Spain Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

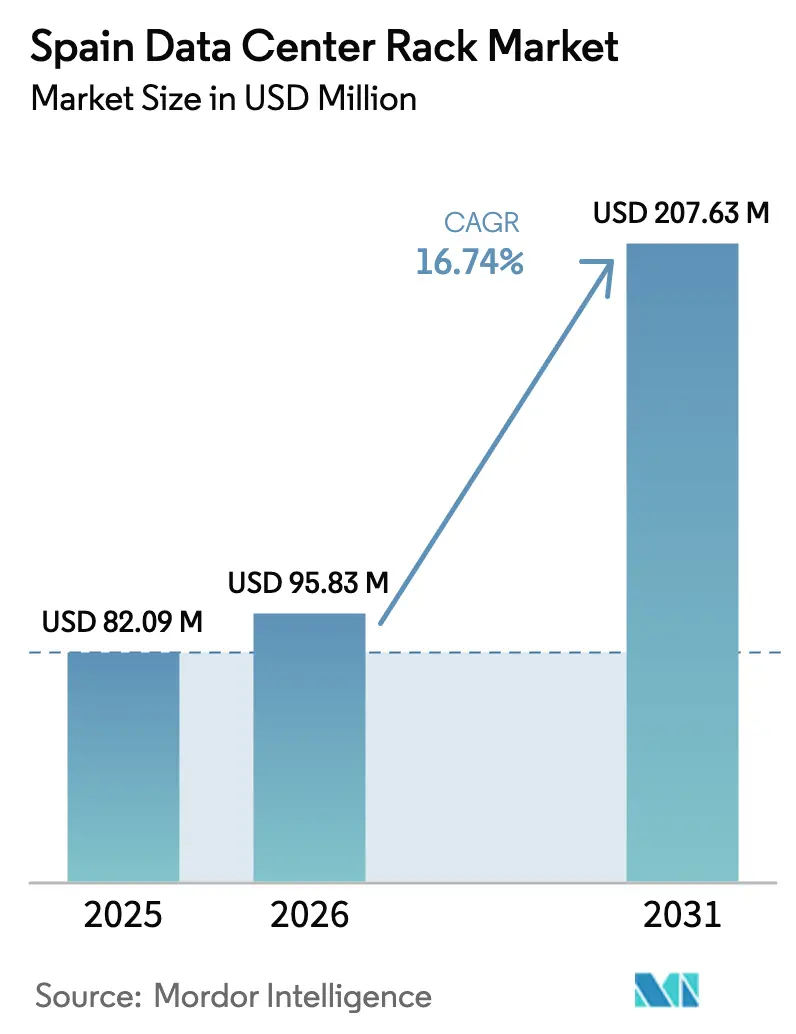

| Base Year Market Size (2025) | USD 82.09 Million |

| Market Size (2026) | USD 95.83 Million |

| Market Size (2031) | USD 207.63 Million |

| Growth Rate (2026 - 2031) | 16.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Data Center Rack Market Analysis by Mordor Intelligence

The Spain data center rack market size is expected to grow from USD 82.09 million in 2025 to USD 95.83 million in 2026 and is forecast to reach USD 207.63 million by 2031 at 16.74% CAGR over 2026-2031. Hyperscale capital expenditure topping EUR 8 billion is positioning Spain as Southern Europe’s digital crossroads, while submarine cable landings in Bilbao and Valencia underpin sustained international connectivity. Government-backed España Digital 2026 funds nationwide fiber and 5G backbones that channel fresh demand into colocation halls, even as AWS, Microsoft and Google pour USD 3 billion into hyperscale campuses designed for AI workloads exceeding 60 kW per rack. Rack densities are climbing to 120 kW in Aragón, prompting operators to favor liquid-ready 52U designs and integrated power distribution. Despite steel retaining 78.3% material share, aluminum’s 19.7% growth rate illustrates a pivot toward lighter, seismically resilient structures that ease installation near coastal cable landings.

Key Report Takeaways

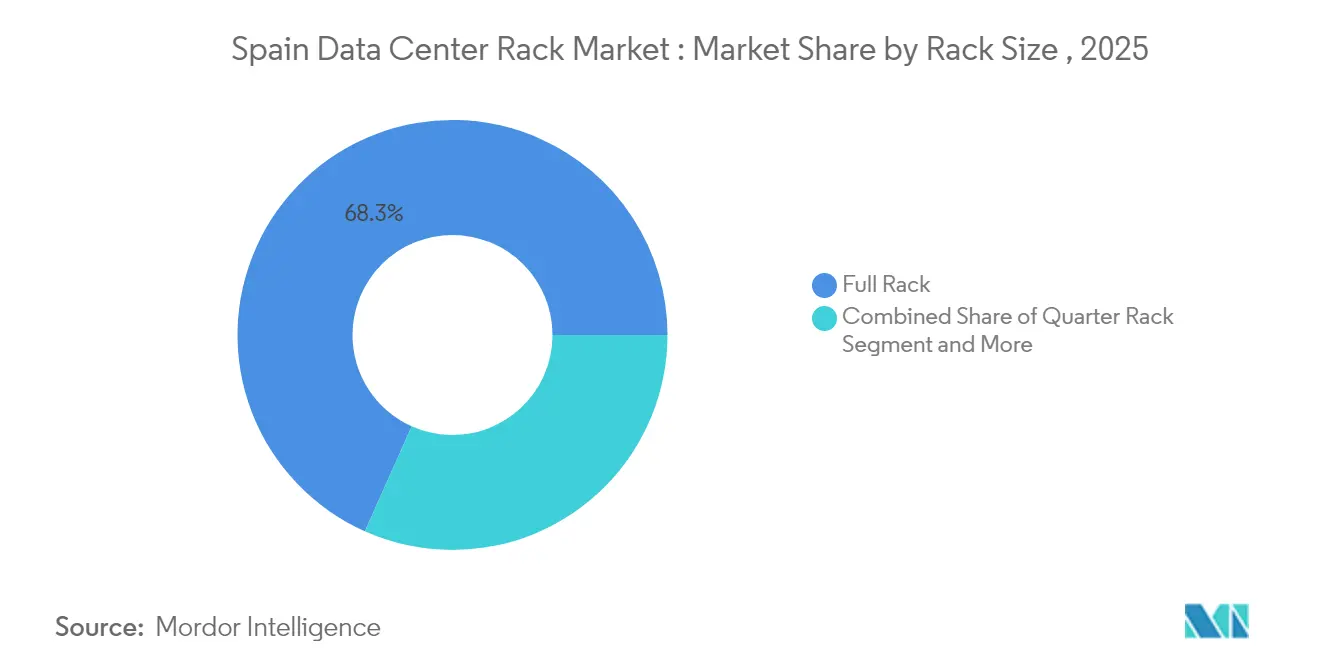

- By rack size, full racks led with 68.32% of Spain data center rack market share in 2025; the same segment is projected to expand at a 18.96% CAGR through 2031.

- By rack height, the standard 42U format held 54.61% share in 2025 in Spain data center rack market, while the 48U segment is forecast to grow fastest at 19.21% CAGR to 2031.

- By rack type, cabinet (closed) racks commanded 71.68% revenue share in 2025 in the Spain data center rack market and are advancing at a 20.62% CAGR on heightened security and airflow demands.

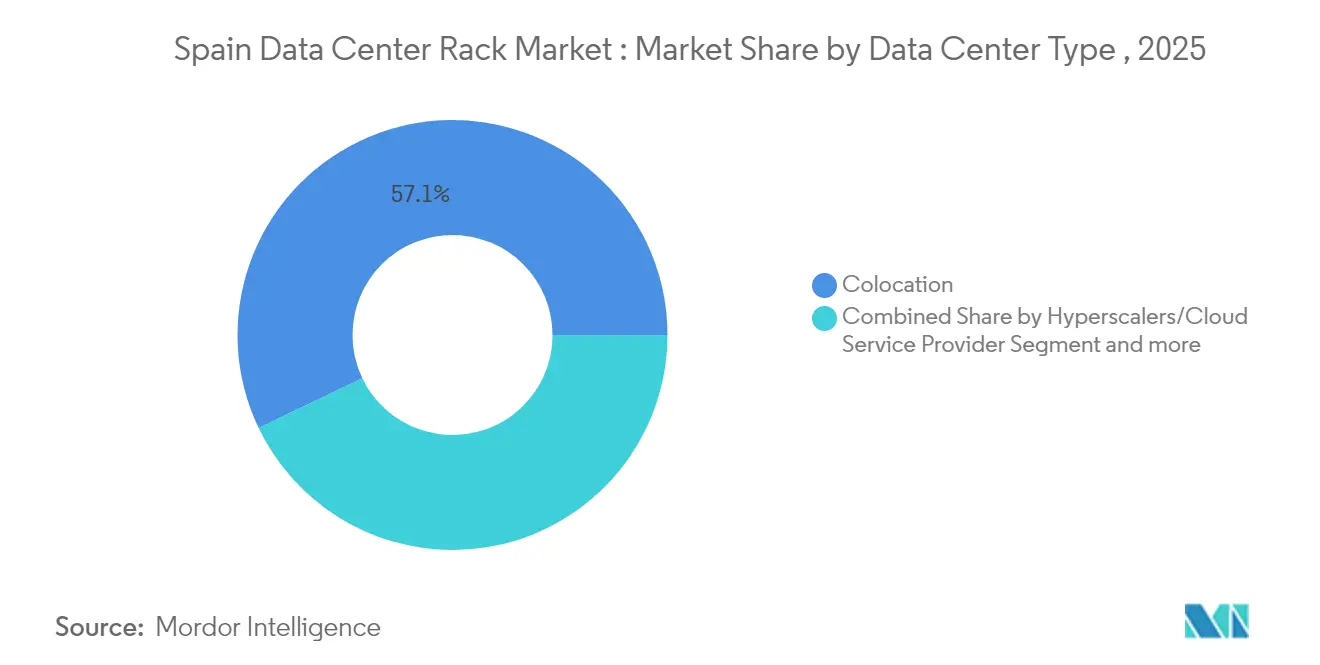

- By data-center type, colocation facilities held 57.12% revenue share in 2025 in the Spain data center rack market ; hyperscale builds are expected to grow at 18.88% CAGR through 2031.

- By material, steel accounted for 77.62% share in 2025 in the Spain data center rack market; aluminum registers the fastest rise at 19.05% CAGR given weight-reduction imperatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Expected changes in Spain many a times form part of a broader pattern of global movement rather than an isolated trend. The report on worldwide data center rack market outlook by Mordor Intelligence brings these expectations together.

Spain Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale build-outs by AWS, Microsoft and Google accelerating above 60 kW rack demand | + 4.2% | Madrid, Aragón, Barcelona | Medium term (2-4 years) |

| Edge-cloud roll-outs by Spanish telcos (Telefónica, Cellnex) require micro-racks | + 2.8% | National, with concentration in urban centers | Short term (≤ 2 years) |

| EU-funded "España Digital 2026" fibre and 5G backbone stimulates colocation growth | + 3.1% | National, priority in underserved regions | Medium term (2-4 years) |

| Corporate cloud migration in BFSI and public sector after Royal Decree-law 14/2019 compliance | + 2.3% | Madrid, Barcelona, regional capitals | Short term (≤ 2 years) |

| AI model training hubs in Aragón driving liquid-cool ready 52U racks | + 3.8% | Aragón, with spillover to Castilla-La Mancha | Long term (≥ 4 years) |

| Sub-sea cable landing in Bilbao (Grace Hopper, Medusa) lifting demand for seismic-rated racks | + 1.5% | Bilbao, Northern Spain coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale build-outs by AWS, Microsoft and Google accelerating above 60 kW rack demand

Hyperscale operators have re-defined specifications in the Spain data center rack market, standardizing 60 kW-plus designs to run generative-AI training clusters. AWS opened its Aragón region in 2024, Microsoft earmarked USD 2.1 billion for the Spain Central cloud region, and Google boosted Madrid capacity with USD 650 million, collectively stretching national power provisioning thresholds Amazon, Microsoft, Google. Their spending shifts preference toward 52U racks with liquid manifolds, heavier gauge cable ladders and frame tolerances exceeding 1,300 kg. Operators now demand integrated bus-bar power strips and tool-less airflow blanking panels to curb thermal hotspots that throttle GPUs. Procurement teams also insist on vendor stock harmonization across multiple campuses to streamline spares, making standardized full racks the baseline choice.

Edge-cloud roll-outs by Telefónica and Cellnex require micro-racks

Telefónica and Cellnex collectively oversee more than 10,462 tower and rooftop sites that are being upgraded to host edge compute pods supporting 5G slicing, connected-vehicle telemetry and AR streaming Cellnex. Space-limited shelters favor 6U-to-12U micro-racks featuring sealed doors, vibration dampers and DC power shelves compatible with telco battery strings. Vendors are responding with wall-mount enclosures carrying outdoor corrosion ratings and remotely monitored door sensors. Roll-outs concentrate inside Madrid’s M-30 ring and Barcelona’s metropolitan area where densification improves latency below 10 ms for IoT transactions. This distributed architecture widens the Spain data center rack market footprint beyond traditional halls, benefiting local fabricators that can deliver bespoke form factors inside shorter lead times.

EU-funded “España Digital 2026” backbone stimulates colocation growth

España Digital 2026 dedicates EUR 4 billion to boost fiber reach and 5G standalone cores, attracting colocation providers that package carrier-neutral cross-connects for enterprises pursuing latency-sensitive SaaS workloads [1] Ministerio de Ciencia e Innovación, “España Digital 2026 Roadmap,” ciencia.gob.es. Regional fiber loops cut backhaul costs for operators in Valencia, Málaga and Bilbao, inspiring new multi-tenant halls to pre-install 42U cabinet rows with modular roof chimneys ready for liquid retrofit. Government grants covering up to 50% of duct-laying expenses lower build costs, letting colo operators compete aggressively on rack rates while maintaining ISO 27001 and Tier III resilience. The initiative’s digital-sovereignty angle also encourages domestic cloud adoption among public agencies, further inflating demand for high-security cabinet racks.

AI training hubs in Aragón driving liquid-cool ready 52U racks

Aragón’s wind-and-solar mix delivers 68% renewable penetration and average industrial tariffs 18% below Madrid, making the region a magnet for GPU megafarms. Amazon’s three data center permits include annual water draws nearing 755,720 m³, signaling large-scale liquid cooling loops that need taller racks to house pumping manifolds and leak-detection rails . Operators specify 52U frames with 19-inch vertical pitch but deeper footprints to seat duplex CDU sets. Fabricators must reinforce caster load bearing and provide anodized aluminum rails resisting coolant corrosion. The Spain data center rack market sees parallel demand for dripless quick-disconnect fittings and ultrasonic flow meters embedded into the rack doors for live monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid congestion in Madrid and Barcelona delaying rack deployments | -2.1% | Madrid, Barcelona metropolitan areas | Short term (≤ 2 years) |

| Escalating steel prices impacting rack cost structure | -1.4% | National, with manufacturing concentration effects | Medium term (2–4 years) |

| Water-use restrictions curbing adoption of high-density chilled-water racks | -1.8% | National, acute in Catalonia and Andalusia | Medium term (2–4 years) |

| Talent shortage for liquid-cool maintenance raising OPEX and slowing adoption | -0.9% | Madrid, Barcelona, emerging data center hubs | Medium term (2–4 years) |

| Permitting delays for edge data center retrofits in heritage zones | -1.2% | Historic urban cores in Spain; notably Seville, Valencia, Granada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Power-grid congestion in Madrid and Barcelona delaying rack deployments

The April 2025 blackout that knocked out power to 55–60 million residents exposed system inertia gaps in a grid leaning on 59% solar generation. Data-center requests for new 120 kW circuits now face six-to-nine-month queue times at Madrid’s Vicálvaro substation, forcing operators to stagger rack installations in 2 MW tranches . Some hyperscalers are shifting expansion toward Zaragoza where redundant 400 kV feeds exist, but colos tied to urban fiber hubs must absorb diesel genset surcharges that add 6–8 EUR per rack monthly. The constraint dents Spain data center rack market momentum in the capital, amplifying interest in energy-efficient aluminum frames that shave power by improving airflow.

Water-use restrictions curbing chilled-water rack adoption

Spain’s worst drought in six decades leaves 78% of land at desertification risk, triggering municipal caps on industrial withdrawals in Catalonia and Andalusia. Traditional chilled-water CRAH loops consuming 1.5 liters per kWh are under scrutiny as city councils link construction permits to water-reuse ratios. Meta’s planned Talavera campus drawing 665 million liters yearly ignited public pushback, illustrating regulatory headwinds. Operators pivot to direct-to-chip or immersion cooling, yet these alternatives entail thicker door heat exchangers that only fit within custom 48U-plus cabinets, inflating capital outlays by 14–17%. Resultant procurement hesitancy trims forecast volumes for high-density rack SKUs until recyclable coolant ecosystems mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full-height frames dominate Spain’s capacity expansion

Full racks controlled 68.32% of shipments in 2025 and form the backbone of hyperscale halls ringing Madrid and Huesca. The Spain data center rack market size for the full-rack segment is projected to reach USD 141.86 million by 2031, underpinning the broader market’s 16.74% CAGR path. Standardizing on full frames lets operators maximize servers per square meter and simplify hot-aisle containment retrofits that preserve PUE below 1.3. Quarter and half racks still populate telecom closets and brownfield enterprise labs, yet their combined share is eroding as cloud migration lifts server consolidation ratios.

Adoption accelerates because global operators apply the same specifications used in Dublin, Frankfurt and Paris to Spanish builds, locking in economies of scale on cable trays, PDUs and door swing clearances. Vendors such as Eaton pre-assemble SmartRack bundles, with brush grommets, blanking panels and bus-way tap-off units, that roll directly onto raised floors, cutting site labor by 12 hours per rack. Contract manufacturers in Asturias and Navarre keep lead times under four weeks for custom color, seismic kits and LoRaWAN sensor rails, a differentiator in Spain data center rack market orders placed by fast-growing SaaS tenants.

By Rack Height: 48U adoption overtakes the 42U incumbent

The 42U format retained 54.61% share in 2025, yet operators now specify 48U enclosures to fit rear-door heat exchangers and extra breakers needed for 415 V three-phase feeds. The Spain data center rack market size for 48U designs is forecast to swell at 19.21% CAGR, mirroring AI GPU density curves. Taller frames raise total static load to 1,500 kg, necessitating welded steel corners or extruded aluminum columns with torsional ribs for stability during seismic events near Bilbao’s cable hubs.

Early adopters report that adding six rack units slashes row length by nearly 15%, freeing white-space for battery cabinets. Schneider Electric’s EcoStruxure firmware update in 2024 broadened environmental sensor support, encouraging facility teams to retrofit 48U rows with digital manifold gauges. Although shipping taller cabinets complicates pallet stacking, domestic carriers adapt with telescopic trailers, limiting freight premiums to 3%. This cost-containment bolsters migration from legacy 42U frames, keeping Spain data center rack market acceleration on track even amid steel inflation.

By Rack Type: Cabinet designs outpace open frames on security and airflow

Cabinet racks represented 71.68% revenue in 2025 and display a 20.62% CAGR through 2031 as Spanish banking, healthcare and public-sector tenants adopt stricter data-sovereignty protocols. Spain data center rack market share for cabinet variants is set to exceed 77.00% by 2027, reflecting mandated biometric locks and tamper-evident screws required under Royal Decree-law 14/2019. Closed doors enable differential pressure zones, permitting chilled rear-door coolers to reject 80% of thermal load without aisle containment.

Open-frame racks remain common in low-risk lab zones or HPC labs where technicians need 360-degree access, yet their share drops as cyber-insurance carriers tie premiums to physical intrusion safeguards. Cabinet makers integrate EMP mesh linings for defense-sector deployments near Madrid’s Torrejón base, a feature now requested by multinational banks migrating mainframes. The granular segmentation of rack SKUs lengthens buyers’ RFPs, but integrated bundles shorten installation cycles, elevating Spain data center rack market competitiveness for turnkey suppliers with in-house cooling IP.

By Data Center Type: Hyperscale growth eclipses colocation dominance

Colocation still accounts for 57.12% of 2025 shipments, sustained by inter-connect density in Madrid’s Las Rozas corridor. Yet hyperscalers show the fastest 18.88% CAGR as Amazon, Microsoft and Google channel capital toward purpose-built campuses in Aragón and Castilla-La Mancha. Correspondingly, the Spain data center rack market size tied to hyperscale facilities should surpass USD 101.6 million by 2031. Vertical integration lets hyperscalers dictate rack specifications, favoring 52U cabinet heights, integrated CDU rails and AI-ready bus-bar harnesses.

Colo operators respond by offering “build-to-suit” suites with 20-year power reservations and vendor-agnostic cage footprints. Smaller enterprise and edge nodes deployed by Telefónica along 5G routes adopt micro-rack arrays slotted into street-level shelters, diversifying revenue streams for Spanish fabricators. Overall, the dual-track deployment model, hyperscale for cloud-native workloads, colocation for latency-sensitive interconnects, enlarges the Spain data center rack market addressable base and buffers cyclicality.

By Material: Aluminum gains traction despite steel’s price edge

Steel held 77.62% of 2025 demand thanks to its low cost and 1,800 kg static-load limits. However, aluminum’s 19.05% CAGR underscores operator appetite for lighter frames that reduce craning loads and improve thermal dispersion. Structural alloys now feature magnesium to heighten tensile strength, letting aluminum racks match 1,200 kg capacities while weighing 35% less. Spain data center rack industry specifiers pair these frames with raised-floor isolation pads that cut seismic sway in Bilbao’s cable-landing halls.

High electricity tariffs hitting European smelters spur cost volatility, yet aluminum’s recyclability aligns with ESG metrics that grant hyperscalers power-usage exemptions. The EU Steel and Metals Action Plan’s 2025 subsidy round may narrow price differentials, but for now steel remains dominant where budget constraints trump weight. Hybrid solutions, steel posts with aluminum side panels, offer compromise options, reflecting continual product innovation driving Spain data center rack market resilience.

Geography Analysis

Madrid retained 60.84% of installed capacity in 2025 and anchors international peering exchanges, yet grid bottlenecks and land scarcity dampen new rack deployments. Aragón houses Spain’s cheapest renewable blend, allowing hyperscalers to secure 500 MW leases and plan rack densities of 120 kW without curtailment penalties. Barcelona remains the second-largest cluster, though Catalonia’s drought-triggered water quotas slow high-density liquid loops, nudging operators to implement airside economizers instead of chilled-water coils.

Northern Spain, led by Bilbao, commands growing interest due to Grace Hopper and Medusa cables, giving carriers sub-50 ms RTT to New York and Tel Aviv. Rack manufacturers court local colocation builds by stocking seismic kits rated to Zone 3 acceleration levels, a niche yet profitable opportunity within the Spain data center rack market. Valencia and Málaga attract edge deployments targeting Mediterranean tourist bandwidth spikes, leveraging municipal tax breaks for green building certifications. Regional governments compete on fast-track permitting and renewable PPAs; Castilla-La Mancha offers 10-year property-tax holidays that shift TCO calculus for hyperscalers weighing Zaragoza against Toledo. Spain’s robust rail network lets integrators stage racks in Madrid and dispatch overnight to satellite cities, mitigating logistics costs for dispersed builds. Consequently, the Spain data center rack market evolves from a Madrid-centric entity into a polycentric fabric optimized for both submarine cable proximity and renewable-energy availability.

Mordor Intelligence's coverage of the data center rack market extends across other regions including Europe, South America, and North America, while country-specific intelligence is also available for Netherlands, Denmark, Chile, Canada, Sweden, and Malaysia, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The competitive field skews moderately concentrated. Schneider Electric, Vertiv and Rittal collectively shipped 46.5% of 2024 volumes, bundling racks with bus-way, monitoring and cooling. Their Iberian warehouses enable 72-hour dispatch into Madrid’s Alcobendas campus lanes. Local firms such as Esnova Racks and Espaciorack differentiate through bespoke paint schemes and rapid prototype cycles, capturing finance and government contracts where Spanish-language engineering support is mandatory.

Legrand’s 17 data-center-focused acquisitions since 2010 expand its containment and power raceway catalog, allowing cross-selling into hyperscale bids. Dell and HPE deepen presence through factory-integrated rack-scale systems bundled with GPU sleds, aiming to secure AI cluster refreshes. Meanwhile, ODMs from Taiwan infiltrate via distribution partners, offering bare-frame options priced 12% below branded equivalents; however, warranty concerns limit uptake among regulated sectors.

Innovation priorities revolve around immersion-ready frames with polymer coatings, tool-less side panels and native support for DC bus-bar harnesses. Aluminum adoption acts as a product-differentiation lever, yet supply chain discipline is critical when London Metal Exchange premiums fluctuate. Strategic partnerships between rack vendors and cooling specialists, such as Vertiv’s tie-up with GRC for immersion tanks, underline converging value-chains inside the Spain data center rack market.

Spain Data Center Rack Industry Leaders

Eaton Corporation

Rittal GMBH & Co.KG

Schneider Electric SE

Vertiv Group Corp.

nVent Electric plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spain suffered a nationwide blackout impacting 55–60 million residents, spotlighting grid fragility and prompting data-center resilience upgrades.

- April 2025: Amazon’s Aragón campuses secured water licenses totaling 755,720 m³ annually, bolstering demand for liquid-ready racks.

- March 2025: The European Commission issued its Steel and Metals Action Plan, shaping raw-material pricing for rack manufacturing.

- February 2025: Microsoft confirmed USD 2.1 billion for the Spain Central region, triggering large cabinet orders.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spain data center rack market as all new, factory-built steel or aluminum enclosures, open frames, and wall-mount racks that host IT equipment inside Spanish colocation, hyperscale, enterprise, and edge facilities. Values are expressed in billed hardware revenue, net of installation.

Scope exclusion: specialized battery cabinets, overhead cable trays, and stand-alone server shelves are left outside this sizing.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with facility operators across Madrid, Barcelona, and Valencia, rack integrators, and thermal-management specialists helped validate shipment volumes, average selling prices, and refresh cycles. Follow-up surveys with cloud architects and procurement leads clarified the shift toward 48 U and 52 U formats and the growing share of closed cabinets in GPU rows.

Desk Research

We started with public indicators from Spanish energy and telecom regulators, customs shipment codes that isolate cabinets and frames, and trade association portals such as SPAIDC and the European Data Centre Association, which reveal build-out pace and import patterns. Additional context came from company 10-K filings, investor decks that break out infrastructure CAPEX, and reputable press releases that announce new halls or rack contracts.

To deepen historical perspective, our analysts tapped D&B Hoovers for vendor revenue splits, Dow Jones Factiva for project news flow, and Questel for recent patent clusters around high-density cabinet cooling. These feeds framed demand drivers, technology adoption, and competitive concentration. The sources listed are illustrative; many other publications were reviewed for data capture and cross-checks.

Market-Sizing & Forecasting

The model applies a top-down build. The installed rack base is reconstructed from MW additions, average rack density (kW per rack), and utilization ratios, which are then valued with verified ASPs. Results are corroborated through selective bottom-up checks, supplier roll-ups, and channel samples before being adjusted for in-flight expansions. Key inputs include annual hyperscale MW announced, colocation occupancy rates, aluminum price index, rack height mix evolution, and data sovereignty legislation that steers local hosting. Forecasts use multivariate regression combined with scenario analysis; growth paths of density and hyperscale CAPEX form the independent variables while macro GDP acts as a moderator. Gaps in bottom-up counts are bridged with weighted averages from our primary panel.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance screens against historical series, and reconciliation with external rack shipments. Models refresh each year; mid-cycle updates trigger if utility tariffs, landmark capacity deals, or currency swings move values by over five percent. A final pre-publication sweep ensures clients receive the latest view.

Why Mordor's Spain Data Center Rack Baseline Commands Reliability

Published estimates often differ because firms pick distinct rack categories, price bases, and refresh cadences.

Key gap drivers here include narrower cabinet-only definitions, older base years, or currency conversions that lag real-time ECB rates, all of which inflate or deflate totals relative to our 2025 USD view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 82.09 million (2025) | Mordor Intelligence | |

| USD 74.9 million (2023) | Regional Consultancy A | older baseline and partial inclusion of open frames only |

| USD 95 million (2024) | Global Consultancy B | aggregates racks with enclosures, excludes edge micro-sites, currency averaged annually |

The comparison shows that once scope, timing, and price assumptions are aligned, our number sits mid-range, signaling a balanced, transparent baseline that decision-makers can retrace through clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current valuation of the Spain data center rack market?

The market is valued at USD 95.83 million in 2026 and is projected to reach USD 207.63 million by 2031.

Which rack type leads demand in Spain

Cabinet (closed) racks dominate with 71.68% revenue share in 2025 and post a 20.62% CAGR through 2031 on heightened security and airflow control needs.

Why are 48U cabinets gaining traction over 42U models?

AI workloads require extra vertical space for liquid cooling manifolds and redundant PDUs, driving 48U designs to a 19.21% CAGR.

How are power-grid constraints affecting data center builds?

Madrid and Barcelona face queue times up to nine months for new circuits, delaying high-density rack roll-outs and shifting some projects to Aragón.

Page last updated on: