGen EU,” tcu.es. Procurement teams emphasize total cost of ownership, tilting decisions toward basic DR systems or long-term leases rather than outright acquisition of premium AI-enabled rooms. This divergence produces two-speed adoption: well-funded hospitals in Madrid and Catalonia pursue high-spec platforms, while cash-constrained regions stretch existing assets.

Shortage of Radiographers Slows Utilization Ramp-Up

Vacancies affect 63% of radiology departments, and Catalonia reports 10-20% open positions, capping throughput at roughly 70% of capacity. Training programs graduate 450 technicians annually against demand for 680, and attrition among senior staff widens the gap. Hospitals deploy AI that flags critical cases and automated positioning to reduce operator burden, yet staffing shortfalls remain a growth headwind until pipeline expansion materializes.

Segment Analysis

By Portability: Fixed Dominance with Hand-Held Momentum

Fixed rooms retain 60.98% share of Spain digital X-ray market size in 2025 because large urban hospitals require high-throughput systems that manage 450 daily exams. The Hospital Universitario La Paz illustrates this efficiency with eight high-capacity rooms. Hand-held units, however, post the fastest 8.9% CAGR as emergency services and mobile clinics prioritize lightweight, battery-operated solutions that shorten trauma triage and rural screening times.

Demand follows a clear dichotomy. Urban centers continue to install ceiling-mounted suites integrated with RIS-PACS networks to ensure image routing within seconds. Rural and pre-hospital settings, supported by EU funds, favor compact devices that fit in ambulances and deliver usable images on a tablet display. Vendors offering cross-compatibility between fixed and portable detectors gain a strategic edge as hospitals bundle purchases under enterprise contracts.

Note: Segment shares of all individual segments available upon report purchase

By Detector Panel Type: Transition toward Flexible and CMOS Platforms

Amorphous silicon panels held 44.10% of Spain digital X-ray market share in 2025 on the back of proven reliability and favorable pricing. Flexible polyimide panels, however, clock a 9.42% CAGR by reducing weight 25% and resisting breakage during bedside use. Hospitals equipping mobile carts and ICU suites prefer these panels to minimize downtime and maintenance.

CMOS and IGZO developments lift demand for rapid frame rates in trauma and fluoroscopy-like sequences. Detection Technology’s 40 fps flat panel delivers 99-148 µm pixel pitches that satisfy low-dose requirements. Budget-sensitive buyers in Andalusia and Extremadura still procure amorphous silicon to maximize coverage with constrained funds, yet technology upgrades accelerate as cost gaps narrow.

By Application: Chest Imaging Leads Growth Trajectory

Orthopedic imaging commands 38.21% of total 2025 revenue, fueled by the ageing population and persistent sports injuries. Chest imaging outpaces all other uses at a 9.5% CAGR, propelled by oncology-driven lung screening and tuberculosis surveillance mandates. AI-based nodule detection, combined with low-dose protocols, cements the business case for premium chest units.

Cardiovascular and abdominal applications maintain steady volumes in emergency departments and routine check-ups. Dental radiography migrates to digital in small increments because thousands of private clinics replace film units as budgets permit. Hospitals integrate multipurpose detectors capable of orthopedic and chest work on the same room, boosting asset utilization.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: Mobile Units Accelerate Rural Access

Hospitals and multispecialty clinics captured 56.02% of Spain digital X-ray market size in 2025 through high patient throughput and comprehensive modality portfolios. Mobile screening units, however, exhibit a 9.72% CAGR as regional governments prioritize outreach. Castilla y León’s 25-unit fleet demonstrates savings in transport costs and clinician time.

Diagnostic imaging centers adapt by emphasizing specialist services such as interventional pain management or advanced MSK studies to protect share. Occupational health clinics and urgent-care centers demand compact, self-shielded devices that fit limited footprints, continuing to purchase entry-level DR rooms with simplified workflows.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Madrid and Catalonia represent the largest buyers in the Spain digital X-ray market. Madrid invested EUR 85 million in imaging upgrades during 2024, equipping 120 digital rooms that process 2.8 million studies annually. High exam volumes justify AI platforms that accelerate triage and reporting. Catalonia’s early adoption of AI mandates positions it as a testbed for new releases, with Barcelona’s leading hospitals acting as reference centers.

Andalusia and Valencia together house more than 11 million residents and retain sizable replacement demand for film and CR systems. Budget ceilings, however, translate into extended tender cycles and preference for cost-efficient configurations. Partnerships with local technology clusters in Valencia encourage vendors to establish service hubs that shorten downtime and enhance training efforts.

Rural autonomous communities—Extremadura, Castilla-La Mancha, Aragón, and Galicia—prioritize mobile care. EU FEDER grants covering up to 75% of equipment cost mitigate financial barriers and unlock demand for van-mounted DR suites. Galicia combines mobile screening with tele-radiology to offset physician shortages, achieving diagnostic parity with urban centers and setting a replicable model for other regions.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The Spain digital X-ray market shows moderate consolidation, with Sedecal harnessing domestic manufacturing to win cost-focused public tenders. International leaders—Siemens Healthineers, Fujifilm, Canon Medical, and Philips—differentiate via AI engines, automated positioning, and end-to-end service contracts that appeal to high-throughput hospitals. Siemens highlights AI-Rad Companion integration, while Fujifilm’s camera-assisted alignment reduces repeat shots and energy use.

Detector specialists such as Detection Technology and Vieworks advance flexible and IGZO panels that enhance portability and speed, challenging incumbent flat-panel suppliers. Software innovators align with hardware vendors to furnish CE-marked triage solutions compliant with forthcoming EU AI Act provisions. The resulting market bifurcates: premium AI-enabled systems dominate urban centers, and cost-optimized packages serve primary care and smaller diagnostic sites.

Spain Digital X-Ray Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Extremadura Health Service invested more than EUR 383,000 to install new digital X-ray equipment at the Castuera and Navalvillar de Pela health centers, replacing 18-year-old systems.

- February 2025: HM Santísima Trinidad Hospital reintegrated its Radiology Department and allocated over EUR 2 million to modernize modalities and workflow platforms.

Table of Contents for Spain Digital X-Ray Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Age-Ing Population Driving Musculoskeletal Imaging Demand

- 4.2.2National Oncology Plan Expanding Radiology Budgets

- 4.2.3Hospital Switch-Outs from CR To Cassette-Less DR to Cut Dose & Workflow Time

- 4.2.4Portable DR For Ambulance & Rural Care Roll-Outs

- 4.2.5AI-Based Triage Mandates in Castilla-La Mancha & Catalonia

- 4.2.6EU-Funded Green Hospital Retrofits Favour Low-Power DR Units

- 4.3Market Restraints

- 4.3.1Tight Regional CAPEX Ceilings Post Nextgen EU Grants Run-Off

- 4.3.2Shortage Of Radiographers Slows Utilisation Ramp-Up

- 4.3.3GDPR-Driven Cloud-Migration Hesitancy for Image Archives

- 4.3.4Competitive Tender Pricing Pressure from Local OEM Sedecal

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Portability

- 5.1.1Fixed Systems

- 5.1.2Mobile DR Systems

- 5.1.3Hand-held Systems

- 5.2By Detector Panel Type

- 5.2.1Amorphous Silicon

- 5.2.2CMOS

- 5.2.3IGZO / Flexible Panels

- 5.3By Application

- 5.3.1Orthopedic

- 5.3.2Chest Imaging

- 5.3.3Cardiovascular

- 5.3.4Dental

- 5.3.5Other Applications

- 5.4By End User

- 5.4.1Hospitals & Multispecialty Clinics

- 5.4.2Diagnostic Imaging Centers

- 5.4.3Mobile Screening Units

- 5.4.4Other End Users

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Agfa-Gevaert N.V.

- 6.3.2Canon Medical Systems

- 6.3.3Carestream Health

- 6.3.4Dentsply Sirona

- 6.3.5DRGEM

- 6.3.6Esaote S.p.A.

- 6.3.7Fujifilm Holdings Corp.

- 6.3.8GE HealthCare

- 6.3.9Hitachi Healthcare

- 6.3.10Hologic Inc.

- 6.3.11Konica Minolta

- 6.3.12Koninklijke Philips N.V.

- 6.3.13Mindray Bio-Medical

- 6.3.14Planmeca Oy

- 6.3.15Samsung Medison

- 6.3.16Sedecal (Spain)

- 6.3.17Shimadzu Corp.

- 6.3.18Siemens Healthineers AG

- 6.3.19Vatech Co.

- 6.3.20Villa Sistemi Medicali

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Spain Digital X-Ray Market Report Scope

As per the scope of this report, digital X-ray or digital radiography is a form of X-ray imaging where digital X-ray sensors are used instead of traditional photographic films. This has the added advantage of time efficiency and the ability to transfer images digitally and enhance them for better visibility. This method bypasses the chemical processing of photographic films. Digital X-ray imaging has high demand, as it requires less radiation exposure compared to traditional X-rays. Spain's digital X-ray market is segmented by application, technology, portability and end user. By Application market is segmented into orthopedic, cancer, dental, cardiovascular, and other applications. By technology market is segmented into computed radiography and direct radiography. By portability market is segmented into fixed systems and portable systems. By end-user market is segmented into hospitals, diagnostic centers, and other end users. The report offers the value (USD) for the above segments.