Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.51 Billion |

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

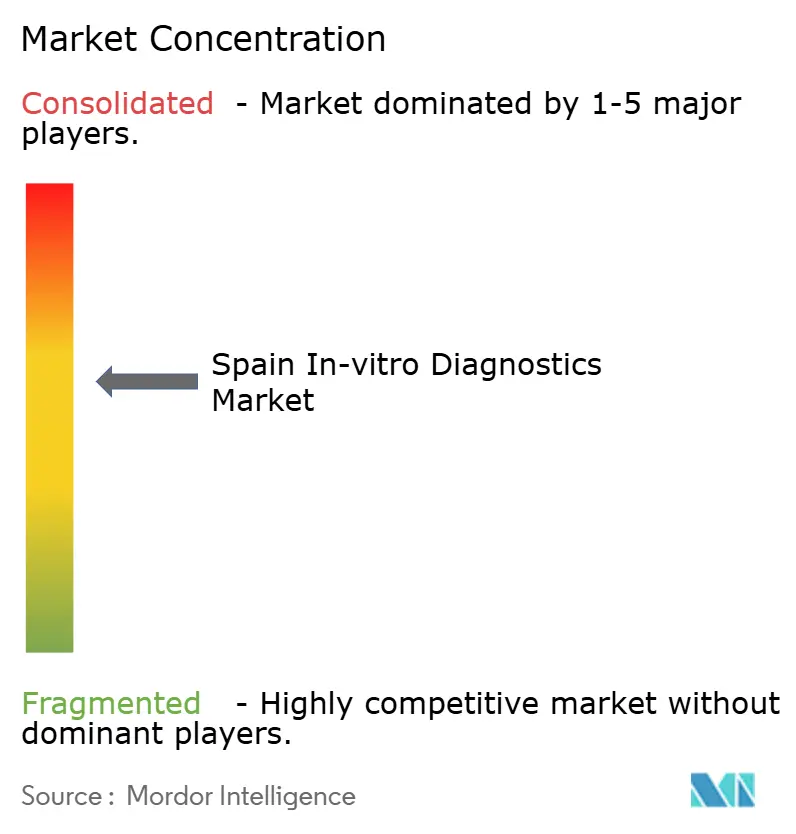

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain In-vitro Diagnostics Market Analysis by Mordor Intelligence

Spain IVD market size in 2026 is estimated at USD 2.62 billion, growing from 2025 value of USD 2.51 billion with 2031 projections showing USD 3.27 billion, growing at 4.49% CAGR over 2026-2031. Continued momentum is rooted in an aging population, higher chronic-disease incidence, and the country’s full transition to the EU In Vitro Diagnostic Regulation (IVDR). Strong demand for frequent renal, diabetes, and hypertension screening is lifting test volumes, while hospital groups in Madrid and Catalonia are modernizing laboratories with AI-enabled analyzers that shorten turnaround times. Molecular assay innovators are benefiting from European Investment Bank financing, and Spain’s Digital Health Strategy is steering budgets toward connected instruments that meet IVDR traceability rules. At the same time, decentralized procurement across 17 autonomous communities is nudging suppliers toward value-based contracts that link reagent spending to clinical outcomes.

Key Report Takeaways

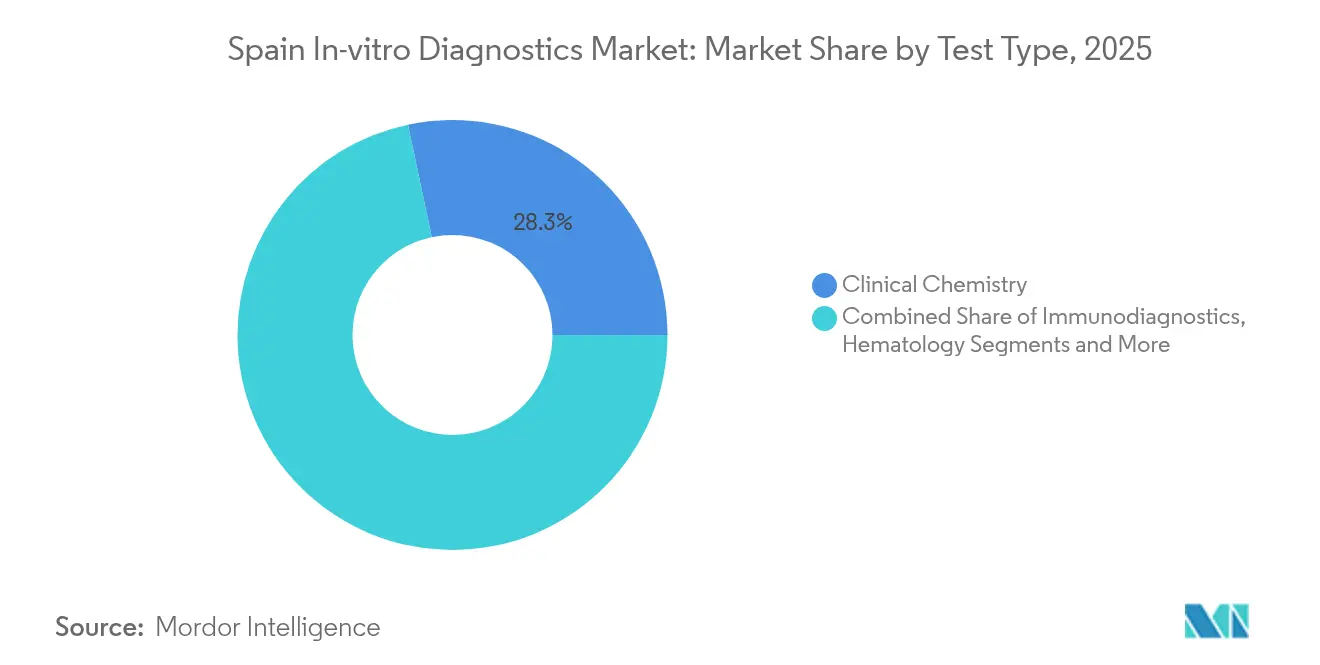

- By test type, clinical chemistry led with 28.32% revenue share in 2025, while molecular diagnostics is projected to advance at a 9.38% CAGR to 2031.

- By product, reagents & consumables captured 70.35% of the Spain IVD market share in 2025, and software & services is forecast to grow at an 8.01% CAGR through 2031.

- By usability, disposable devices commanded 82.75% of the Spain IVD market size in 2025, whereas reusable devices are expected to expand at an 8.12% CAGR to 2031.

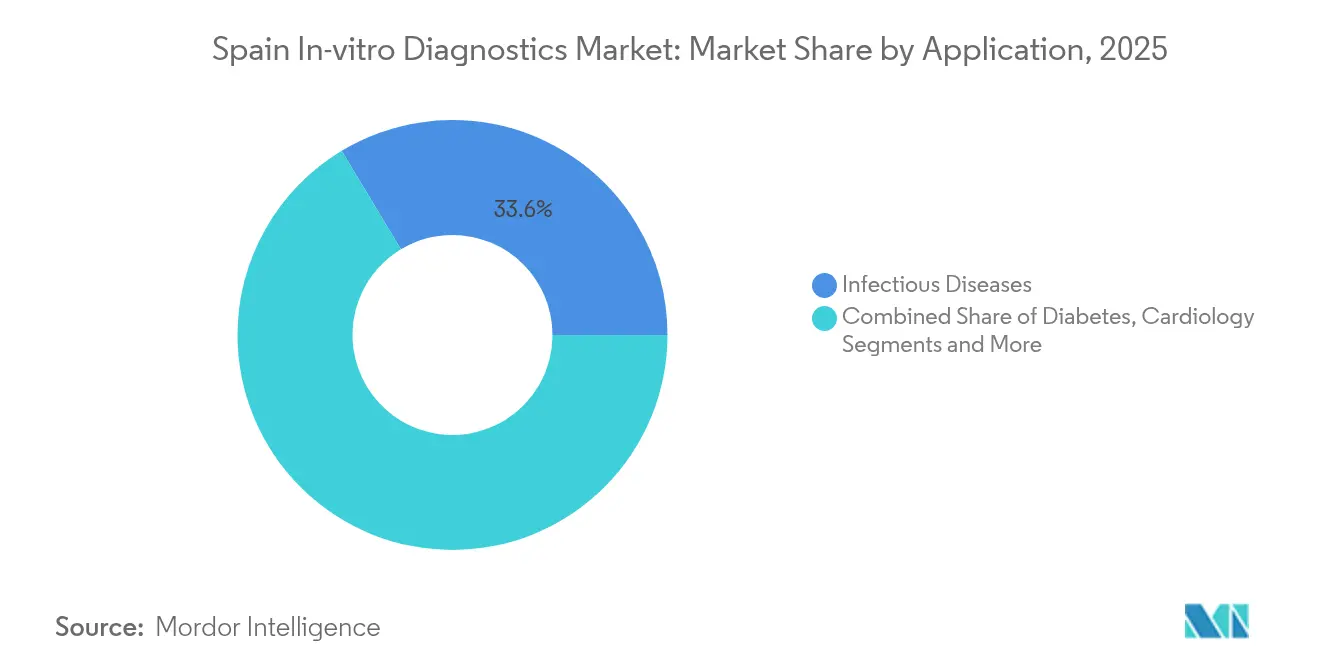

- By application, infectious-disease testing accounted for a 33.62% share in 2025, and oncology diagnostics is on track for a 9.42% CAGR between 2026 and 2031.

- By end user, hospital & reference laboratories held 60.92% revenue share in 2025, while home-care and ambulatory point-of-care settings are growing the fastest at a 10.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain In-vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic and lifestyle diseases | +1.8% | Asturias, Castile and León, Galicia | Long term (≥ 4 years) |

| Rapid technological innovation in molecular and immunodiagnostics | +1.2% | Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Expansion of point-of-care testing across primary and home settings | +0.9% | Catalonia, Madrid | Medium term (2-4 years) |

| Government and EU investment programs for digital lab modernization | +0.7% | National | Short term (≤ 2 years) |

| Growth of precision medicine and companion-diagnostics adoption | +0.5% | Madrid, Barcelona, Valencia, Seville | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Lifestyle Diseases

About 15.1% of Spanish adults live with chronic kidney disease, a figure that continues to climb with population aging. Higher prevalence of diabetes, cancer, and cardiovascular disorders is prompting earlier, more frequent testing in primary care clinics. The CARABELA-CKD program standardizes nephrology pathways and lifts demand for creatinine, eGFR, and micro-albumin tests across the Spain IVD market. Laboratories in Galicia and Asturias report double-digit yearly increases in renal panels, pushing reagent distributors to boost stock levels. Regional health authorities now bundle screening targets into hospital financing agreements, an approach that ties purchasing volumes to chronic-care metrics. Collectively, these factors underpin consistent baseline growth for routine and specialty assays.

Rapid Technological Innovation in Molecular & Immunodiagnostics

The European Investment Bank’s EUR 20 million loan to Universal DX accelerates liquid-biopsy development for early colorectal-cancer detection[1]European Investment Bank, “Universal DX Liquid-Biopsy Financing,” eib.org. Spanish startups mix next-generation sequencing with machine-learning algorithms to profile multiple biomarkers in one run, lowering per-test costs. University hospitals in Valencia validate multiplex respiratory panels that deliver 90-minute results and reduce inpatient isolation days. Immunodiagnostic platforms now integrate chemiluminescent detection with automated calibration, raising sensitivity for thyroid and cardiac markers. As IVDR pushes traceability and performance benchmarking, local firms adopt cloud-based quality-control dashboards that feed directly into notified-body audits, strengthening compliance while sharpening competitive differentiation.

Expansion of Point-of-Care Testing Across Primary & Home Settings

Catalonia’s EUR 580 million primary-care improvement plan channels fresh funds into rapid analyzers for glucose, CRP, and coagulation monitoring. General practitioners deploy handheld readers linked to electronic health records, allowing same-visit treatment adjustments for chronic patients. In Madrid, pharmacies pilot antigen-test kiosks that transmit anonymized data to regional surveillance databases within minutes, supporting real-time outbreak tracking. Supply-chain managers report that barcode-enabled cartridge systems cut wastage by 12% compared with manual strips, making point-of-care economics more favorable. Home-based INR monitoring also gains traction as insurers reimburse remote data uploads, easing pressure on hospital anticoagulation clinics.

Government & EU Investment Programs for Digital Lab Modernization

Spain’s Recovery & Resilience Plan earmarks EUR 800 million for high-tech cancer-diagnostic devices, driving replacement cycles for outdated analyzers[2]OECD/European Observatory, “Recovery and Resilience Plan,” oecd.org. The PERTE for Cutting-edge Health adds EUR 2.36 billion for AI integration and a national health data lake. University Hospital La Paz in Madrid installs robotic sample-track lines that lift hourly throughput by 40% while improving specimen traceability. Regional tenders now require middleware interoperability, prompting mid-tier suppliers to partner with software vendors for IVDR-ready connectivity. Collectively, these capital injections speed lab automation and promote standards-based data exchange across the Spain IVD market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and evolving EU IVDR regulatory landscape | -0.9% | National | Short term (≤ 2 years) |

| Regional reimbursement delays and budget constraints | -0.7% | Andalusia, Extremadura, Murcia | Medium term (2-4 years) |

| Shortage of skilled laboratory personnel and training gaps | -0.5% | Rural provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent & Evolving EU IVDR Regulatory Landscape

Seventy-three percent of Spanish laboratories say they lack adequate guidance to complete IVDR conformity files[3]Association for Molecular Pathology, “EU IVDR Survey,” amp.org. High-risk assays must meet new performance-study and post-market-surveillance rules by May 2025, yet notified-body capacity remains tight. The 2024/1860 amendment extends certain timelines but also adds supply-chain traceability duties, raising administrative workloads. Smaller reagent makers divert R&D budgets toward documentation, slowing product-pipeline turnover. Because each autonomous community interprets EU law through its own procurement filters, suppliers face variable local checklists that complicate national launches.

Regional Reimbursement Delays & Budget Constraints

Only 9.49% of reimbursement decisions reference formal HTA conclusions, exposing gaps in Spain’s evidence-based funding process. Andalusia and Extremadura apply tight annual spending caps that postpone adoption of new oncology panels, whereas Madrid greenlights them within six months. Draft royal-decree proposals aim to create a single national HTA framework, but interim uncertainty restrains hospital buyers. Point-of-care devices struggle most: without a uniform tariff code, clinics finance them from discretionary budgets, slowing roll-out despite proven efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Reshaping Diagnostic Paradigms

Clinical chemistry generated 28.32% of the Spain IVD market size in 2025, supported by its central role in metabolic, renal, and hepatic panels. Routine analyzers achieve high throughput and cost efficiency, which stabilizes reagent demand. However, molecular diagnostics is posting a 9.38% CAGR as hospitals expand oncology and infectious-disease gene testing. The Spain IVD market benefits from Seegene and Werfen’s joint venture, which promises syndromic PCR menus tailored to local antimicrobial-resistance profiles. As next-generation sequencing costs fall, regional centers pilot cancer-risk screening programs financed through EU innovation funds, cementing growth.

A shift toward hybrid panels that combine immunoassay and PCR markers blurs traditional segment boundaries. Laboratories deploy reflex-testing protocols that trigger confirmatory molecular runs after abnormal chemistry results, raising cross-segment reagent consumption. IVDR mandates traceable lot-release data, encouraging integration of chemistry and molecular middleware. These developments reinforce molecular diagnostics’ strategic importance while ensuring clinical chemistry retains volume leadership in the Spain IVD market.

By Product: Software Integration Driving Diagnostic Intelligence

Reagents & consumables represented 70.35% of the Spain IVD market share in 2025, reflecting high test frequency and replenishment cycles. Automated inventory modules tied to laboratory-information systems trim expiry-related wastage, yet tight tender pricing keeps margins thin. Software & services—currently under 10% of revenues—will outpace other categories at an 8.01% CAGR as digital pathology, cloud middleware, and AI analytics become procurement priorities. Hospitals adopt subscription models that bundle instrument leasing with predictive-maintenance modules, converting capital outlays into operating expenses.

Instrument vendors now embed open APIs so third-party algorithms can interrogate analyzer data, turning platforms into clinical-decision hubs. Spain’s Digital Health Strategy sets interoperability standards that favor HL7-FHIR messaging, nudging suppliers to certify integrations. In turn, reagent makers collaborate with software firms to package quality-control dashboards, tying consumable sales to analytical-performance guarantees. This convergence between hardware, reagents, and analytics drives holistic purchasing decisions across the Spain IVD market.

By Usability: Disposable Dominance Reflects Infection-Control Priorities

Disposable IVD devices accounted for 82.75% of 2025 revenues, a figure cemented by post-pandemic infection-control protocols. Single-use cassettes simplify staff workflows and align with IVDR sample-traceability rules, outweighing per-test cost premiums. Environmental policymakers, however, press laboratories to adopt circular-economy practices, spurring interest in reusable plastics and validated reprocessing cycles. New polymer blends withstand autoclave temperatures without leaching, supporting an 8.12% CAGR for reusable formats through 2031.

Manufacturers position hybrid solutions—disposable microfluidic chips housed in reusable readers—to balance sustainability and biosafety. Procurement teams include carbon-footprint criteria in tenders, rewarding suppliers that offer recycling schemes. As a result, the Spain IVD market observes gradual convergence between disposability and reusability, with device design increasingly optimized for both infection control and ecological stewardship.

By Application: Oncology Diagnostics Driving Precision-Medicine Adoption

Infectious-disease assays delivered 33.62% of Spain IVD market revenues in 2025, buoyed by persistent respiratory-virus surveillance and antimicrobial-resistance screening. Yet oncology diagnostics will expand at a 9.42% CAGR, propelled by non-invasive liquid-biopsy initiatives funded by EU and national grants. Early-detection programs in Barcelona now include annual circulating-tumor-DNA tests for high-risk populations, elevating demand for ultra-sensitive PCR reagents.

Diabetes monitoring remains a sizeable niche due to sustained prevalence and government emphasis on chronic-disease management. Cardiology assays increasingly pair high-sensitivity troponin with digital ECG analytics, providing faster rule-out of acute coronary syndromes in emergency departments. Advanced multiplex platforms allow autoimmune-panel consolidation, shortening diagnostic journeys for systemic lupus and rheumatoid arthritis patients. These dynamics keep application portfolios diverse while reinforcing oncology’s role as a future growth anchor for the Spain IVD market.

By End User: Home-Care Settings Disrupting Traditional Testing Paradigms

Hospital and reference laboratories captured 60.92% of Spain IVD market revenues in 2025, underpinned by integrated networks that serve acute-care and specialist clinics. Automation upgrades yield high productivity, yet capacity constraints persist amid rising test complexity. Home-care and ambulatory point-of-care channels will rise at a 10.18% CAGR as telehealth reimbursement widens. Pharmacies in Catalonia pilot HbA1c testing services linked to virtual endocrinology consults, cutting referral times by two weeks.

Diagnostic laboratories negotiate reagent-rental contracts that swap higher menu breadth for lower upfront instrument fees, aligning with variable outpatient demand. Academic centers leverage sequencing cores for translational-research contracts, blurring lines between patient testing and research. Community health centers expand basic panels such as lipid and thyroid profiles using portable analyzers, enhancing access in underserved areas. Collectively these shifts point to a distributed yet interconnected ecosystem that keeps the Spain IVD market resilient and patient-centric.

Geography Analysis

Madrid and Catalonia together account for over 35.24% of the Spain IVD market size, supported by dense hospital networks and concentrated R&D funding. Regional health ministries funnel EU cohesion funds into molecular-oncology hubs that attract multinational clinical-trial activity. Andalusia, although budget-constrained, shows steady uptake of high-throughput chemistry analyzers driven by chronic-care programs, while Galicia and Asturias focus on renal and cardiac panels aligned with their aging demographics. In central Castilla-La Mancha, procurement pools negotiate multi-year reagent contracts that stabilize pricing yet slow product refresh cycles. Valencia integrates AI-driven triage tools within public hospitals, accelerating imaging-to-lab data handoffs. Basque Country’s technology park hosts IVD startups that export middleware solutions, illustrating regional specialization within the Spain IVD industry. Across the Canary and Balearic Islands, maritime logistics shape inventory practices, favoring compact instruments and extended-shelf-life reagents. These geographic nuances require suppliers to tailor channel strategies, bolstering the Spain IVD market’s heterogeneity while broadening its growth base.

Regulatory Landscape

Spain regulates in-vitro diagnostic (IVD) medical devices under the EU IVDR (Regulation (EU) 2017/746), implemented nationally by AEMPS (Agencia Espanola de Medicamentos y Productos Sanitarios) and the Ministry of Health (Ministerio de Sanidad). A key national anchor is Royal Decree 942/2025, published in the BOE on October 23, 2025 and effective October 24, 2025, which completes Spain's alignment to IVDR requirements and clarifies national procedures affecting manufacturers, importers, and healthcare laboratories.

Royal Decree 942/2025 adds Spain-specific operational requirements that shape market access and laboratory operations. These include prior operating licenses from AEMPS (valid for five years) for manufacturers, importers, and sterilization service providers, along with additional obligations for in-house IVD manufacturing in healthcare facilities (notification to AEMPS, designation of a Person Responsible for Regulatory Compliance, and ISO 15189 accreditation for facilities producing and using in-house IVDs). Until EUDAMED becomes fully operational, economic agents marketing IVDs in Spain must use AEMPS-managed registration mechanisms, and products used in Spain must carry Spanish-language labeling and documentation. This reinforces national traceability and compliance burdens alongside EU-level conformity assessment.

Competitive Landscape

The top vendors—Roche, bioMeriux, Bio-Rad Laboratories, and Danaher Corp—collectively hold significant revenue, indicating moderate concentration. Global firms leverage scale in reagents and automation, whereas Spanish specialists compete in niche molecular panels, software, and instrument service contracts. Werfen’s partnership with Seegene brings syndromic PCR portfolios under a local manufacturing umbrella, tightening lead times and easing IVDR conformity. Roche pilots bundle contracts that guarantee uptime for digital immunoassay lines, shifting risk to the supplier side.

Small- to mid-size startups focus on AI-assisted pathology and point-of-care connectivity, often collaborating with academic incubators. PERTE grants accelerate prototype validation, although many newcomers still outsource final assembly to larger contract manufacturers. Procurement decentralization leads established players to maintain region-specific sales teams, while distributors bundle multi-brand reagents to win provincial hospital bids. Technology, regulatory agility, and service quality thus become pivotal differentiators in the Spain IVD market.

Spain In-vitro Diagnostics Industry Leaders

Becton, Dickinson and Company

Bio-Rad Laboratories Inc.

F. Hoffmann-La Roche AG

Danaher Corporation (Beckman Coulter, Cepheid)

bioMerieux SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The national implementation of IVDR via Royal Decree 942/2025 creates near-term demand for services and tools that reduce compliance friction. This includes Spanish-language labeling and documentation workflows, traceability support linked to AEMPS registration while EUDAMED operability matures, and turnkey quality-management packages for manufacturers and laboratories. The decree's requirements around operating licenses, PRRC designation, and ISO 15189 expectations for in-house manufacturing also lift demand for consultancy, validation, and software that can evidence performance, post-market surveillance readiness, and auditability across multi-site hospital networks.

Digital and connected laboratory modernization is a specific pull for IVD software, middleware, and integrated automation stacks, supported by active national programs cited in the report context (Spain's Recovery and Resilience Plan and PERTE for Cutting-edge Health) and reinforced by professional bodies funding digital health tools integrated with IVD (SEMEDLAB and the Fundacion Jose Luis Castano-SEQC). With procurement decentralized across autonomous communities, suppliers that package interoperability, cybersecurity-ready connectivity, and value-based contracting into region-ready offers can address fragmentation in adoption pathways, especially for molecular and oncology diagnostics where evidence generation and data integration increasingly factor into purchasing criteria.

Recent Industry Developments

- April 2026: Sequentia Biotech announced MICK Clinical, a gastrointestinal pathogens diagnostic solution launched after achieving CE-IVD marking under the EU IVDR. The IVDR-marked launch strengthens the availability of compliant molecular testing menus for hospital and reference laboratories managing infectious-disease workflows under tighter traceability and performance expectations.

- May 2025: Miura Partners invested new capital in Saesco to scale local manufacturing of laboratory consumables. The move supports domestic supply resilience for high-throughput testing environments where reagents and consumables dominate purchasing and continuity of supply is a tender differentiator.

- October 2024: Seegene and Werfen created a Spanish NewCo to co-develop syndromic real-time PCR panels for respiratory and gastrointestinal pathogens. The joint structure brings assay development closer to local needs and procurement requirements, helping shorten lead times while aligning product documentation and lifecycle controls with IVDR compliance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Spain in vitro diagnostics market covers the value of IVD products used to test patient samples outside the body, mainly across labs, hospitals, and point-of-care settings, with revenues counted at the level of products sold into the country.

Scope exclusions: We exclude in vivo diagnostic imaging and procedures, and we also exclude pure lab services that do not include the sale of IVD products.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immunodiagnostics

- Molecular Diagnostics

- Hematology

- Microbiology

- Coagulation

- Point-of-Care (POC) Tests

- By Product

- Instruments & Analyzers

- Reagents & Consumables

- Software & Services

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Application

- Infectious Disease

- Diabetes

- Oncology (Cancer)

- Cardiology

- Autoimmune Disorders

- Other Applications

- By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

- Home-Care / Ambulatory POC Settings

- Other End-Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear demand context for Spain, so the market model does not diverge from real testing activity. We referred to public health statistics and health system publications such as the Spanish Ministry of Health, Eurostat, OECD health indicators, and the World Health Organization, which help us map disease burden, demographics, and utilization signals.

To connect demand to supply, we also reviewed regulatory and trade-facing sources such as the European Commission and Spanish medicines and health products regulator publications (for IVDR and device oversight), along with customs and import-export statistics where relevant. Company annual reports, investor presentations, association websites, and reputed press were used to cross-check product mix trends and pricing direction. In a few places, we also relied on paid subscriptions for company financials and patent databases to validate innovation pace and revenue exposure, while keeping the sizing logic reproducible. These sources are illustrative only, and many other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test the desk assumptions and narrow the input ranges around volumes, price movements, and adoption by setting. We spoke with manufacturers, distributors, laboratory decision-makers, and procurement and quality leads across Spain, then used follow-up questions where responses did not align with observed demand signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | |

| Mid tier: 50% | Functional/Unit leaders: 36% | |

| Smaller Players: 15% | Managers: 49% |

Market-Sizing & Forecasting

Sizing is built using top-down logic, where the Spain demand pool is reconstructed from testing needs and healthcare activity and then converted into product spending using realistic price and mix assumptions. In practice, we translate indicators such as aging population share, chronic disease load, infectious disease testing intensity, IVDR-driven product transition timing, and point-of-care adoption into expected test volumes and the related product pull.

After forming the country total, selective bottom-up approximations are used to keep it grounded, including sampled supplier revenue exposure to Spain, channel checks on reagent and instrument mix, and ASP times volume checks for high-usage areas like clinical chemistry and molecular diagnostics. When data is missing for smaller product lines, gaps are handled through conservative penetration ranges tied to end-user coverage (hospital labs, independent labs, and near-patient settings), then normalized to avoid double counting.

For forecasting, we used scenario analysis supported by checks on the main drivers, and the final path was selected based on what experts see as the most likely balance between testing demand, procurement constraints, and pricing progression. Year-to-year pricing was not kept flat, since reagent-heavy baskets tend to move differently than instruments, and this was reflected through separate ASP trajectories before totals were rolled up.

Data Validation & Update Cycle

Validation is done through repeated cross-checks, where outputs are compared with independent signals such as healthcare spend patterns, test demand indicators, and observed shifts in product mix. Any sharp jumps are reviewed, and assumptions are revisited if the implied volumes or pricing do not match what interview feedback and public indicators suggest.

A multi-step review happens before sign-off, including internal checks for arithmetic consistency, scope alignment, and year-to-year variance. Reports are refreshed annually, and interim updates are made when a material event changes pricing, regulation timing, or procurement behavior. Before delivery, the model gets a final pass so clients receive the latest updated view.

Mordor Intelligence's Vitro Diagnostics Spain Market Size Measured Against Other Published Estimates

Published market sizes for Spain IVD often vary, even when they appear to cover the same category, because the measurement choices are not identical. The biggest drivers are usually the year used for currency conversion, how reagent and instrument ASPs are moved over time, and whether the estimate is refreshed after procurement or regulatory changes.

In this study, the refresh cadence is treated as a sizing variable, since late-year price updates and mix shifts can move the total. The table shows how that plays out across sources, including the way Mordor Intelligence aligns FX timing and separates reagent-led ASP progression from instrument replacement cycles before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.51 B (2025) | |

| Global Consultancy A | USD 1.74 B (2024) | Uses an earlier base year and a narrower product grouping (instruments, reagents, services), which can understate adjacent IVD product categories and also locks in earlier-year pricing and FX timing. |

| Industry Publisher B | USD 2.00 B (2025) | Applies a broader regional breakdown but appears to use more averaged pricing assumptions across test types, which can compress reagent-heavy spending and reduce the impact of mix shifts in high-volume hospital labs. |

Overall, the spread is mostly explained by timing and pricing logic rather than a disagreement that Spain needs more diagnostics. By keeping the steps traceable to testing demand, end-user mix, and separate ASP tracks for major product baskets, the resulting market size stays easier to replicate and update as new signals come in.

Key Questions Answered in the Report

How large is the Spain IVD market in 2026?

The Spain IVD market size is valued at USD 2.62 billion in 2026.

What is the expected growth rate for Spain's in-vitro diagnostics through 2031?

Revenue is projected to rise at a 4.49% CAGR, reaching USD 3.27 billion by 2031.

Which test segment is expanding the fastest?

Molecular diagnostics leads with a forecast 9.38% CAGR, driven by oncology and infectious-disease panels.

Why are disposable IVD devices prevalent in Spain?

Infection-control protocols and streamlined workflows push disposable devices to an 82.75% share of total sales.

How is IVDR affecting market entry?

New conformity requirements raise documentation costs and lengthen approval timelines, especially for smaller manufacturers.

What region shows the highest adoption of digital lab technology?

Madrid and Catalonia invest most heavily in AI-enabled analyzers and data-sharing platforms under EU modernization schemes.

Page last updated on: