Spain Nuclear Imaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

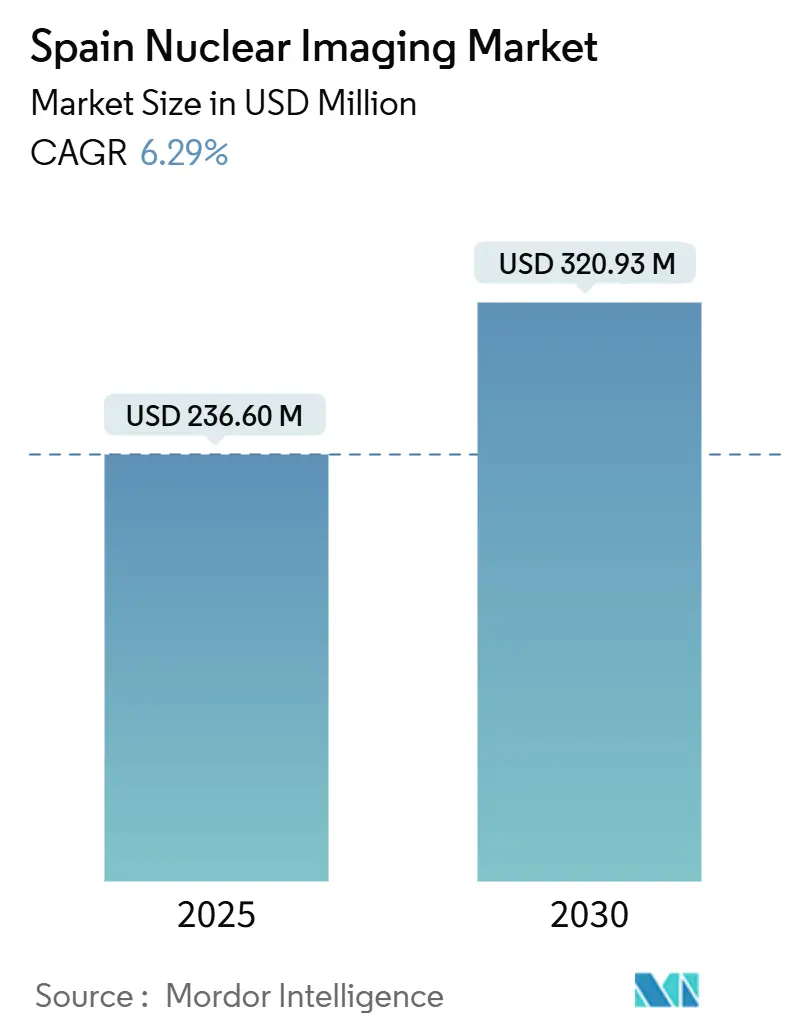

| Market Size (2025) | USD 236.60 Million |

| Market Size (2030) | USD 320.93 Million |

| Growth Rate (2025 - 2030) | 6.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Nuclear Imaging Market Analysis by Mordor Intelligence

The Spain Nuclear Imaging Market size is estimated at USD 236.60 million in 2025, and is expected to reach USD 320.93 million by 2030, at a CAGR of 6.29% during the forecast period (2025-2030).

Expansion is underpinned by soaring demand for personalized oncology care, rapid adoption of PSMA-PET imaging, and public-sector investment in PET-cyclotron hubs that strengthen domestic radioisotope supply resilience. Infrastructure modernization, marked by widespread silicon-photomultiplier detector upgrades and AI-enabled reporting workflows, is further narrowing scan-to-treatment intervals and elevating diagnostic throughput. At the same time, pronounced regional disparities in cancer mortality, volatile technetium-99m logistics, and workforce shortages present formidable operational hurdles that providers must navigate.

Key Report Takeaways

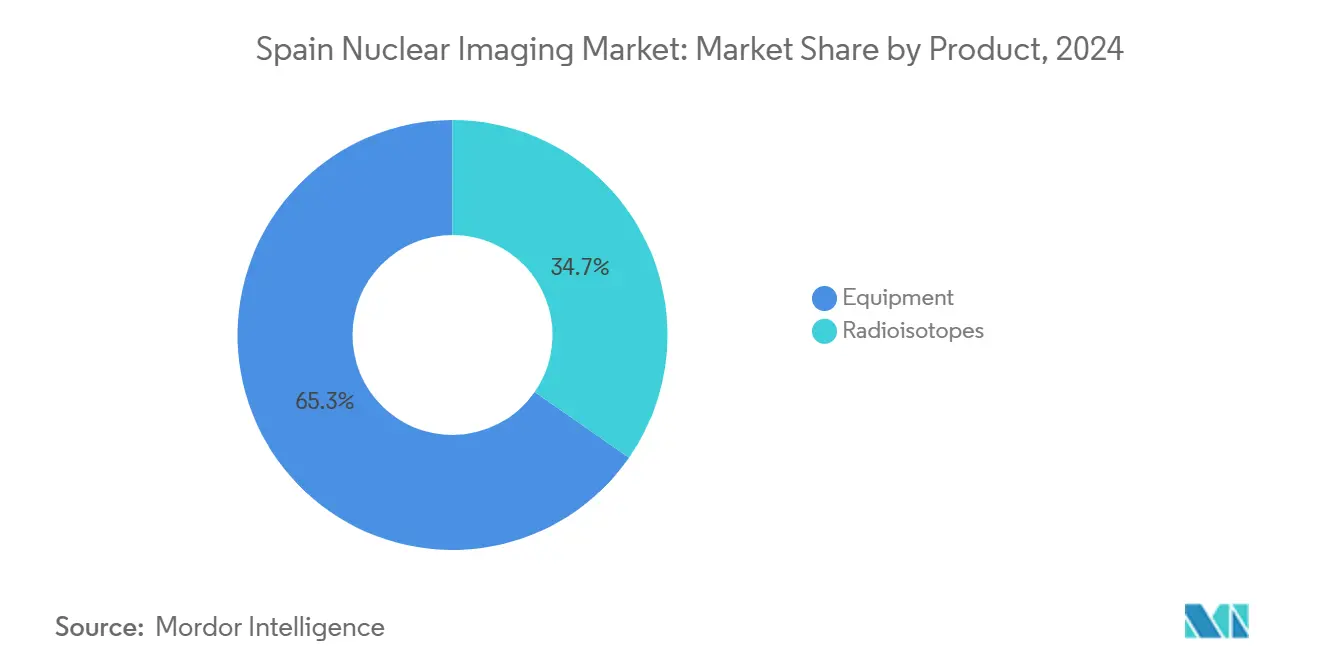

- By product, equipment led with 65.34% of Spain nuclear medicine market share in 2024, whereas radioisotopes are projected to expand at a 6.84% CAGR through 2030.

- By application, oncology accounted for 69.89% of Spain nuclear medicine market size in 2024 while neurology is advancing at a 7.19% CAGR to 2030.

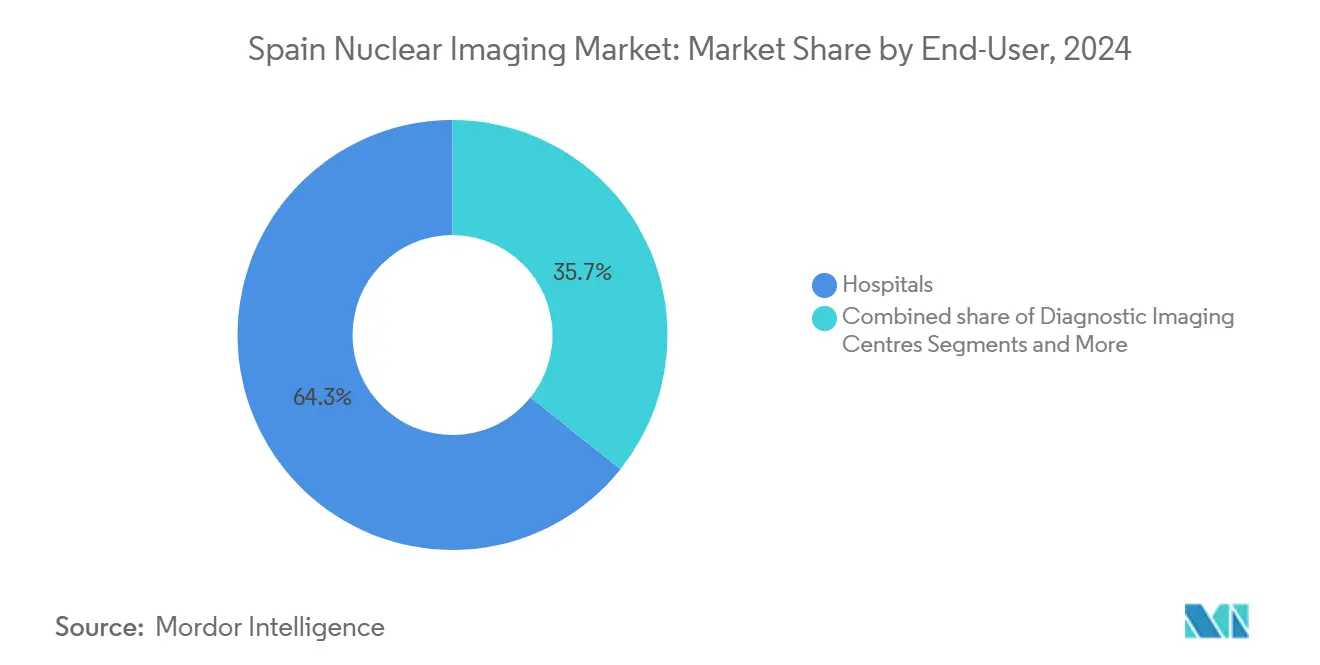

- By end user, hospitals retained 64.26% share of the Spain nuclear medicine market in 2024, and diagnostic imaging centers record the highest projected CAGR at 7.39% through 2030.

Spain Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PSMA-PET reimbursement acceleration | +1.2% | National, with early adoption in Madrid, Barcelona | Medium term (2-4 years) |

| Rising oncology & cardiology incidence in ageing population | +1.8% | National, higher impact in northern autonomous communities | Long term (≥ 4 years) |

| Expansion of public PET-cyclotron hubs (Proyecto RICORS) | +0.9% | Regional focus on underserved areas | Medium term (2-4 years) |

| Digitisation & SiPM-based detector upgrades | +0.7% | Major hospital networks in Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| AI-enabled total-body PET pilots (Madrid, Barcelona) | +0.5% | Metropolitan areas with research hospitals | Medium term (2-4 years) |

| Installation of brain-dedicated PET for Alzheimer's trials | +0.4% | Academic medical centers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PSMA-PET Reimbursement Acceleration

Reimbursement reforms are catalyzing PSMA-PET diffusion, illustrated by Hospital del Mar’s 53% lesion detection rate in biochemical recurrence cases at PSA 0.2-2.0 ng/mL that altered therapeutic decisions in 84.4% of patients. Spanish payers now recognize the modality’s downstream cost savings from avoided futile therapies, prompting broader inclusion across autonomous-community formularies. Uptake aligns with European Association of Urology guidance and is reinforced by Spanish Agency of Medicines and Medical Devices quality oversight. Momentum is strongest in Madrid and Catalonia, but Andalusia and Valencia have begun cross-border referral programs to expand patient access. Collectively, reimbursement clarity trims diagnostic pathways and lifts demand for gallium-68 and fluorine-18 PSMA tracers.

Rising Oncology & Cardiology Incidence in Ageing Population

Spain’s longevity gains elevate cancer and heart-disease caseloads, with oncology procedures already commanding 69.89% of Spain nuclear medicine market share in 2024.[1]European Commission, “Beating Cancer Inequalities,” europa.eu Northern regions such as Cantabria and Asturias exhibit the highest age-standardized cancer rates, driving accelerator installation grants under Proyecto RICORS. Cardiology services equally benefit from hybrid PET/CT perfusion protocols, co-developed by CNIC Madrid and Philips, that shorten acquisition time and enhance image fidelity. Screening participation lags EU averages, especially among rural seniors, positioning nuclear medicine as a critical bridge for early pathology detection. The demographic shift necessitates geriatric-oriented imaging protocols and further strains an already limited specialist workforce.

Expansion of Public PET-Cyclotron Hubs (Proyecto RICORS)

Proyecto RICORS is mitigating radioisotope deserts by funding cyclotron clusters in Extremadura, Castilla-La Mancha, and Galicia, reducing dependence on overseas molybdenum sources that faltered during the 2024 High Flux Reactor outage. Each hub integrates centralized synthesis labs, cold kits, and regional delivery fleets, slashing radiotracer transit times and waste. Coordinated procurement lowers unit isotope costs and enhances negotiating leverage with power utilities, a vital consideration as nuclear-derived baseload wanes ahead of Spain’s 2030 plant phase-out. Successful roll-outs hinge on inter-community licensing harmonization and technical staff mobility incentives.

Digitization & SiPM-Based Detector Upgrades

Hospitals in Madrid and Valencia are fast-tracking silicon-photomultiplier retrofits that boost timing resolution, enabling reduced dose protocols ideal for pediatric and frail elderly cohorts. Digital detectors markedly raise throughput, permitting two extra PET/CT slots daily per scanner and lightening technologist workload. Quibim’s AI-assisted reconstruction software further compresses acquisition times while sustaining diagnostic accuracy, evidenced by 15% faster reporting in multi-institutional trials. Capital investments are bundled into long-term vendor value partnerships that spread costs and guarantee uptime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Molybdenum-99 / Tc-99m supply volatility | -1.1% | National, affecting all SPECT procedures | Short term (≤ 2 years) |

| Nuclear-medicine workforce shortages | -0.8% | Major metropolitan areas and rural regions | Medium term (2-4 years) |

| Autonomous-Community reimbursement disparities | -0.6% | Regional variations across 17 communities | Long term (≥ 4 years) |

| High electricity costs for cyclotron uptime | -0.4% | Facilities with on-site cyclotron operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Molybdenum-99 / Tc-99m Supply Volatility

The October 2024 High Flux Reactor restart delay curtailed Mo-99 shipments by 50%, forcing Spanish SPECT suites to defer bone and cardiac scans for nearly two weeks.[2]SNMMI, “Mo-99/Tc-99m Shortage Alert,” snmmi.org Hospital pharmacies extended generator reuse cycles and substituted thallium-201 where possible, but patient backlogs persisted. The shock accelerated procurement of 18 MeV cyclotrons in Andalusia and Galicia for in-house technetium production via molybdenum-100 targets. Nonetheless, fuel-cost inflation threatens competitiveness against reactor-based isotopes until scale economies emerge.

Nuclear-Medicine Workforce Shortages

Spain fields only 1.2 nuclear medicine physicians per 100 000 inhabitants, well below the EU average, and radiopharmacist certification mandates three years of supervised practice. Staffing gaps prolong scan scheduling to seven weeks in some centers, dampening Spain nuclear medicine market growth. AI-driven reading aids have cut lymphoma PET/CT interpretation time by 15% without compromising sensitivity, partially alleviating pressure. Government scholarships and salary uplifts to EUR 23 000 (USD 25 100) target recruitment, yet attrition to higher-paying EU markets persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Equipment Dominance Drives Infrastructure Modernization

The equipment segment captured 65.34% of Spain nuclear medicine market share in 2024, reflecting sustained scanner replacement cycles and fresh installations under regional modernization plans. Widespread adoption of silicon-photomultiplier PET/CT systems during 2025-2026 has shortened average scan times from 20 minutes to 10 minutes, enabling two additional daily slots per device. Vendor value-partnership models bundle hardware, service, and staff training into predictable annual fees, mitigating upfront capital barriers for public hospitals. Diagnostic imaging centers leverage refurbished SPECT/CT units to expand outpatient services in suburban locales, bringing advanced imaging closer to population clusters previously reliant on tertiary centers.

Radioisotopes underpin the fastest-growing component with a 6.84% CAGR, fueled by theranostic Lu-177 demand and emergent Cu-61 tracers whose generator-based production sidesteps reactor bottlenecks. Domestic cyclotron investments under Proyecto RICORS buttress supply certainty, while Curium’s 2025 acquisition of Monrol boosts Lu-177 output across 46 European sites, easing logistics into Spain. The Spain nuclear medicine market size for radioisotopes is projected to reach USD 118 million by 2030, representing 36.7% of overall revenues. Ongoing R&D into terbium-161 and actinium-225 compounds positions Spain as an early adopter of alpha-therapy pipelines that promise superior tumor-absorbed-dose profiles.

By Application: Oncology Leadership Amid Neurology Acceleration

Oncology retained 69.89% of Spain nuclear medicine market size in 2024 as hospitals broadened PSMA-PET protocols and Lu-177-based therapies, with 12 de Octubre Hospital pioneering dual-modality PET/MR trials for neuroendocrine tumors. The national cancer strategy earmarks EUR 784 million for imaging upgrades through 2028, ensuring continuous demand for fluorine-18 FDG and gallium-68 peptides. Clinical pathways now integrate total-body PET, which captures metastatic burden in 30 seconds and allows ultra-low-dose follow-up at four-week intervals without cumulative radiation concerns.

Neurology, although smaller, is rising at a 7.19% CAGR, spurred by brain-dedicated PET deployments supporting amyloid-imaging protocols that underpin recent monoclonal antibody approvals. The Spain nuclear medicine market share for neurology could rise from 6.3% in 2024 to 8.5% by 2030 as provincial memory clinics adopt Centiloid-standardized quantification. Additionally, dopamine transporter imaging for movement disorders has grown 9% annually, driven by earlier Parkinson’s diagnosis mandates in primary care guidelines. Together, these factors diversify revenue streams beyond oncology and stabilize isotopic demand profiles year-round.

By End User: Hospitals Lead While Imaging Centers Accelerate

Hospitals accounted for 64.26% of Spain nuclear medicine market in 2024, leveraging multidisciplinary teams to deliver complex theranostic regimens and spearhead clinical trials. Teaching centers in Madrid and Barcelona collectively run more than 50 active radiopharmaceutical studies, drawing both domestic and EU grants. Nonetheless, diagnostic imaging centers are charting a 7.39% CAGR as reforms encourage outpatient pathways to relieve inpatient bottlenecks. Centers like Echevarne Diagnostics in Catalonia have installed compact PET/CT suites that process 25 patients daily, driven by employer-paid check-ups and self-pay oncology staging.

Academic and research institutes, while representing a modest revenue slice, inject innovation by validating AI algorithms and novel tracers. Valencia’s Quibim collaborates with La Fe Hospital to pilot federated learning models that secure patient data locally while generating multicenter AI models. This ecosystem approach feeds a virtuous cycle where research findings swiftly migrate into routine clinical workflows, accelerating diffusion of best practices across Spain nuclear medicine industry stakeholders.

Geography Analysis

Madrid and Catalonia together generated nearly half of 2025 revenues as dense hospital networks, including Gregorio Marañón and Vall d’Hebron, house total-body PET pilots and theranostic wards. Valencia ranks third, aided by Quibim’s AI ecosystem and La Fe’s cyclotron hub that slashed fluorine-18 delivery times from four hours to 90 minutes.

Southern Andalusia and Extremadura face sparser scanner density—0.8 PET units per million residents versus the national average of 1.4—yet they enjoy earmarked EU cohesion funds for equipment upgrades. Proyecto RICORS will add two cyclotrons in Málaga and Badajoz by 2027, narrowing supply inequities. In northern Galicia and Asturias, aging populations propel cardiology nuclear imaging; rubidium-82 PET myocardial perfusion volumes climbed 11% in 2024 following public insurance inclusion. Basque Country leverages CIC-biomaGUNE’s research infrastructure to explore copper-61 peptide potentials, positioning the region as a theranostic incubator.

Cross-community variance in cancer mortality—spanning 37%—creates asynchronous demand surges that complicate national procurement planning. Energy-price heterogeneity further skews cyclotron economics; Catalonia’s access to hydropower moderates tariffs, whereas Castilla-La Mancha’s reliance on gas-fired plants inflates isotope production costs. These dynamics foster a patchwork deployment pattern that equipment and isotope vendors must navigate via tiered service agreements and regional stock buffers.

Competitive Landscape

The Spain nuclear medicine market exhibits moderate concentration, with the top five players collectively controlling an estimated half of revenue. Curium’s March 2025 purchase of Monrol vaulted it to Europe’s foremost Lu-177 supplier, reinforcing vertical integration from target irradiation to patient dose delivery. GE HealthCare, Siemens Healthineers, and Philips secure scanner footprints through decade-long managed-service deals that embed staff training and AI software modules, building customer lock-in.

GE HealthCare’s €25.3 million Thera4Care consortium exemplifies cooperative R&D, aligning isotope producers, cyclotron vendors, and Gregorio Marañón Hospital to standardize theranostic workflows. Siemens’ value partnership with Murcia’s Ministry of Health cut PET/CT backlog by 35% within 12 months, enhancing corporate visibility among regional policymakers. Valencia-based Quibim, a digital native, differentiates via imaging-biomarker discovery platforms used by 18 pharmaceutical sponsors, positioning itself as a data-driven disruptor.

White-space entrants are targeting underserved autonomous communities by deploying mobile PET/SPECT vans that bridge equipment gaps while sidestepping costly brick-and-mortar sites. Yet regulatory compliance with Royal Legislative Decree 1/2015 and stringent AEMPS oversight create entry barriers that historically deterred small-scale foreign players. As AI integration and isotope diversification accelerate, competitive advantage will hinge on platform interoperability, sustainable energy strategies, and clinical-trial partnerships.

Spain Nuclear Imaging Industry Leaders

Canon Inc. (Canon Medical Systems Corporation)

Fujifilm Holdings Corporation

Siemens Healthineers AG

Koninklijke Philips N.V

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Curium Pharma completed the acquisition of Monrol, expanding Lu-177 production capacity and PET footprint across Europe, including Spain

- February 2025: Philips extended its cloud-based enterprise imaging services to Spain, delivering AI-enabled workflows that mitigate staffing shortages

Spain Nuclear Imaging Market Report Scope

According to the report's scope, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are typically painless medical tests that aid physicians in diagnosing and evaluating various medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance that is used in the treatment of cancer, and cardiac and neurological disorders. The Spanish Nuclear Imaging Market is segmented into Equipment and Radioisotopes by product. The radioisotopes are further subsegemnted into SPECT Radioisotopes and PET Radioisotopes. By application, market is segmented into Cardiology, Neurology, Thyroid, Oncology, and other applications. By end user, market is segmnted into Hospitals, Diagnostic Imaging Centre and academic and research institutes. The report offers the value (in USD) for the above segments.

| Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) |

| Thallium-201 (Tl-201) | ||

| Gallium-67 (Ga-67) | ||

| Iodine-123 (I-123) | ||

| Other SPECT Isotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (Rb-82) | ||

| Other PET Isotopes | ||

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) | |

| Thallium-201 (Tl-201) | |||

| Gallium-67 (Ga-67) | |||

| Iodine-123 (I-123) | |||

| Other SPECT Isotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (Rb-82) | |||

| Other PET Isotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What CAGR is expected for Spain's nuclear medicine segment between 2025 and 2030?

The market is projected to grow at 6.29% CAGR, rising from USD 236.60 million in 2025 to USD 320.93 million by 2030.

Which modality currently holds the largest share of nuclear medicine procedures in Spain?

Oncology applications dominate with 69.89% share due to widespread PSMA-PET and Lu-177 therapy adoption.

How is Spain mitigating radioisotope supply disruptions?

The Proyecto RICORS program funds regional cyclotron hubs to lessen reliance on imported Mo-99 and expand local fluorine-18 and copper-61 production.

What technological trends are shaping Spanish nuclear medicine services?

Key advances include silicon-photomultiplier detector upgrades, AI-enabled reporting platforms, and pilot deployments of total-body PET systems.

Page last updated on: