Mexico Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

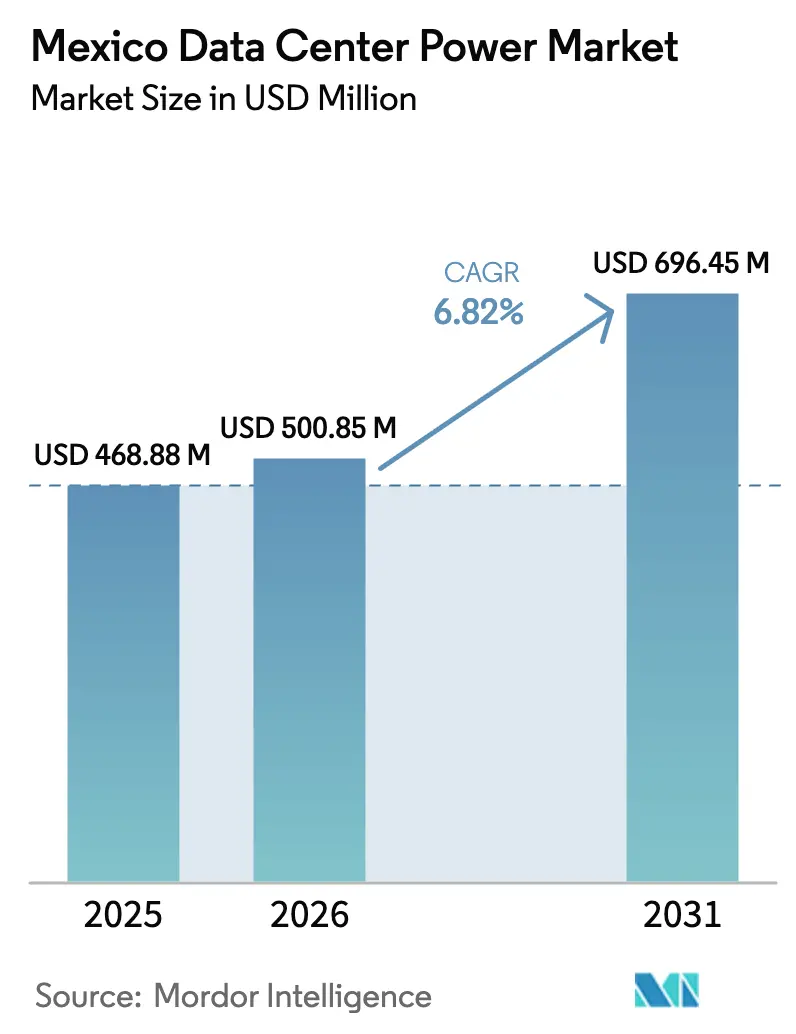

| Base Year Market Size (2025) | USD 468.88 Million |

| Market Size (2026) | USD 500.85 Million |

| Market Size (2031) | USD 696.45 Million |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

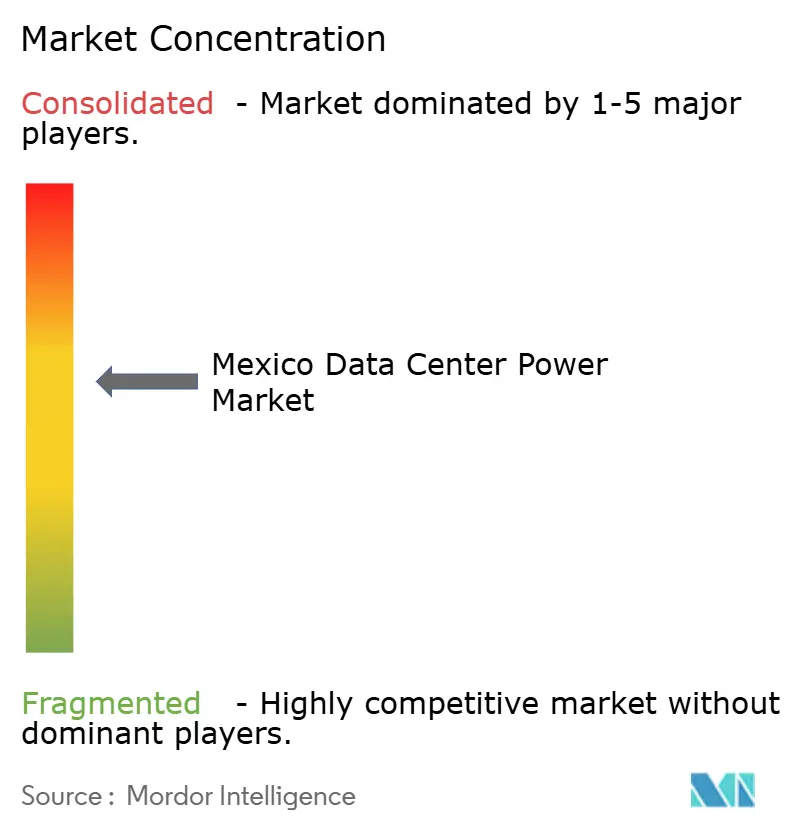

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Data Center Power Market Analysis by Mordor Intelligence

The Mexico data center power market size was valued at USD 468.88 million in 2025 and estimated to grow from USD 500.85 million in 2026 to reach USD 696.45 million by 2031, at a CAGR of 6.82% during the forecast period (2026-2031). Growth is powered by nearshoring-led digitalization, rapid hyperscale cloud expansion, and mounting AI workloads that increase rack-level power density. Federal incentives under Plan México foster capital inflows into new campuses, while operators adopt energy-efficient UPS and PDU technologies to curb operating expenses. Renewable power purchase agreements (PPAs) and battery storage are gaining traction as firms align with 2030 carbon-neutrality targets. Grid instability remains the chief operational risk, prompting widespread N+1 and 2N redundancy designs and a shift to Tier IV certifications in mission-critical builds.

Key Report Takeaways

- By component, UPS systems led with 35.62% revenue share in 2025; PDUs are forecast to expand at an 7.75% CAGR through 2031.

- By data center type, colocation held 44.72% of the Mexico data center power market share in 2025, while hyperscale/cloud services are advancing at a 9.12% CAGR to 2031

- By size, large facilities accounted for 45.85% of the Mexico data center power market size in 2025; mega centers are growing at an 8.31% CAGR through 2031.

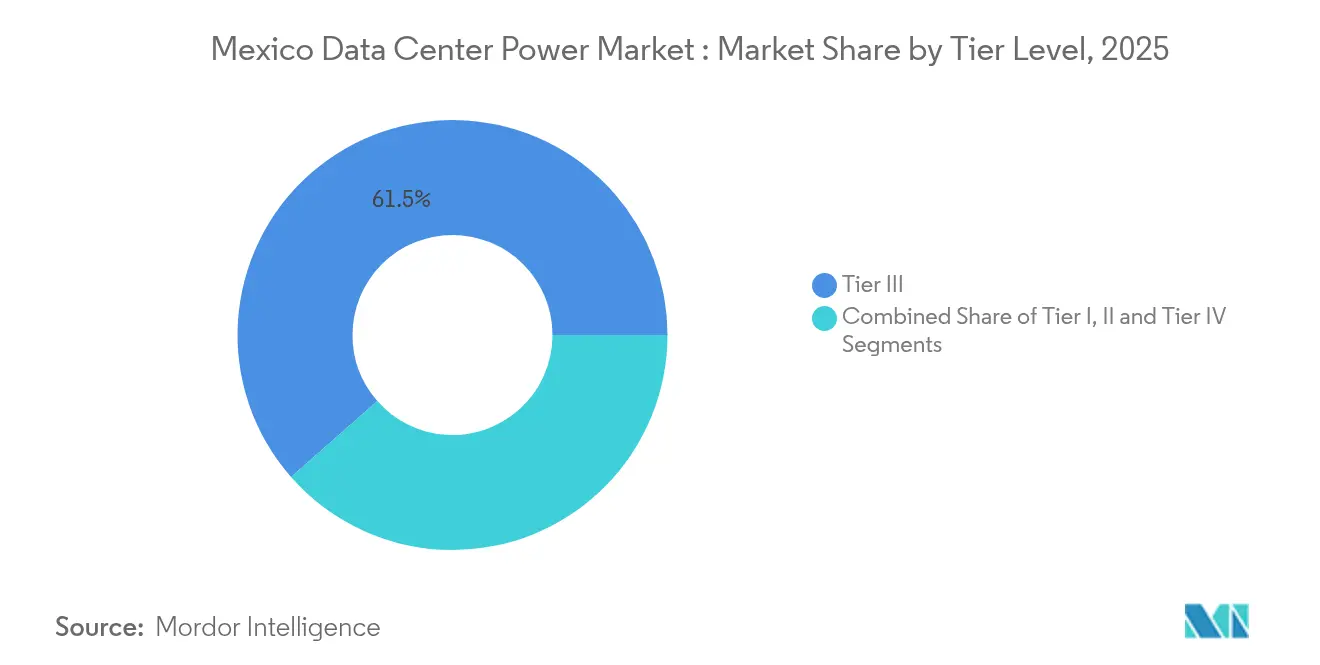

- By tier level, Tier III sites captured 61.48% revenue share in 2025, whereas Tier IV implementations post the fastest 9.02% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale & cloud build-out acceleration | +2.1% | National, with concentration in Querétaro, Mexico City | Medium term (2-4 years) |

| Energy-efficiency & OpEx reduction mandates | +1.3% | National | Long term (≥ 4 years) |

| Federal incentives under Mexico Digital Agenda | +0.9% | National | Medium term (2-4 years) |

| Near-shoring led edge DC proliferation on US–MX border | +1.8% | Northern Mexico (Monterrey, Tijuana, Ciudad Juárez) | Short term (≤ 2 years) |

| Surplus renewable-PPA availability for green DC power | +0.7% | Querétaro, Mexico City, Guadalajara | Long term (≥ 4 years) |

| 5G-driven ultra-low-latency micro-DC roll-outs | +0.5% | Urban centers nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale & Cloud Build-out Acceleration: Transforming Mexico’s Digital Landscape

Cloud majors are commissioning multi-megawatt campuses to serve regional AI and SaaS demand. Microsoft launched its first Mexican cloud region in 2024, while AWS committed USD 5 billion for three facilities in Querétaro by 2025. These builds alone require more than 700 MW of commissioned power, pressuring the grid and creating strong pull for high-efficiency switchgear and modular UPS. Providers are clustering near renewable corridors to secure long-term PPAs and meet corporate sustainability pledges. Utility coordination now influences site selection more than fiber availability, reshaping the competitive map of the Mexico data center power market.

Energy-Efficiency & OpEx Reduction Mandates: Driving Innovation in Power Management

Electricity can account for 60% of Mexican data-center operating costs. Operators therefore prioritize low-loss power paths, lithium-ion UPS, and wider temperature envelopes. Equinix achieved a PUE of 1.5 in several facilities by combining advanced airflow, liquid cooling, and ISO 50001 energy-management programs. ABB’s 98% efficient UPS line trims conversion losses, producing immediate savings and shorter payback periods. [1]ABB, “The Drive Towards Energy-Efficient Data Centres,” abb.comThese measures enhance competitiveness as hyperscalers benchmark local costs against U.S. counterparts.

Federal Incentives Under Mexico Digital Agenda: Catalyzing Investment

Plan México grants tax deductions of 41%–91% on fixed assets tied to data-center builds, power generation, and technology R&D during 2025–2026. [2]Covington & Burling, “President Sheinbaum's Mexico Plan,” cov.com The program also targets a 22 GW national capacity increase, with priority for solar and wind. These measures de-risk large-scale projects and accelerate timelines, especially in second-tier cities where land is plentiful. Investors anticipate faster NIMBY approvals under streamlined permitting rules.

Nearshoring-Led Edge DC Proliferation on the US–MX Border: Redefining Regional Connectivity

Manufacturers relocating from Asia need sub-5 ms latency for production control and supply-chain analytics. Edge facilities in Monterrey, Tijuana, and Ciudad Juárez fill this need, typically consuming under 1 MW yet demanding highly efficient rack-level PDUs. MDC Data Centers’ new cross-border hub improves interconnection between Mexican carriers and U.S. IXPs, underscoring the convergence of telecom and compute services. Edge growth diversifies the Mexico data center power market, mitigating over-reliance on central hubs.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation & maintenance costs | -1.2% | National | Medium term (2-4 years) |

| Grid unreliability requiring costly redundancy | -1.6% | National, particularly severe in emerging data center hubs | Short term (≤ 2 years) |

| Lengthy permitting in industrial growth corridors | -0.8% | Querétaro, Mexico City, Monterrey | Short term (≤ 2 years) |

| Scarcity of certified DC-power engineers | -0.7% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation & Maintenance Costs: Challenging ROI Calculations

Building a Tier III facility in Mexico averages USD 38 million per MW, with power infrastructure as the largest cost share.[3]Bank of America, “Industrials/Multi-Industry: Who Makes the Data Center,”bankofamerica.com/ Import duties on switchgear and batteries raise the capex further. Smaller domestic players struggle to access financing, consolidating the market around capital-rich multinationals. To manage risk, operators favor modular builds that align expenditure with occupancy ramp-up.

Grid Unreliability Requiring Costly Redundancy: The Power Paradox

The national grid needs an estimated USD 8.8 billion upgrade to support 70 planned data centers by 2029. Frequent voltage sags force operators to deploy 2N generators and battery banks, inflating both capex and opex. Adoption of Hydrotreated Vegetable Oil (HVO) in backup gensets reduces emissions yet adds fuel procurement complexity. This paradox offsets Mexico’s cost advantage in electricity tariffs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Anchor Reliability and Spur Innovation

UPS systems captured 35.62% revenue in 2025, underlining their role as the primary defense against Mexico’s unstable utility feed. Lithium-ion chemistry adoption lowers floor space and cuts refresh cycles, supporting densification trends. Hybrid-mode UPS with eco-mode features slashes conversion losses by 70% during normal operation, supporting payback periods under three years. Modular designs grant live-swap capability, reducing mean time to repair and thus bolstering the Mexico data center power market.

PDUs post the fastest 7.75% CAGR through 2031 as rack-level densities surpass 15 kW. Intelligent PDUs with outlet-level metering allow AI-driven load balancing that trims stranded power. Environmental sensors integrated into PDUs feed holistic DCIM suites, driving preventive maintenance. Generator demand persists despite sustainability pressures; OEMs now bundle HVO-ready engine packages to retain compliance with emerging carbon norms. Service revenues rise in tandem, reflecting a skills shortage in certified power engineers.

By Data Center Type: Colocation Dominance Meets Hyperscale Surge

Colocation providers owned 44.72% of the Mexico data center power market share in 2025, offering enterprises a capex-light path to compliant infrastructure. These sites average 8 kW per rack and integrate carrier-neutral meet-me rooms that support cloud on-ramps. As companies repatriate critical workloads from the U.S., demand for in-country compliance and data sovereignty strengthens colocation bookings.

Hyperscale operators grow at 9.12% CAGR by deploying 20 MW-plus campuses with water-free cooling and on-site substations. Their build-to-core model accelerates component volumes, benefiting switchgear and bus-duct suppliers active in the Mexico data center power industry. Enterprise and edge sites remain relevant for specific latency-sensitive applications such as smart manufacturing, forming a balanced ecosystem that stabilizes nationwide demand for power equipment.

By Data Center Size: Large Facilities Lead, Mega Sites Accelerate

Large facilities between 5 MW and 10 MW held 45.85% revenue in 2025. They achieve economies of scale while keeping land and interconnection costs manageable. Operators favor N+1 topology in these sites, balancing uptime with lower redundancy spend.

Mega facilities, defined at 30 MW and above, expand at 8.31% CAGR. ODATA’s 300 MW campus exemplifies this leap, featuring 2N + 1 electrical paths and scalable blocks energized in 50 MW phases.As AI training clusters demand contiguous power, mega designs pull in higher-capacity transformers and medium-voltage UPS, altering the supply-chain landscape of the Mexico data center power market size.

By Tier Level: Tier III as Baseline, Tier IV Gains Strategic Ground

Tier III sites delivered 61.48% of 2025 revenue due to their cost-versus-uptime balance and 99.982% availability. These facilities rely on N+1 architecture, providing concurrent maintainability attractive to finance and ecommerce workloads. Tier IV grows fastest at 9.02% CAGR to serve fintech, healthcare, and government mandates for fault tolerance. HostDime’s 6 MW Guadalajara build uses 2N + 1 electrical paths and isolated redundant distribution, reflecting an industry-wide pivot toward zero single-point-of-failure designs. The premium spend on Tier IV encourages strategic colocation partnerships where cost is shared across anchor tenants.

Geography Analysis

Mexico City retains relevance due to its concentration of finance and public services. Claro Triara’s Tier IV complex illustrates best-practice redundancy, pairing dual feeds with diesel-HVO gensets to maintain 99.995% uptime. Urban density limits new builds, so brownfield modernization dominates investment patterns, emphasizing higher-efficiency PDUs and predictive analytics.

Northern border cities Monterrey, Tijuana, Ciudad Juárez benefit from nearshoring and demand for sub-10 ms latency to U.S. endpoints. Scala Data Centers’ USD 80 million Tepotzotlán site (5 MW expandable to 7.9 MW) showcases this secondary-market momentum. Variability in grid strength leads operators to favor modular containerized power rooms that can relocate if utility expansion lags.

Competitive Landscape

Global power majors ABB, Schneider Electric, Vertiv, Eaton—dominate supply, each offering UPS, bus-duct, and DCIM portfolios tailored to Mexico’s high-temperature, high-altitude environment. Siemens Energy’s 2025 alliance with Eaton underscores the trend toward vertically integrated solutions spanning generation to rack distribution

Regional system integrators fill service gaps with 24/7 maintenance and rapid-response spares depots, critical in secondary cities where OEM footprints remain thin. Edge deployments open white-space for niche suppliers of plug-and-play power modules and lithium-ion battery cabinets optimized for 1 MW micro-sites. Renewable mandates spur innovation in grid-interactive UPS and hydrogen-ready generators, differentiating vendors in contract tenders.

Mexico Data Center Power Industry Leaders

ABB Ltd.

Caterpillar Inc.

Cummins Inc.

Eaton Corporation plc

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ODATA inaugurated a USD 3 billion, 400 MW campus in Querétaro, energizing 200 MW during phase 1

- May 2025: Siemens Energy and Eaton partnered to co-engineer renewable-compliant power chains for Mexican data centers.

- February 2025: Alibaba Cloud opened a new cloud region in Mexico, intensifying hyperscale competition.

- January 2025: Plan México introduced tax deductions up to 91% for data-center fixed assets, alongside a 22 GW generation-expansion pledge.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Mexico data center power market as all on-site electrical infrastructure, uninterruptible power supply systems, power distribution units, switchgear, transfer switches, generators, and associated services installed to deliver continuous, redundant electricity to IT racks housed in purpose-built or colocation facilities across the country.

Scope Exclusions: Grid electricity sales and non-electrical building systems such as chillers and CRAH/CRAC cooling units sit outside this assessment.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with facility design engineers, colocation procurement heads, and utility planners across Querétaro, Monterrey, and Mexico City. Discussions validated real-world lead times for generator sets, typical UPS price per kVA bands, and forecast adoption of Tier IV architectures, filling data gaps left by secondary sources.

Desk Research

We began with trade regulation reviews from Mexico's Energy Regulatory Commission and Secretaría de Energía, followed by customs import data that detail shipments of UPS modules above 20 kVA. Industry white papers from the Uptime Institute, statistics from the International Energy Agency, and investment filings on BMV for listed power equipment vendors supplied baseline volume, pricing, and commissioning trends. Additional insight flowed from tier-1 sources such as OECD power intensity tables, data center project registries published by Querétaro's local government, and news archives accessed through Dow Jones Factiva. These sources illustrate capacity pipelines, redundancy preferences, and average selling prices. The list is indicative; many other public and paid references informed the desk phase.

Patent abstracts mined through Questel helped us trace emerging lithium-ion UPS chemistries, while D&B Hoovers financials verified revenue splits for OEMs operating in Mexico. Such triangulation flags technology shifts that influence our component mix outlook.

Market-Sizing & Forecasting

A top-down construct starts with installed and planned IT load (MW) published by state authorities, which we convert into power infrastructure spend using penetration coefficients for UPS, PDUs, and generators. Results are cross-checked through selective bottom-up roll-ups of major supplier revenues and sampled ASP times volume calculations. Key drivers modeled include hyperscale rack density, grid stability indices, average diesel price, nearshoring-led server demand, and Tier transition rates. Forecasts employ multivariate regression with scenario analysis to capture swings in federal energy policy and renewable integration costs. Where bottom-up estimates showed gaps, we interpolated using weighted regional benchmarks before reconciling to the master model.

Data Validation & Update Cycle

Outputs undergo variance checks against historic import values and quarterly OEM disclosures; anomalies trigger a second analyst review. Reports refresh each year, with interim revisions when material events, such as CFE tariff changes, shift assumptions. A final pre-publication sweep ensures clients receive the most current view.

Why Mordor's Mexico Data Center Power Baseline Earns Trust

Published numbers often diverge because firms differ on component scope, redundancy tiers considered, and refresh cadence.

Our disciplined variable selection and annual update cycle keep the baseline firmly anchored.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 468.88 Mn (2025) | Mordor Intelligence | - |

| USD 437 Mn (2024) | Global Consultancy A | Excludes Tier IV sites; applies regional ASPs that ignore peso depreciation |

| USD 167.9 Mn (2024) | Trade Journal B | Counts only solutions revenue, omits services and medium voltage switchgear |

These comparisons show that Mordor's balanced split between component and service revenues, peso-adjusted pricing, and inclusion of future-ready Tier IV deployments produces a dependable, transparent baseline that decision-makers can replicate and stress test with confidence.

Key Questions Answered in the Report

What is the current value of the Mexico data center power market?

The market is valued at USD 500.85 million in 2026 and is forecast to reach USD 696.45 million by 2031

Which component category leads spending in Mexican data centers?

UPS systems account for 35.62% of 2025 revenue, reflecting their central role in safeguarding operations against grid instability.

How do federal incentives support new data-center builds?

Plan México provides tax deductions of 41%–91% on qualifying assets and targets a 22 GW increase in generation capacity, lowering project payback periods.

What strategies are operators using to cope with grid unreliability?

Firms deploy N+1 or 2N redundancy, integrate battery storage, and adopt HVO-ready generators to ensure continuous power.

Page last updated on: