Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

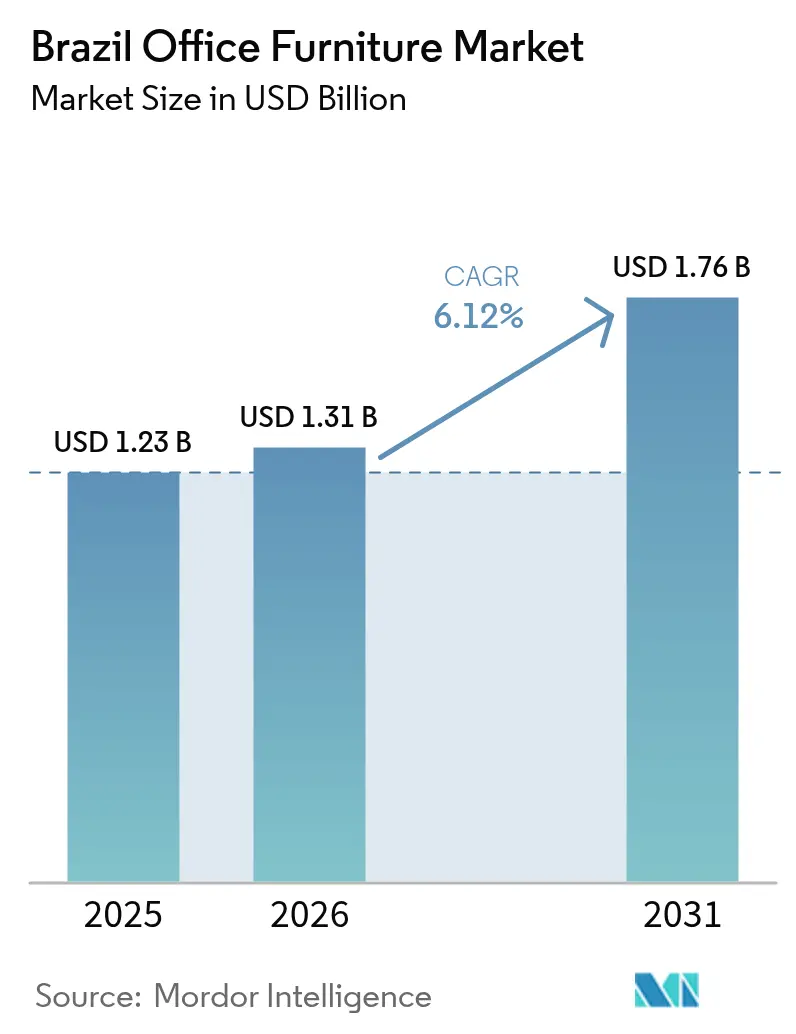

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Office Furniture Market Analysis by Mordor Intelligence

The Brazil office furniture market size is expected to grow from USD 1.23 billion in 2025 to USD 1.31 billion in 2026 and is forecast to reach USD 1.76 billion by 2031 at 6.12% CAGR over 2026-2031. Demand accelerates as hybrid-work policies, flexible occupancy contracts, and rising corporate wellness budgets converge to reshape workspace planning. Employers now treat ergonomic compliance as a productivity lever, fueling orders for height-adjustable desks and certified seating that meet NR17 requirements. Co-working operators are scaling beyond first-tier metros, and virtual-office subscriptions remain three times higher than pre-pandemic levels. Regional vacancy compression in São Paulo underscores the move from expansionary leasing to retrofit activity that favors modular, reconfigurable furniture. Meanwhile, federal tax incentives for FSC-certified timber and falling steel prices encourage domestic manufacturers to modernize plants and compete on sustainability credentials[1]Ana Luiza Tieghi & Paula Martini, “Escritórios em SP têm menor vacância desde a pandemia,” Valor Econômico, valor.globo.com.

Key Report Takeaways

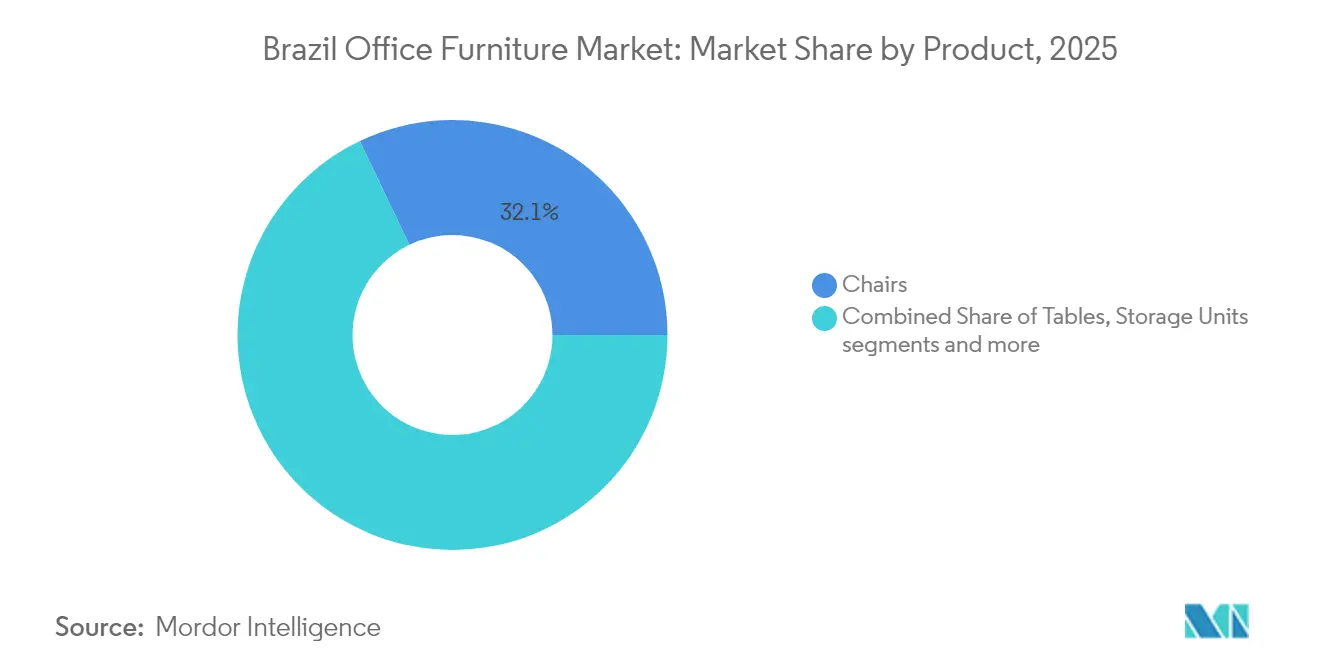

- By product category, chairs led with 32.10% Brazil office furniture market share in 2025, while tables are projected to expand at a 6.45% CAGR through 2031.

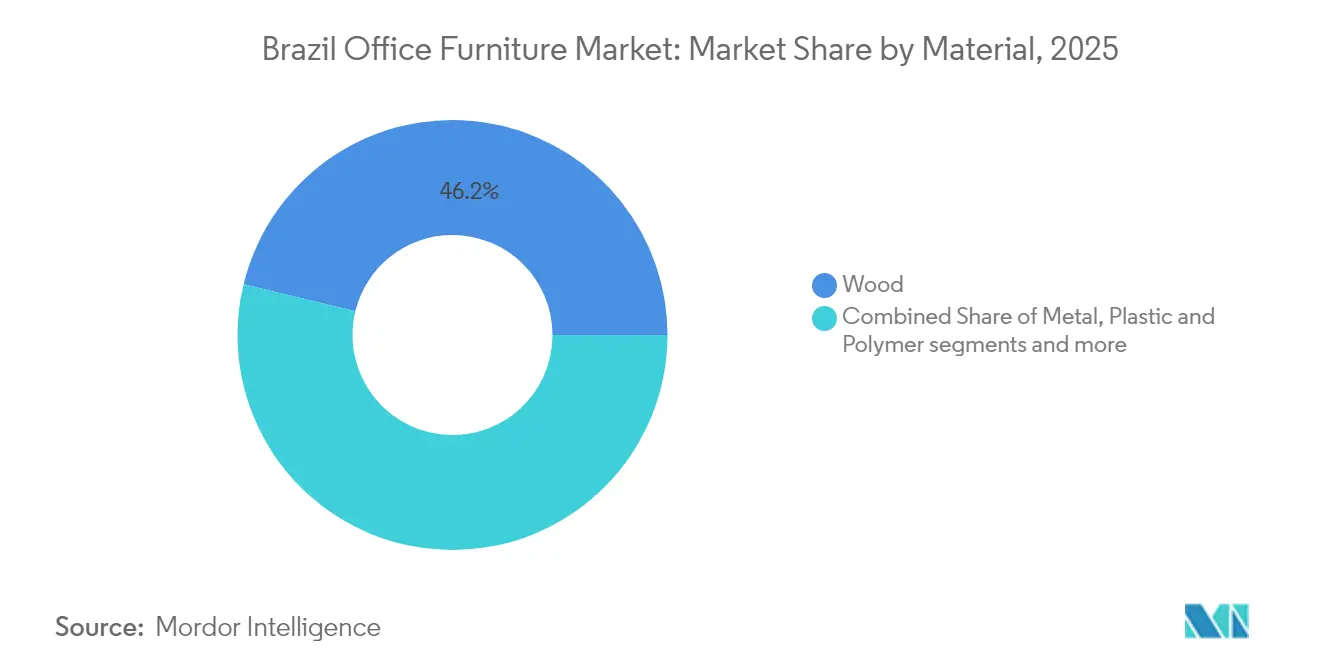

- By material, wood accounted for 46.20% of the Brazil office furniture market size in 2025; plastic & polymer is set to post the fastest 6.55% CAGR over 2026-2031.

- By price range, the economy segment captured 52.80% revenue in 2025, yet mid-range products are on track for a 6.33% CAGR to 2031.

- By end-user, corporate offices commanded 50.90% of the Brazil office furniture market size in 2025, whereas healthcare offices are forecast to grow at a 6.92% CAGR.

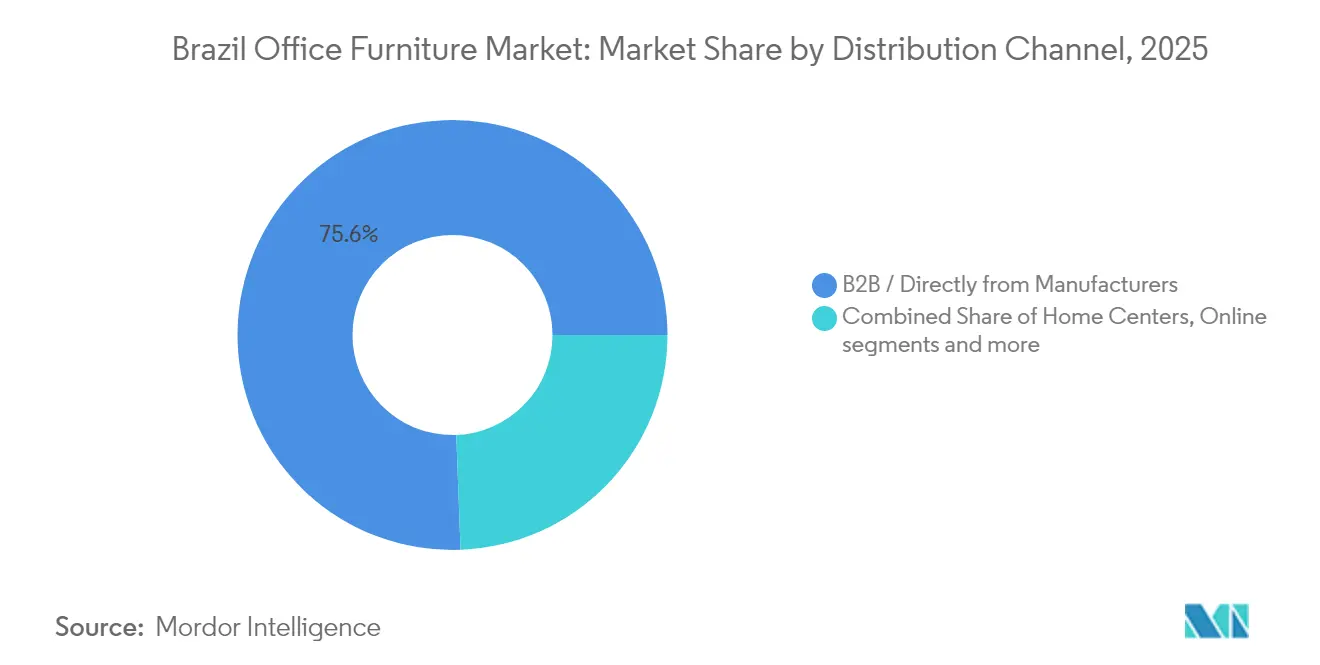

- By distribution channel, B2B direct sales held 75.60% of the Brazil office furniture market share in 2025 and will maintain a 6.52% CAGR through 2031.

- By geography, the Southeast led with 50.70% revenue in 2025; the North region is projected to log the fastest 6.66% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-work adoption is fueling ergonomic demand | +1.8% | National; São Paulo, Rio de Janeiro, Belo Horizonte | Medium term (2-4 years) |

| Corporate investment in employee well-being & productivity | +1.5% | Southeast & South; tier-2 expansion | Long term (≥ 4 years) |

| Expansion of co-working & flex-office footprints | +1.2% | Metros extending to Campinas, Florianópolis, Curitiba | Short term (≤ 2 years) |

| Tax-credit incentives for FSC-certified wood sourcing | +0.8% | Nationwide, Santa Catarina, Paraná producers | Long term (≥ 4 years) |

| Near-shore BPO growth in tier-2 Brazilian cities | +0.7% | Interior São Paulo, Minas Gerais, Rio Grande do Sul | Medium term (2-4 years) |

| Digital procurement platforms easing SMB access | +0.4% | National; higher in Southeast & South | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hybrid-work adoption is fueling ergonomic demand

Hybrid work has altered the logic of space allocation, pushing companies to retrofit existing floors rather than lease new ones. Office layouts now include hot-desking hubs, quiet booths, and collaboration corners that share adjustable furniture in constant rotation. Because each station may host multiple users, NR17-compliant chairs with intuitive levers have become a procurement staple, and vendors highlight certification to pre-empt labor-inspection penalties. Facility managers specify sit-stand desks to encourage movement and reduce sedentary fatigue, aligning with wellness dashboards tracking musculoskeletal claims[2]JLL, “Designing workplaces to drive success,” us.jll.com. Audio-visual integration shapes table demand because conference surfaces must conceal cabling and position cameras at eye level for hybrid meetings. Foam suppliers report higher density-grade orders, while fastener makers see uptake in quick-lock mechanisms that enable daily reconfiguration. Collectively, ergonomic furniture has shifted from discretionary spend to baseline infrastructure across the Brazil office furniture market.

Corporate investment in employee well-being & productivity

Brazilian employers frame workspace quality as a talent-retention tool, bundling furniture upgrades with mental-health initiatives and ESG scorecards. Procurement teams move from price-per-unit to whole-life-cost analyses that consider warranty length and recyclability. Vendors offering take-back programs gain preference because they help companies meet waste-reduction targets. Biophilic design enters the mainstream brief as projects request timber accents and natural fabrics to moderate cognitive fatigue. On-site physio consultations audit chair settings, reinforcing links between ergonomic adherence and lower absenteeism. As wellness targets enter quarterly KPIs, furniture budgets shift from capex to multi-year operational envelopes tied to health metrics.

Expansion of co-working & flex-office footprints

Virtual-office clientele has tripled versus pre-pandemic benchmarks, underscoring demand for flex-space solutions. Operators demand furniture with universal aesthetics, durable laminates, and tool-free assembly that accelerates tenant turnover. As the model penetrates tier-2 cities, local installers partner with national manufacturers to meet 48-hour fit-out timelines embedded in leases. Fabric mills develop easy-clean textiles that pass stringent rub tests, responding to hospitality-inspired interior palettes. Co-working chains influence retail perception; freelancers who frequent these spaces later purchase familiar brands for home offices, creating a halo effect.

Tax-credit incentives for FSC-certified wood sourcing

Law 14,789/23 reduces import duties on woodworking machinery and accelerates depreciation for domestically produced equipment, driving manufacturers to enhance production capabilities[3]PwC, “Brazil – Corporate tax credits and incentives,” taxsummaries.pwc.com. FSC-certified sawmills are utilizing these incentives to install CNC routers, which optimize material usage and enable the production of complex geometries. Export-driven brands are emphasizing certified material provenance on their specification sheets to ensure compliance with the EUDR[4]ATIBT, “ATIBT strengthens ties with Brazil's forestry sector,” atibt.org. The inclusion of deforestation-free clauses in tenders by large corporate buyers has made FSC certification a critical factor for securing national contracts. These developments are expected to strengthen the adoption of sustainable practices across the woodworking industry. Additionally, the policy changes are likely to boost investments in advanced machinery, further improving operational efficiency and competitiveness in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel & lumber prices | -1.4% | National, acute on metal-furniture makers | Short term (≤ 2 years) |

| Cyclical corporate CAPEX cuts | -0.9% | Southeast & South | Medium term (2-4 years) |

| Port-side logistics bottlenecks | -0.6% | Santos and Rio de Janeiro ports | Short term (≤ 2 years) |

| BYO-furniture trend among gig workers | -0.3% | Metros with high freelancer density | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile steel & lumber prices

Global steel prices have declined; however, the anticipated cost savings are limited due to currency volatility and freight surcharges. Engineered-wood producers are encountering similar challenges, as imported veneers are invoiced in U.S. dollars, exposing them to exchange rate risks. To mitigate cost fluctuations, manufacturers are adopting dual-sourcing strategies and entering into quarterly supply contracts. These measures aim to stabilize procurement expenses and ensure supply chain reliability. Additionally, designers are exploring hybrid construction methods to reduce dependency on individual commodities. Such approaches are becoming critical in navigating the volatile pricing environment across global markets.

Cyclical corporate CAPEX cuts

Economic slowdowns have led CFOs to impose freezes on furniture upgrades, extending replacement cycles beyond typical depreciation schedules. Facility management teams are prioritizing cost-effective solutions, such as repair kits, over complete furniture replacements. Refurbishment services are experiencing increased demand, ensuring production lines remain operational. Sales teams are adapting their strategies by targeting pilot zones, where upgrades are positioned as critical investments in productivity rather than optional expenditures. This approach aims to align with budget constraints while emphasizing long-term value. The shift in strategy reflects a broader trend of prioritizing efficiency and cost management in response to market conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Tables Drive Workspace Reconfiguration

Chairs retained 32.10% of the Brazil office furniture market share in 2025, underscoring their role as the baseline purchase for every workstation. The segment’s momentum stems from mandatory NR17 compliance, which obliges buyers to specify height-adjustable seats with lumbar support and high-density foam. Even so, tables are poised for faster expansion; they are forecast to register a 6.45% CAGR between 2026 and 2031 as companies redesign floorplates for hybrid collaboration zones and technology-integrated conference rooms. Demand spikes for flip-top training tables, mobile conference slabs with embedded power ports, and sit-stand desks that accommodate different employee height profiles, pushing vendors to standardize modular leg systems and quick-lock casters.

As hybrid scheduling reshapes utilization patterns, ancillary surfaces-side tables, laptop carts, credenzas-also gain prominence because they allow workers to switch tasks without relocating. The surge in table orders catalyzes follow-on demand for cable-management kits and under-desk storage accessories that maximize legroom in shared stations. Chairs, meanwhile, evolve toward auto-tension mechanisms and breathable mesh backs to cope with multiple daily users. Together, these dynamics position tables as the structural backbone of activity-based layouts, while chairs continue to serve as the ergonomic cornerstone of the overall Brazil office furniture market size.

By Material: Plastic Innovation Challenges Wood Dominance

Wood commanded 46.20% of revenue in 2025, holding its status as the preferred finish for executive suites and reception counters that rely on warm aesthetics to convey brand gravitas. Manufacturers leverage FSC-certified supplies to satisfy ESG clauses, ensuring the segment’s endurance even as buyers diversify their material palettes. The competitive edge for wood also lies in machining versatility, which enables intricate veneer inlays and curved forms now popular in biophilic interiors.

Plastic and polymer lines are set to outpace every other material group, advancing at a 6.55% CAGR through 2031 as designers embrace glass-fiber shells and post-consumer resins that provide lightweight durability without sacrificing premium finishes. The growth of this category is reinforced by rising freight costs that favor lighter freight classes and by heightened demand for bold pastel colorways that polymers can achieve without secondary painting. Metal frames continue to feature inside desk skeletons and chair bases, but their share fluctuates with commodity-price swings, encouraging hybrid constructions that marry wood accents with polymer edges. These trends reveal a maturing buyer mindset that balances sustainability targets with long-term durability expectations, reallocating spend within the overall Brazil office furniture market share rather than cannibalizing it.

By Price Range: Mid-Range Segment Captures Quality Migration

Economy products captured 52.80% of 2025 demand, illustrating that cost efficiency remains central for small and mid-sized enterprises operating on tight budgets. Buyers in this tier gravitate toward locally fabricated desks and stackable chairs that promise fast delivery and easy replacement. However, mid-range furniture is forecast to expand at a 6.33% CAGR over 2026-2031 as procurement teams shift focus from upfront sticker price to lifecycle economics that factor in warranty length, repairability, and resale value.

Mid-tier vendors are responding by importing high-function mechanisms-synchronous tilts, memory-height presets-then marrying them with locally sourced frames to moderate cost. Premium offerings, often imported from U.S. and European brands, keep influencing design language across the spectrum, but their uptake is constrained to marquee headquarters and design studios. Refurbished premium chairs trading on secondary platforms at discounted rates blur traditional tier lines, enabling budget-conscious firms to access high-end ergonomics. This tier interplay suggests a gradual quality migration that will shrink the absolute gap between economy and mid-range specifications while preserving clear segmentation within the Brazil office furniture market.

By End-User: Healthcare Offices Lead Growth Acceleration

Corporate offices held 50.90% of revenue in 2025, fueled by hybrid-work retrofits that roll out hot-desking and collaboration nooks across headquarters campuses. These projects prioritize adjustable desks, acoustic dividers, and power-ready tables that can be re-plotted overnight, keeping contract flows steady for full-line vendors. Healthcare facilities, on the other hand, are projected to record the highest 6.92% CAGR by 2031 as public and private hospital networks launch expansion phases to meet aging-population needs.

Ergonomic stools, antimicrobial vinyl-covered task chairs, and height-variable nurse-station desks top the healthcare shopping list, widening the product mix that manufacturers must stock. Educational institutions supply a reliable but slower-moving pipeline, constrained by government budget cycles yet gradually pivoting toward collaborative library layouts that echo corporate agile zones. Government and municipal offices remain price-conscious, though NR17 enforcement ensures baseline quality standards. The diversified customer spread cushions suppliers against cyclical shocks, creating a multi-sector shield for sustaining the Brazil office furniture market share.

By Distribution Channel: Direct Sales Dominate Corporate Relationships

B2B direct sales from manufacturers accounted for 75.60% of 2025 turnover and are forecast to climb at a 6.52% CAGR because large enterprises value end-to-end accountability in design, delivery, and maintenance. These contracts often embed space-planning services, asset-tagging, and periodic ergonomic audits, creating recurring revenue beyond the initial furniture drop. Project-management portals allow facility managers to track milestones, installation crews, and punch-list resolutions in real time, a level of transparency seldom matched by third-party dealers.

Retail and e-commerce channels split the remaining share, catering to freelancers, startups, and branch locations that place small-batch orders requiring immediate dispatch. Marketplace listings of certified refurbished chairs deliver brand-name ergonomics at accessible prices, strengthening the circular economy narrative. Home-center chains showcase office vignettes that double as educational displays on seat-height norms and monitor placement, subtly upselling accessories like footrests and anti-fatigue mats. Collectively, this channel blend ensures comprehensive market reach, anchoring the overall Brazil office furniture market size while empowering different buyer archetypes to procure on their own terms.

Geography Analysis

The Southeast region remains the gravitational center of the Brazil office furniture market, capturing 50.70% of revenue in 2025, thanks to the dense concentration of corporate headquarters and design studios clustered around São Paulo and Rio de Janeiro. Retrofit activity is brisk: Grade-A towers in São Paulo now prioritize lounge-style collaboration zones over traditional cubicles, and vacancy in the city dropped to its lowest post-pandemic level of 18.3% in Q1 2025, signaling that tenants are refreshing interiors rather than expanding footprints. Local upholstery mills benefit from short-run orders that demand custom colorways and rapid turnaround, reinforcing the region’s reputation for design agility.

Momentum is shifting northward as well. The North region is forecast to log the fastest 6.66% CAGR through 2031, powered by near-shore BPO operators setting up large call-center hubs in Manaus and Belém that require dense layouts of ergonomic chairs and compact desks. Federal free-zone incentives trim import duties on IT hardware, prompting multinationals to co-locate furniture purchases in the same logistics corridors to shorten lead times. Suppliers respond by establishing micro-warehouses near river ports and tapping indigenous design cues-such as woven-fiber backrests-to distinguish product lines while honoring local culture.

Elsewhere, growth unfolds along multiple, more measured paths. The Northeast benefits from tourism-linked refurbishments in Salvador and Fortaleza, where hotels convert back-office spaces into co-working lounges for digital nomads. Central-West demand tracks agribusiness diversification: new regional headquarters in Goiânia and Cuiabá commission mid-range fit-outs that balance cost control with brand presentation. In the South, vertically integrated manufacturers leverage Santa Catarina’s forestry ecosystem to prototype certified-wood desks with minimal transport emissions, then export surplus production to Mercosur neighbors via well-developed road networks. Together, these regional narratives create a geographically diversified revenue base that buffers the national market against localized economic shocks.

Competitive Landscape

The Brazil office furniture market exhibits moderate fragmentation with domestic manufacturers competing alongside international brands through authorized distributors and direct operations. Domestic stalwarts such as Flexform anchor their market presence by fusing Italian-inspired styling with local manufacturing, a blend that insulates clients from currency volatility while preserving design cachet. Showrooms serve as collaborative labs where architects and facility managers co-create prototypes, allowing rapid iteration and reinforcing deep, consultative relationships. Regional competitors like Marelli and Cavaletti sustain relevance through flexible production cells that can shift quickly from large corporate orders to bespoke color runs for boutique projects, illustrating how operational agility competes head-to-head with brand heritage.

International labels—among them Herman Miller and Haworth—maintain premium positioning by enforcing rigorous showroom standards, ensuring that Brazilian clients experience identical acoustics, ergonomics, and material palettes to those found in New York or Milan. Haworth’s recent consolidation of luxury subsidiaries under the Haworth Lifestyle banner broadens its reach into lounge and hospitality categories, signaling a strategy to embed the brand across the full spectrum of workspace touchpoints. These global players lean on local distributors for after-sales service, blending international design language with domestic customer-support networks.

A newer cohort of digital-native challengers is reshaping go-to-market dynamics. Some focus on direct-to-consumer flat-pack desks promoted through social-media storytelling, capitalizing on the growing BYO-furniture trend among freelancers. Others integrate algorithmic configurators into procurement platforms like Mercado Eletrônico, enabling architects to drag-and-drop certified components into virtual floor plans in minutes. Many of these newcomers outsource fabrication to established factories during off-peak shifts, creating collaborative rather than adversarial supply-chain relationships. As sustainability audits become standard in RFPs, both incumbents and disruptors highlight circular-economy credentials—from take-back programs to recycled-plastic seating—illustrating that competitive advantage now rests as much on narrative coherence as on product engineering.

Brazil Office Furniture Industry Leaders

Interstuhl Brasil

Flexform

Marelli

Herman Miller Brazil

Haworth Brazil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Haworth restructured its design division under the Haworth Lifestyle banner, unifying luxury brands Poltrona Frau, Cassina, and Zanotta. The consolidation streamlines cross-brand sourcing so clients can specify high-end lounge pieces and task seating under one contract. Management signaled intent to add niche acquisitions within six months to deepen hospitality offerings, underscoring a commitment to full-lifecycle interior solutions.

- March 2025: Caderode unveiled the STIM collection, blending architect Emerson Borges’ organic curves with high-density foams calibrated for long-shift comfort. The launch coincided with a “Hub de Soluções,” an experiential showroom where clients test modular layouts via augmented reality. Early adopters include healthcare clinics drawn to STIM’s wipe-clean upholstery and compact footprints.

- February 2025: Brazil’s development bank approved a credit line for Tramontina, funding upgrades to machining centers and powder-coating booths at its Rio Grande do Sul campus. The investment underpins Tramontina’s move from commodity seating toward modular office systems, with automation expected to cut lead times and enable customized color runs for project-based bids.

- February 2025: After regulatory clearance, WeWork acquired SoftBank’s minority stake in its Brazilian arm and trimmed its network from 32 to 28 locations. The rationalization frees capital for tech enhancements such as occupancy sensors and AI-driven room allocation, while sustained retrofits keep demand steady for modular desks and durable seating.

Brazil Office Furniture Market Report Scope

A complete background analysis of the Brazil Office Furniture Market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report.

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Guest Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas/Soft Seating | |

| Booths & Office Dividers | |

| Other Office Furniture (Stools, Reception, Accessories) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

| Premium |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Direct from Manufacturers |

By Geography

| North Region |

| Northeast Region |

| Central-West Region |

| Southeast Region |

| South Region |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Guest Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas/Soft Seating | ||

| Booths & Office Dividers | ||

| Other Office Furniture (Stools, Reception, Accessories) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| Premium | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Direct from Manufacturers | ||

| By Geography | North Region | |

| Northeast Region | ||

| Central-West Region | ||

| Southeast Region | ||

| South Region | ||

Key Questions Answered in the Report

What is the current valuation of the Brazil office furniture market?

The market is valued at USD 1.31 billion in 2026.

How quickly is revenue expected to increase?

Sales are forecast to climb at a 6.12% CAGR, reaching USD 1.76 billion by 2031.

Why are tables gaining importance in workplace design?

Firms emphasize collaborative layouts and hybrid-meeting technology, driving a 6.45% CAGR for tables.

Which region is experiencing the fastest demand growth?

The North region leads with a projected 6.66% CAGR thanks to BPO expansion and infrastructure builds.

How do direct manufacturer channels benefit corporate buyers?

Direct channels bundle design, installation, and maintenance, delivering single-source accountability.

What is sparking furniture demand in healthcare facilities?

Hospital expansions and hygiene standards push healthcare offices to the highest 6.92% CAGR.

Page last updated on: