Spain Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

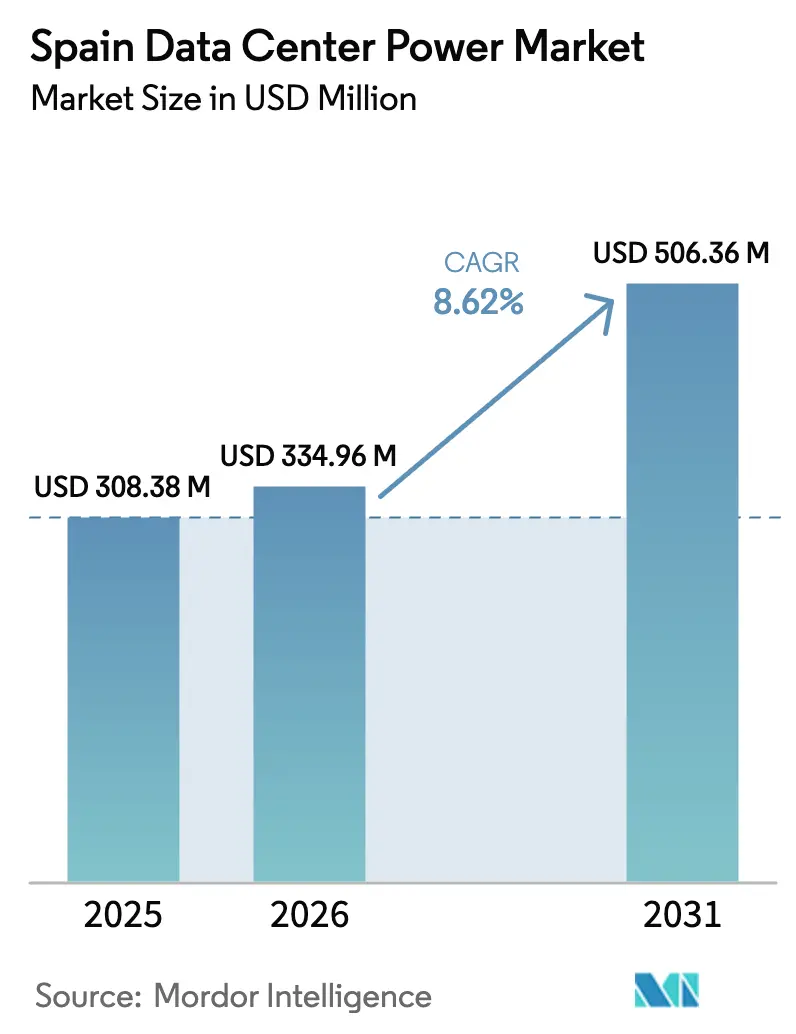

| Base Year Market Size (2025) | USD 308.38 Million |

| Market Size (2026) | USD 334.96 Million |

| Market Size (2031) | USD 506.36 Million |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Data Center Power Market Analysis by Mordor Intelligence

Spain data center power market size in 2026 is estimated at USD 334.96 million, growing from 2025 value of USD 308.38 million with 2031 projections showing USD 506.36 million, growing at 8.62% CAGR over 2026-2031. Robust cloud-service uptake, large renewable-energy additions, and heavy grid-modernization spending keep demand on a steep upward curve. Rising hyperscale investments in Aragón and Madrid, aggressive corporate power-purchase agreements (PPAs), and submarine-cable build-outs extend the runway for capacity additions. Lithium-ion retrofit programs launched after the April 2025 blackout lift replacement demand, while hydrogen fuel-cell pilots signal a pivot away from diesel. Competitive dynamics remain moderate as global power-equipment majors face new entrants offering clean-energy technologies and turnkey service bundles.

Key Report Takeaways

- By component, power distribution units led with 26.70% of Spain data center power market share in 2025; hydrogen fuel-cell generators are on course for an 8.84% CAGR to 2031.

- By data-center type, hyperscale/cloud service providers held 44.50% Spain data center power market share in 2025, and this segment is expanding at a 10.23% CAGR through 2031.

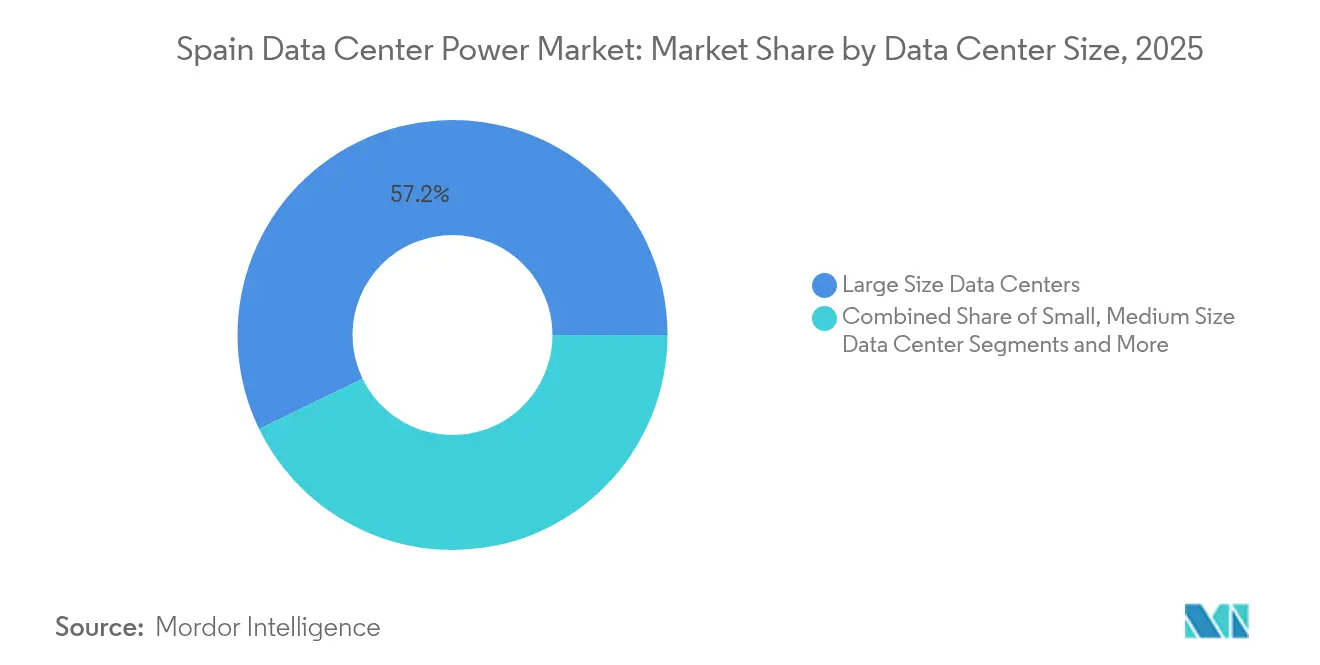

- By size, large facilities accounted for 57.20% of the Spain data center power market size in 2025, while mega sites above 100 MW are forecast to post a 8.95% CAGR to 2031.

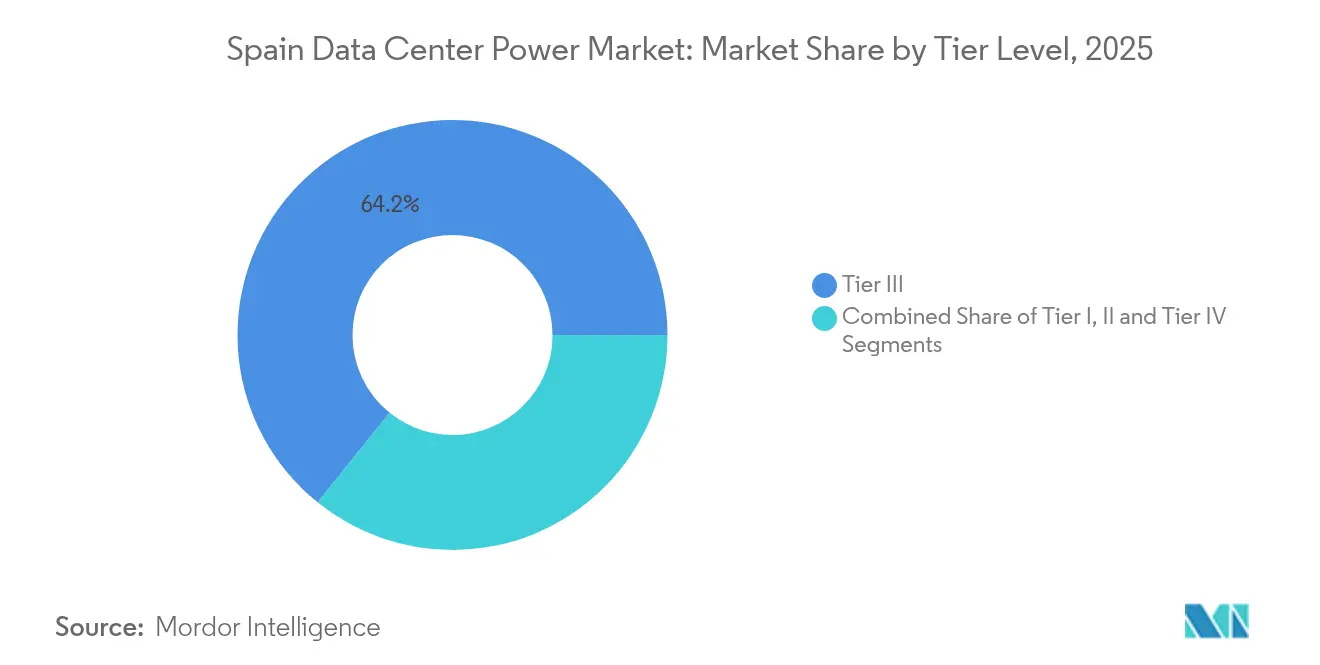

- By tier level, Tier III sites captured 64.20% of the Spain data center power market size in 2025; Tier IV is the fastest-growing tier at an 10.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale and cloud mega-campuses | +2.1% | Madrid, Barcelona, Zaragoza | Medium term (2-4 years) |

| Corporate PPAs and 74% renewables target | +1.8% | Nationwide; Aragón focus | Long term (≥ 4 years) |

| Edge-to-core submarine-cable build-outs | +1.4% | Madrid, Valencia, Barcelona | Medium term (2-4 years) |

| Post-blackout lithium-ion UPS retrofits | +1.2% | Nationwide; Madrid priority | Short term (≤ 2 years) |

| Small modular reactor pilots (greater than 20 MW) | +0.9% | Aragón, Castilla-La Mancha | Long term (≥ 4 years) |

| Utility-backed “green power rings” | +0.8% | Madrid, Zaragoza | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of hyperscale and cloud mega-campuses

A wave of mega-campus announcements underpins the Spain data center power market. Amazon Web Services committed EUR 15.7 billion to Aragón, and Microsoft added USD 7.16 billion for new northeastern campuses. Each complex needs 100-300 MW, demanding multi-feed transmission upgrades and modular factory-built switchgear. Utility Red Eléctrica is revising grid planning to match these clusters, while suppliers standardize scalable PDU and busway offerings that compress site-delivery times. Bulk procurement gives hyperscalers leverage to integrate on-site solar or wind at sub-EUR 30/MWh, reducing operating costs and curbing carbon footprints.[1]International Energy Agency, “Spain 2024 Energy Policy Review,” iea.org

Corporate PPAs and Spain’s 74% renewables target

Spain aims for 74% renewable electricity by 2030, and hyperscale operators sign multi-year PPAs to hedge long-term energy costs. Amazon’s 476 MW deal with Iberdrola and Google’s wind-energy accord with Exus Renewables spotlight how clean electricity underpins expansion plans. Solar bids clearing below EUR 20/MWh widen cost advantages over grid tariffs, yet variable output raises the need for battery storage and hybrid UPS layouts. Red Eléctrica’s 2024 data show renewable penetration already at 56.8%, emphasizing the balancing challenge that storage vendors now address. [2]Iberdrola, “Amazon and Iberdrola Sign 476 MW PPA Expansion,” iberdrola.com

Edge-to-core submarine-cable build-outs fueling regional clusters

Spain handles more than 70% of Europe-to-Latin America data traffic because of new trans-Atlantic and Mediterranean subsea cables. Landing stations outside Valencia and Barcelona trigger demand for localized 5-10 MW facilities that use high-availability rectifiers for cable-repeater power. This deepens Spain data center power market diversification beyond the traditional Madrid–Barcelona corridor and accelerates transformer and generator orders in coastal zones.[3]NTT Ltd., “Madrid 1 Data Center Overview,” global.ntt

The 23-hour April 2025 blackout revealed the limits of lead-acid batteries, prompting an industry-wide upgrade cycle. Lithium-ion systems demonstrated higher energy density and quicker recharge, leading operators to prioritize replacements in under two years. Vendors layer predictive analytics modules onto UPS fleets, giving operators visibility on runtime and remaining useful life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and O&M cost of Tier III/IV gear | -1.5% | Nationwide; Madrid acute | Short term (≤ 2 years) |

| Madrid grid-connection queue and substation bottlenecks | -1.2% | Madrid metro area | Medium term (2-4 years) |

| Negative-price curtailment risk for solar-heavy PPAs | -0.8% | Aragón, Andalusia | Medium term (2-4 years) |

| Immature hydrogen fuel-cell supply chain | -0.6% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High installation and O&M cost of Tier III/IV electrical gear

Tier IV designs require 2N+1 redundancy and synchronous-transfer systems that push equipment costs 40-60% above Tier II benchmarks. Spain’s shortage of high-voltage specialists extends commissioning by up to 30%, inflating project budgets. Integration of renewable generation drives extra spend on power-conditioning units and microgrid controllers. Smaller operators struggle to absorb these premiums, limiting their entry into the Spain data center power industry.

Madrid grid-connection queue and substation bottlenecks

The capital retains 55% of national capacity yet faces 18-36-month wait times for new 220 kV connections. Selective queue management favors hyperscale names, forcing others toward secondary hubs or on-site generation. Land near uncongested substations commands escalating premiums, eroding Spain data center power market competitiveness versus other EU locations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Intelligent PDUs anchor modernization

Power distribution units captured 26.70% of Spain data center power market share in 2025, underscoring their role in high-density racks that now exceed 30 kW. Intelligent models with outlet-level metering help operators track real-time loads and respond to demand spikes triggered by AI workloads. Hydrogen fuel-cell generators deliver the fastest 8.84% CAGR, riding policy bans on diesel in urban zones. UPS systems shift to lithium-ion chemistries that offer twice the lifecycle of valve-regulated lead-acid units. Switchgear demand climbs as Tier III and Tier IV builds require automatic transfer capabilities. Energy-storage racks bridge renewable intermittency and supply ride-through services, creating a USD 74.35 million Spain data center power market size opportunity by 2031. Services from design through lifecycle maintenance expand in parallel, reflecting skills shortages around fuel-cell and battery integration.

By Data-Center Type: Hyperscale drives structural change

Hyperscale and cloud campuses held 44.50% Spain data center power market share in 2025 and will log a 10.23% CAGR to 2031. Their 100-300 MW footprints necessitate dedicated substations, 400 V busway trunking, and on-site renewables. Colocation retains relevance by offering upgradeable 2-20 MW suites in metro fiber hubs where hyperscale demand outstrips land supply. Enterprise and edge builds offset latency gaps, provisioning under-10 MW sites with compact lithium UPS and fuel-cell micro-grids. The segment mix shapes procurement; hyperscalers standardize across global designs, whereas edge nodes buy pre-fabricated power rooms that shorten deployment to 16 weeks.

By Size: Large and mega sites dominate capacity

Large facilities above 25 MW account for 57.20% of Spain data center power market size, reinforcing the pull of scale economies in cooling, staffing, and renewable PPAs. Mega campuses, those surpassing 100 MW, will expand 8.95% annually as AI inference boosts rack power to 40 kW. Medium data centers (5-25 MW) serve region-specific cloud zones, while small and micro sites handle low-latency content caching. Mega builders adopt on-site solar portfolios sized at 25-40% of peak load, complemented by 4-hour battery storage. These hybrid architectures anchor Spain’s grid-stability projects, especially in Aragón’s 22 GW renewable pipeline.

By Tier Level: Tier IV races ahead

Tier III still represents two-thirds of shipments thanks to its cost-reliability balance, yet Tier IV’s 10.72% CAGR reflects financial-services and health-sector demand for concurrent maintainability. The April 2025 outage highlighted Tier I/II vulnerability; resulting RFPs specify 2N+1 UPS strings and multiple fuel sources. Tier IV designs now integrate hydrogen fuel-cell strings in parallel with diesel to meet zero-carbon mandates while preserving eight-hour autonomy. Condition-based monitoring platforms dispatch maintenance crews based on real-time breaker temperature and harmonic-distortion readings, reducing downtime risk in Spain data center power market facilities.

Geography Analysis

Fiber density, corporate headquarters, and Spain-to-LatAm cable regeneration nodes keep it attractive. However, substation queues and land scarcity lengthen delivery schedules beyond 30 months. Utilities counter with EUR 400 million for looped “green power rings” that pair 150 MW battery banks with HVDC feeders. Aragón is the fastest-growing geography, buoyed by EUR 30 billion of announced hyperscale commitments and a renewable fleet expected to top 30 GW by 2030. Zaragoza’s dry climate trims cooling loads, enabling power-usage-effectiveness (PUE) levels near 1.15.

Barcelona sustains secondary-hub status, leveraging cross-Mediterranean cable routes and strong disaster-recovery demand from French enterprises. Coastal zones near Valencia open new clusters tied to landing-station builds that integrate redundant power for submarine-cable amplifiers. Andalusia’s solar abundance spurs solar-plus-storage data-center projects where negative-price curtailment risk is hedged by on-site batteries providing secondary-reserve services. The geographic shift spreads Spain data center power market risk more evenly and lowers overall grid-congestion exposure.

Competitive Landscape

The Spain data center power market features moderate fragmentation: top equipment manufacturers Schneider Electric, ABB, and Eaton together account for roughly half of shipments, while emerging suppliers push hydrogen fuel-cells and lithium battery racks. After the 2025 blackout, operators demanded SLA-backed lithium retrofits and zero-emission gensets, spurring ABB to roll out 1 MW container-based fuel-cell modules in Aragón. Schneider’s EcoStruxure suite gains traction by integrating PDU telemetry with building-management dashboards. Eaton pilots solid-state switchgear delivering millisecond transfer for AI clusters.

Strategic moves include Hitachi Energy’s EUR 30 million Zaragoza transformer-factory expansion and Vertiv’s alliance with Ballard for low-carbon UPS solutions. Local EPC players such as ACS and Acciona integrate turnkey power blocks, bundling PV arrays with 2-hour battery strings. Patent filings reveal rising interest in 48 V DC bus architectures that slash conversion losses to 2-3%, positioning innovators for efficiency-driven tenders.

Spain Data Center Power Industry Leaders

ABB Ltd

Caterpillar Inc.

Cummins Inc.

Eaton Corporation

Legrand Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: A 10 MW landing-station-plus-data-center project was confirmed for Valencia, underscoring coastal expansion.

- May 2025: Red Eléctrica secured 12 government approvals to fast-track transmission upgrades that benefit new data-center interconnections.

- April 2025: ACS announced Aragón data-center plans, strengthening the region’s hyperscale cluster.

- March 2025: Azora unveiled a EUR 2 billion, 300 MW Zaragoza campus designed for AI workloads and near-zero water use Azora.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spain data center power market as all revenue generated within the country from the sale, rental, and long-term service of electrical infrastructure that delivers, converts, backs up, and monitors facility power, namely UPS systems, PDUs, busways, switchgear, generators, batteries, and related design or maintenance services.

Scope Exclusion: Cooling plant hardware, as well as building shell and fit-out costs, are outside the power remit and therefore excluded.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed power-equipment vendors, design-build contractors, hyperscale energy managers, and regional regulators across Madrid, Aragón, Catalonia, and Andalusia. Dialogues clarified rack-density roadmaps, PPA contract lengths, and typical service margins, which were then used to validate assumptions and close data gaps flagged during desk work.

Desk Research

We began with open datasets from the Spanish National Statistics Institute, Red Eléctrica de España load profiles, Customs Tariff Chapter 85 shipment records, and filings housed on the CNMV portal. We then layered in technical papers from the Spain DC association and guidance released under the EU Energy Efficiency Directive. Trade publications such as DataCenter Dynamics and public investor decks added near-term capacity announcements, while paid repositories, D&B Hoovers for company revenue splits and Dow Jones Factiva for project news, helped us date-stamp pipeline milestones. These secondary inputs provided baseline volumes and pricing corridors. The sources listed are illustrative, not exhaustive, and many additional references informed the desk review.

Market-Sizing & Forecasting

A top-down reconstruction that starts with installed IT-load (MW) and average PUE values yields Spain's annual electrical demand, which is then priced using blended ASPs for UPS, PDUs, generators, and services. Selective bottom-up checks, supplier revenue roll-ups and sampled ASP × unit imports, adjust totals before sign-off. Key variables in the model include hyperscaler capex pipelines, renewable PPA volumes, replacement cycles of lithium-ion UPS, average rack density progression, and utility-scale power prices. Forecasts employ multivariate regression with scenario controls for grid-connection lead times and renewable share targets. Where supplier splits were missing, weighted regional ratios from interviewed experts bridged gaps.

Data Validation & Update Cycle

Outputs pass variance tests against historical import data, listed-firm segment revenue, and cross-country intensity ratios. Senior reviewers question anomalies, and corrective interviews are triggered when deviations exceed preset thresholds. Mordor refreshes every twelve months, with interim revisions after material policy, macro-energy, or hyperscale investment events.

Why Mordor's Spain Data Center Power Baseline Commands Strong Confidence

Published estimates often diverge because firms pick different equipment baskets, density trajectories, and forecast cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 281.55 million (2024) | Mordor Intelligence | - |

| USD 162.90 million (2024) | Global Consultancy A | counts only UPS + PDU hardware and omits service revenue |

| USD 312.18 million (2024) | Industry Tracker B | bundles cooling power systems and assumes accelerated 15 kW-per-rack adoption |

The comparison shows that scope selection and density assumptions, rather than arithmetic errors, drive most gaps. By using a balanced equipment basket, realistic adoption curves, and an annual refresh, Mordor Intelligence delivers a transparent baseline that decision-makers can trace back to publicly verifiable variables and repeatable steps.

Key Questions Answered in the Report

How big is the Spain Data Center Power Market?

The Spain Data Center Power Market size is expected to reach USD 334.96 million in 2026 and grow at a CAGR of 8.62% to reach USD 506.36 million by 2031.

What is the current Spain Data Center Power Market size?

In 2026, the Spain Data Center Power Market size is expected to reach USD 334.96 million.

Who are the key players in Spain Data Center Power Market?

ABB Ltd., Eaton Corporation, Schneider Electric SE, Cisco Systems Inc. and Fujitsu Limited are the major companies operating in the Spain Data Center Power Market.

What years does this Spain Data Center Power Market cover, and what was the market size in 2025?

In 2025, the Spain Data Center Power Market size was estimated at USD 334.96 million. The report covers the Spain Data Center Power Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Spain Data Center Power Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: