Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

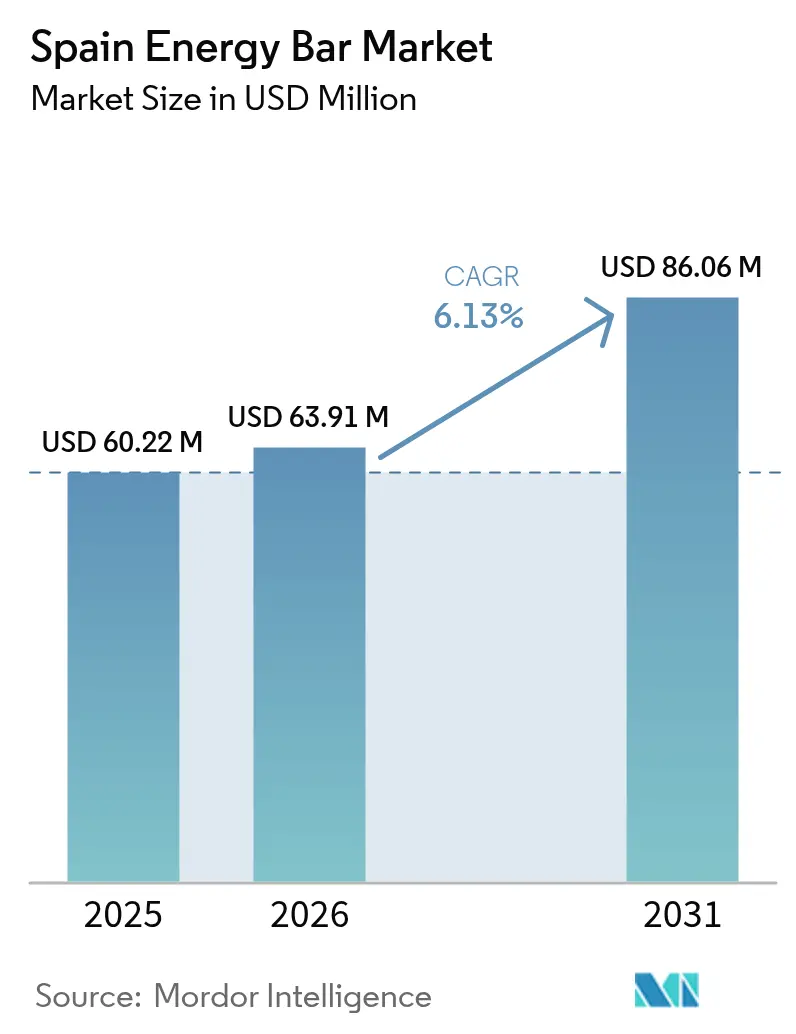

| Base Year Market Size (2025) | USD 60.22 Million |

| Market Size (2026) | USD 63.91 Million |

| Market Size (2031) | USD 86.06 Million |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

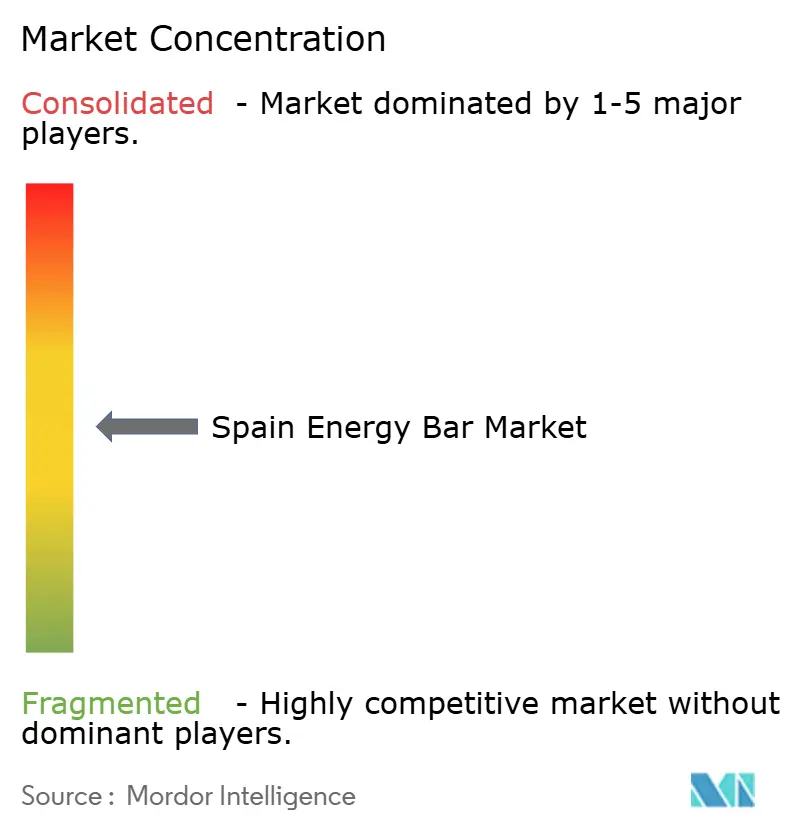

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Energy Bar Market Analysis by Mordor Intelligence

The Spain Energy Bar Market size was valued at USD 60.22 million in 2025 and estimated to grow from USD 63.91 million in 2026 to reach USD 86.06 million by 2031, at a CAGR of 6.13% during the forecast period (2026-2031). This expansion is driven by changing consumer lifestyles, increasing health awareness, and a rising demand for convenient nutritional options. Factors such as busy urban schedules, higher gym participation, and a preference for functional, clean-label, and high-protein products are shifting the market focus from basic snack bars to specialized products catering to fitness, wellness, and daily energy requirements. Additionally, innovation in the form of low-sugar formulations, plant-based options, and functional ingredient bars is intensifying competition, particularly as online retail gains momentum due to Spain’s high digital adoption. Despite market fragmentation and competition from other healthy snack alternatives, the sector continues to grow, supported by shifting consumer preferences, enhanced product offerings, and broader availability across retail channels.

Key Report Takeaways

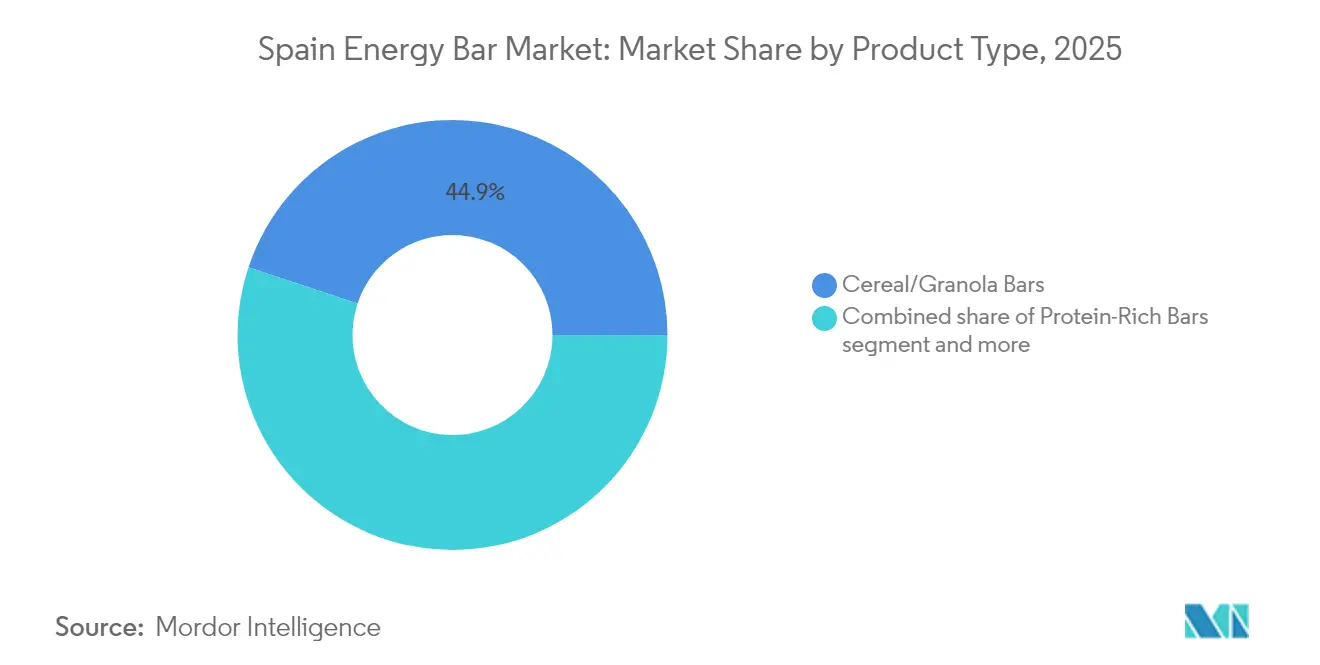

- By product type, cereal and granola bars accounted for 44.89% of the Spain energy bar market share in 2025, whereas protein-rich bars are forecast to expand at a 6.33% CAGR through 2031.

- By flavor profile, chocolate-based variants led with 41.39% revenue share in 2025, while fruit-based bars are projected to post a 7.22% CAGR to 2031.

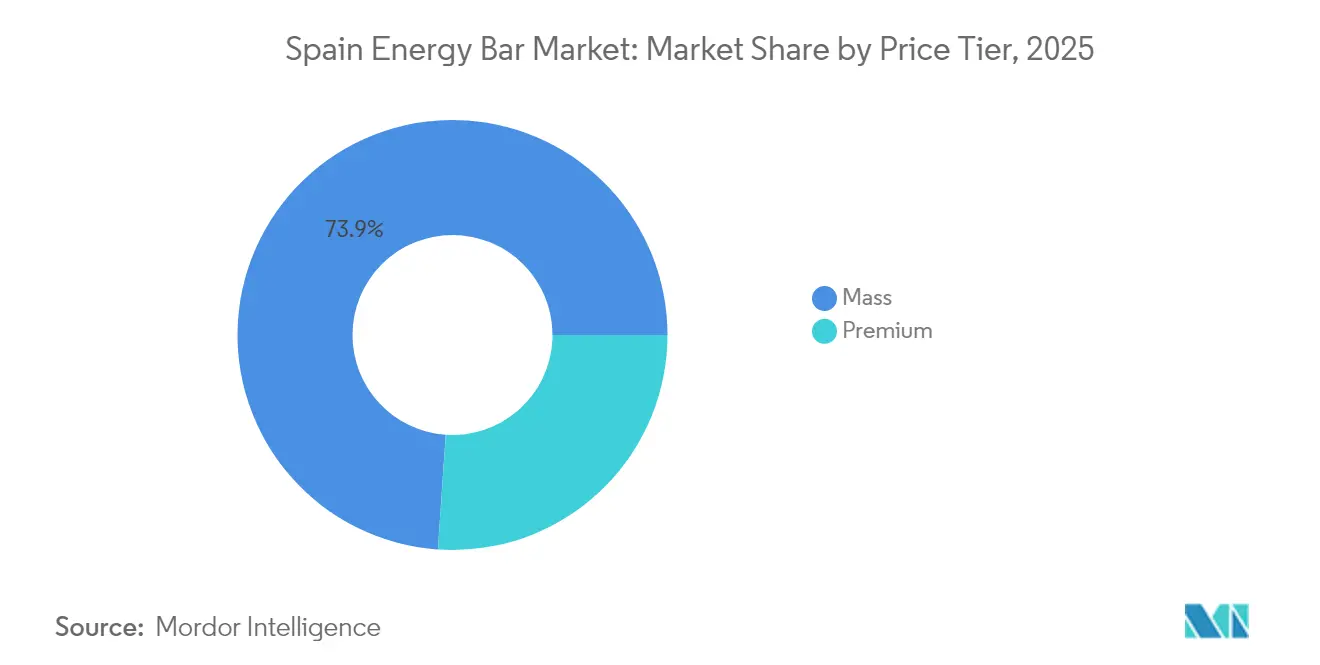

- By price tier, the mass segment captured 73.92% share of the Spain energy bar market size in 2025, but premium offerings are advancing at a 6.41% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets held 56.22% share in 2025; online retail is on track for the fastest 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Energy Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of fitness centers and gyms | +1.2% | National, concentrated in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Busy, on-the-go urban lifestyles | +1.5% | National, urban centers (Madrid, Barcelona) | Short term (≤ 2 years) |

| Product innovation and functional nutrition | +1.1% | National, premium segment focus | Medium term (2-4 years) |

| Rising health-conscious consumer base | +1.3% | National | Long term (≥ 4 years) |

| Demand for clean-label/organic products | +0.8% | National, premium segment | Medium term (2-4 years) |

| Changing demographic and lifestyle patterns | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of fitness centers and gyms

The growth of fitness centers and gyms in Spain is a key driver for the energy bar market, as it has increased demand for convenient, high-energy, and protein-rich snacks that support pre- and post-workout nutrition. With more consumers adopting regular exercise and fitness routines, energy bars have become a popular choice for quick energy replenishment, muscle recovery, and sustained performance, making them an essential component of an active lifestyle. This trend has not only boosted demand for protein-rich and functional bars but also spurred innovation in formulations, flavors, and portion sizes to meet the needs of fitness-focused consumers. For example, data from the Association for Media Research (AIMC) in 2023 indicates that approximately 16.5% of Spain's population had visited a gym, highlighting a significant and growing base of health- and fitness-conscious individuals [1]Source: Association for Media Research (AIMC), "Share of respondents who went to a fitness studio", aimc.es. This expanding fitness culture directly supports the energy bar market, as gyms and fitness enthusiasts increasingly seek convenient and nutritious options to complement their workouts, creating opportunities for both global and domestic brands to cater to this dedicated consumer segment.

Busy, on-the-go urban lifestyles

Busy, on-the-go urban lifestyles have significantly increased the demand for convenient, ready-to-eat snacks that integrate seamlessly into consumers’ daily routines. Urban residents, including professionals, students, and commuters, often have limited time for traditional meals, making energy bars an appealing option for quick energy, satiety, and nutrition while traveling, working, or studying. The combination of convenience, portable packaging, and diverse flavors ensures that energy bars remain a favored choice for urban consumers who value efficiency without sacrificing nutrition or taste. Brands are addressing these needs by offering products in smaller, grab-and-go sizes, a variety of flavors, and functional formulations tailored to busy individuals. As urbanization progresses and the pace of life accelerates in major Spanish cities such as Madrid, Barcelona, and Valencia, the demand for quick, nutritious, and portable snack options is expected to remain strong. This trend continues to drive growth in the energy bar market.

Product innovation and functional nutrition

Product innovation and functional nutrition are key drivers of the Spain Energy Bar Market, as consumers increasingly prefer snacks that offer targeted health benefits, enhanced satiety, and performance support in addition to basic energy provision. Manufacturers are addressing this demand by introducing bars fortified with protein, fiber, vitamins, minerals, and other functional ingredients, meeting the growing preference for healthier and more nutritionally advanced options. This trend has led to the development of specialized segments, including high-protein bars, low-sugar or low-calorie options, and bars designed for meal replacement or fitness recovery, helping products stand out in a competitive market. For example, the Barbells brand offers a High Protein Bar with 20 g of protein, while being low in sugar and calories, demonstrating how functional nutrition and product innovation cater to health- and fitness-conscious consumers. Such products combine convenience with the ability to meet specific dietary or lifestyle needs, enhancing the value proposition of energy bars beyond traditional snacking.

Rising health-conscious consumer base

The Spain Energy Bar Market is primarily driven by the increasing health-consciousness among consumers, as more individuals focus on balanced nutrition, weight management, and healthier snacking options. This trend has led to a demand for products offering functional benefits, controlled calorie content, clean ingredients, and improved macronutrient profiles, positioning energy bars as a preferred choice for daily consumption. Growing awareness of lifestyle diseases, diet-related health concerns, and the importance of maintaining a healthy weight is prompting consumers to replace traditional sugary snacks with energy bars that provide sustained energy, protein, fiber, and natural ingredients. For example, data from the Spanish Statistical Office indicates that in 2023, 55.0% of the population aged 18 and over were overweight, highlighting increasing concerns about diet quality and associated health risks [2]Source: Spanish Statistical Office, "Spain Health Survey (SHS)", ine.es. Consequently, consumers are actively seeking healthier snack alternatives that support weight management, enhance energy levels, and align with their wellness objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from alternative healthy snacks | -0.9% | National | Short term (≤ 2 years) |

| Strict food safety regulations and labeling requirements | -0.5% | National, Europe-wide compliance | Medium term (2-4 years) |

| Consumer skepticism toward artificial ingredients | -0.4% | National | Medium term (2-4 years) |

| Limited shelf life of energy bars | -0.3% | National, distribution-dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense competition from alternative healthy snacks

Intense competition from alternative healthy snacks poses a significant challenge for the Spain Energy Bar Market, as consumers now have a wider range of nutritious, convenient, and appealing options. The growing preference for health-focused lifestyles has led to an increase in demand for snacks that align with these values, offering consumers more choices beyond traditional energy bars. Products such as trail mixes, dried fruits, nuts, yogurt-based snacks, protein cookies, functional beverages, and ready-to-drink nutrition shakes increasingly target the same health-conscious and on-the-go consumer segment as energy bars. Many of these alternatives are perceived as more natural, less processed, or more satisfying, which can reduce demand for traditional and premium energy bars. Furthermore, brands in these competing categories often emphasize clean label, high-protein, or low-sugar attributes, requiring energy bar manufacturers to continuously innovate to remain competitive.

Strict food safety regulations and labeling requirements

Strict food safety regulations and labeling requirements pose a significant challenge to the Spain Energy Bar Market, creating operational and financial burdens for both established manufacturers and smaller, emerging brands. Spain, in alignment with broader EU regulations, enforces stringent standards on ingredient traceability, allergen disclosure, nutritional accuracy, hygiene protocols, and permissible health claims. These regulations require companies to make substantial investments in compliance systems, product testing, laboratory verification, and third-party audits. As a result, production costs increase, product development timelines are extended, and smaller domestic brands face greater difficulty in innovating or entering the market. These brands must navigate complex documentation, nutritional validation, and safety certifications to ensure compliance with European and national requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein-Rich Bars Gain Despite Cereal Dominance

Cereal/Granola Bars accounted for 44.89% of the Spain Energy Bar Market share in 2025, leading the segment due to their alignment with consumer preferences for convenient, nutritious, and wholesome snacking options. These bars are widely regarded as a healthy choice, often made with ingredients such as oats, whole grains, nuts, seeds, and dried fruits. They appeal to a broad demographic seeking balanced nutrition without sacrificing taste or convenience. Their ready-to-eat format and portability make them suitable for on-the-go consumption, catering to busy professionals, students, and travelers. Additionally, their versatility in flavors and formulations, including fiber-rich, low-sugar, plant-based options and superfood-enhanced recipes, enables brands to meet the demands of increasingly health-conscious and ingredient-aware consumers.

Protein-Rich Bars are projected to grow at a CAGR of 6.33% from 2026 to 2031, fueled by rising consumer demand for convenient, high-protein nutrition that supports fitness, recovery, satiety, and balanced macronutrient intake. This segment appeals not only to gym-goers and sports enthusiasts but also to everyday consumers seeking healthier snack options or meal replacements. Manufacturers are focusing on innovations such as higher-quality protein sources, plant-based alternatives, cleaner-label formulations, reduced sugar content, and the inclusion of functional ingredients like fiber and essential nutrients. These advancements are broadening the appeal of protein bars, making them a versatile choice for health-conscious individuals across various demographics.

By Flavor Profile: Fruit-Based Bars Accelerate on Clean-Label Wave

Chocolate-based bars accounted for a 41.39% market share in the Spain Energy Bar Market in 2025. Their popularity stems from their appeal as a convenient snack that combines indulgence with functional nutrition. These bars offer the familiar taste of chocolate paired with energy-boosting ingredients such as oats, nuts, and proteins, making them a preferred choice for on-the-go consumption, post-workout recovery, or quick energy replenishment. Consumers view chocolate-flavored bars as both satisfying and nutritious, driving repeat purchases and sustained demand. For example, brands like Isostar in Spain provide chocolate-flavored energy bars in 23 g portions, offering a compact and easily consumable option for athletes and everyday users, further solidifying the segment's market dominance.

Fruit-based bars are projected to grow at a CAGR of 7.22% from 2026 to 2031. These bars are gaining traction among consumers who prioritize natural ingredients, lighter nutrition, and convenience. They offer a balance of taste and perceived wholesomeness, appealing to a broad audience beyond health-conscious or fitness-oriented buyers. Families, students, commuters, and busy professionals increasingly choose fruit-based bars as a quick snack or clean-label alternative, perceiving them as a "natural snack" rather than a processed product. As awareness of clean-label ingredients, minimal processing, and plant-based nutrition continues to rise, manufacturers are responding by developing fruit-based bars that incorporate dried fruits, nuts, seeds, grains, or other whole-food ingredients.

By Price Tier: Premium Segment Outpaces Mass Despite Dominance

Mass-tier products accounted for 73.92% of the market share in 2025 in the Spain Energy Bar Market, underscoring their strong dominance. This performance is driven by affordability, accessibility, and widespread consumer preference for value-oriented options. These products cater to the largest segment of the population, providing convenient energy and nutrition at a price point appealing to daily snackers, students, office workers, and casual consumers who prioritize cost-effectiveness without sacrificing basic quality or taste. The mass-tier segment is defined by standardized flavors and formats, ensuring consistent availability and familiarity, which fosters repeat purchases and brand loyalty. Additionally, the extensive distribution networks and promotional strategies employed by mass-tier brands further strengthen their market presence, making them a staple choice for a broad consumer base.

Premium energy bars are projected to grow at a compound annual growth rate (CAGR) of 6.41% from 2026 to 2031. This growth is attributed to the increasing number of health- and quality-conscious consumers willing to pay a premium for better ingredients, cleaner formulations, and added functional or better-for-you attributes. As lifestyles shift toward wellness, clean eating, dietary awareness, and a preference for higher nutritional value, premium bars often featuring high-quality protein, clean-label ingredients, lower sugar content, allergen-free options, or formulations for specialty diets, appeal strongly to consumers who prioritize ingredient transparency and health credentials over price. Furthermore, the growing trend of personalized nutrition and the rising influence of social media in promoting health-focused products are expected to drive the demand for premium energy bars, positioning them as a preferred choice for discerning consumers.

By Distribution Channel: Online Retail Surges as Supermarkets Hold Ground

Supermarkets and hypermarkets accounted for 56.22% of the distribution share in the Spain Energy Bar Market in 2025, maintaining their position as the leading purchasing channel for consumers. This dominance is attributed to their extensive product variety, competitive pricing, and convenience, making them the preferred choice for consumers seeking energy bars for on-the-go consumption, fitness needs, or general snacking. The high visibility of brands, frequent promotional activities, and the availability of diverse flavors, product types, and price ranges under one roof further strengthen consumer preference for these large-format retailers.

Online retail is projected to grow at a compound annual growth rate (CAGR) of 7.98% from 2026 to 2031, driven by the increasing demand for convenience, home delivery, and digital shopping experiences among Spanish consumers. Online platforms provide access to a broader range of energy bar products, enable price comparisons, and allow consumers to read reviews and make purchases from the comfort of their homes. This channel is particularly appealing to busy professionals, fitness enthusiasts, and tech-savvy younger demographics. For example, according to the World Bank, internet usage in Spain reached 96% in 2024, underscoring the strong digital connectivity that supports the rapid expansion of online retail . Additionally, innovations in e-commerce, subscription models, and targeted online marketing enable brands to directly engage with consumers and expand their market presence beyond traditional retail outlets.

Geography Analysis

Spain's energy bar market is predominantly concentrated in urban centers such as Madrid, Barcelona, and Valencia, which collectively account for the majority of sales and consumption. These cities are characterized by large populations, higher income levels, and a significant presence of health-conscious, fitness-oriented, and working professionals, all of whom drive the demand for convenient and functional snacks. The availability of modern retail infrastructure, including supermarkets, hypermarkets, and a growing e-commerce ecosystem, ensures widespread access to energy bar products. Additionally, urban consumers are more exposed to international brands, marketing campaigns, and lifestyle trends that emphasize health, wellness, and on-the-go nutrition, further supporting the strong adoption of energy bars in these metropolitan areas.

Outside the major urban hubs, the market exhibits moderate growth in secondary cities and regional towns, where consumer awareness and purchasing power are comparatively lower. In regions such as Andalusia, Galicia, and Castilla-La Mancha, energy bars are primarily purchased in supermarkets and convenience stores. Demand in these areas is often driven by family-oriented or general snacking consumption rather than fitness- or nutrition-focused trends. While the penetration of premium and specialized energy bars remains limited, mass-tier products with popular flavor profiles maintain stable consumption due to their affordability and familiarity.

Rural and remote regions of Spain show lower but steadily increasing demand for energy bars, driven by rising health consciousness and the expanding reach of online retail. As e-commerce becomes more accessible, consumers in smaller towns and villages are gaining exposure to a wider variety of energy bar options, including protein-rich, fruit-based, and premium offerings. Combined with the impact of digital marketing and growing lifestyle awareness, this trend is gradually contributing to market growth outside traditional urban strongholds. However, urban centers are expected to remain the primary drivers of volume and revenue in Spain's energy bar market over the forecast period.

Competitive Landscape

Spain's energy bar market is highly fragmented, with both global multinationals and smaller domestic players competing for market share. Prominent international brands, including Amway Corp., Enervit S.p.A., Nestlé S.A., Mondelēz International, Inc., and Simply Good Foods Company, lead the market due to their strong brand recognition, extensive distribution networks, and significant marketing resources. These companies utilize established supply chains, robust retailer relationships, and diverse product portfolios, ranging from protein-rich and chocolate-based to fruit-based bars, to secure their presence in supermarkets, hypermarkets, and increasingly in online channels across Spain.

Adherence to international standards plays a crucial role in this competitive market. Certifications such as BRCGS Food Safety and ISO 14001 are often essential for securing supermarket listings. For example, Glanbia Performance, which distributes Optimum Nutrition bars across Europe, including Spain, leverages these certifications to demonstrate quality, safety, and sustainability. These standards are critical for gaining retailer and consumer trust, serving as a baseline requirement for major players aiming for broad market access. Additionally, they help international brands maintain consistency and reliability across markets, providing a competitive advantage over smaller or emerging local brands.

Smaller Spanish brands, while agile and adept at addressing niche segments or local taste preferences, face significant challenges in meeting regulatory and certification requirements. The costs associated with audits, traceability systems, and sustainability compliance can strain their resources, making it difficult to compete with multinational companies on a larger scale. However, local brands often differentiate themselves through innovation in flavors, the use of functional ingredients, or by emphasizing natural and clean-label products, allowing them to carve out niche opportunities in the market.

Spain Energy Bar Industry Leaders

-

Amway Corp.

-

Enervit S.p.A.

-

Nestlé S.A. (PowerBar)

-

Mondelēz International, Inc.

-

Simply Good Foods Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Saica Group, a prominent company in packaging solutions, has partnered with Mondelez to introduce a new paper-based product designed for multipack confectionery items, including energy bars.

- November 2023: Enervit SpA has signed a binding agreement to acquire the remaining 50% stake in Enervit Nutrition SL from Laboratorios Farmacéuticos ROVI, gaining full ownership of its Spanish branch for a total cash consideration of EUR 1.8 million.

Spain Energy Bar Market Report Scope

The Spanish energy bar market is segmented by type and distribution channel. By type, the market is segmented into organic and conventional. On the basis of distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialist retailers, online retail, and other distribution channels.

By Product type

| Cereal/Granola Bars |

| Protein-Rich Bars |

| Fruit and Nut Bars |

By Flavor Profile

| Chocolate-based Bars |

| Fruit-based bars |

| Nut and Seed-based bars |

| Other Flavors |

By Price Tier

| Mass |

| Premium |

Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product type | Cereal/Granola Bars |

| Protein-Rich Bars | |

| Fruit and Nut Bars | |

| By Flavor Profile | Chocolate-based Bars |

| Fruit-based bars | |

| Nut and Seed-based bars | |

| Other Flavors | |

| By Price Tier | Mass |

| Premium | |

| Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the projected value of Spain’s energy bar segment by 2031?

The segment is expected to reach USD 86.06 million by 2031, growing at a 6.13% CAGR.

Which product type will post the fastest growth through 2031?

Protein-rich bars are forecast to register the quickest expansion, advancing at a 6.33% CAGR.

How large is the online sales opportunity for bar suppliers?

Food e-commerce in Spain grew 203% from 2019 to 2024 and is set for an 7.98% CAGR, giving brands a fast-scaling digital channel for direct-to-consumer subscriptions.

What formulation gaps could new entrants address?

Reformulating with lower sodium, reduced saturated fat, and functional ingredients such as fermented plant proteins, probiotics, or collagen can satisfy rising clean-label and performance expectations.

Page last updated on: