Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Mexico Data Center Water Consumption Market Report is Segmented by Source of Water Procurement (Potable (municipal / Private Utilities), Non-Potable (treated Sewage / Recycled) and More), Data-Centre Type (Enterprise, Colocation, and More), Data-Centre Size (Mega, Massive, and More), Cooling Technology (Indirect Evaporative Cooling, and More), and by Region. The Market Forecasts are Provided in Terms of Volume (Liters).

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

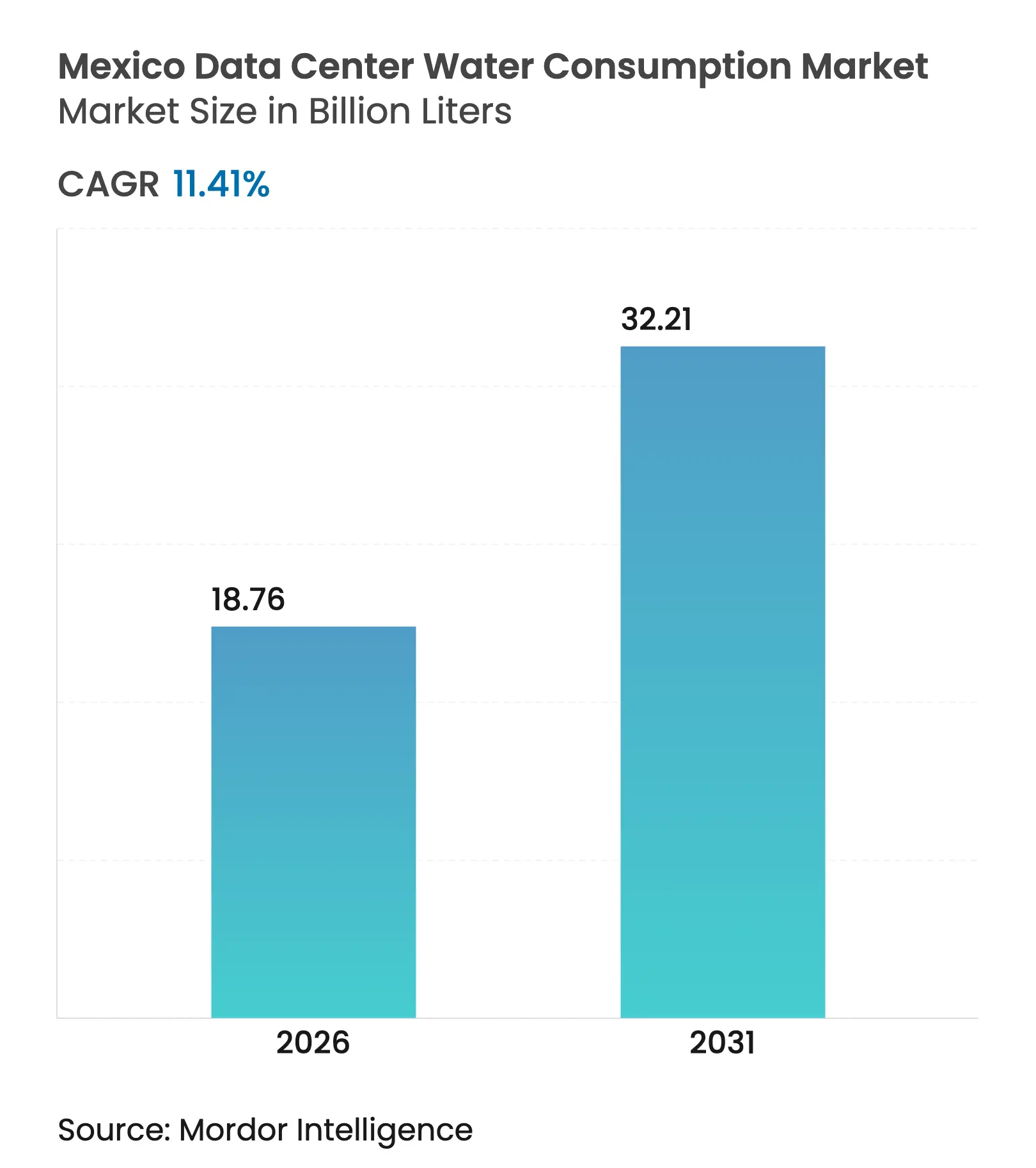

| Market Volume (2026) | 18.76 Billion liters |

| Market Volume (2031) | 32.21 Billion liters |

| CAGR | 11.41 % |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Mexico data center water consumption market size in 2026 is estimated at 18.76 billion liters, growing from 2025 value of 16.84 billion liters with 2031 projections showing 32.21 billion liters, growing at 11.41% CAGR over 2026-2031. Growth is rooted in large-scale cloud investments, near-shoring of North American workloads, and the steady migration from air to liquid cooling. Central Mexico remains the dominant cluster, but accelerated build-outs in Monterrey are redistributing demand. Operators are deepening commitments to alternative water sources and closed-loop reuse systems as stricter discharge rules close in. Intensifying droughts and rising electricity prices further amplify interest in immersion technology, which promises near-zero water usage. Competitive positioning increasingly depends on securing reliable water concessions, deploying efficient cooling, and satisfying local communities that are wary of industrial consumption spikes.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging

AI-driven rack densities raising cooling-water demand

Surging

AI-driven rack densities raising cooling-water demand

| +2.8% | Central Mexico, Northeast Mexico | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.8%

|

Geographic Relevance

:

Central

Mexico, Northeast Mexico

|

Impact Timeline

:

Medium

term (2-4 years)

|

Strong

hyperscale and near-shoring investments in Querétaro and Monterrey

Strong

hyperscale and near-shoring investments in Querétaro and Monterrey

| +2.1% | Central Mexico, Northeast Mexico | Short term (≤ 2 years) | |||

Escalating

power tariffs pushing operators to water-efficient hybrid cooling

Escalating

power tariffs pushing operators to water-efficient hybrid cooling

| +1.4% | National, concentrated in Central Mexico | Medium term (2-4 years) | |||

Stricter

CONAGUA discharge limits accelerating on-site reuse technologies

Stricter

CONAGUA discharge limits accelerating on-site reuse technologies

| +1.2% | National, enforcement focus in Central Mexico | Long term (≥ 4 years) | |||

Corporate

“net-water-positive” pledges by AWS, Microsoft, Google

Corporate

“net-water-positive” pledges by AWS, Microsoft, Google

| +0.9% | National, hyperscale facilities | Medium term (2-4 years) | |||

State-level

grey-/reclaimed-water incentives

State-level

grey-/reclaimed-water incentives

| +0.6% | Northeast Mexico, expanding nationally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging AI-driven rack densities raising cooling-water demand

AI servers such as NVIDIA DGX H100 now draw up to 10.2 kW per rack, compared with 2–4 kW in legacy deployments, pushing liquid-cooling volumes to 300–500 L/h per rack.[1]NVIDIA Corporation, “Liquid Cooling for DGX H100 Systems,” nvidia.com As hyperscalers deploy racks forecast to hit 600 kW, closed-loop systems aiming for 0.2 L/kWh have become essential to avoid 40–60% water spikes versus air-cooled designs. Querétaro’s AI-optimized halls intensify this load, pressuring municipal networks and accelerating the pivot toward reclaimed and desalinated sources. Operators are pairing direct-liquid and immersion methods with evaporative-tower retrofits so the Mexico data center water consumption market can scale sustainably while meeting performance targets.

Strong hyperscale and near-shoring investments in Querétaro and Monterrey

AWS committed USD 5 billion and Microsoft USD 1.3 billion to Mexican infrastructure through 2030, clustering more than 15 facilities within a 50-km radius of Querétaro that already consume an estimated 2.8 billion liters annually.[2]Amazon Web Services, “AWS Announces USD 5 Billion Investment in Mexico,” aws.amazon.com Low-latency access to US users (20–40 ms) keeps these cities attractive, yet the growth concentrates withdrawal on stressed aquifers. As a hedge, operators channel new capital toward Nuevo León, where industrial water-recycling incentives offset higher temperatures. Direct investment is complemented by joint ventures with treatment specialists that guarantee permit compliance and community acceptance.

Escalating power tariffs pushing operators to water-efficient hybrid cooling

Federal tariffs rose from USD 119.52/MWh in 2022 to USD 151.60/MWh in 2023, a 27% jump that raised operating costs for air-cooled plants consuming up to 40% of site power. Indirect evaporative and closed-loop liquid cooling can cut this power slice by 50–70%, and facilities achieving a 1.05–1.10 PUE save USD 2–3 million yearly on a 10 MW block. Although chemical treatment costs rise, the economics favor hybrid designs that vary water draw by hour-ahead power pricing, helping stabilize Mexico data center water consumption market growth against volatile energy expenses.

Stricter CONAGUA discharge limits accelerating on-site reuse technologies

NOM-001-SEMARNAT-2021 enforces 90% BOD and 85% TSS cuts by March 2027, pushing data-center operators toward membrane bioreactors, reverse osmosis, and advanced oxidation to recycle 80–90% of tower blow-down.[3]Secretaría de Medio Ambiente y Recursos Naturales, “NOM-001-SEMARNAT-2021,” semarnat.gob.mx CONAGUA’s 163 inspectors cover more than 523,000 permits, so companies that exceed the new thresholds early mitigate enforcement uncertainty. Recycled output feeds cooling circuits directly, slashing freshwater withdrawals and strengthening social licenses to operate in water-stressed districts.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intensifying

droughts and aquifer depletion in Central Mexico

Intensifying

droughts and aquifer depletion in Central Mexico

| -1.8% | Central Mexico, Northwest Mexico | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.8%

|

Geographic Relevance

:

Central

Mexico, Northwest Mexico

|

Impact Timeline

:

Short

term (≤ 2 years)

|

Community

push-back and NGO litigation over water concessions

Community

push-back and NGO litigation over water concessions

| -1.2% | Central Mexico, Northeast Mexico | Medium term (2-4 years) | |||

Grid-wide

power brownouts limiting pump and treatment uptime

Grid-wide

power brownouts limiting pump and treatment uptime

| -0.9% | National, concentrated in Central Mexico | Short term (≤ 2 years) | |||

Rising

capex / opex for advanced treatment membranes and chemicals

Rising

capex / opex for advanced treatment membranes and chemicals

| -0.7% | National, water-scarce regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Intensifying droughts and aquifer depletion in Central Mexico

The Cutzamala system edges toward “day zero” while the Querétaro Valley aquifer drops 2–3 m every year, forcing municipal rationing and threatening continuous cooling operations.[4]Comisión Nacional del Agua, “Reporte de Disponibilidad del Sistema Cutzamala 2024,” conagua.gob.mx Spring 2024 heatwaves above 45 °C cut surface reserves 30–35%, compelling facilities to import reclaimed water at premiums of USD 0.50–0.80 per m³. Operators counter by banking rain capture during June–September and piloting atmospheric water generators, yet escalating scarcity still restrains overall Mexico data center water consumption market expansion.

Community push-back and NGO litigation over water concessions

Local groups argue that data-center withdrawals of 15–20 million L per day equal household needs for up to 150,000 residents, triggering lawsuits that prolong permit timelines 12–18 months. More than USD 64 billion in global builds have stalled following similar disputes. Mexican operators now embed community outreach and water-positive pledges into project charters, often agreeing to return 110% of taken volumes through municipal reuse partnerships, yet litigation risk still trims Mexico data center water consumption market CAGR in contested zones.

By Source of Water Procurement: Sustainability Drives Alternative Uptake

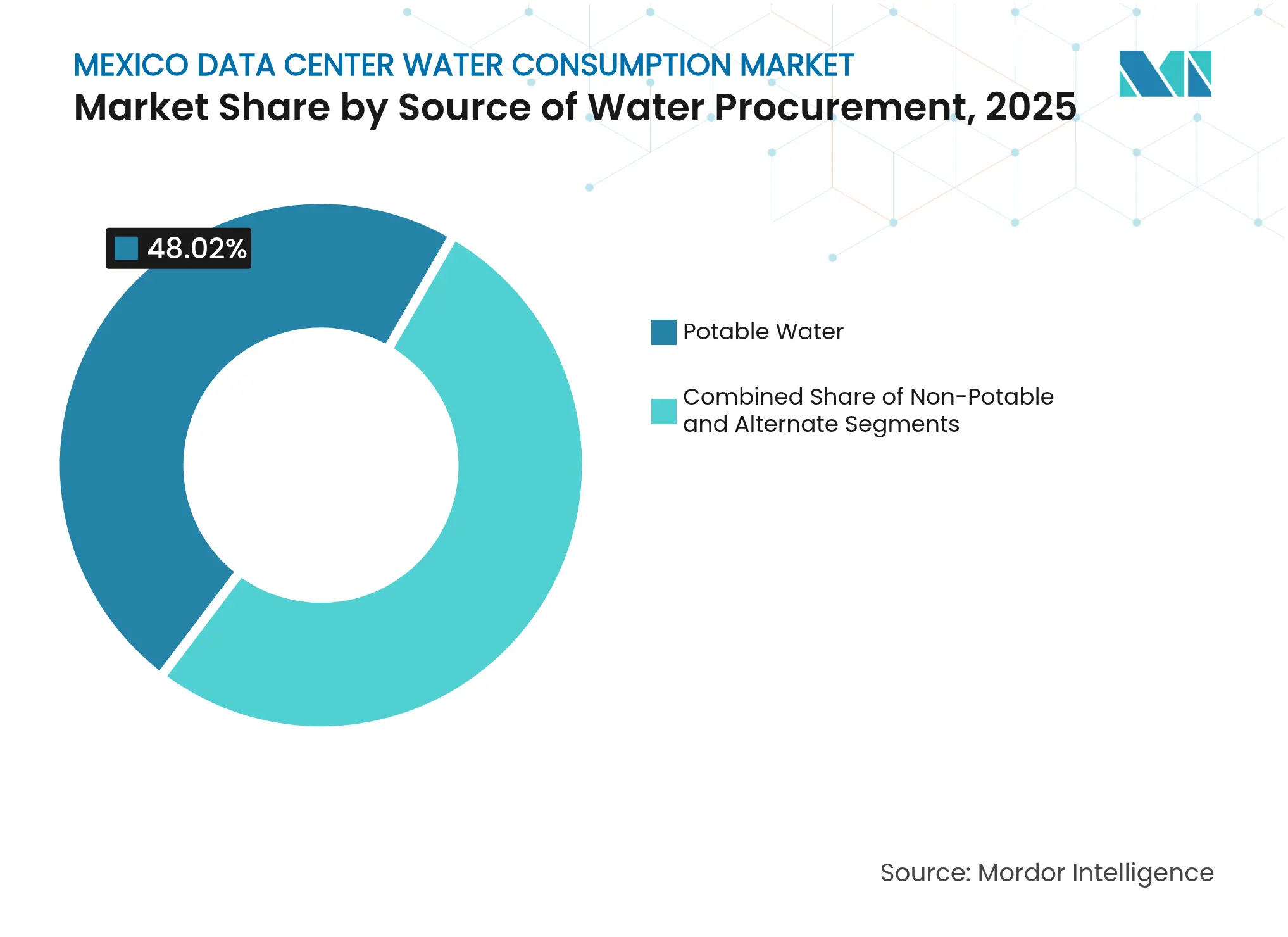

Potable Water held 48.02% share in 2025, but they are on track to eclipse potable abstractions by 2028 as operators secure on-site recycling and municipal grey-water pipelines. Alternate Sources, including treated wastewater and rain harvest, expand at 14.68% CAGR, underpinning the fastest slice of the Mexico data center water consumption market. Closed-loop plants in Querétaro now recycle 80–90% of effluent, shrinking net withdrawals and easing regulatory pressure. Surface water and groundwater remain important yet face tighter quotas as aquifer drawdown accelerates. Seawater desalination, priced at USD 2.62 per m³, gains interest for coastal campuses in Baja California and Sonora where pipeline extensions can supply inland substations.

Where potable sources once dominated total demand, alternative water sources achieved 51.00% of the Mexico data center water consumption market size for new capacity sanctioned in 2025. Incentive decrees in Nuevo León subsidize reclaimed supply lines, lowering payback to fewer than four years. Atmospheric water generation units supplement peak needs during the rainy season, capturing 40–60% of annual precipitation for onsite reuse. Regulatory clarity and rising community expectations ensure that non-potable uptake will remain the main lever for balancing growth with resource stress across the Mexico data center water consumption market.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Hyperscale Expansion Reshapes Demand Mix

Colocation players retained 41.30% share in 2025, yet hyperscale lines are growing 14.07% annually as AWS, Microsoft, and Google extend sovereign estates. Hyperscale halls consume up to 3× more water per MW because AI racks generate higher waste heat, lifting their contribution to the Mexico data center water consumption market size. Enterprise sites grow marginally, constrained by cloud migration, while cloud service provider footprints bridge the latency gap through distributed edge hubs.

Hyperscale installations deploy immersion and direct-liquid cooling that deliver water-usage effectiveness below 0.2 L/kWh. These advances place pressure on colocation providers to retrofit older halls or risk occupancy declines. Edge micro-sites dotted across city cores rely on water-free refrigerant loops, adding a resilient layer of capacity without heavy aquifer impact. The reshaped mix encourages technology vendors to customize modular treatment skids sized for hyperscale blow-down as well as small edge drips, creating diverse but specialized demand inside the Mexico data center water consumption market.

By Data Center Size: Mega Facilities Concentrate Volume and Efficiency

Large facilities captured 35.74% of the Mexico data center water consumption market share in 2025, while mega campuses above 50 MW log a 14.46% CAGR. Scale advantages permit centralized treatment and shared seawater or reclaimed-water pipelines, cutting unit costs by 20–30%. Mega designs allocate reclaimed effluent to indoor farms or municipal networks, lifting social acceptance.

Massive builds exceeding 100 MW integrate renewable power parks and on-site desal units, aiming for net-positive water status. Medium footprints still serve regional latency needs but face higher $/m³ because they cannot justify sophisticated reuse arrays. Small legacy halls lose ground as tenants migrate to efficient clusters. The consolidation dynamic funnels capex into fewer but larger reservoirs of demand, steering innovation toward very-large-scale filtration modules that fit the evolving scale profile of the Mexico data center water consumption market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

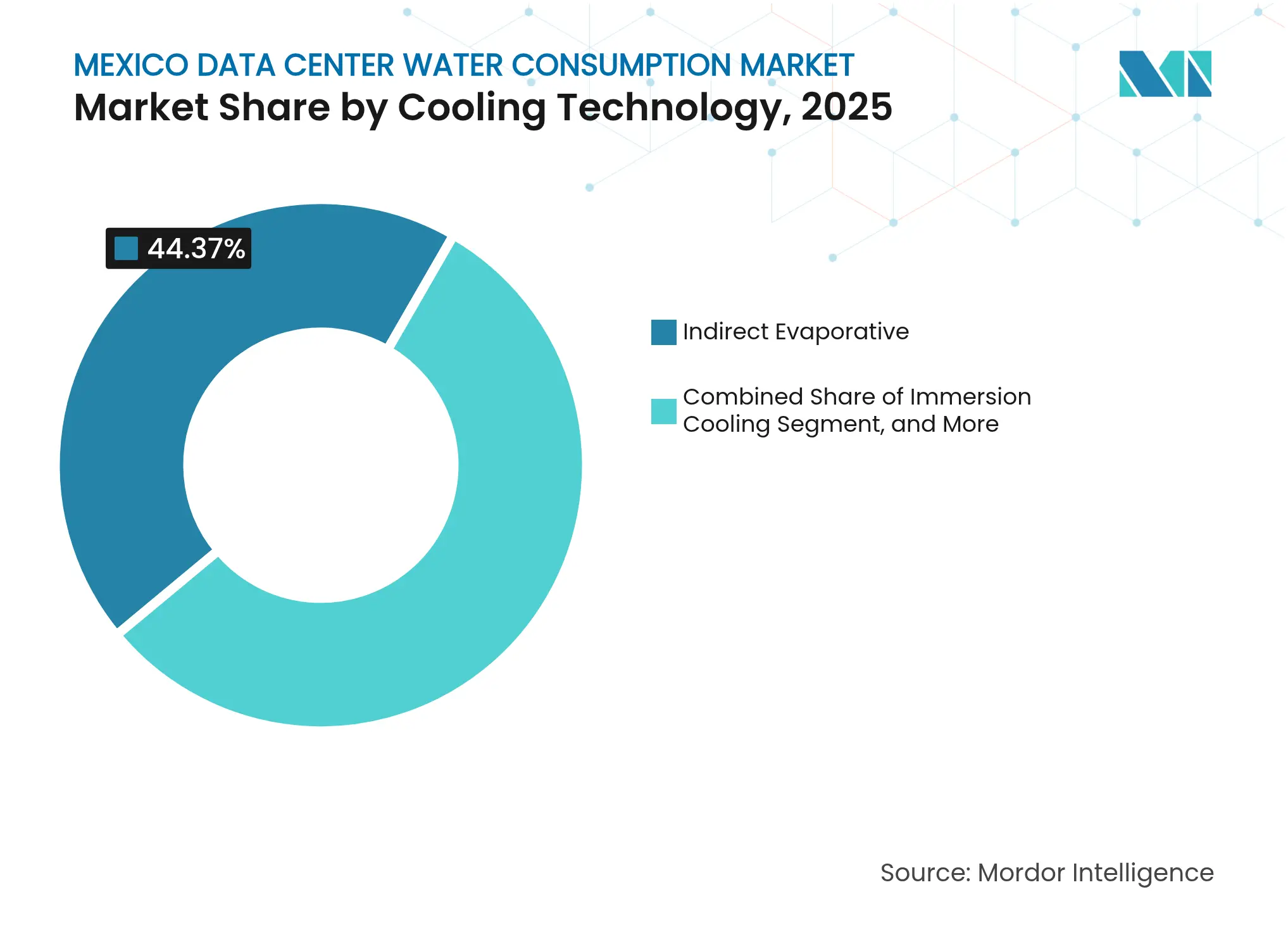

By Cooling Technology: Immersion Systems Lead Water-Free Frontier

Indirect evaporative cooling held 44.37% share in 2025, yet immersion setups race ahead at 20.32% CAGR, eliminating evaporative towers and bringing water draw near zero. Direct-liquid loops continue to gain traction for racks below 100 kW, allowing phased retrofits in existing shells. Water-free heat-exchange units with refrigerant circuits post PUEs of 1.15–1.25, rising slightly versus evaporative systems but sidestepping community concerns.

Immersion’s dielectric baths capture heat at chip level, enabling AI racks above 200 kW while channeling warm fluid into district-heating pilots. Chilled-water air coils linger in older enterprise suites but will fade as compliance costs for makeup supply climb. Vendors like Aligned Data Centers claim 85% water cuts with Delta³ arrays. Technology choice is now a reputational metric, propelling operator disclosures of usage-effectiveness indexes alongside carbon metrics across the Mexico data center water consumption market.

Note: Segment shares of all individual segments available upon report purchase

Central Mexico generated over half of national consumption in 2025, reflecting heavy hyperscale clustering and the 8–10 billion liter draw projected for 2025. Municipal reuse schemes now deliver 70–80% recycle rates using membrane bioreactors and RO skids. Community rallies have nudged operators to guarantee water-positive outcomes, and several facilities pledge to return 110% of extracted volumes to public networks.

Northeast Mexico emerges as the quickest grower, with Monterrey spearheading a 14.23% CAGR on the back of near-shoring and Nuevo León’s grey-water policy. Coahuila and Tamaulipas add capacity through industrial corridors that already handle recycled process streams. Temperatures surpassing 45 °C in summer raise chiller loads, but advanced adiabatic and liquid systems maintain efficiency.

Northwest, West, and South-Southeast states each capture a smaller current footprint but hold strategic importance for diversity. Sonora and Baja California couple solar generation with desalinated supply lines. Guadalajara’s tech hub appeals for latency-sensitive workloads. Yucatán’s edge clusters support tourism applications though full-scale campuses are limited by grid constraints. Collectively these areas broaden resilience and temper the geographic risk profile embedded in the Mexico data center water consumption market.

Market Concentration

The Mexico data center water consumption market displays moderate concentration. Hyperscale giants, AWS, Microsoft, and Google, anchor multi-billion commitments, often bundling water-efficiency technologies into each build. Colocation incumbents such as Equinix and Digital Realty retrofit towers with indirect evaporative plus RO polishing to retain tenants. Regional firms like KIO Networks and Layer 9 focus on local relationships and state-level incentives to secure concessions quickly.

Competition now pivots on water-usage effectiveness. AWS claims 0.19 L/kWh through proprietary recycling, while conventional halls linger near 1.5 L/kWh. Operators invest in patent filings covering zero-water or atmospheric harvesting, seen in Microsoft’s 2024 disclosures. Financing rounds increasingly cite water efficiency as a covenant, illustrated by Aligned’s USD 12 billion raise tied to Delta³ cooling.

White-space remains in secondary metros where community engagement is still formative. Treatment-equipment vendors and fluid-cooling specialists enter through partnerships, enabling smaller operators to leapfrog to immersion. As water scarcity intensifies, consolidation is expected, with resource-strong players acquiring stranded or delayed projects, elevating the bar for compliance and community stewardship across the Mexico data center water consumption market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VOLUME)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The study tracks the critical applications of water in large data centers, such as cooling and power generation. It includes key applications based on water consumption in data centers and quantifies overall water usage in billion liters across regions. The study also identifies underlying trends and developments conceptualized by leading industry data center operators.

The Mexico Data Center Water Consumption Market Report is Segmented by Source of Water Procurement (Potable (municipal / Private Utilities), Non-Potable (treated Sewage / Recycled) and More), Data-Centre Type (Enterprise, Colocation, and More), Data-Centre Size (Mega, Massive, and More), Cooling Technology (Indirect Evaporative Cooling, Direct Liquid Cooling, and More), and by Region. The Market Forecasts are Provided in Terms of Volume (Liters).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.