Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.05 Billion |

| Market Size (2026) | USD 11.35 Billion |

| Market Size (2031) | USD 13.02 Billion |

| Growth Rate (2026 - 2031) | 2.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Furniture Market Analysis by Mordor Intelligence

The Spain Furniture market size was valued at USD 11.05 billion in 2025 and estimated to grow from USD 11.35 billion in 2026 to reach USD 13.02 billion by 2031, at a CAGR of 2.76% during the forecast period (2026-2031). Momentum stems from a rebound in residential renovations, a sharp resurgence in tourism-led hospitality refurbishments, and rising acceptance of omnichannel shopping models that blend in-store engagement with e-commerce convenience. Demand is also supported by EU-funded energy-efficiency retrofits that incentivize home upgrades, while value-oriented Scandinavian-design chains enlarge their Spanish footprints to capture price-sensitive consumers. Meanwhile, urban downsizing and sustainability preferences steer households toward modular, recycled, and circular-economy offerings, prompting manufacturers to recalibrate material choices and packaging formats. Supply-side conditions remain mixed: input-cost swings in wood, metal, and logistics squeeze margins for small workshops, yet scale-driven retailers negotiate global contracts that buffer volatility and sustain competitive pricing[1]Horváth Partners, “International Market Study on Raw Material Prices,” horvath-partners.com..

Key Report Takeaways

- By application, Home Furniture led with 72.45% of the Spain Furniture market share in 2025; Hospitality Furniture is forecast to advance at a 3.96% CAGR to 2031.

- By material, wood held 60.20% of the Spain Furniture market share in 2025, while plastics and polymers are projected to expand at the fastest 4.37% CAGR through 2031.

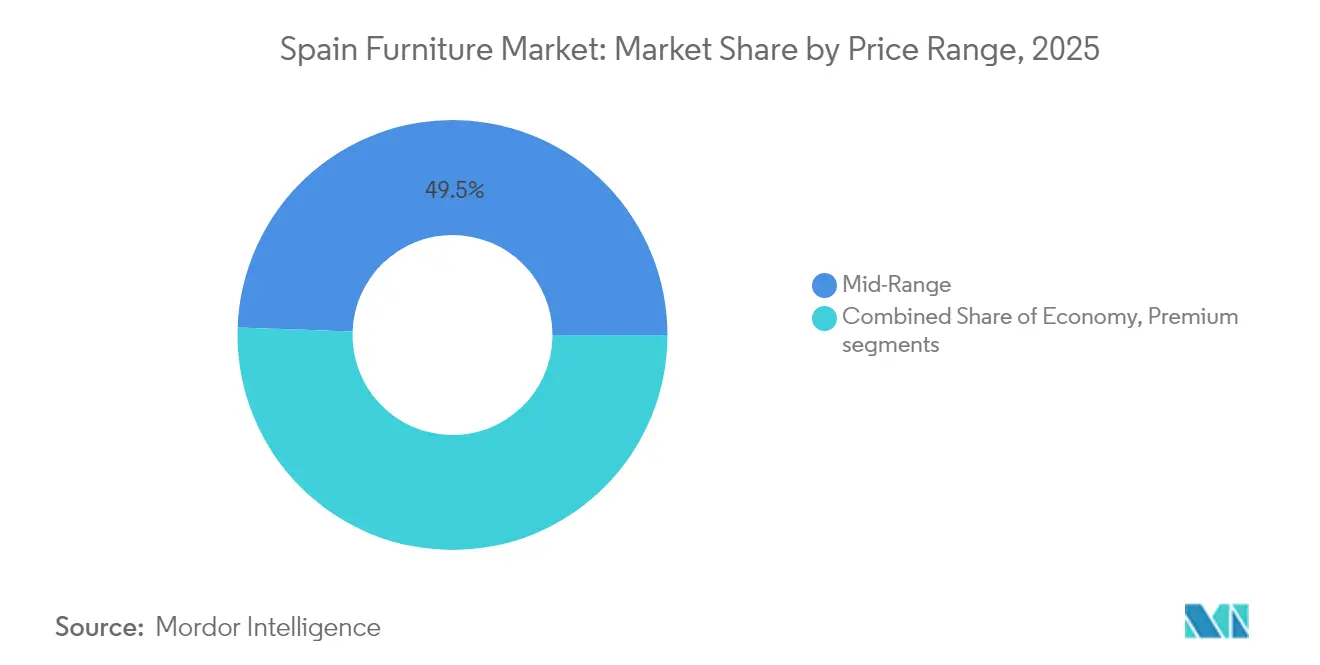

- By price range, the mid-range tier accounted for 49.45% of the Spain Furniture market size in 2025, yet the premium tier is poised to rise at a 4.18% CAGR between 2026-2031.

- By distribution channel, B2C/Retail controlled 80.05% of the Spain Furniture market share in 2025; online-enabled omnichannel formats are on track for a 4.09% CAGR over the forecast horizon.

- By region, Catalonia captured 21.90% of the Spanish furniture market share in 2025, whereas the Balearic and Canary Islands are set to record the swiftest 3.96% CAGR thanks to tourism-driven hospitality refurbishments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential construction rebound & renovation boom | +0.8% | Nationwide focus on Madrid, Catalonia, Valencia | Medium term (2-4 years) |

| Tourism-led hospitality refurbishment cycle | +0.6% | Balearic & Canary Islands, Andalusia coasts, Madrid | Short term (≤ 2 years) |

| Omnichannel & e-commerce penetration surge | +0.5% | Large urban areas nationwide | Medium term (2-4 years) |

| Value-oriented Scandinavian-design retail expansion | +0.4% | National, led by IKEA and JYSK store rollouts | Short term (≤ 2 years) |

| EU-funded energy-efficiency retrofits | +0.3% | Older housing stock in northern Spain, Catalonia, and urban centers | Medium term (2–4 years) |

| Second-hand & circular-economy trade-in platforms | +0.2% | Urban and suburban areas with high renter populations (e.g., Barcelona, Madrid) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Residential Construction Rebound & Renovation Boom

Building permits exceeded 127,000 units in 2024, outpacing sector capacity and signalling strong refurbishment pipelines that will translate into furniture purchases through 2027. Spain logged 1.85 million scheduled home renovations for 2025 after years of under-building, redirecting demand from new housing to interior upgrades. Construction costs climbed 4.20% in 2024, making retrofits more cost-effective than new builds and spurring appetite for modular cabinets, wardrobes, and space-saving seating. The Spain Furniture market benefits because renovations prompt whole-room refurnishing rather than piecemeal replacement. EU Recovery funds earmarked for energy-efficient retrofits further enlarge budgets for quality furnishings that complement thermal upgrades. Manufacturers with rapid-fit, customizable lines are best positioned to monetize the renovation wave.

Tourism-Led Hospitality Refurbishment Cycle

International arrivals rebounded to 93.8 million in 2024, restoring the cash flow hotels need for property upgrades[2]DatosMacro, “España: Turismo 2024,” datosmacro.expansion.com. Tourism services generated a 4.20% of GDP surplus, enabling chains such as RIU and Radisson to accelerate multi-million-euro refurbishments that soak up contract-grade furniture. Islands heavy on short-term rentals, Balearic and Canary, present concentrated demand where replacement cycles run every 3-4 years, far quicker than residential averages. Suppliers secure higher margins on hospitality orders because buyers prioritize durability and uniform aesthetics. Logistic advantages arise when manufacturers cluster deliveries to tourism zones, trimming transport costs. The Spain Furniture market therefore, captures elevated per-unit spending in coastal hospitality corridors.

Omnichannel & E-Commerce Penetration Surge

Spanish consumers increasingly research online before visiting showrooms, pushing retailers to synchronize inventory visibility, AR planning tools, and click-and-collect services. Online furniture sales growth outpaces total retail as shoppers grow comfortable with virtual room simulators that mitigate the tactile barrier. IKEA’s potential Vitoria-Gasteiz outlet and JYSK’s 30-store 2025 rollout both hinge on seamless app-to-store experiences that lift conversion rates. Smaller chains adopt marketplace integrations to tap digital traffic without heavy tech investment. As checkout journeys shift online, data analytics empower retailers to personalize promotions and manage stock, fostering repeat purchases that sustain the Spain Furniture market.

Value-Oriented Scandinavian-Design Retail Expansion

Nordic retailers resonate with Spanish households that prefer minimalist, space-efficient designs suited to shrinking average household size, projected at 2.32 persons by 2039[3]INE, “Population Projections 2024-2074,” ine.es. Flat-pack formats compress shipping volumes, enabling low-cost home delivery nationwide and reinforcing competitive pricing. IKEA’s 24% market leadership showcases the formula: standardized SKUs, global procurement, and strong sustainability narratives. JYSK targets a 300-store scale to narrow the gap, intensifying price competition yet expanding consumer choice. Domestic manufacturers respond by blending Spanish craftsmanship with Nordic aesthetics to defend their share. The result is wider design diversity that keeps the Spain Furniture market vibrant.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Input-cost volatility in wood & logistics | −0.4% | Valencia manufacturing cluster is heavily exposed | Short term (≤ 2 years) |

| Import-price pressure on fragmented local makers | −0.3% | Traditional production hubs nationwide | Medium term (2-4 years) |

| Demographic drag from aging & low household formation | −0.2% | Rural interior provinces | Long term (≥ 4 years) |

| Tightened fire-safety & eco-design compliance costs | −0.2% | Nationwide, driven by EU regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Input-Cost Volatility in Wood & Logistics

Raw material price inflation poses significant margin pressure on Spanish furniture manufacturers, with wood prices experiencing potential increases up to 30% by year-end 2025 according to European manufacturing surveys, while steel could rise 25% and plastics at least 20%. Although pine timber prices have fallen EUR 4-10 (USD 4.28–10.70) per tonne since March 2023, the underlying volatility creates planning difficulties for manufacturers who must balance inventory costs against supply security. Logistics costs compound these pressures, with land prices for logistics facilities rising 1.70% in 2024 and rental rates increasing 3.70%, directly impacting furniture distribution networks that rely on large-format warehousing. The combination of material and logistics inflation disproportionately affects smaller, fragmented Spanish manufacturers who lack the purchasing power and vertical integration of multinational competitors.

Demographic Drag from Ageing & Low Household Formation

Spain's demographic transition presents a structural headwind for furniture demand, with the population aged 65+ reaching 20.40% in December 2024 and the old-age dependency ratio hitting a record high of 30.80%[4]Trading Economics, “Spain – Population Aged 65 and Over,” tradingeconomics.com. . While total households are projected to grow from 19.3 million in 2024 to 23 million by 2039, the increase is driven primarily by single-person households rising to 33.50% of the total, indicating smaller average household sizes and reduced per-household furniture consumption. The aging population tends to reduce furniture replacement frequency as older consumers prioritize durability over style updates and downsize living spaces rather than expand them. Rural and interior regions face particularly acute demographic challenges as younger populations migrate to urban centers for employment, leaving behind aging communities with limited furniture purchasing power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Residential Scale and Hospitality Upside

Home Furniture dominated the Spain Furniture market with a 72.45% revenue stake in 2025, reflecting Spanish households’ deep cultural investment in living-space aesthetics. That leadership is forecast to expand at only 3.38% CAGR as replacement cycles lengthen, but it still anchors overall growth because renovation spending converts into whole-room re-furnishing orders. Sofas, dining sets, and modular storage remain staples, although urban apartments spur demand for collapsible tables and wall-mounted shelving. Hospitality Furniture trails in absolute size yet races ahead at a projected 3.96% CAGR, as hotel groups, short-term rentals, and boutique hostels refresh interiors to meet global guest expectations. Spain's Furniture market size for hospitality is expected to edge up each year as the Canary and Balearic Islands upgrade aging room inventories. Suppliers seeking stability hedge by serving both residential and contract pipelines, smoothing seasonal tourism swings.

The applications portfolio is diversifying into office, educational, and healthcare categories as hybrid work, school modernization, and hospital expansions progress. Office purchases skew toward ergonomic chairs and height-adjustable desks that accommodate flexible working styles, although volumes remain small compared to household needs. Educational furniture captures public-sector tenders focused on collaborative classroom layouts, while healthcare demand centers on antimicrobial surfaces and mobility aids. Even within niche segments, Spain Furniture market share gains accrue to brands offering rapid customization, strict certification, and clear sustainability credentials.

By Material: Wooden Heritage Meets Polymer Innovation

Wood retained a 60.20% share in 2025, underpinned by Valencia’s centuries-old carpentry cluster and consumer affinity for natural finishes. Spain Furniture market size for wooden pieces is expected to inch forward, but relinquish a few points as recycled plastics gain acceptance. Polymer furniture, growing at a brisk 4.37% CAGR, benefits from lower cost, weather resistance, and design flexibility, making it popular for outdoor terraces and budget apartments. Manufacturers like Actiu showcase chairs moulded from recycled fruit crates, reinforcing circular-economy storytelling.

Metal retains a niche in office frames and hospitality fixtures where durability trumps weight concerns. Composite panels and engineered woods widen in cabinetry, blending resource efficiency with strength. EU eco-design directives accelerate the pivot toward FSC-certified timber and traceable recycled content, reshaping supply chains. Compliance introduces documentation costs but also differentiates brands that validate sustainable sourcing. Consequently, Spain's Furniture market share is likely to tilt toward material innovators capable of meeting strict environmental benchmarks without eroding affordability.

By Price Range: Mid-Range Core and Premium Lift

Mid-range products captured 49.45% of 2025 revenue as households balance style aspirations with tight discretionary budgets. Value-oriented Scandinavian chains anchor this tier via standardized SKUs, flat-pack logistics, and self-assembly instructions that compress the total cost of ownership. Even so, the premium tier is on course for a 4.18% CAGR because affluent buyers in Madrid, Barcelona, and coastal resorts elevate spending on artisan craftsmanship, FSC woods, and bespoke upholstery. Spain Furniture market size for premium lines remains modest but yields higher margins, enticing domestic brands like Andreu World to double down on design awards and export channels.

At the other end, economy products cater to student rentals and secondary residences; however, rising freight and raw-material costs strain margins, prompting some discounters to rationalize SKUs or adopt lighter flat-pack designs. Price polarization intensifies middle-class consumers gravitate to promotional bundles, while high-net-worth households seek experiential retail experiences with interior-design consultations. The segmentation underscores divergent paths within the Spain Furniture market, compelling companies to specialize rather than straddle all price points.

By Distribution Channel: Omnichannel Supremacy

B2C/Retail accounted for 80.05% of the 2025 value as Spanish shoppers still prefer tactile inspections before large-ticket purchases. Nonetheless, web traffic guides showroom visits, so retailers synchronize real-time stock data and flexible payment tools to close sales. Spain's Furniture market share for online-only transactions is small but growing inside omnichannel ecosystems, pushed by mobile-first millennials who appreciate AR room planners and doorstep delivery. B2B/Project channels, while smaller, spike when hotel refurbishments or office fit-outs bundle bulk orders with tight timelines.

Home-center chains reinvent store layouts into experience hubs where curated vignettes encourage add-on sales. Meanwhile, pure-play e-tailers such as Sklum leverage rapid dropship partnerships to expand catalogues without inventory risk, enticing impulsive purchases. Last-mile logistics is a battleground: same-day delivery in Madrid and Barcelona sets customer expectations that ripple nationwide. Firms mastering reverse logistics for returns and trade-ins will unlock repeat business and reinforce the Spain Furniture market.

Geography Analysis

Catalonia generated 21.90% of 2025 sales, buoyed by Barcelona’s design culture, export-ready workshops in Girona and Tarragona, and robust household incomes. Its diversified manufacturing ecosystem balances residential demand with contract export orders to France and Italy, fortifying resilience. Madrid ranks second, leveraging the nation’s highest GDP per capita of EUR 42,198 (USD 45,152) and dense populations of new apartment dwellers seeking turnkey furnishings. Valencian Community benefits from entrenched production know-how but contends with cost inflation that tests competitiveness.

The Balearic and Canary Islands headline growth at 3.96% CAGR, where hotel refurbishments and short-term rentals renew interiors every few years, pushing high-value, quick-turnaround contracts. Logistic premiums are offset by pricing power as island operators prioritize supplier reliability. Andalusia contributes sizeable volume via its large population and coastal tourism assets, even though average ticket sizes trail northern regions. Remaining autonomous communities round out national coverage, with demand patterns tied closely to local economic conditions and aging dynamics. Combined, these geographic strands weave a balanced Spain Furniture market with both mature cores and high-growth fringes.

Competitive Landscape

The Spain furniture market shows moderate concentration, with the top five players controlling a significant share. IKEA Ibérica leads by combining standardized Scandinavian designs, global sourcing advantages, and an efficient click-and-collect system that simplifies bulky-item logistics. JYSK is rapidly expanding, with plans for over 30 new stores in 2025, using aggressive real estate strategies and localized marketing that emphasizes its Danish roots. Conforama España, now owned by XXXLutz, competes through deep discounts and fast product rotation, benefiting from pan-European purchasing power to manage cost pressures. These major players rely on scale and strategic positioning to maintain their competitive edge.

Mid-tier domestic brands like Sklum and Kave Home focus on e-commerce niches, appealing to millennial renters with trend-driven, Instagram-ready designs. Operating asset-light models, they minimize inventory risks by using rapid dropshipping logistics, but must invest heavily in digital marketing to sustain customer traffic. Meanwhile, premium manufacturers such as Andreu World and Actiu differentiate through sustainability, offering FSC-certified products, recycled materials, and award-winning ergonomic designs. Their client base includes corporate buyers and international distributors, reinforcing their strong export orientation. This tiered structure highlights the diversity of market approaches depending on target demographics and channel strategies.

Strategic developments emphasize the sector’s ongoing evolution. Actiu’s 2025 debut of the Fluit chair—made from recycled fruit crates—illustrates innovation rooted in sustainability. Andreu World leverages ISO-certified production to attract eco-conscious designers abroad, strengthening its global appeal. IKEA’s plans to expand into locations like Vitoria-Gasteiz reflect continued commitment to physical retail, even as online shopping grows. These moves show how sustainability, omnichannel presence, and operational scale are becoming key drivers of long-term success in Spain’s furniture market.

Spain Furniture Industry Leaders

IKEA Ibérica

Conforama España

JYSK Spain

El Corte Inglés (Home & Decor)

Sklum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Thermador Groupe opened exclusive talks to acquire Quilinox for EUR 14.6 million (USD 15.62 million) in revenue, highlighting continued foreign investment in Spanish industrial suppliers.

- February 2025: JYSK Spain confirmed plans to open 30+ stores during 2025, driving toward a 300-location network nationwide.

- January 2025: Cosentino announced a USD 430 million investment for 2025-2027 capacity expansion in premium surface materials.

- December 2024: European Commission adopted the Ecodesign for Sustainable Products Working Plan 2025-2030, earmarking furniture for delegated acts by 2028.

Spain Furniture Market Report Scope

Furniture comprises portable objects designed to support various human activities. This report provides a comprehensive analysis of the Spanish furniture market, including national accounts, economic landscape, and emerging segment trends. It also examines significant shifts in market dynamics and presents an overall market overview.

The Spanish furniture market is segmented by material, application, and distribution channel. By material, the market is segmented into wood, metal, plastic, and other materials. By application, the market is segmented into home furniture, office furniture, hospitality furniture, and other applications. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online platforms, and other distribution channels. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Application

| Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | |

| Beds | |

| Wardrobe | |

| Sofas | |

| Dining Tables/Sets | |

| Kitchen Cabinets | |

| Other Home Furniture | |

| Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas & Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Retail Channels | |

| B2B/Project |

By Region

| Catalonia |

| Andalusia |

| Community of Madrid |

| Valencian Community |

| Balearic & Canary Islands |

| Remaining Autonomous Communitie |

| By Application | Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | ||

| Beds | ||

| Wardrobe | ||

| Sofas | ||

| Dining Tables/Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture | ||

| Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas & Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Retail Channels | ||

| B2B/Project | ||

| By Region | Catalonia | |

| Andalusia | ||

| Community of Madrid | ||

| Valencian Community | ||

| Balearic & Canary Islands | ||

| Remaining Autonomous Communitie | ||

Key Questions Answered in the Report

How big is the Spain Furniture market in 2026?

It is valued at USD 11.35 billion, with a projected 2.76% CAGR to 2031.

Which application category sells the most units?

Home Furniture accounts for roughly 72.45% of 2025 revenue due to ongoing residential renovations and replacement purchases.

Which region is growing fastest for furniture sales?

The Balearic and Canary Islands are projected to grow at a 3.96% CAGR because of tourism-driven hotel and rental refurbishments.

What material segment is gaining share quickest?

Plastics and polymers are expanding at a 4.37% CAGR thanks to affordability, lightweight properties, and recycled content innovations.

How is e-commerce influencing furniture retail in Spain?

Online research now precedes most store visits, driving omnichannel models that link virtual showrooms with click-and-collect or home delivery services.

What sustainability rules will impact Spanish furniture makers?

The EU Ecodesign for Sustainable Products framework will introduce recyclability and recycled-content mandates for furniture by 2028, raising compliance requirements.

Page last updated on: