Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

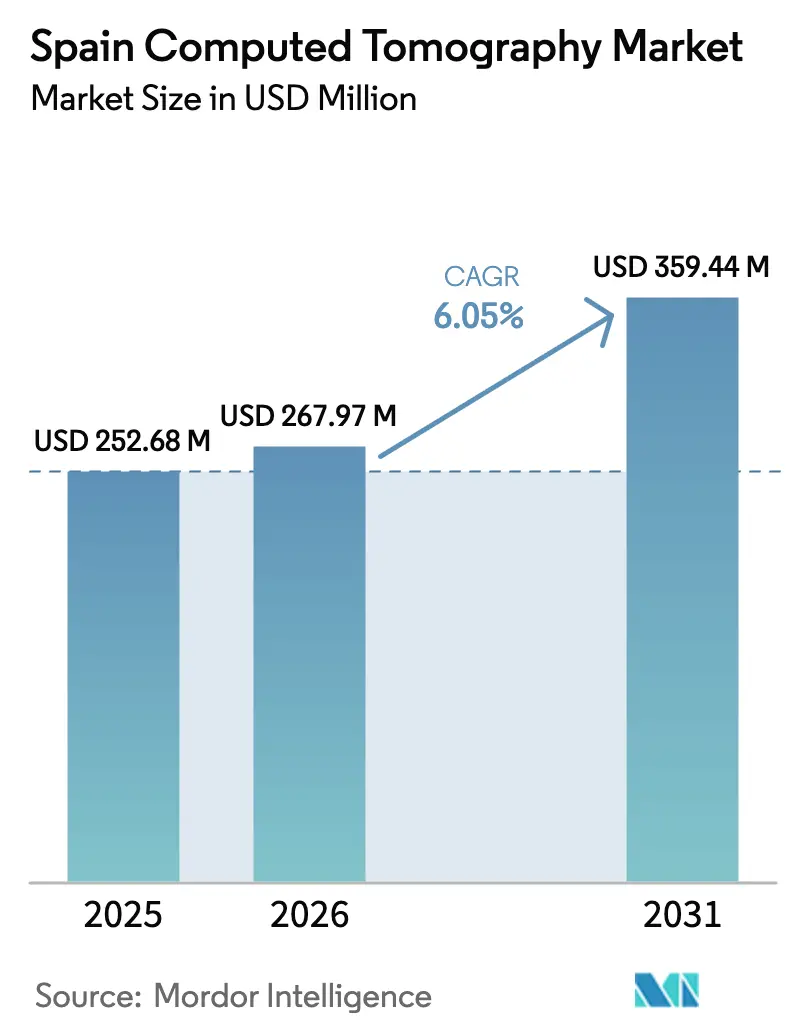

| Base Year Market Size (2025) | USD 252.68 Million |

| Market Size (2026) | USD 267.97 Million |

| Market Size (2031) | USD 359.44 Million |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Computed Tomography Market Analysis by Mordor Intelligence

The Spain computed tomography market size is expected to grow from USD 252.68 million in 2025 to USD 267.97 million in 2026 and is forecast to reach USD 359.44 million by 2031 at 6.05% CAGR over 2026-2031. Population aging, the government’s EUR 400 million INVEAT equipment renewal plan, and the rapid roll-out of AI-ready scanners are the primary catalysts for steady volume growth. Fixed installations form the backbone of public hospitals, yet mobile units are expanding quickly across rural provinces, reflecting a shift toward point-of-care imaging. Private insurers now cover 26% of Spain’s residents, unlocking a premium segment that absorbs high-slice and photon-counting systems. Vendors are therefore balancing price-performance medium-slice platforms for public tenders with spectral upgrades for private facilities. Supply constraints in radiology staffing and stricter EURATOM dose limits act as friction but are being countered by workflow automation and low-dose protocols.

Key Report Takeaways

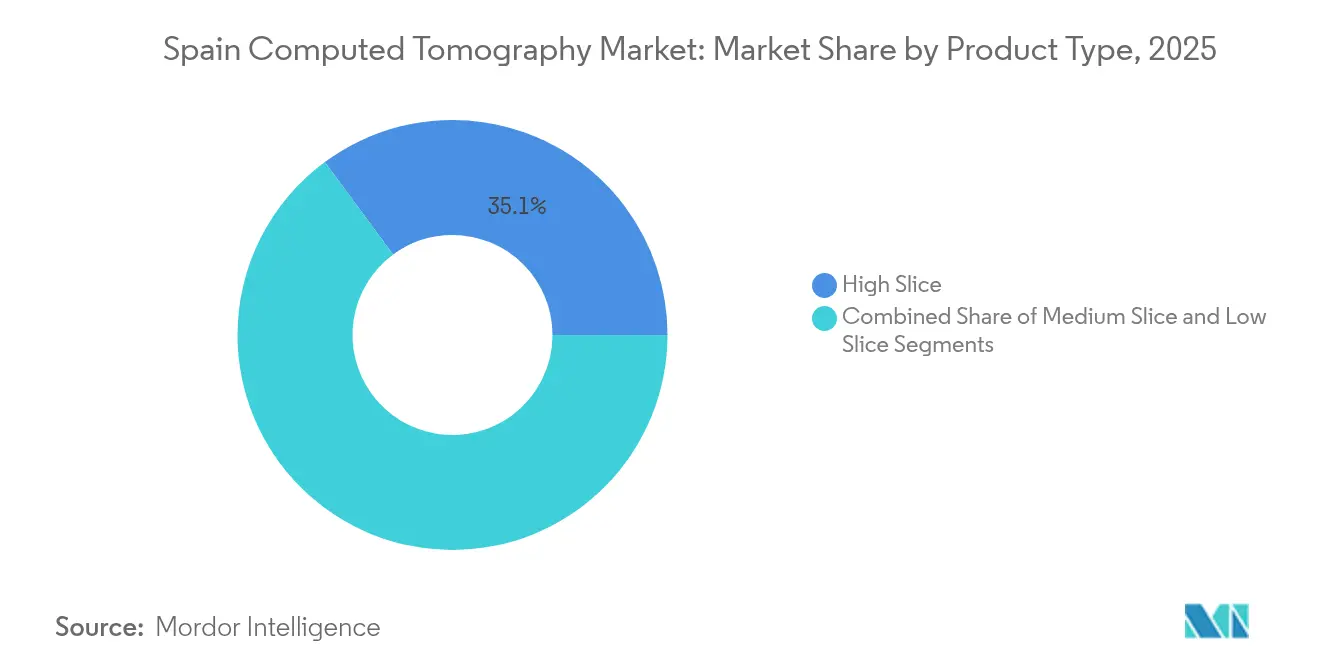

- By product type, high-slice systems led with 35.12% of Spain computed tomography market share in 2025; medium-slice systems are forecast to expand at 6.78% CAGR to 2031.

- By application, oncology accounted for 31.05% share of the Spain computed tomography market size in 2025, while neurology is advancing at a 6.85% CAGR through 2031.

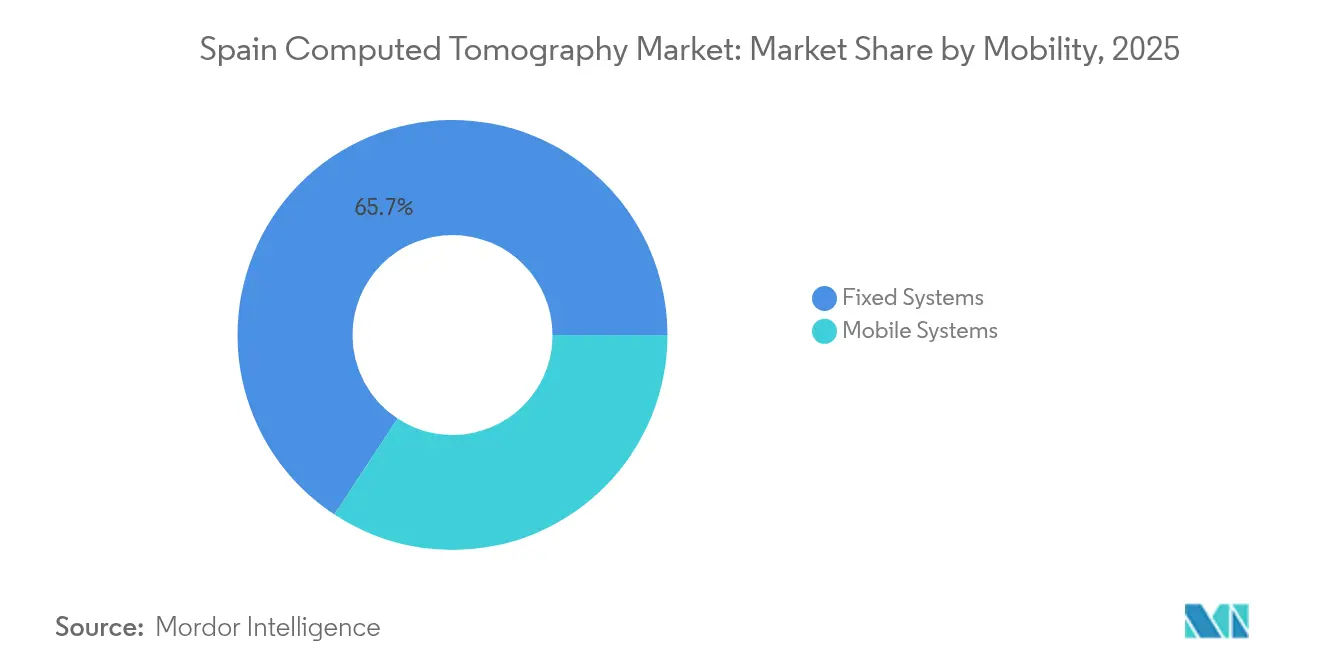

- By mobility, fixed platforms held 65.74% share of the Spain computed tomography market size in 2025 and mobile units are projected to grow at 7.1% CAGR to 2031.

- By end user, hospitals captured 49.20% of Spain computed tomography market share in 2025, whereas diagnostic imaging centers register the fastest expansion at 7.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Computed Tomography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government INVEAT programme accelerating scanner replacement | +1.8% | National, with priority in underserved regions | Medium term (2-4 years) |

| Rising geriatric population & chronic disease incidence | +1.5% | National, concentrated in rural and coastal areas | Long term (≥ 4 years) |

| Rapid uptake of spectral / photon-counting CT upgrades | +1.2% | Urban centers, private hospitals, academic medical centers | Short term (≤ 2 years) |

| Private health-insurance expansion boosting scan volumes | +1.0% | Madrid, Barcelona, Valencia metropolitan areas | Medium term (2-4 years) |

| AI-ready DICOM standardisation mandates in public hospitals | +0.8% | National, phased implementation by autonomous communities | Medium term (2-4 years) |

| Growing demand for ultra-low-dose paediatric protocols | +0.4% | National, specialized pediatric centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government INVEAT Programme Accelerating Scanner Replacement

Spain’s INVEAT plan allocates EUR 400 million for high-tech equipment, positioning the public sector to replace aging scanners and close regional gaps in diagnostic capacity. The Spanish Society of Medical Radiology reported that between 32% and 59% of imaging devices exceeded 10 years in service, underscoring the programme’s urgency. Madrid is already linking all public hospitals to a unified imaging network scheduled for completion by end-2025, enabling shared protocols and bulk servicing economies [1]Comunidad de Madrid, “Plan de digitalización de imagen diagnóstica 2025,” comunidad.madrid . Standardized specifications under INVEAT are encouraging hospitals to favor 64-slice platforms that dovetail with AI upgrades. Training grants attached to the plan are also mitigating the learning curve for spectral imaging and dose-optimization tools.

Rising Geriatric Population & Chronic Disease Incidence

The share of Spaniards aged 65 and above is projected to climb from 20.4% in 2024 to 30.5% by 2055, driving long-run demand for CT-based cancer staging, stroke evaluation, and coronary assessment [2]Instituto Nacional de Estadística, “Population Projections 2024–2055,” ine.es . New cancer diagnoses are expected to reach 296,103 in 2025, led by prostate, breast, and lung malignancies. Hypertension affects 47% of adult men and 39% of women, increasing CT angiography referrals for plaque characterization [3]European Association of Preventive Cardiology, “EAPC Country of the Month - Spain,” escardio.org . Rural provinces with the steepest aging rates rely on mobile scanners that rotate among district hospitals, ensuring population coverage despite staffing shortages. Low-dose algorithms tailored for frail patients now form part of standard procurement criteria.

Rapid Uptake of Spectral / Photon-Counting CT Upgrades

Photon-counting detectors deliver higher spatial resolution with radiation savings and have begun scaling beyond academic centers into private hospitals. Early adopters note clearer coronary visualization and improved oncologic lesion conspicuity, reducing follow-up imaging by nearly 19% over 10 years. Siemens Healthineers’ NAEOTOM Alpha installations in Spain illustrate a competitive pivot toward premium differentiation. Cost-effectiveness studies estimate lifetime savings of USD 794 per oncology patient due to fewer additional scans. Vendors are bundling AI-guided calcium scoring and spectral lung protocols that match Spain’s cardiovascular and oncology caseload.

Private Health-Insurance Expansion Boosting Scan Volumes

Health insurance coverage rose from 19% to 26% of the population over the past decade, trimming wait times from public queues exceeding 94 days for specialist visits. SegurCaixa Adeslas now insures 5.6 million clients, paying network providers rates that support same-day CT slots. Out-of-pocket CT pricing ranges from EUR 200-700 without insurance versus EUR 5-30 with coverage, reinforcing the migration to private diagnostics. Madrid, Barcelona, and Valencia concentrate the bulk of new private imaging centers, each outfitted with high-slice cardiology packages and oncology spectral modes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance cost of multi-slice systems | -1.5% | National, particularly affecting smaller hospitals and rural centers | Long term (≥ 4 years) |

| Radiation-dose concerns and tightening EURATOM limits | -0.8% | EU-wide, with stricter enforcement in academic medical centers | Medium term (2-4 years) |

| Shortage of radiologists lengthening scan-to-report times | -1.2% | National, acute in rural areas and smaller cities | Medium term (2-4 years) |

| Regional procurement audits slowing equipment tenders | -0.7% | Andalusia, other autonomous communities with procurement irregularities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost of Multi-Slice Systems

Purchasing a 128-slice scanner can exceed EUR 1 million, with annual service contracts adding 8-12% of the purchase price. Smaller hospitals therefore favor refurbished 64-slice units even though diagnostic throughput is lower. One-third of Spain’s CT inventory remains past recommended replacement cycles, raising downtime risk and repair bills. Public tenders attempt to counter cost pressures through group purchasing yet budget ceilings still cap the number of units awarded per region. Maintenance complexity is heightened for photon-counting scanners that require specialized calibration engineers and spare detector modules.

Shortage of Radiologists Lengthening Scan-to-Report Times

Aging radiology personnel and limited residency slots have resulted in an estimated 12-13% attrition rate, creating reporting delays particularly in smaller cities. AI triage solutions route urgent head trauma or pulmonary embolism cases to available readers but do not fully solve staffing gaps. Private groups lure specialists with higher pay and flexible schedules, intensifying geographic imbalances. Teleradiology fills part of the void yet some autonomous communities restrict cross-border reading for medico-legal reasons, prolonging turnaround times in remote areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medium-Slice Systems Drive Modernization

Medium-slice platforms are projected to register a 6.78% CAGR through 2031 as hospitals prioritize balanced performance and cost. High-slice models kept a 35.12% Spain computed tomography market share in 2025, cemented by academic centers that manage complex cardiac and oncology protocols. Hospitals use medium-slice units for emergency throughput, abdominal workups, and routine chest scans, stretching budgets without compromising core capability. The Spain computed tomography market size expansion for medium-slice equipment is further supported by standardized INVEAT specifications that list 64-slice minimums, effectively sidelining low-slice offerings. Photon-counting options slot into the high-end niche, attracting private facilities that differentiate on image clarity.

Budget pressures inside the public system tilt replacement cycles toward modular upgrades rather than full-chassis swaps, extending hardware life while adding AI-based dose management. Rural centers deploy refurbished systems sourced from large urban hospitals, yet still benefit from software enhancements covering metal artifact reduction. Vendor service contracts increasingly bundle remote monitoring that predicts tube wear, a feature that trims unplanned downtime.

By Application: Oncology Leadership Amid Neurology Acceleration

Oncology held 31.05% share in 2025 as CT remains fundamental for tumor staging, radiation planning, and recurrence surveillance. The Spain computed tomography market size for oncology segments is forecast to keep pace with rising cancer incidence that tops 296,000 new cases in 2025. Neurology scans, driven by stroke codes and dementia workups, are set to grow at 6.85% CAGR, fastest among applications. Stroke prevalence is 2.02% nationally, and door-to-scan times are benchmarked at under 20 minutes for thrombectomy eligibility, stimulating neurology demand.

Cardiovascular studies gain traction on the back of 47% male hypertension prevalence, relying on CT angiography to guide statin therapy and invasive angiograms. Musculoskeletal indications pivot toward low-dose protocols for sports injuries, aligning with Spain’s active aging demographic. AI decision support tools in oncology flag subtle lung nodules and bone metastases, decreasing false negatives and standardizing follow-up intervals.

By Mobility: Mobile Systems Gain Rural Traction

Fixed scanners anchored 65.74% of installations in 2025, yet mobile units are projected to climb at 7.1% CAGR through 2031. Mobile platforms bring chest, trauma, and head imaging to provincial hospitals lacking permanent suites. Coastal regions employ truck-mounted scanners during summer tourist surges, alleviating overflow from local emergency departments. Bedside CT in intensive care units reduces transport risk for ventilated patients while exploiting a compact footprint.

Vendors are refining vibration dampening and generator efficiency to extend mobile uptime across Spain’s varied terrain. Integrated telepresence screens allow radiologists in Madrid to observe scans executed hundreds of kilometers away, improving scan protocol adherence. Private operators run subscription models that supply mobile CT services on scheduled routes, capturing revenue from small clinics without capital capacity.

By End User: Diagnostic Centers Accelerate Growth

Hospitals accounted for 49.20% of scanner placements in 2025 because emergency and in-patient workflows demand round-the-clock imaging. Diagnostic imaging centers show a 7.02% CAGR, propelled by private insurance coverage and consumer preference for short waiting lists. Centers typically house dual-energy or high-slice scanners plus MRI suites, positioning themselves as one-stop shops. Capital groups such as Nexxus Iberia finance chain expansion, standardizing brand experience and raising service quality benchmarks.

Diagnostic centers concentrate in Madrid, Barcelona, and Valencia, regions where private plans dominate. Competitive pricing bundles CT angiography with cardiology consults, edging specialist demand away from public hospitals. Mobile CT vendors complement this ecosystem by leasing hours at rural clinics, broadening reach without bricks-and-mortar investment.

Geography Analysis

Spain’s CT footprint reflects the nation’s economic and demographic mosaic. Madrid and Catalonia combine for nearly 40% of scanner stock, powered by tertiary hospitals and dense private networks. Andalusia is the fastest-growing region through 2031; its coastal provinces host retired and expatriate populations that push imaging volumes for oncology and cardiology. The Basque Country and Valencia leverage strong industrial bases and research clusters, with Valencia acting as an AI hub via Quibim’s imaging development.

Rural regions such as Castilla-La Mancha, Extremadura, and Galicia contend with population decline yet benefit from state-funded mobile programs. These mobile routes follow weekly circuits connecting district hospitals and primary care centers, balancing equity in diagnostic access. The Canary and Balearic Islands service tourist peaks with flexible mobile fleets and seasonal staffing, ensuring throughput for trauma and chest scans. Cross-border care with Portugal influences Extremadura and Galicia, where bilateral agreements allow patient referrals, stabilizing demand despite local demographics. The INVEAT allocation includes regional quotas, anchoring a baseline of two new CT units per underserved province by 2026. Implementation pace varies, with decentralized regions finalizing tenders slower than centrally managed ones. Procurement audits in Andalusia temporarily slowed rollouts but also spurred transparent tender reforms.

Competitive Landscape

The Spain computed tomography market is moderately consolidated. GE HealthCare, Siemens Healthineers, Philips, and Canon Medical Systems supply the majority of hardware. Siemens capitalizes on photon-counting early-bird adoption and recently signed a EUR 60.3 million multi-vendor partnership with Nantes University Hospital that includes nine CT scanners, reinforcing service-based revenue streams. GE HealthCare commands cardiology niches with its Revolution line and heads a EUR 25.3 million Thera4Care consortium that advances cancer theranostics.

Local innovators shape the AI stack. Valencia-based Quibim raised USD 50 million to scale multi-modal imaging algorithms that embed into vendor-neutral viewers. Partnerships with Philips integrate AI lesion characterization into routine workflows. Private hospital group Ribera Salud is expanding into Aragon and Asturias, enhancing bargaining power over equipment pricing while widening regional service coverage. Mergers among diagnostic chains are expected as private equity seeks to pool procurement leverage and brand presence.

White-space growth lies in mobile fleet operators that provide subscription-based rural coverage and in turnkey AI platforms that streamline radiologist throughput. Market risk stems from procurement scrutiny, as evidenced by the EUR 1.223 billion Andalusian contract investigation. Vendor compliance programs and local service centers become decisive differentiators in future tenders.

Spain Computed Tomography Industry Leaders

GE Healthcare

Canon Medical System

Koninklijke Philips N.V.

Fujifilm Holdings Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare unveiled the Revolution Vibe CT system featuring Unlimited One-Beat Cardiac imaging and AI solutions to enhance cardiovascular workflows.

- January 2025: Quibim closed a USD 50 million Series A round to advance AI interpretation tools across MRI, CT, and PET modalities.

- January 2025: Ribera Salud expanded into Aragon and Asturias, adding two hospitals and six clinics to its network.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spain computed tomography market as the yearly revenues from sales, installation, and first-year service of fixed, mobile, and cone-beam scanners ranging from 16-slice to 320-slice that are used for human diagnostic imaging in hospitals, diagnostic imaging centers, and selected outpatient facilities.

Scope exclusion: scanners dedicated solely to veterinary or industrial non-destructive testing are not counted.

Segmentation Overview

- By Product Type

- Low Slice

- Medium Slice

- High Slice

- By Application

- Oncology

- Neurology

- Cardiovascular

- Musculoskeletal

- Other Applications

- By Mobility

- Fixed Systems

- Mobile Systems

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiology department heads in Madrid, Barcelona, and Seville, procurement officers at private hospital chains, and regional equipment distributors. These conversations validated slice-mix trends, typical average selling prices, and the real-world impact of the INVEAT grants before we locked assumptions.

Desk Research

We began by mapping publicly available demand signals, scanner import-export codes from the Spanish Customs Agency, procedure volumes from the Ministry of Health's CMBD database, aging population tables from Instituto Nacional de Estadística, and radiology funding allocations disclosed in Spain's INVEAT modernization program. Complementary insights came from peer-reviewed journals such as Radiología Española, position papers of the Spanish Radiology Society, and manufacturer 10-K filings.

Subscription repositories, notably D&B Hoovers for company financials and Dow Jones Factiva for press coverage, helped us benchmark vendor shipments, while patent screenshots from Questel flagged pipeline upgrades. This list is illustrative; many additional sources were consulted to cross-check facts and fill subtle data gaps.

Market-Sizing & Forecasting

A top-down reconstruction starts with annual CT scan procedure counts, inflation-adjusted Medicare reimbursement equivalents, and average scanner replacement cycles. Results are then sanity-checked with sampled supplier roll-ups of units multiplied by ASP. Key variables include slice-mix shift toward 128+ systems, hospital capital budget growth, price erosion on legacy 16-slice models, regulatory lead times, and forecasted oncology incidence. Multivariate regression combined with three-scenario ARIMA smoothing produces our 2025-2030 outlook, while small residual gaps in bottom-up estimates are bridged using mobile unit penetration ratios shared by field engineers.

Data Validation & Update Cycle

Every draft passes an anomaly scan, peer review, and senior analyst sign-off. Material news, such as a new INVEAT tranche or currency shock, triggers an interim refresh. Reports are fully rebuilt each year, and just before delivery, an analyst re-runs the model so clients receive the latest calibrated view.

Why Mordor's Spain Computed Tomography Baseline Commands Reliability

Published figures often diverge because firms pick different scanner classes, install base churn assumptions, and refresh cadences. We anchor our baseline to procedure-driven demand pools and current ASP reality, an approach that clients tell us feels tangible.

Key gap drivers include whether mobile CT and cone-beam units are counted, the treatment of grant-funded units that have not yet been installed, currency conversion dates, and the aggressiveness of price deflation curves. Our annual rebuild means Mordor's totals move sooner when INVEAT or euro inflation shifts, whereas others may run on two-year update cycles.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 252.68 million (2025) | Mordor Intelligence | - |

| 201.54 million (2024) | Global Consultancy A | excludes mobile CT, uses five-year refresh |

| 201.59 million (2023) | Regional Consultancy B | counts only scanners >=64 slices |

| 80 million (2024) | Industry Association C | values factory gate sales, omits service and installation |

In short, our disciplined variable selection, yearly update rhythm, and dual-pass validation give decision-makers a clear, reproducible baseline they can trust when sizing Spain's CT opportunities.

Key Questions Answered in the Report

What is the current value of the Spain computed tomography market?

The Spain computed tomography market is valued at USD 267.97 million in 2026.

How fast will the Spain computed tomography market grow by 2031?

It is projected to expand at a 6.05% CAGR, hitting USD 359.44 million by 2031.

Which segment holds the largest Spain computed tomography market share?

High-slice scanners dominate with 35.12% share in 2025, driven by cardiac and oncology demand.

Why are mobile CT units gaining traction in Spain?

Mobile scanners grow at 7.1% CAGR because they improve access in rural and tourist regions that lack fixed installations.

How is private health insurance influencing CT scan volumes?

Private coverage now reaches 26% of Spaniards, cuts wait times, and boosts premium scan demand in urban diagnostic centers.

Page last updated on: