Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.84 Billion |

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 3.99 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

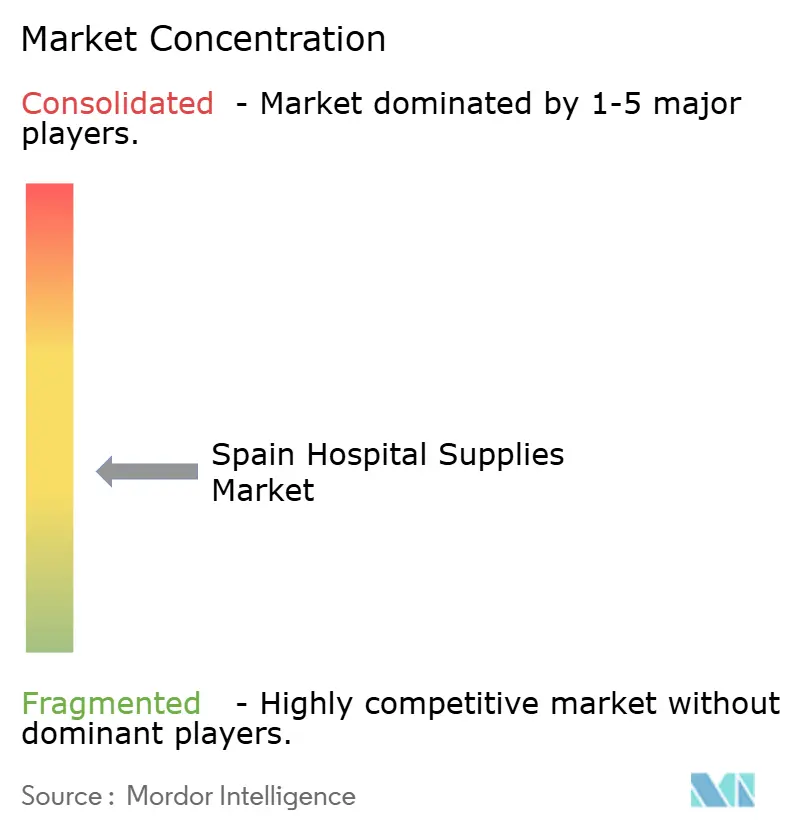

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Hospital Supplies Market Analysis by Mordor Intelligence

The Spain hospital supplies market size is expected to grow from USD 2.84 billion in 2025 to USD 3.01 billion in 2026 and is forecast to reach USD 3.99 billion by 2031 at 5.83% CAGR over 2026-2031. Spain’s solid public-sector foundation, together with targeted Recovery and Resilience Facility investments, underpins this consistent trajectory even as other European healthcare systems show greater volatility. Rising life expectancy, a sharply expanding population segment aged 90 years and above, and stricter infection-prevention standards reinforce equipment renewal cycles, while digital procurement mandates accelerate order fulfilment. Global multinationals and domestic specialists compete on value, compliance support and rapid logistics, creating a balanced yet dynamic competitive field. Continued EU harmonisation through the Medical Device Regulation (MDR) and the European Health Data Space is driving both standardisation benefits and added compliance costs.

Key Report Takeaways

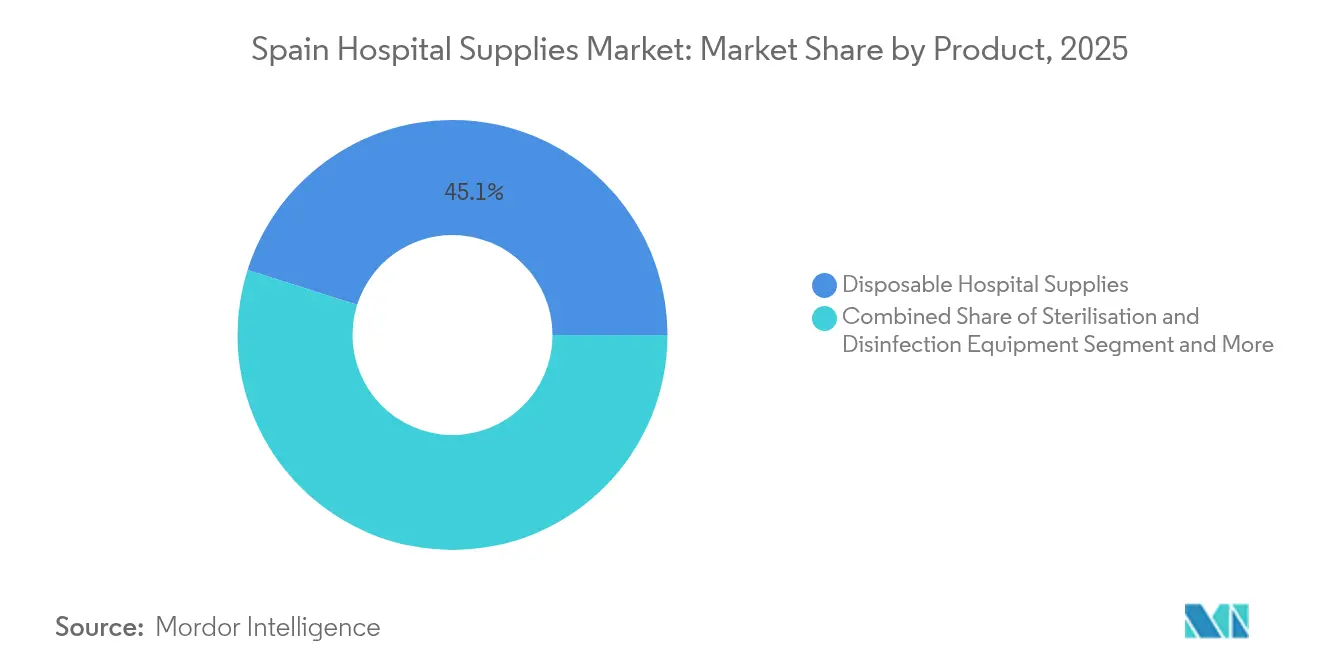

- By product, disposable hospital supplies held 45.12% of Spain hospital supplies market share in 2025; sterilisation and disinfection equipment is projected to register the fastest 7.56% CAGR to 2031.

- By end-user facility, public hospitals commanded 62.10% of the Spain hospital supplies market size in 2025, while private hospitals are expanding the quickest at a 6.76% CAGR through 2031.

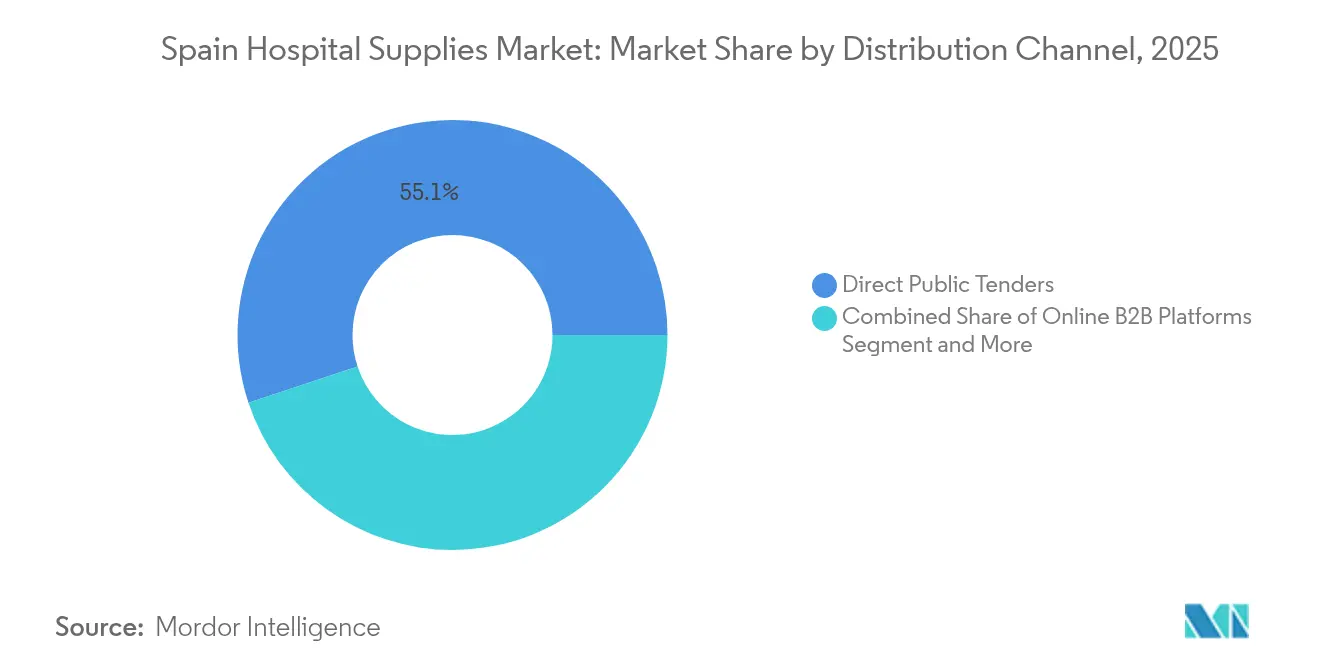

- By distribution channel, direct public tenders retained 55.10% share in 2025; online B2B platforms are set to grow at a 9.69% CAGR on the back of mandatory e-invoicing legislation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of infectious & chronic diseases | +1.2% | National, urban centres | Medium term (2-4 years) |

| Growing awareness of hospital-acquired infections | +0.8% | National, acute-care facilities | Short term (≤ 2 years) |

| Rapidly ageing Spanish population | +1.5% | National, rural weight | Long term (≥ 4 years) |

| Digitalised public procurement accelerating fulfilment | +0.6% | National, regional governments | Medium term (2-4 years) |

| EU RRF funds modernising hospital infrastructure | +0.9% | National, underserved areas | Short term (≤ 2 years) |

| Domestic single-use plastics capacity expansions | +0.4% | Catalonia & Valencia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Infectious & Chronic Diseases

Surveillance data show that 7.1% of EU hospital patients experience healthcare-associated infections, with respiratory conditions at the forefront[1]European Centre for Disease Prevention and Control, “Healthcare-Associated Infections,” ecdc.europa.eu. Spain’s universal health system guarantees treatment for those cases, translating into predictable bulk procurement of diagnostic kits, sterile consumables and respiratory support devices. The 2024 Universal Health-Care Bill extended coverage to temporary residents and asylum seekers, widening the beneficiary pool. As hospitals integrate chronic-care and infection-control pathways, suppliers benefit from bundled tenders that combine disposables with automated sterilisation units, while analytics-enabled devices support longitudinal disease management across inpatient and outpatient settings.

Growing Awareness of Hospital-Acquired Infections

An estimated 3.5 million HAI cases and more than 90,000 related deaths occur annually across the EU, up to half of which are preventable through stronger infection-control practices. Spanish hospitals respond by favouring CE-marked single-use devices and traceable sterilisation systems that comply with MDR post-market surveillance rules. Tender specifications increasingly reference antimicrobial surfaces and closed-system drug-transfer solutions, rewarding vendors that certify ISO-compliant clean-room manufacturing. As procurement teams quantify the cost of outbreak containment versus up-front product premiums, infection-control portfolios gain strategic weight.

Rapidly Ageing Spanish Population

Citizens over 90 years old reached 608,321 by 2023, a 58.29% jump in a decade. Ageing prompts steady demand for wound-management dressings, mobility aids and implantable devices. The European Central Bank projects ageing-related fiscal costs in Spain to rise by 7 percentage points of GDP by 2070, the highest in the euro area. Hospitals must therefore retrofit wards for geriatric care, install low-height beds and adopt remote monitoring to reduce readmissions, creating multi-year equipment replacement cycles that favour suppliers with modular, upgrade-ready systems.

Digitalised Public Procurement Accelerating Fulfilment

Spain’s FACe e-invoicing hub now processes more than 12 million invoices per year, while Law 18/2022 obliges companies above EUR 8 million revenue to issue electronic bills within one year of regulatory approval. The Plataforma de Contratación del Sector Público provides real-time tender notices, shrinking quotation lead times. This digitisation accelerates replenishment of frequently-used disposables, encourages smaller firms to bid nationwide, and underpins the 9.85% CAGR forecast for online B2B platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory framework | –0.7% | Nationwide, EU compliance | Long term (≥ 4 years) |

| Shift toward home-care services | –0.5% | Urban hubs | Medium term (2-4 years) |

| EU plastic-tax driven input-cost volatility | –0.3% | National, packaging items | Short term (≤ 2 years) |

| Fragmented regional-budget procurement cycles | –0.4% | 17 autonomous communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Framework

The MDR requires legacy devices to align with updated quality-management standards by May 2024, while transitional grace periods run no later than December 2028. Spain’s AEMPS further obliges in-country registration of all medical devices and mandates supply-interruption notifications under Regulation (EU) 2024/1860. Smaller manufacturers face high compliance costs for risk-based classification, unique-device identification labelling and periodic safety-update reports. Consequently, distributors consolidate their portfolios around MDR-approved products, potentially narrowing brand choice and lengthening market-entry timelines for innovative SMEs.

Shift Toward Home-Care Services

Policy makers and patients increasingly favour home-based chronic-disease management to alleviate hospital bed shortages. The InCARE study shows Spain’s long-term-care model emphasises personal autonomy, with family caregivers playing a critical role[2]InCARE Project, “Long-Term-Care System in Spain,” incare.euro.centre.org. Funds earmarked for telehealth and remote-monitoring pilots reduce certain procedure volumes within hospitals, dampening demand for selected inpatient consumables. Suppliers aiming to offset this trend tailor kits for domiciliary infusion, wound care and portable diagnostics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Disposables Drive Infection-Control Priorities

Disposable hospital supplies accounted for 45.12% of Spain hospital supplies market share in 2025, reflecting persistent emphasis on single-use safety protocols. Sterilisation and disinfection equipment, posting a 7.56% CAGR to 2031, benefits from rising HAI awareness and MDR traceability rules. The Spain hospital supplies market size for sterilisation systems is projected to expand steadily as hospitals upgrade to low-temperature and hydrogen-peroxide units that protect heat-sensitive devices.

Operating-room equipment and diagnostic instruments continue to receive budget allocations tied to Recovery Plan grants, while syringe and needle specifications evolve following ophthalmology safety alerts on silicone-oil droplets. Suppliers of CE-marked micro-volume syringes with zero residual volume capture niche but high-value orders.

By End-User Facility: Public Hospitals Anchor Demand

Public facilities represented 62.10% of Spain hospital supplies market size in 2025, mirroring the tax-funded Sistema Nacional de Salud’s nationwide reach. Procurement frameworks stipulate open, competitive tenders with multi-year supply contracts, providing volume stability but lower margin.

Private hospitals, though smaller, are forecast to grow 6.76% annually as investors target specialist care and medical tourism. Technology-heavy private clinics favour premium imaging, robotic-surgery and point-of-care testing devices to differentiate services, expanding addressable revenue pools for high-capability vendors.

By Distribution Channel: Digital Transformation Accelerates

Direct public tenders controlled 55.10% of 2025 purchases, underpinned by obligatory use of the FACe and PLACE portals for invoice routing and contract publishing. Nonetheless, the Spain hospital supplies market is rapidly pivoting toward electronic catalogues, and online B2B platforms will post a 9.69% CAGR to 2031 as e-invoicing enforcement spreads to firms below the EUR 8 million threshold.

Group purchasing organisations pool demand for smaller clinics, while retail and community pharmacies fill urgent gaps for ambulatory care. Multinationals increasingly integrate ERP systems with public portals to automate order confirmation and shipment tracking, cutting average lead times from days to hours.

Geography Analysis

Spain is the EU’s fourth-largest public healthcare spender, committing USD 99 billion of public funds in 2025—7.4% of GDP—and a further USD 35 billion from private sources. Madrid, Catalonia and Valencia host the densest hospital networks and the majority of high-complexity referral centres. Urban hubs capture early deployments of AI-enabled endoscopy towers, closed-loop sterilisation and automated drug compounding, raising per-bed expenditure above the national average.

Rural regions face physician shortages and longer logistics chains, prompting a shift to mobile diagnostics and modular treatment units. Recovery Plan grants target these underserved areas with digital radiology vans, negative-pressure tent systems and tele-ICU platforms, expanding the Spain hospital supplies market while easing urban congestion.

Manufacturing clusters along the Mediterranean corridor enhance supply security. Facilities such as Essity’s Tarragona plant and QIAGEN’s QIAstat-Dx site in Barcelona shorten lead times for critical consumables and diagnostics. Port infrastructure in Valencia and Barcelona facilitates raw-material imports and finished-goods exports, positioning Spain as a potential distribution hub for southern Europe and northern Africa.

Competitive Landscape

The Spain hospital supplies industry is moderately fragmented. Global groups—Solventum, B. Braun, Medtronic—leverage broad portfolios and MDR-compliant quality systems, securing framework agreements with regional health ministries. Domestic champions Grifols, Werfen and ROVI exploit deep clinician relationships and rapid service response; Grifols recorded EUR 7.212 billion revenue in 2024 and continues to expand immunoglobulin production capacity[3]Europa Press, “Grifols 2024 Financial Results,” europapress.es.

Recent strategies centre on digital supply-chain visibility and in-house sustainability programmes. Werfen’s EUR 20 million venture fund targets start-ups in rapid sepsis diagnosis, reinforcing its critical-care franchise. Essity deploys real-time OEE dashboards across its Spanish plants to cut downtime and plastic waste. Competitors are also tailoring product lines for home-care settings—portable suction units, wearable infusion pumps—to counter volume shifts away from inpatient wards.

Cross-border M&A remains active as MDR compliance expenses rise: private-equity interest in medium-sized Spanish manufacturers is growing, exemplified by ongoing speculation over a potential Brookfield offer for Grifols. Larger acquirers gain immediate CE-mark portfolios and established e-tendering credentials, while sellers gain the capital to fund next-generation R&D.

Spain Hospital Supplies Industry Leaders

Cardinal Health Inc.

Medtronic plc

B. Braun SE

GE HealthCare Technologies Inc.

Solventum Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Essity opened a EUR 24 million production line in Tarragona capable of 150 million incontinence units annually.

- November 2024: QIAGEN established a new Barcelona site dedicated to QIAstat-Dx operations, reinforcing Spanish diagnostic capabilities.

Spain Hospital Supplies Market Report Scope

As per the scope of the report, hospital supplies include every medical utility product that serves both the patient and medical professional with hospital infrastructure and enhances the network and transportation between hospitals. These include hospital equipment, patient aid, mobility equipment, and sterilization disposable hospital supplies. Spain Hospital Supplies Market is Segmented by Product (Patient Examination Devices, Operating Room Equipment, Mobility Aids and Transportation Equipment, Sterilization and Disinfectant Equipment, Disposable Hospital Supplies, Syringes and Needles, and Other Products). The report offers the value (in USD million) for the above segments.

By Product

| Patient Examination Devices |

| Operating-Room Equipment |

| Mobility Aids & Transport Equipment |

| Sterilisation & Disinfection Equipment |

| Disposable Hospital Supplies |

| Syringes & Needles |

| Other Products |

By End-User Facility

| Public Hospitals |

| Private Hospitals |

| Specialised Clinics |

| Diagnostic & Imaging Centres |

By Distribution Channel

| Direct Public Tenders |

| Group-Purchasing Organisations (GPOs) |

| Online B2B Platforms |

| Retail & Community Pharmacies |

| By Product | Patient Examination Devices |

| Operating-Room Equipment | |

| Mobility Aids & Transport Equipment | |

| Sterilisation & Disinfection Equipment | |

| Disposable Hospital Supplies | |

| Syringes & Needles | |

| Other Products | |

| By End-User Facility | Public Hospitals |

| Private Hospitals | |

| Specialised Clinics | |

| Diagnostic & Imaging Centres | |

| By Distribution Channel | Direct Public Tenders |

| Group-Purchasing Organisations (GPOs) | |

| Online B2B Platforms | |

| Retail & Community Pharmacies |

Key Questions Answered in the Report

What is the current value of Spain hospital supplies and how fast is it growing?

Spending reached USD 3.01 billion in 2026 and is projected to advance to USD 3.99 billion by 2031 at a 5.83% CAGR over 2026-2031.

Which product segment generates the most revenue in Spain hospital supplies?

Disposable hospital supplies lead with 45.12% share, driven by strict infection-control protocols in public and private facilities.

How large is the role of Spain's public hospitals in overall purchasing?

Public facilities account for 62.10% of national procurement, ensuring steady tender volumes through the tax-funded Sistema Nacional de Salud.

Why are online B2B platforms expanding so quickly in Spain hospital supplies?

Mandatory e-invoicing and centralized portals such as FACe simplify bidding and payment, supporting a 9.69% CAGR for digital channels through 2031.

What impact does the EU plastic tax have on Spain hospital supplies?

The EUR 0.45/kg levy increases packaging costs, but medical-device exemptions soften the blow for single-use items while spurring eco-design shifts.

Which regional investments are shaping future supply capacity?

Projects like Essity's EUR 24 million Tarragona line and QIAGEN's new Barcelona diagnostics site boost domestic output and shorten delivery times.

Page last updated on: