Spain Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

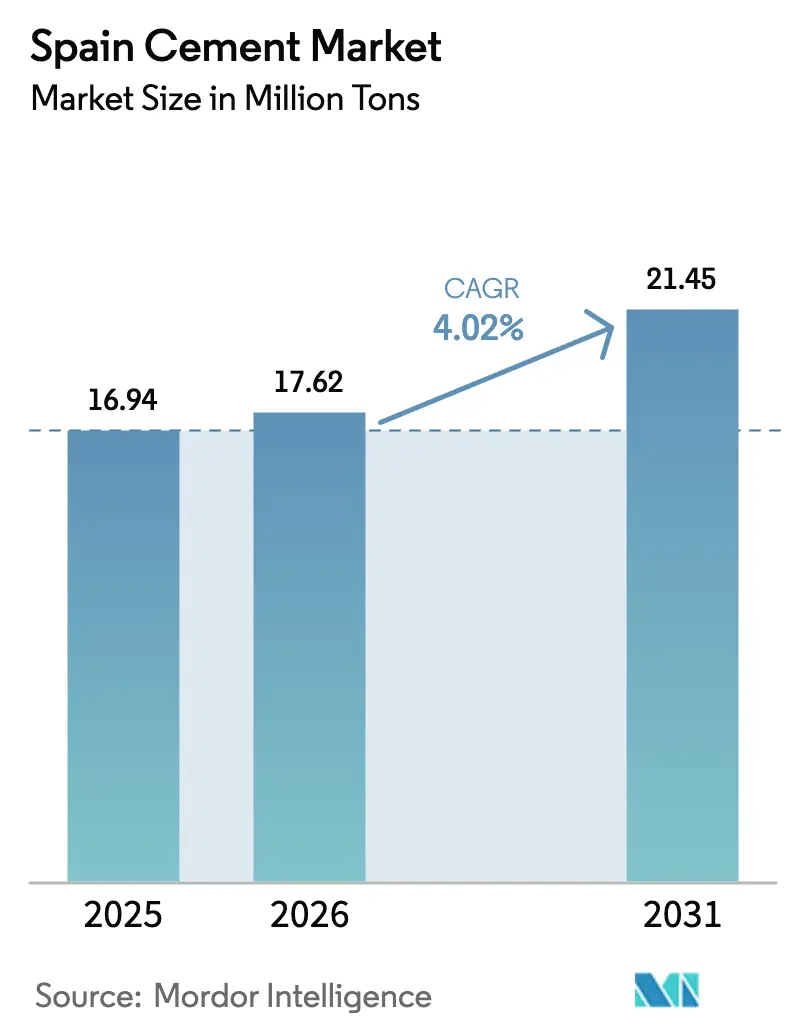

| Base Year Market Size (2025) | 16.94 Million tons |

| Market Volume (2026) | 17.62 Million tons |

| Market Volume (2031) | 21.45 Million tons |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

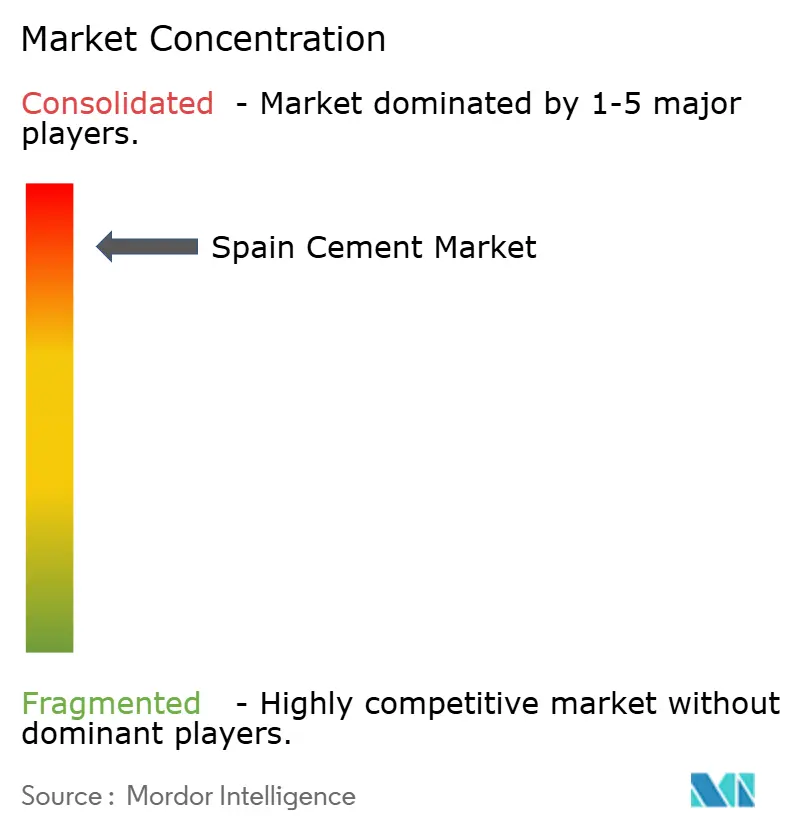

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Cement Market Analysis by Mordor Intelligence

Spain Cement Market size in 2026 is estimated at 17.62 million tons, growing from 2025 value of 16.94 million tons with 2031 projections showing 21.45 million tons, growing at 4.02% CAGR over 2026-2031. Robust public-sector outlays under the EUR 163 billion National Recovery and Resilience Plan, coupled with pent-up residential demand and ongoing industrial decarbonization, underpin this expansion. Construction permits, housing transactions, and infrastructure corridors spanning high-speed rail, port upgrades, and grid modernization are all translating directly into higher cement offtake. EU taxonomy rules are accelerating the tilt toward low-clinker blended cements even as traditional Portland grades remain essential for structural work. Producers are responding through fuel-switch programs, AI-driven kiln optimization and deeper regional logistics integration, enabling the Spain cement market to grow despite the drag from elevated EU-ETS compliance costs.

Key Report Takeaways

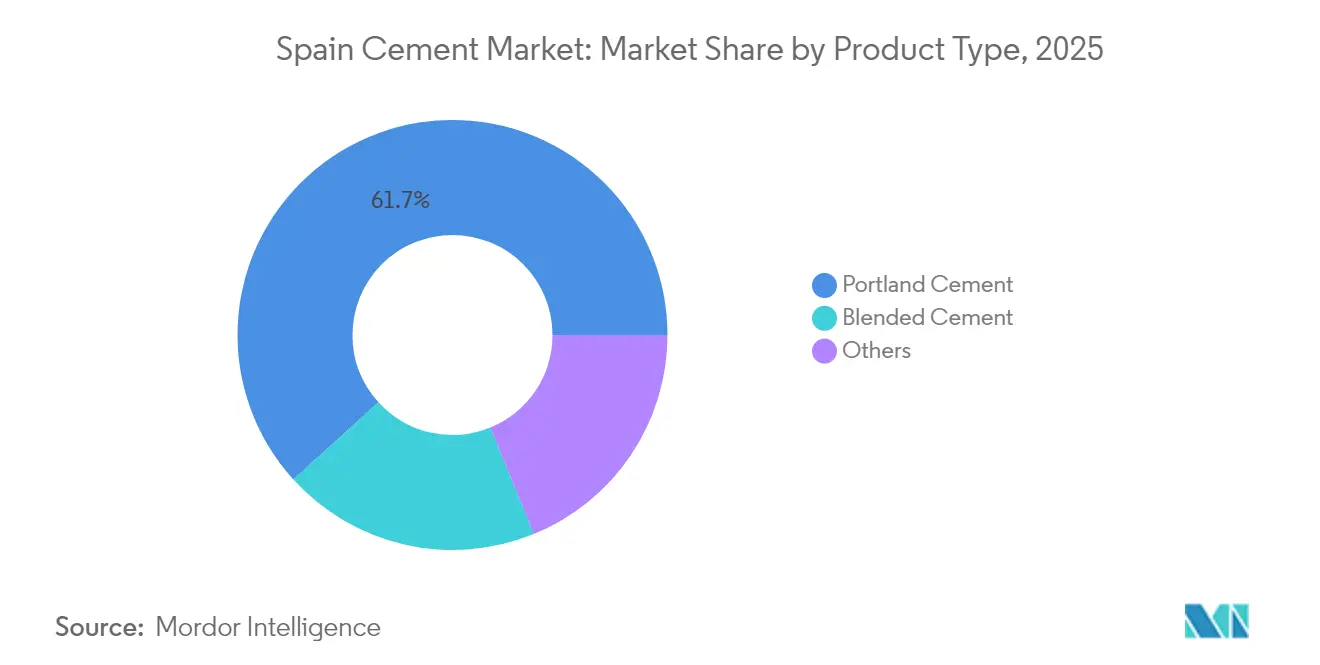

- By product type, Portland Cement led with 61.74% of the Spain cement market share in 2025. Blended Cement is projected to post the fastest growth at 6.05% CAGR through 2031.

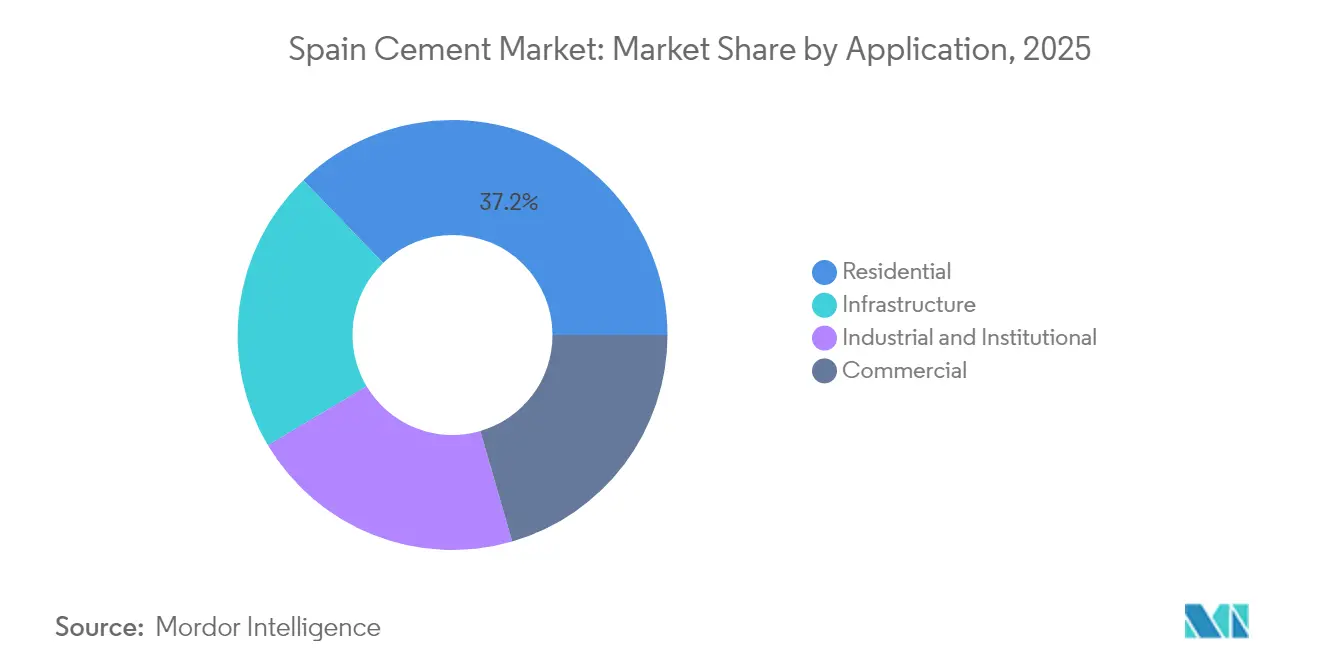

- By application, residential construction commanded 37.21% of the Spain cement market size in 2025, while infrastructure is set to outpace all segments at 5.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential & commercial construction activities | +1.20% | National, concentrated in Madrid, Barcelona, Valencia metropolitan areas | Medium term (2-4 years) |

| Increasing infrastructure investment (transport, energy) | +1.50% | National, with priority corridors in Andalusia, Catalonia, Basque Country | Long term (≥ 4 years) |

| Shift toward low-clinker blended cements (EU taxonomy) | +0.80% | EU-wide, early adoption in Northern Spain industrial regions | Medium term (2-4 years) |

| AI-driven predictive maintenance in Spanish kilns | +0.30% | National, focused on major production hubs in Andalusia, Catalonia | Short term (≤ 2 years) |

| Growth of offshore wind & green-hydrogen concrete demand | +0.40% | Coastal regions, Canary Islands, Galicia, Valencia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential & Commercial Construction Activities

Housing permits are set to move from 125,000 to 135,000 units in 2025, supporting a stable baseline demand of roughly 15-20 tons of cement per dwelling. Migration inflows, tourism-driven mixed-use projects, and logistics hubs along the Mediterranean coast amplify commercial floor-space starts. Madrid and Barcelona collectively represent a significant share of new builds, yet secondary cities such as Valencia and Bilbao are expanding plot approvals faster on a percentage basis. Tight urban land supply and a lingering housing deficit from the 2008-2014 downturn sustain volume resilience even when mortgage costs fluctuate. While builder margins are pressured by labor shortages and material inflation, project pipelines are being preserved through phased releases and build-to-rent models that lock in forward cement commitments. The Spain cement market benefits directly from these commitments as housing and retail shells consume large blocks of ordinary Portland grades for foundations and vertical elements.

Increasing Infrastructure Investment (Transport, Energy)

Spain has secured EUR 241 million in Connecting Europe Facility grants for rail electrification, port expansion, and trans-European highway upgrades[1]Spanish Government, “Spain obtains 241 million euros in European funds,” lamoncloa.gob.es . Flagship examples include the Zaragoza-Teruel-Sagunto corridor and the 700 m Ebro River high-speed rail viaduct, each requiring marine-grade, sulfate-resistant mixes. Grid reinforcement to host 11 GW of green-hydrogen capacity by 2030 also pulls demand for high-performance concretes able to withstand hydrogen embrittlement. EV charging corridors, coastal resiliency walls, and data-center shells deepen the structural pipeline, positioning infrastructure as the dominant growth vector within the Spain cement market over the next decade.

Shift Toward Low-Clinker Blended Cements (EU Taxonomy)

EU taxonomy thresholds have triggered a 6.12% blended-cement CAGR as producers pivot to CEM II/CEM IV mixes incorporating fly ash, slag, and calcined clay. CEMEX’s Vertua range now accounts for 56% of its Spanish volume, reflecting a 45% average CO₂ reduction per ton. Access to suitable clay deposits in Andalusia and Catalonia, plus steel-slag streams in the Basque Country, lowers input costs versus imported clinker, granting integrated players a strategic edge. Public tenders increasingly embed carbon caps, crowding out pure-Portland bids and accelerating portfolio realignment across the Spain cement market.

AI-Driven Predictive Maintenance in Spanish Kilns

CEMEX’s partnership with Basque firm Optimitive deploys machine-learning models that trim kiln energy by 10% and cut unplanned stoppages. Microsoft’s Copilot platform is being rolled out across dispatch and customer-service modules to hasten quotation cycles and dispatch accuracy. Early adopters report a 2-3 percentage-point EBITDA lift from tighter process control, supporting continued investment even under tight EU-ETS headroom. AI integration thus reinforces operational resilience and cost competitiveness, sustaining positive volume momentum within the Spain cement market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-emission regulations & EU-ETS cost escalation | -0.90% | EU-wide, acute impact on energy-intensive Spanish plants | Short term (≤ 2 years) |

| Volatile fuel & electricity prices | -0.60% | National, severe impact on Andalusia, Catalonia production hubs | Medium term (2-4 years) |

| Scarcity of alternative fuels & raw materials | -0.30% | Regional, concentrated in inland production centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carbon-Emission Regulations & EU-ETS Cost Escalation

Carbon allowances consumed 13.4% of total production cost in 2024, forcing cash-strapped operators to defer capex or risk margin squeeze. Free-allocation cuts under Phase 4 and the looming Carbon Border Adjustment Mechanism compound compliance complexity, especially for export-oriented plants shipping clinker to North Africa. While the EU’s Industrial Decarbonisation Accelerator promises grants, rollout lags current cash burn, prompting smaller players to consider asset sales or toll-grinding deals. These headwinds temper the headline CAGR yet do not derail overall growth in the Spain cement market due to offsetting demand factors.

Volatile Fuel & Electricity Prices

EU industrial power prices averaged 2.5× US levels in 2024; Spanish kilns are particularly exposed because thermal energy accounts for up to 70% of clinker heat demand. Gas spikes post-Ukraine conflict prompted an industry-wide 37% alternative fuel substitution in 2024, with leading firms targeting 50% by 2030. Cementos Portland Valderrivas locked in 80,000 MWh a year of wind power from Cantabria to hedge electricity risk. Despite mitigation, volatility remains a margin overhang that slightly trims overall growth momentum for the Spain cement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portland Cement Dominates Amid Blended Upsurge

Portland Cement retained 61.74% of the Spain cement market share in 2025 on the strength of familiarity and code compliance, yet its growth rate trails that of blended alternatives. The Spain cement market size for Portland grades is forecast to advance at a slower pace as public procurement progressively penalizes high-clinker mixes. Blended Cement, expanding at 6.05% CAGR from 2026 to 2031, captures the sustainability premium as CEM II/B-L and CEM IV/C targets proliferate in green building certifications. EU taxonomy alignment, ample fly-ash and slag streams, and domestic calcined clay deposits allow producers to scale blended output without major import dependencies, enhancing supply resilience. Specialty cements for marine, sulfate-resistant and high-early-strength applications sit in a smaller “Others” bucket yet command premium pricing tied to offshore wind and hydrogen projects. As uptake widens, blended grades are projected to narrow the volume gap with Portland, reinforcing the medium-term transition narrative within the Spain cement market.

By Application: Infrastructure Growth Outpaces Residential Weight

Residential construction represented 37.21% of the Spain cement market size in 2025, reflecting steady apartment starts in metropolitan areas. However, infrastructure displays the highest CAGR at 5.72% through 2031 as rail electrification, port dredging and grid upgrades absorb large continuous pours. Commercial segments benefit from tourism-linked refurbishments and logistics warehouses near coastal gateways, while industrial and institutional builds receive a boost from hydrogen valleys and wind-component factories. Application mix shifts toward projects demanding higher durability and lower carbon profiles, reinforcing demand for blended and specialty cements. Regional divergence persists: Madrid and Barcelona anchor residential consumption, Andalusia leads industrial volumes, and the Basque Country sees strong infrastructure pilot programs. Collectively, these dynamics sustain diversified demand streams that buttress the Spain cement market against cyclical shocks.

Geography Analysis

Andalusia, with its abundant limestone reserves and export-friendly ports, serves as the production heartland of Spain's cement market, contributing significantly to the nation's clinker capacity. Catalonia and the Basque Country rank next, leveraging industrial ecosystems and infrastructure budgets to absorb output through local projects. Madrid’s status as the primary consumption node necessitates efficient road-rail logistics from southern and eastern plants, spurring investments in satellite grinding stations to trim freight costs.

Northern coastal regions—Galicia, Asturias, and Cantabria—are evolving into hubs for marine-grade cement tied to offshore wind substructures. Cementos Portland Valderrivas has secured renewable-energy PPAs in Cantabria to power these niche, high-margin lines. Valencia and Murcia on the Mediterranean corridor enjoy demand uplift from cruise-terminal expansions and cold-storage logistics serving agrifood exports, sustaining continuous bagged-cement draw.

Island territories face structural import reliance; the Canary Islands in particular offer premium pricing for low-alkali, sulfate-resistant blends critical to floating wind demos. Freight optimization and modular grinding units are being studied to secure supply and limit price dispersion. Overall, geographic dispersion provides a natural hedge, distributing risk and stabilizing aggregate volumes for the Spain cement market.

Competitive Landscape

The spain cement market exhibits highly consolidated concentration. Global majors—CEMEX, Heidelberg Materials, and Holcim—operate integrated plants and grinding terminals that jointly command a majority of national output. CEMEX spearheads digitalization, piloting kiln-AI with Optimitive and adopting Microsoft Copilot to automate customer-facing tasks. Heidelberg pushed sustainable products to 42.8% of cement revenue in 2024, while Holcim consolidated its Tarragona distribution arm to streamline coastal shipments.

Domestic champion Cementos Portland Valderrivas taps renewable PPAs and waste-fuel grants to raise alternative fuel substitution to 45% by 2027. Mid-tier regional player Cementos La Cruz positions on low-carbon niche products and supplies 1.5 million tons of capacity to Mediterranean contractors[2]Cementos La Cruz, “Fabricación y distribución de cementos,” cementoscruz.com . New entrants include Çimsa, which purchased the Buñol white-cement plant and later acquired Mannok, signaling Turkish capital’s appetite for Iberian assets.

Competitive intensity is sharpening around fuel-switch innovation, circularity services and blended-cement quality credentials. Producers with integrated slag and ash sources command cost advantages once the Carbon Border Adjustment Mechanism penalizes imported clinker streams. The Spain cement market therefore rewards scale, alternative-fuel optionality and digital process control, driving ongoing consolidation and technology partnerships.

Spain Cement Industry Leaders

CEMENTOS PORTLAND VALDERRIVAS, S.A

CEMEX S.A. de C.V.

Heidelberg Materials

Holcim

Molins

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Holcim Spain has absorbed its subsidiary, Cementos Esfera, which operates a cement distribution facility in the port of Tarragona, Spain. This strategic consolidation strengthens Holcim Spain's market position and enhances control over its distribution network, enabling quicker adaptation to market changes.

- February 2024: Cemex has introduced a micronization process to reduce CO2 emissions in cement production by minimizing clinker particle size. This innovation lowers the clinker factor per ton of cement, significantly cutting its carbon footprint. This advancement is expected to enhance sustainability and competitiveness in the Spain cement market.

Spain Cement Market Report Scope

Cement serves as a binder, a chemical agent pivotal in construction. It sets, hardens, and adheres to various materials, effectively binding them together. Typically, cement appears as a fine, soft powder. When mixed with water and other substances, it forms mortar or concrete. While cement can stand alone, its primary role is to bind sand and gravel (aggregate). When combined with fine aggregate, it produces mortar for masonry; mixed with sand and gravel, it yields concrete.

The Spanish cement market is segmented by type and application. By product type, the market is segmented into portland, blended and other types. By application, the market is segmented into residential, commercial, infrastructure, and industrial and institutional. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Portland Cement |

| Blended Cement |

| Others |

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

| By Product Type | Portland Cement |

| Blended Cement | |

| Others | |

| By Application | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional |

Key Questions Answered in the Report

What is the current size of the Spain cement market?

The Spain cement market size reached 17.62 million tons in 2026 and is forecast to climb to 21.45 million tons by 2031.

Which product segment is growing fastest in Spain’s cement sector?

Blended Cement is projected to expand at a 6.05% CAGR between 2026 and 2031 due to EU taxonomy incentives for low-clinker mixes.

How significant are infrastructure projects to future cement demand in Spain?

Infrastructure is the fastest-growing application segment at 5.72% CAGR, driven by rail electrification, port upgrades, and renewable-energy investments.

What role do environmental regulations play in shaping the market?

EU-ETS costs and carbon-border adjustments are raising production expenses, accelerating the shift to low-carbon cements and alternative fuels.

How are Spanish cement producers leveraging technology?

Firms like CEMEX use AI-driven kiln optimization and predictive maintenance to trim energy use by up to 10% and reduce unplanned downtime, bolstering margins amid price volatility.

Page last updated on: