Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

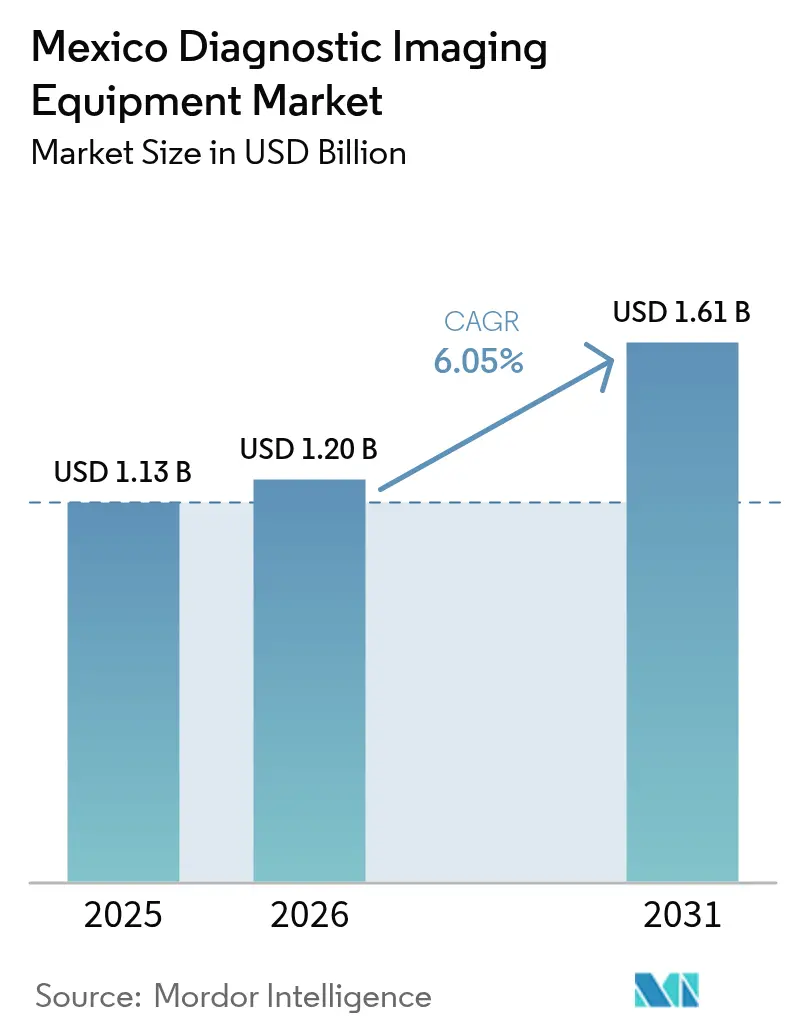

| Base Year Market Size (2025) | USD 1.13 Billion |

| Market Size (2026) | USD 1.2 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

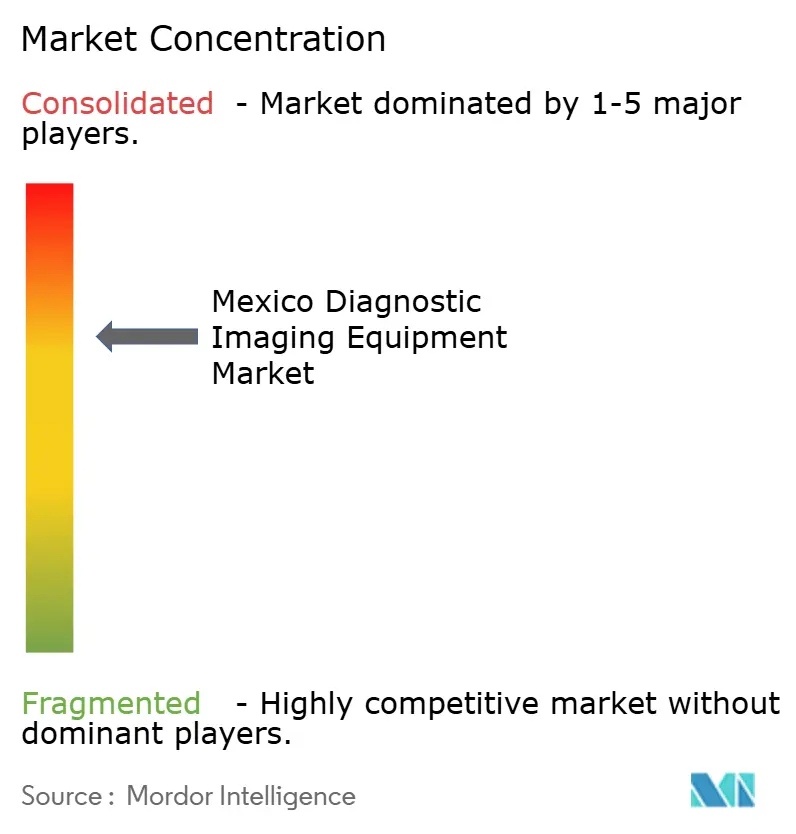

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Mexico Diagnostic Imaging Equipment Market size was valued at USD 1.13 billion in 2025 and estimated to grow from USD 1.2 billion in 2026 to reach USD 1.61 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). Strong public-sector modernization, universal-coverage ambitions under the IMSS-Bienestar program, and private investment aimed at medical tourism underpin sustained capital outlays for new imaging systems. Chronic-disease prevalence keeps demand elevated for cardiac, neurological, and oncological imaging modalities. Technological upgrades such as AI-assisted workflows, autonomous image acquisition, and edge-device analytics are diffusing quickly from large urban hospitals to smaller facilities, helped by lower-cost mobile units and cloud-based teleradiology. Budget constraints remain, yet IMSS-Bienestar’s 30.2% funding jump and nine new public hospitals slated for 2025 provide multi-year procurement visibility for vendors.[1]Source: Instituto Mexicano del Seguro Social, “Serán inaugurados nueve Hospitales y seis Unidades de Medicina Familiar del IMSS en 2025,” imss.gob.mx

Key Report Takeaways

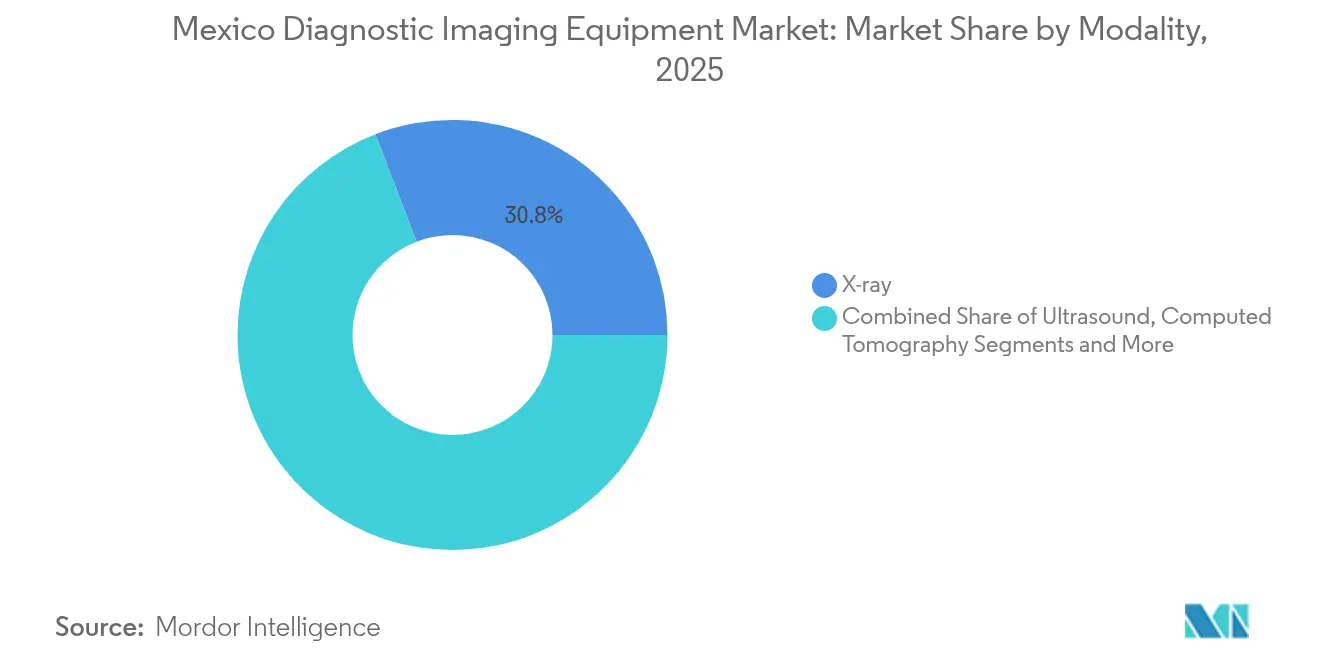

- By modality, X-ray systems captured 30.84% of the Mexico Diagnostic Imaging Equipment market share in 2025; MRI is projected to expand at an 8.03% CAGR through 2031.

- By portability, fixed installations held 80.65% share of the Mexico Diagnostic Imaging Equipment market size in 2025, while mobile and hand-held units are advancing at a 7.55% CAGR to 2031.

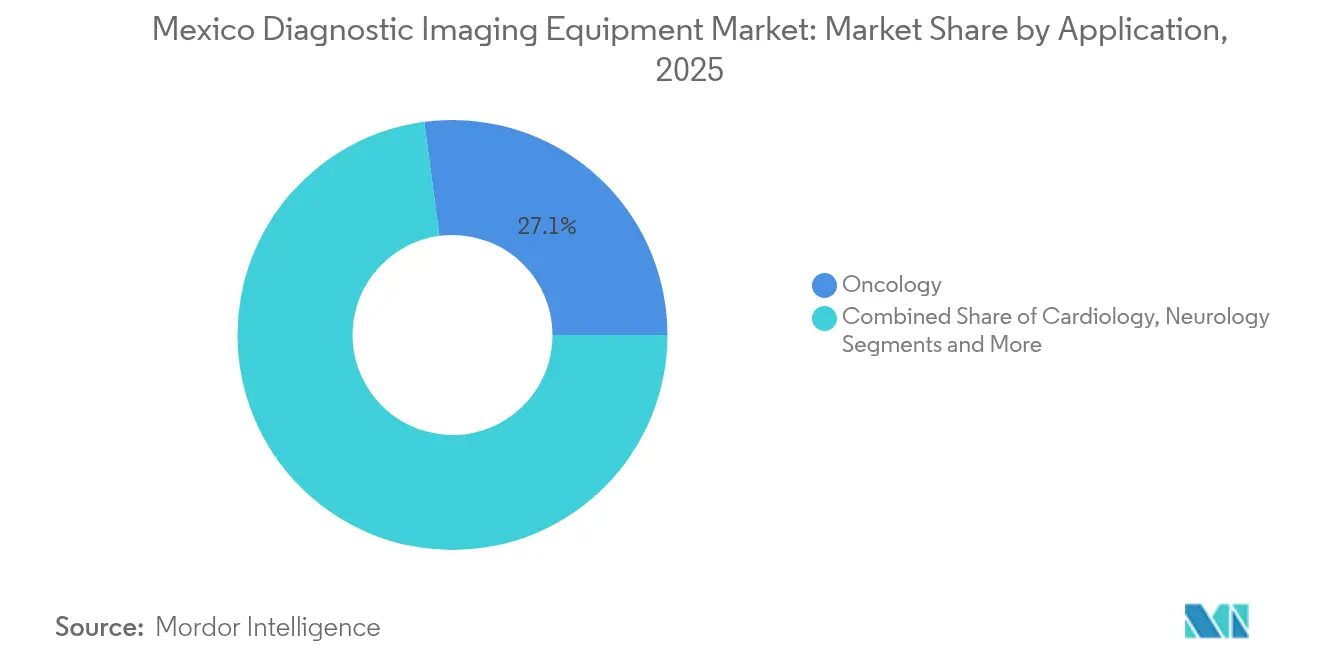

- By application, oncology retained 27.10% of the Mexico Diagnostic Imaging Equipment market size in 2025; neurology is set to grow the fastest at a 7.68% CAGR.

- By end user, hospitals accounted for 55.02% share of the Mexico Diagnostic Imaging Equipment market size in 2025, whereas diagnostic imaging centers are forecast to rise at a 6.70% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic Diseases and Increasing Geriatric Population | +1.2% | National, with concentration in urban centers | Long term (≥ 4 years) |

| Technological Advancements in Imaging Equipment | +0.9% | National, with early adoption in private sector | Medium term (2-4 years) |

| Surge in Medical Tourism | +0.7% | Border states and major cities | Short term (≤ 2 years) |

| Growing Healthcare Infrastructure and Investments | +0.8% | National, prioritizing underserved regions | Long term (≥ 4 years) |

| AI-enabled Teleradiology Improving ROI for Rural Mobile Imaging | +0.6% | Rural and remote areas | Medium term (2-4 years) |

| Increasing Patient Awareness and Preventive Health Practices | +0.4% | Urban areas with higher education levels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases and Increasing Geriatric Population

Cardiovascular disease mortality illustrates a steady rise that directly escalates demand for high-resolution cardiac CT and MRI. Disabilities affect 16.5% of residents, and 31% of those cases require advanced imaging follow-up, intensifying pressure on diagnostic workflows.[2]Source: Emerson Baptista et al., “Disability and Its Impact on Life Expectancy,” BMC Public Health, bmcpublichealth.biomedcentral.com The MexOMICS Consortium has begun integrating MRI findings into national registries, indicating institutional momentum toward imaging-heavy, population-health studies. Breast-cancer incidence at 39.9 per 100,000 women accelerates mammography adoption and encourages digital upgrades for early detection. As life expectancy rises, demand for neurology scans will likely outpace overall population growth, especially where dementia and stroke rates are climbing.

Technological Advancements in Imaging Equipment

GE Healthcare’s NVIDIA-powered autonomous X-ray and ultrasound prototypes show how AI addresses Mexico’s limited radiologist workforce, which averages fewer than one specialist per imaging unit. Edge computing allows ultrasound and portable CT devices to analyze images locally, supporting diagnostics in areas with weak internet connectivity. Academic literature notes a post-2019 surge in machine-learning applications, with neural networks and support-vector machines now widespread in Mexican imaging projects. Samsung Medison’s USD 51 million purchase of Sonio underscores rising vendor interest in AI algorithms optimized for obstetric and abdominal scans. Together, these innovations shorten exam times, enhance diagnostic consistency, and elevate throughput without adding personnel.

Surge in Medical Tourism

Procedure costs that can be 60% lower than in the United States keep cross-border patient flows vibrant, requiring private hospitals to install premium MRI and CT systems that satisfy Joint Commission standards. CHRISTUS Health’s USD 84 million hospital in Cabo San Lucas targets 23,000 U.S. expatriates and deploys AI-enabled scanners calibrated to U.S. imaging protocols. General Atlantic’s USD 160 million infusion into Hospitales MAC directs funds toward advanced diagnostic infrastructure across new urban locations. These investments raise the competitive standard and ripple into equipment replacement cycles at domestic facilities seeking to retain local patients.

Growing Healthcare Infrastructure and Investments

The IMSS will bring nine hospitals and six Family Medicine Units online in 2025, each configured with CT, MRI, ultrasound, and digital X-ray suites. Chiapas alone has received MX$677.5 million (USD 35 million) to upgrade imaging capability, reflecting a push to close regional service gaps. A forthcoming 260-bed IMSS hospital in Nuevo León, budgeted at MX$3.2 billion (USD 165 million), is linked to the automotive cluster and will feature hybrid operating rooms with interventional imaging. ISSSTE’s 2024-2025 modernization plan also prioritizes imaging equipment upgrades across its network. The continuous build-out secures multi-year demand for vendors and establishes replacement markets for 2030-plus.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Costs Associated with the Device and Procedure | -0.8% | National, more pronounced in rural areas | Long term (≥ 4 years) |

| Shortage of Skilled Professionals | -0.6% | National, acute in rural regions | Medium term (2-4 years) |

| Stringent Regulations Delaying the Approval Processes | -0.4% | National regulatory framework | Short term (≤ 2 years) |

| Limited Insurance Coverage for Imaging | -0.5% | National, affecting uninsured population | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs Associated with the Device and Procedure

COFEPRIS registration fees of USD 5,000–10,000, plus mandatory testing, lengthen break-even horizons for vendors entering the Mexico Diagnostic Imaging Equipment market.[3]Source: Pure Global, “COFEPRIS Mexico Medical Device Regulations,” pureglobal.com Public spending pressure intensified after the 2025 federal health budget fell 11% to MX$918.4 billion (USD 47.38 billion). Per-capita outlays for IMSS-Bienestar beneficiaries also slid 24.9%, limiting funding for advanced scanners at safety-net hospitals. MRI installations remain capital-heavy, often exceeding USD 1.5 million before shielding and lifecycle service contracts, a hurdle for regional clinics. These economics foster a two-tier structure where high-end private providers upgrade swiftly while public facilities stagger replacements.

Shortage of Skilled Professionals

Fewer than one radiologist per imaging unit hampers scan throughput and delays reporting at many facilities. Technician scarcity compounds the bottleneck, as vocational programs graduate fewer specialists than growth requires. GE Healthcare’s autonomous prototype aims to mitigate workforce gaps by automating positioning and protocol selection. Although the administration plans to hire 20,000 healthcare workers, imaging talent needs advanced training that extends beyond generalized recruitment. Rural retention remains problematic given lower compensation and professional isolation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: MRI Growth Outpaces X-ray Stability

X-ray retained 30.84% of the Mexico Diagnostic Imaging Equipment market share in 2025 on the strength of low cost and broad clinical utility. The modality’s replacement cycle now centers on digital upgrades that raise throughput and reduce radiation. MRI is climbing fastest at an 8.03% CAGR as neurology and oncology protocols demand greater tissue contrast and functional imaging. Computed-tomography demand benefits from emergency-department expansions, while ultrasound adoption accelerates via mobile obstetrics and cardiology clinics. As vendors embed AI into image reconstruction, MRI throughput rises without extra magnet rooms, narrowing cost-per-study gaps versus CT.

Rising cancer burdens steer facilities toward PET/SPECT, but nuclear-medicine penetration remains low given cyclotron scarcity and isotope logistics. Mammography units face mandated digital transitions that favor tomosynthesis. Fluoroscopy and C-arms support interventional suites where trauma and orthopedic procedures expand with industrial-accident volumes. Technology alliances, such as Samsung Medison’s Sonio acquisition, illustrate a shift to ecosystem solutions that pair hardware with AI to cut exam times.

By Portability: Mobile Platforms Carving Share from Fixed Rooms

Fixed installations still hold 80.65% of the Mexico Diagnostic Imaging Equipment market size, primarily at tertiary hospitals where infrastructure can handle high-power draws and radiation shielding. They remain the anchor for complex studies like cardiac MRI or PET/CT. Mobile and hand-held units, however, post a 7.55% CAGR due to rural programs and disaster-response readiness. Government tenders now bundle portable ultrasound with primary-care vans to support the door-to-door senior-care initiative. Battery-powered X-ray devices improve injury triage at construction sites and athletic events.

The Mexico Diagnostic Imaging Equipment market size captured by mobile platforms is forecast to grow in the coming years, reflecting distributed-care priorities. Edge-device analytics let technologists confirm diagnostic sufficiency on-site, avoiding recalls that burden patients. DMS Group’s Onyx mobile DR system pairs with cloud PACS, cutting integration timelines for regional hospitals. As domestic manufacturing grows, portable units will arrive with lower import tariffs, further eroding fixed-room dominance.

By Application: Oncology Dominant, Neurology Momentum Builds

Oncology consumed 27.10% of the Mexico Diagnostic Imaging Equipment market size in 2025, powered by breast-cancer screening expansions and precision-medicine protocols. Facilities depend on multiparametric MRI, PET/CT, and contrast-enhanced mammography for staging and therapy monitoring. GE’s Thera4Care collaboration in Europe hints at molecular-imaging roadmaps that Mexican centers may soon replicate. Neurology trails but posts a 7.68% CAGR as dementia prevalence grows and stroke care timelines shrink.

Cardiology remains a major volume driver with CT angiography and echocardiography adoption sharpened by rising ischemic heart-disease deaths. Orthopedics consumes digital-portable X-ray capacity, especially in the manufacturing corridors of Baja California and Nuevo León. Obstetrics benefits from AI-enhanced fetal-anatomy ultrasound modules. Screening programs for colorectal, thyroid, and prostate diseases form the “other applications” bucket, which grows as preventive medicine gains policy traction.

By End User: Hospitals Lead, Imaging Centers Accelerate

Hospitals concentrated 55.02% of the Mexico Diagnostic Imaging Equipment market share in 2025, driven by emergency, inpatient, and surgical imaging needs. New IMSS and ISSSTE sites ensure the hospital segment retains purchasing scale for high-end modalities. Imaging centers, however, expand at a 6.70% CAGR as private operators exploit fast-turnaround service models that capture self-pay and medical-tourism traffic. These centers often deploy 3-Tesla MRI and dual-energy CT early, leveraging shorter procurement cycles.

Specialty clinics focus on cardiology and cancer care, installing dedicated MR-linacs or cath-lab hybrid systems that integrate imaging with interventions. Mobile service providers fill rural gaps, contracting with local authorities for scheduled visits. The Mexico Diagnostic Imaging Equipment market size attributed to imaging centers will likely grow at a substantial rate, underpinned by venture funding and vendor financing models. Keirón México’s workflow-automation software illustrates how technology optimizes scheduling, boosting scanner uptime.

Geography Analysis

Northern border states host a dense cluster of private hospitals catering to U.S. medical tourists, where MRI and PET/CT penetration exceeds national averages thanks to international-accreditation requirements. Mexico City’s academic centers house subspecialty modalities, including intraoperative MRI and hybrid ORs, anchoring research and residency training.

Southern states, particularly Chiapas and Oaxaca, rely on federal expansion funds for fixed digital X-ray and ultrasound. IMSS-Bienestar’s MX$677.5 million allocation to Chiapas earmarked equipment for five hospitals, closing diagnostic gaps across mountainous terrain. Central industrial hubs like Nuevo León attract employer-funded health facilities; the planned Tesla-cluster hospital features cardiovascular cath-labs and 64-slice CT for injury screening. The Pacific tourist corridor (Los Cabos, Puerto Vallarta) deploys premium imaging suites to tap expatriate demand, mirroring CHRISTUS Health’s USD 84 million project.

Mobile fleets expand in arid northern and jungle southern zones where road networks dictate outreach frequency. AI-enabled teleradiology minimizes the expertise gap between metropolitan and rural settings, maintaining consistent diagnostic quality. Overall, the Mexico Diagnostic Imaging Equipment market displays a dual structure: technology-rich urban anchors and flexible mobile solutions in geographically challenging districts.

Regulatory Landscape

Diagnostic imaging equipment in Mexico is regulated as a medical device under COFEPRIS, which administers pre-market sanitary registration requirements. A key shift in market access occurred with the formalization of the Abbreviated Regulatory Pathway in July 2025 (published in the Diario Oficial de la Federacion), enabling recognition of approvals from Reference Regulatory Authorities and WHO prequalification, with an intended 30-business-day review timeline for eligible devices.

Compliance is also shaped by updated national standards, including NOM-241-SSA1-2025 (Good Manufacturing Practices) and NOM-137-SSA1-2025 (labeling). In June 2026, COFEPRIS published a Requirements Guide for the Sanitary Registration of Medical Devices, unifying criteria for equivalence agreements and the abbreviated pathway, while reinforcing the practical need for foreign manufacturers to work through a Mexico Registration Holder (MRH) as the local legal applicant and registration owner.

Value Chain Analysis

Mexico remains structurally import-dependent for advanced diagnostic imaging hardware (CT, MRI, PET/CT), while local value capture is concentrated downstream in distribution, systems integration, software, installation, and lifecycle service. The typical chain runs from global OEM manufacturing and component sourcing through importation and customs handling, a Mexico Registration Holder (for COFEPRIS filings), authorized distributors, site planning (shielding and facility readiness), installation and commissioning, and recurring service contracts, parts, and upgrades. COFEPRIS sanitary registration and applicable NOMs add documentation, labeling, and quality-system steps that affect lead times and influence partner selection.

Domestic and in-country participants are more visible in X-ray equipment, software, and service layers, which are central to utilization and uptime. Compañia Mexicana de Radiologia (CMR) supports local X-ray manufacturing and PACS-related offerings, while firms such as Grupo PTM provide teleradiology and digital image storage solutions that complement multi-vendor imaging fleets. Common bottlenecks include logistics for sensitive high-value systems, Spanish-language technical documentation, and the need for certified local maintenance capability, which makes nationwide service coverage and spare-parts availability a key differentiator beyond the initial equipment sale.

Competitive Landscape

Global multinationals dominate volume yet face intensifying rivalry from technology firms and regional OEMs. GE Healthcare, Siemens Healthineers, and Philips maintain broad modality portfolios and nationwide service networks. GE’s AWS generative-AI pact aims to embed clinical-decision support into imaging workflows, differentiating its installed base. Siemens directs USD 3.36 billion of its wider USD 27.38 billion MedTech spend to diagnostics, advancing spectral CT and photon-counting detectors. Philips leverages cloud-PACS and remote-fleet monitoring to deepen aftermarket ties.

Supply-chain moves reshape manufacturing footprint; Siemens’ relocation of Varian production from Mexico to the United States may open whitespace for local contract manufacturers. Emerging brands such as United Imaging expand with high-end PET/CT installations at pediatric institutes, while DMS Group posts double-digit growth through mobile-system exports. AI-focused acquisitions—Hologic’s USD 350 million purchase of Gynesonics and its Google Cloud alliance—signal a pivot toward software-heavy ecosystems. Vendor-financed equipment leases and outcome-based contracts gain traction as public buyers look to preserve cash.

Regulatory complexity favors incumbents with in-country compliance teams. New entrants partner with Mexican Registration Holders to reduce COFEPRIS timelines yet must absorb labeling-standard updates and post-market surveillance costs. Competitive focus therefore shifts to integrated service offerings—AI-enabled protocols, remote uptime monitoring, and clinician-training portals—that lock in customers beyond hardware sales.

Mexico Diagnostic Imaging Equipment Industry Leaders

GE Healthcare

Siemens Healthineers

Koninklijke Philips N.V.

Canon Medical Systems

Fujifilm Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public-sector modernization and centralized procurement create whitespace for vendors and service partners that can deliver compliant, install-ready imaging capacity quickly. In January 2026, the Ministry of Health announced a 2026 plan to acquire 816 high-technology medical devices (MX$11.25 billion), explicitly including imaging-heavy categories such as 500 mammography units, 238 CT scanners, 38 MRI systems, and 5 PET-CT units. This procurement scale supports opportunities not only for modality suppliers, but also for shielding and site-prep contractors, PACS/RIS integration, and multi-year maintenance coverage across dispersed facilities.

A parallel opportunity sits in premium imaging deployments and workflow upgrades anchored in named projects and hospital networks. In January 2026, the Ministry of Health also commenced construction of a High-Specialty Diagnostic Center in Tlalpan (Mexico City) with planned capacity including 5 MRI units and 3 PET-CT scanners, signaling demand for high-acuity oncology and advanced diagnostics infrastructure. On the delivery and adoption side, OEMs and providers can expand through AI-enabled protocol standardization and remote reporting models already used by large networks, while meeting updated labeling and GMP expectations under NOM-137-SSA1-2025 and NOM-241-SSA1-2025 and navigating COFEPRIS pathways, including the abbreviated route for eligible imported systems.

Recent Industry Developments

- June 2026: IMSS reported the integration of 17 high-end MRI systems to strengthen second- and third-level care capacity, including units from Philips, Siemens Healthineers, and GE HealthCare. The rollout supports higher public-sector scan throughput and creates recurring demand for applications, coils, uptime services, and training across the installed base.

- April 2026: Siemens Healthineers launched its Mammomat B.brilliant 3D mammography system in Mexico following regulatory clearance. The launch raises the competitive benchmark in breast imaging and aligns with expanding mammography procurement and digital-upgrade cycles in both public tenders and private screening networks.

- July 2024: United Imaging delivered its uMI 550 PET/CT to the Instituto Nacional de Pediatria to support pediatric oncology imaging. The installation broadened high-end nuclear imaging capability in a reference pediatric center and reinforced competitive momentum for PET/CT placements in Mexico beyond the largest adult oncology hubs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from selling diagnostic imaging equipment in Mexico, counted at the point of equipment purchase and installation across healthcare settings where imaging is performed.

Scope exclusions: We exclude imaging services, consumables, and extended maintenance-only revenue that is not bundled with an equipment sale.

Segmentation Overview

- By Modality

- X-ray

- Ultrasound

- Computed Tomography

- MRI

- Nuclear Imaging (PET/SPECT)

- Fluoroscopy & C-arms

- Mammography

- By Portability

- Fixed Systems

- Mobile & Hand-held Systems

- By Application

- Oncology

- Cardiology

- Neurology

- Orthopedics

- Obstetrics & Gynecology

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Clinics

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map the healthcare and imaging environment in Mexico, so the market model is anchored in observable demand signals and policy context. We relied on public sources such as national health and statistics releases, regulator and customs trade data, and clinical imaging literature, which together help explain how imaging capacity and utilization are changing.

To translate that context into sizing inputs, we also reviewed sources such as hospital and public procurement portals, association publications, peer reviewed journals, and reputed press coverage around new installations and technology refresh cycles. Company filings and investor presentations were referenced when they described Mexico exposure or modality mix, and selective paid subscriptions for company financial intelligence, news and financials, and patent databases helped fill gaps on product launches and pricing direction. These examples are not exhaustive, and many other sources were also consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to test what we saw in desk research, especially around procurement timing, replacement cycles, and how modality demand is shifting across public and private settings. Interviews and surveys covered a mix of equipment suppliers and channel partners, along with hospital imaging teams, diagnostic center operators, and biomedical engineering and procurement roles across Mexico, so assumptions could be corrected where practice differs from published sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | |

| Mid tier: 43% | Functional/Unit leaders: 43% | |

| Smaller Players: 19% | Managers: 44% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up logic, with the top-down view guided by Mexico healthcare spending patterns and imaging capacity and procurement indicators that help reconstruct annual equipment demand. Once that picture was formed, it was cross-checked using selective bottom-up approximations such as sampled average selling prices by modality multiplied by expected unit placements, along with channel checks on tender activity and replacement-led purchases.

Key model inputs included modality mix across major equipment types, replacement cycle assumptions (by installed base age and uptime expectations), public versus private purchase behavior, and price progression based on configuration shifts and currency timing. Where data was uneven, gaps were handled by using conservative ranges from interviews and then narrowing them using observed trade and procurement signals, so the final totals remain explainable. Forecasts were developed using scenario analysis tied to variables like healthcare investment appetite, diagnostic load trends for chronic conditions, and expected pace of technology upgrades, and then aligned to what primary respondents see in their order pipelines and budgeting cycles.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, where the market total had to stay consistent with procurement intensity, trade patterns, and the implied unit economics by modality. When a result looked out of line, the assumptions were rechecked, outliers were investigated, and follow up calls were triggered with the most relevant respondent profiles before the numbers were finalized.

A multi step internal review was then completed, including a fresh pass on key inputs and year-over-year movements to ensure the story matches the math. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery check is performed so clients receive the most current view available at the time of publication.

Mordor Intelligence's Mexico Diagnostic Imaging Equipment Market Market Estimate Compared With Other Published Estimates

Published numbers for Mexico diagnostic imaging can look far apart, even when they appear to describe the same topic, because the market can be counted in different ways and for different revenue streams. The biggest drivers tend to be what gets included as revenue, which year is treated as the anchor, and whether prices are modeled from equipment configurations or from blended spending ratios.

In this market, the spread is often explained by whether the estimate counts only equipment sales at the time of purchase, or whether it also folds in imaging services and other related revenue, which can be sizable in Mexico. Differences also come from how modalities are grouped, how replacement cycles are translated into annual unit demand, and how currency conversion timing is handled when imports influence pricing. Here, equipment-only revenues are counted and then checked against modality level ASP and placement logic, a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.20 B (2026) | |

| Industry Research Publisher A | USD 0.44 B (2025) | This figure appears to reflect a broader diagnostic imaging market that includes service revenue and is anchored to 2025, which reduces the value when compared to an equipment-only view and also shifts the base year used for comparison. |

| Global Consultancy B | USD 0.70 B (2024) | This estimate is based on a different base year and is described as medical imaging revenue that can blend equipment with related services, which typically lowers comparability to a pure equipment procurement model and can change implied ASP and volume assumptions. |

Taken together, the table shows that scope and anchoring year explain most of the gap, and the remaining difference is usually pricing and replacement-cycle math. By keeping inclusions explicit and tying totals back to modality demand signals that can be revisited each year, the approach gives decision makers a number they can trace and reuse in planning.

Key Questions Answered in the Report

What is the 2026 value of the Mexico Diagnostic Imaging Equipment market?

The market is worth USD 1.2 billion in 2026.

How fast is the MRI segment growing in Mexico?

MRI revenues are projected to rise at an 8.03% CAGR through 2031, the fastest among major modalities.

Which portability category is gaining share most quickly?

Mobile and hand-held systems are expanding at a 7.55% CAGR as rural programs scale.

Why is medical tourism relevant to imaging vendors?

Border and resort hospitals install premium MRI and CT scanners to serve U.S. patients paying 60% less than domestic prices.

What major policy supports future equipment demand?

IMSS-Bienestar’s expansion, including nine new hospitals in 2025, ensures continuous procurement of advanced imaging modalities.

Page last updated on: