Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 67.47 Million |

| Market Size (2026) | USD 72.94 Million |

| Market Size (2031) | USD 107.78 Million |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Mammography Market Analysis by Mordor Intelligence

The Spain Mammography Market size is projected to be USD 67.47 million in 2025, USD 72.94 million in 2026, and reach USD 107.78 million by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

This growth is primarily attributed to the increasing incidence of breast cancer, efforts to restore pre-pandemic screening volumes, and a nationwide transition to tomosynthesis-capable equipment. A government-led initiative that includes funding for 61 new digital systems and emphasizes mandatory environmental standards is accelerating the digital transformation and establishing replacement cycles through bundled ten-year service contracts. In 2024, the launch of a unified Cancer Surveillance System highlighted participation gaps, particularly among foreign-born and rural women.[1]SEOM, “Cifras del Cáncer en España 2024,” seom.org This has driven demand for GDPR-compliant cloud PACS capable of integrating images across autonomous community boundaries. The competitive landscape is shifting, with a focus on low-dose detectors and AI-powered positioning systems that support hospital networks in meeting decarbonization objectives while reducing examination times. Additionally, mobile screening fleets are expanding, especially in coastal and rural areas, where outreach models are being tested to align with tourist surges and harvest seasons.

Key Report Takeaways

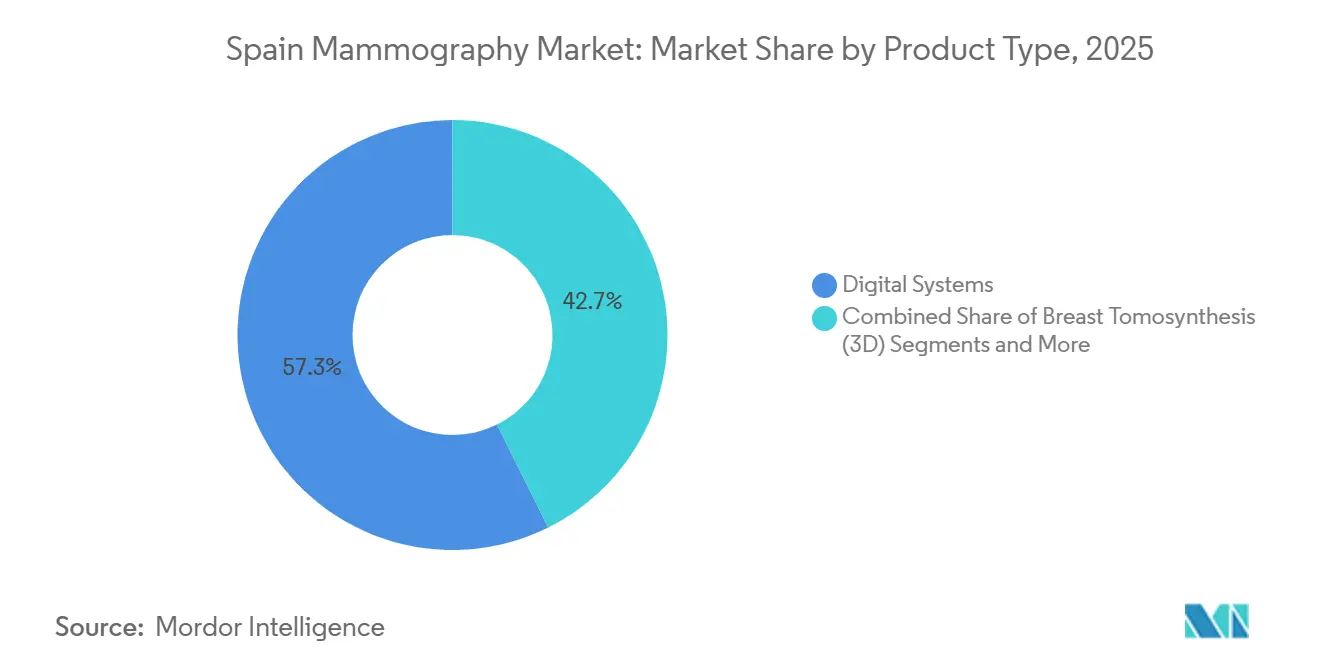

- By product type, digital systems led with a 57.34% share of the Spain mammography market size in 2025 and are tracking an 11.50% CAGR through 2031.

- By end user, hospitals captured 68.72% of the Spain mammography market share in 2025, while mobile screening units posted the fastest projected growth at a 9.70% CAGR to 2031.

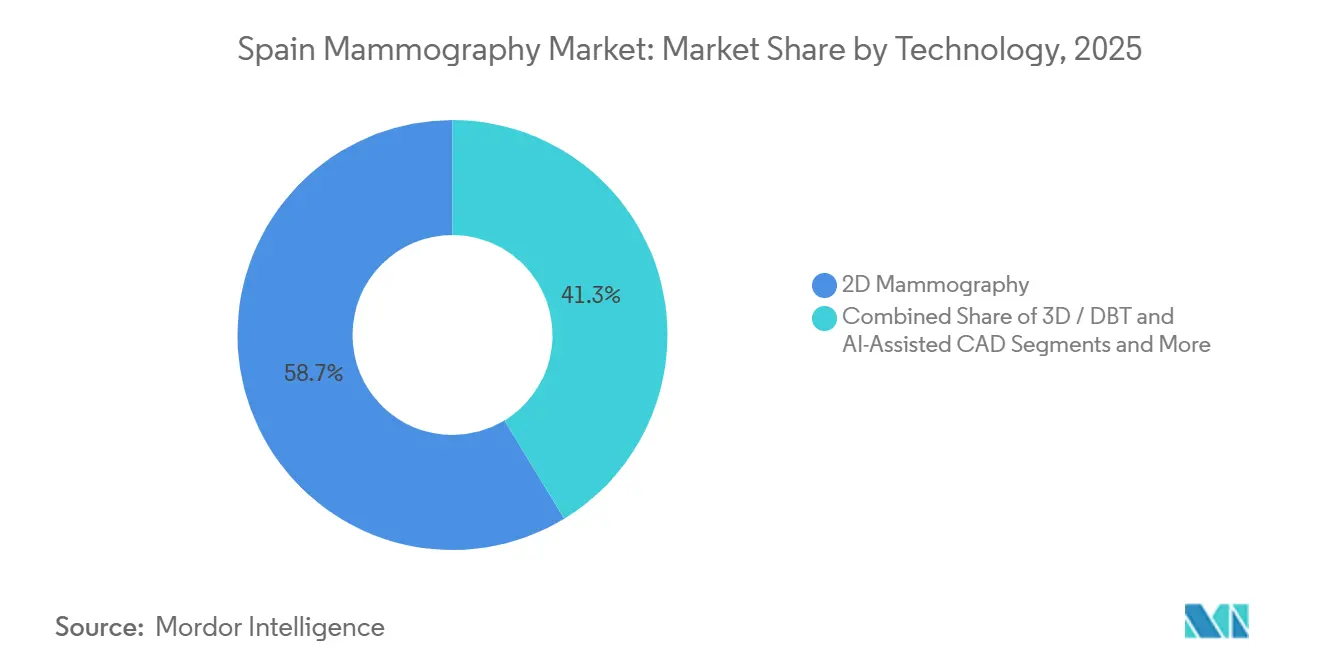

- By technology, 2-D mammography accounted for 58.70% of the installed base in 2025, and 3-D DBT is forecast to expand at a 10.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Mammography Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing breast-cancer incidence in women 40-69 | +1.8% | National, higher volumes in Madrid, Catalonia, Andalusia | Medium term (2-4 years) |

| Expansion of biennial national screening | +1.5% | National, early gains in Basque Country, Navarra, Galicia, Valencia, Castilla y León | Short term (≤ 2 years) |

| Regional tenders accelerating 3-D tomosynthesis roll-out | +2.2% | National, led by Catalonia, Andalusia, Madrid | Medium term (2-4 years) |

| Shift to personalized, risk-based screening | +0.9% | Catalonia, multi-regional MyPeBS sites | Long term (≥ 4 years) |

| GDPR-compliant cloud PACs for teleradiology | +1.1% | National, priority in Extremadura and Castilla-La Mancha | Medium term (2-4 years) |

| Hospital decarbonization goals | +0.7% | National, aligned with Ministry sustainability roadmap | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Breast-Cancer Incidence in Women 40-69

In 2024, Spain reported 36,395 new breast cancer diagnoses, making it the country's most prevalent malignancy. Catalonia experienced a 16% increase in cases over the past decade. The majority of diagnoses occur among women aged 50-69, aligning with the demographic targeted for biennial screening.[2]Spanish Association Against Cancer, “Breast Cancer Awareness Month Impact 2024,” contraelcancer.es Even slight increases in participation can drive system utilization rates beyond 85%. Advocacy efforts are pushing to expand screening age eligibility to 45-74, which could result in an additional 1.5 million screenings annually and require 20-25 more units to maintain wait times under 30 days. Awareness campaigns in October led to a 12% rise in self-referrals in 2024, further straining traditional analog platforms. These factors collectively highlight the growing demand for advanced digital systems.[3]Spanish Association Against Cancer, “Breast Cancer Awareness Month Impact 2024,” contraelcancer.es

Expansion of Biennial National Screening

All 17 autonomous communities in Spain invite women aged 50-69 to biennial screenings, but participation rates dropped from 83% in 2017 to 74% in 2020, primarily due to COVID-19-related disruptions. Five regions have extended invitations to women aged 45-49 and 70-74, providing valuable insights for an upcoming EU guideline revision. Real-time tracking by the national Cancer Surveillance System reveals disparities, with foreign-born women and rural residents participating at lower rates. Mobile units are being deployed to address these gaps. For instance, Galicia's mobile fleet increased coverage in towns with fewer than 5,000 residents from 68% to 79% within a year. Similarly, Andalusia's program screened 42,000 women in 2024, reflecting a 15% annual growth.

Regional Tenders Accelerating 3-D Tomosynthesis Roll-Out

Hospitals such as Valme in Seville invested EUR 200,000 (USD 218,000) in wide-angle tomosynthesis, achieving daily throughputs of 500 scans and sharply cutting recall rates. Osuna Hospital’s contrast-enhanced add-on now covers 25,000 women annually, delivering results in 20 minutes and an efficiency edge that shortens diagnostic pathways. Procurement frameworks are increasingly specifying requirements for dual-angle tomosynthesis, AI guidance, and low-dose detectors. In late 2024, Catalonia issued a tender for 18 units, emphasizing AI-driven compression features. Evidence from Córdoba’s Hospital Reina Sofía demonstrated a 27% reduction in recall rates and a 15% improvement in detection sensitivity with tomosynthesis, justifying a 30-40% price premium. Additionally, Siemens Healthineers secured a preventive-maintenance contract in 2024, reflecting a shift toward extended service agreements designed to minimize hospital downtimes.

Shift to Personalized, Risk-Based Screening Models

Catalonia’s study on risk-based screening intervals found a 67.4% acceptance rate and 97% satisfaction, challenging the traditional uniform approach. Spain's randomized trial on personalized screening models, involving over 53,000 women, focuses on factors such as polygenic risk and family history. Hospital del Mar’s AI model achieved high accuracy in two-year risk predictions, outperforming density-only methods. The adoption of these models depends on the availability of decision-support tools and reimbursement mechanisms to accommodate longer consultations.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cumulative-dose anxiety among younger cohorts | -0.5% | National, especially urban centers with high health literacy | Short term (≤ 2 years) |

| Reimbursement gaps for tomosynthesis outside public programs | -0.8% | National, acute where extended age bands are not funded | Medium term (2-4 years) |

| Radiologist shortage delaying AI validation | -1.1% | National, critical in Extremadura and Castilla-La Mancha | Medium term (2-4 years) |

| Litigation over interval cancers diverting budgets | -0.6% | National, higher frequency in private networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Radiologist Shortage Delaying AI Validation & Deployment

Prospective AI trials require extensive ground-truth labeling, but Spain's below-average radiologist density poses a significant challenge to this process. Kheiron's Mia algorithm demonstrated a 13% improvement in detection rates and a 25% reduction in interval cancers across three Catalan hospitals. However, broader implementation is contingent on the availability of local validation data. Additionally, the eHealth Network now requires BI-RADS-compliant metadata for cross-border data exchange, necessitating IT system upgrades in hospitals before large-scale AI pilot projects can proceed.

Reimbursement Gaps for Tomosynthesis Outside Public Programs

Public insurance currently covers only 2-D screenings, leaving women who need tomosynthesis outside organized programs to bear costs ranging from EUR 150 to 300 at private facilities. This financial barrier has limited tomosynthesis usage to less than 2% of total nationwide exams, despite an increasing installed base. While five regions have extended funding to include broader age groups, this perpetuates regional disparities in access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Platforms Capture Government Procurement

In 2025, Spain's digital mammography market was valued at USD 57.34%, with a projected CAGR of 11.50% through 2031. The AMAT-I fund initiatives are driving the adoption of low-dose, energy-efficient detectors, accelerating the shift from analog systems. Long-term service agreements, such as GE HealthCare's recent contract in Huesca, are increasing switching costs and strengthening the position of established players. While tomosynthesis platforms command a 30-40% price premium, procurement decisions are justified by sensitivity improvements, such as a 15% gain reported by leading hospitals. However, contrast-enhanced digital mammography adoption remains limited due to reimbursement challenges, restricting its use to private networks catering to self-pay patients.

Rising R&D efforts are focusing on detector materials that reduce the average glandular dose by up to 30%, aligning with sustainability goals in healthcare. Vendors are also integrating AI-triage software to streamline workflows by prioritizing high-suspicion cases, enabling radiologists to focus on complex analyses. The market increasingly favors cloud-ready platforms, driven by regional health IT projects requiring Vendor-Neutral Archives to manage tomosynthesis datasets without on-premise servers. With federal funding tied to energy efficiency and cybersecurity compliance, digital systems are expected to continue outpacing analog replacements.

By End User: Hospitals Dominate but Mobile Units Accelerate

Hospitals delivered 68.72% of total examinations in 2025, underscoring their dominance in procedure volumes. Tertiary centers in Madrid and Barcelona regularly exceed 50,000 scans per year and drive early adoption of AI-assisted tools. Mobile screening units, however, represent the fastest riser, with a 9.70% CAGR, aided by public health targets to reach rural and migrant populations. Studies show mobile teams can deliver over 2,000 exams annually and identify earlier-stage disease in cohorts historically absent from hospital programs. Each incremental mobile trailer places two digital detectors, cloud PACS, and vehicle maintenance contracts into the Spain mammography market size.

Diagnostic centers and specialty clinics preserve stable demand by focusing on high-risk follow-ups, biopsies, and second opinions. Yet lack of tomosynthesis reimbursement in these venues can slow equipment refresh cycles, placing renewed emphasis on value-based AI add-ons that shorten appointment slots and increase daily throughput, offsetting reimbursement gaps.

By Technology: 2-D Largest but 3-D/DBT Fastest

In 2025, the 2-D segment accounted for 58.70% of the installed-base value, reflecting the impact of early statewide digital roll-outs. Although the 3-D DBT segment in Spain's mammography market is smaller, it is projected to grow at a 10.40% CAGR through 2031, driven by tenders prioritizing multi-slice capture. Catalonia’s late-2024 procurement required AI-assisted positioning and contrast-enhanced capabilities, prompting vendors to integrate advanced features without high additional costs.

AI-assisted CAD adoption remains limited due to delays in prospective validation. For instance, Kheiron’s Mia has reduced interval cancers by 25% but is operational in only a few hospitals. Broader adoption depends on standardized BI-RADS coding across diverse PACS, a challenge cloud-native vendors are addressing with middleware solutions for tagging legacy DICOMs. With ongoing radiologist shortages, 3-D platforms featuring embedded triage capabilities are expected to capture incremental market share in Spain's mammography market.

Geography Analysis

Catalonia, Madrid, and Andalusia collectively account for approximately 55% of national healthcare spending, driven by their combined population of 24 million and concentrated tertiary-care facilities. Catalonia's 2024 procurement of 18 dual-angle tomosynthesis systems highlights the region's focus on investing in advanced technologies to enhance workflow efficiency. Regions such as the Basque Country, Navarra, and Valencia have expanded age bands in their screening programs, positioning themselves as pilot zones for EU screening guidelines. Nationwide participation ranges from 65% to 88%, with foreign-born women showing lower engagement, though initiatives like Galicia's mobile fleet have significantly reduced this gap.

Murcia's 15-year Value Partnership with Siemens Healthineers demonstrates the effectiveness of outcome-based pricing, eliminating a two-year backlog by 2025 and ensuring sustained vendor collaboration. Coastal areas, including Costa del Sol, are optimizing resources by piloting seasonal mobile circuits aligned with tourist surges, increasing examination capacity without additional infrastructure. The national Cancer Surveillance System, launched in 2024, now provides real-time dashboards across all 17 regions, enabling efficient reallocation of mobile fleets and budget adjustments.

Inland regions like Castilla-La Mancha are leveraging cloud PACS to transmit images to urban reading hubs, reducing turnaround times by 20%. As GDPR-compliant networks advance and radiologist shortages persist, cross-community teleradiology is expected to minimize geographic disparities, fostering more consistent procurement patterns across Spain's mammography market.

Competitive Landscape

Leading multinational OEMs, including Hologic, Siemens Healthineers, GE HealthCare, Fujifilm, Canon Medical, and Philips, sustain price leadership by offering bundled ten-year service contracts, uptime guarantees, and proprietary AI solutions. Siemens Healthineers exemplifies outcome-based contracting through long-term partnerships that secure equipment pipelines and maintenance revenue. Hologic leverages its extensive Iberian installed base to drive cross-selling opportunities for low-dose upgrades and bone-health adjuncts.

Smaller European specialists like Planmed and IMS Giotto differentiate themselves with modular upgrades, fast 12-week delivery, and flexible leasing options tailored to cost-sensitive buyers. Metaltronica focuses on retrofit kits that digitize analog detectors, aligning with sustainability standards. Opportunities are emerging in GDPR-compliant cloud PACS that integrate hospital and mobile fleets, with Sectra and Agfa leading in vendor-neutral archiving solutions.

Hospitals, responding to litigation risks and new EU AI governance rules, increasingly prefer vendors offering integrated AI triage under unified warranties. Multimodality bundling, combining mammography with ultrasound and MRI, is gaining traction as it broadens diagnostic pathways and mitigates medico-legal risks. Consequently, competition in the Spanish mammography market is shifting from hardware specifications to comprehensive service ecosystems.

Spain Mammography Industry Leaders

Koninklijke Philips NV

Fujifilm Holdings Corporation

Siemens Healthineers AG

Carestream Health Inc.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hologic, Inc. displayed its breast and skeletal health portfolio at EUSOBI Congress in Valencia.

- September 2025: The Valencian Community chose Lunit Insight MMG and Lunit Insight DBT as the AI backbone for its public screening program.

- March 2024: Castilla-La Mancha approved EUR 23 million (USD 27.1 million) to provide 575,000 mammograms over five years, detecting around 800 suspected tumors annually.

- February 2024: Povisa Hospital launched contrast-enhanced mammography in Galicia, introducing a unit with advanced diagnostic capabilities.

Spain Mammography Market Report Scope

As per the scope of the report, mammography is a standard diagnostic and screening technique used to evaluate breast tissues for the presence of a malignant tumor. The process involves the use of low-frequency X-rays to locate tumors in the breast.

The Spain mammography market is segmented by product type, end user, and technology. By product type, the market is segmented into digital systems, breast tomosynthesis (3-D), analog systems, and contrast-enhanced digital mammography. By end user, the market is segmented into hospitals, diagnostic centers, specialty clinics, mobile screening units, and breast imaging centers. By technology, the market is segmented into 2-D mammography, 3-D/DBT, AI-assisted CAD, and contrast-enhanced digital mammography. The report offers market size and forecasts in value (USD) for the above segments.

By Product Type

| Digital Systems |

| Breast Tomosynthesis (3-D) |

| Analog Systems |

| Contrast-Enhanced Digital Mammography |

By End User

| Hospitals |

| Diagnostic Centers |

| Specialty Clinics |

| Mobile Screening Units |

| Breast Imaging Centres |

By Technology

| 2-D Mammography |

| 3-D / DBT |

| AI-Assisted CAD |

| Contrast-Enhanced Digital Mammography |

| By Product Type | Digital Systems |

| Breast Tomosynthesis (3-D) | |

| Analog Systems | |

| Contrast-Enhanced Digital Mammography | |

| By End User | Hospitals |

| Diagnostic Centers | |

| Specialty Clinics | |

| Mobile Screening Units | |

| Breast Imaging Centres | |

| By Technology | 2-D Mammography |

| 3-D / DBT | |

| AI-Assisted CAD | |

| Contrast-Enhanced Digital Mammography |

Key Questions Answered in the Report

What is the current size of Spain Mammography Market

Spain Mammography Market is USD 72.94 million in 2026.

Which Spanish regions invest most heavily in new mammography units?

Catalonia, Madrid, and Andalusia account for roughly 55% of national equipment spending because they host the largest tertiary hospitals and receive the highest regional health budgets.

Why are mobile mammography units gaining popularity?

Mobile fleets boosted participation in hard-to-reach municipalities from 68% to 79% within one year and are expanding at a 9.70% CAGR to offset radiologist shortages and geographic disparities.

What is the main barrier to nationwide adoption of tomosynthesis?

Lack of a public reimbursement code forces many women to pay EUR 150 to 300 out-of-pocket, which suppresses volume outside organized screening programs.

How are AI tools being integrated into breast-cancer screening?

Early deployments such as Kheirons Mia lifted detection 13% but broader roll-out awaits local validation studies that are slowed by Spains below-average radiologist density.

What sustainability criteria influence purchasing decisions?

Plan AMAT-I ties public funding to low-dose detectors and energy-efficient cooling systems that align with Ministry decarbonization targets set for 2027.

Page last updated on: