GCC Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

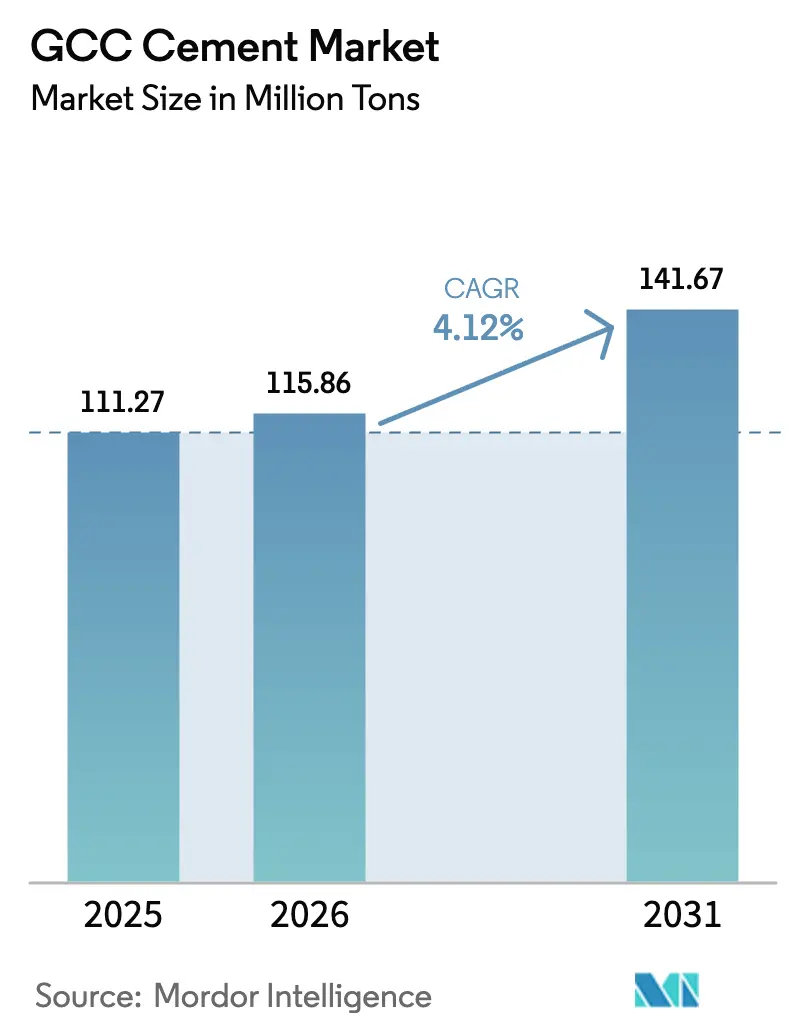

| Base Year Market Size (2025) | 111.27 Million tons |

| Market Volume (2026) | 115.86 Million tons |

| Market Volume (2031) | 141.67 Million tons |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

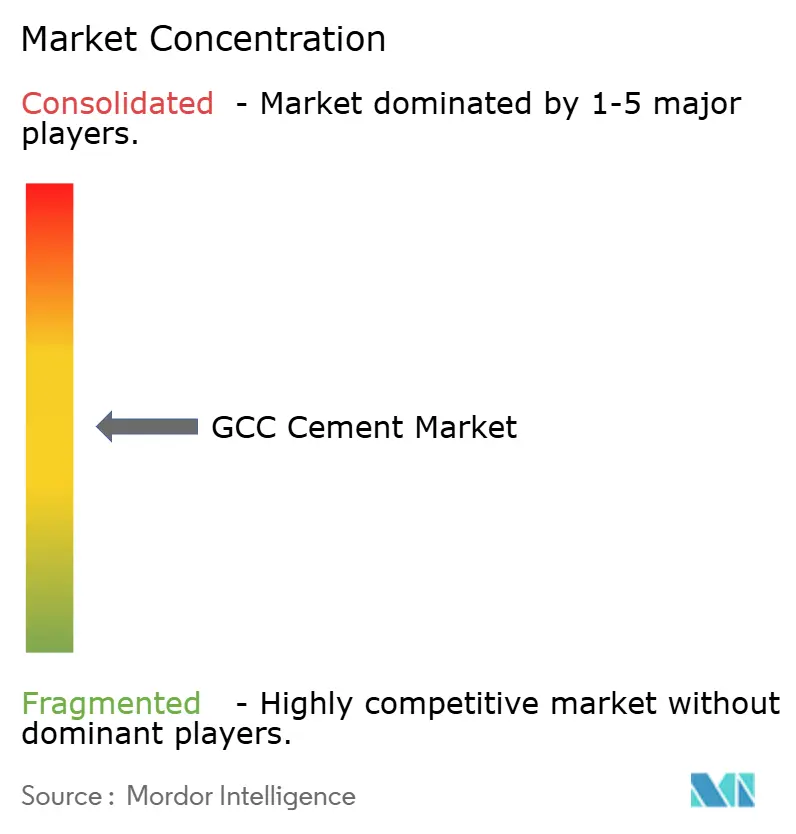

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Cement Market Analysis by Mordor Intelligence

GCC Cement Market size in 2026 is estimated at 115.86 million tons, growing from 2025 value of 111.27 million tons with 2031 projections showing 141.67 million tons, growing at 4.12% CAGR over 2026-2031. Sustained megaproject spending, expanding residential programs, and coordinated Vision 2030 agendas position the GCC cement market for steady growth despite oil–revenue transitions, carbon pricing debates, and tightening global supply of supplementary cementitious materials. Saudi Arabia and the UAE dominate consumption through large‐scale projects such as NEOM, Etihad Rail, and Dubai Vertical City, while Qatar, Kuwait, Oman, and Bahrain provide incremental demand that supports regional supply-chain resilience. Policy-led clinker‐capacity consolidation, coupled with aggressive waste-heat recovery investments, is helping producers lower operating costs, enhance resource efficiency, and prepare for carbon-credit compliance regimes. At the same time, accelerating adoption of blended cement underscores a strategic pivot toward lower-carbon solutions that align with Net-Zero targets and emerging ESG financing criteria. Competitive intensity remains high because regional capacity continues to outstrip domestic need, yet companies with scale, modern kilns, and proximity to high-growth clusters are improving utilization rates and protecting margins.

Key Report Takeaways

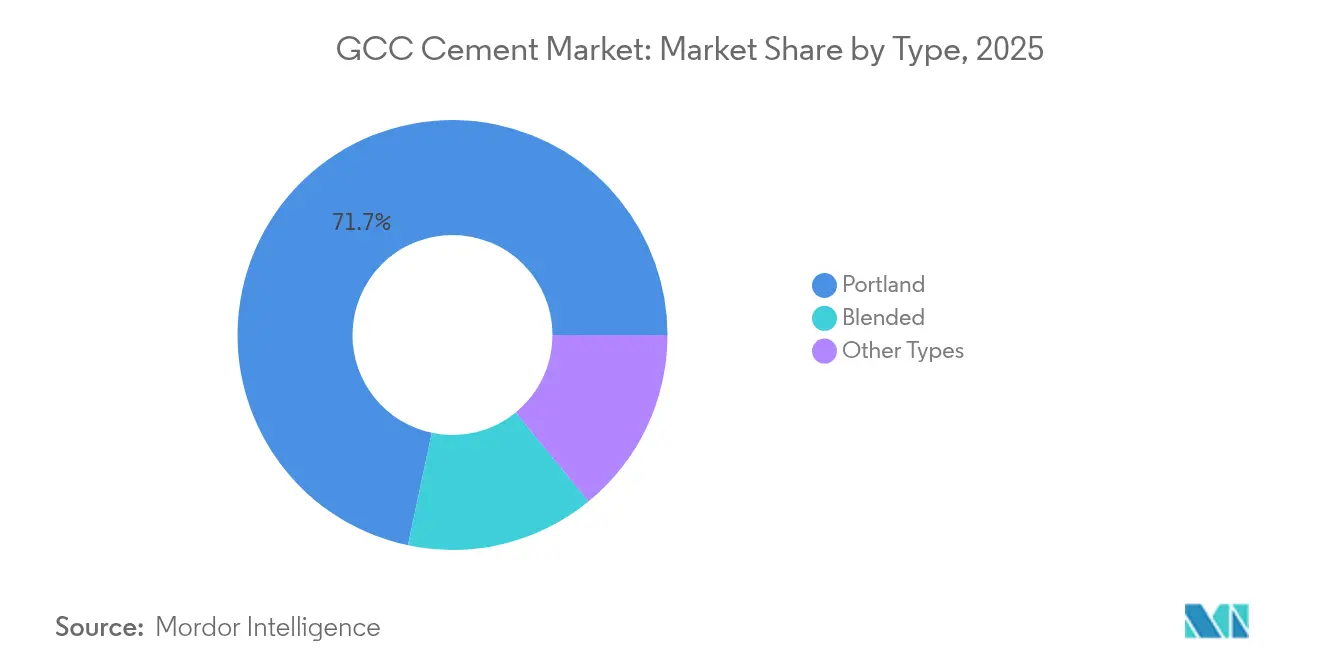

- By type, Portland cement led with 71.68% share of the GCC cement market size in 2025, while blended cement posted the highest forecast CAGR at 5.18% through 2031.

- By end-user, the residential segment captured 64.12% of the GCC cement market share in 2025 and is projected to expand at a 4.89% CAGR between 2026 and 2031.

- By geography, Saudi Arabia accounted for 51.62% of the GCC cement market size in 2025 and is advancing at a 5.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Cement Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing residential construction programs | +0.8% | Saudi Arabia, UAE primary; Qatar, Kuwait secondary | Medium term (2-4 years) |

| Public-sector megaproject pipeline | +1.1% | Saudi Arabia, UAE dominant; regional spillover | Long term (≥ 4 years) |

| Mandatory clinker capacity consolidation policies | +0.4% | GCC-wide, Saudi Arabia is leading the implementation | Medium term (2-4 years) |

| Rapid adoption of blended/PLC cements to meet Net-Zero road-maps | +0.6% | UAE, Saudi Arabia, early adopters; regional follow | Long term (≥ 4 years) |

| Waste-heat recovery retrofits cutting unit costs for older kilns | +0.5% | GCC-wide, focus on aging facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Residential Construction Programs

Rising household formation and Vision 2030 mandates are pushing governments to accelerate housing delivery. NEOM alone incorporates multi-district residential zones that require several million tons of cement during the current phases. High-rise developments in Dubai, including towers topping 100 stories, illustrate a pivot toward vertical density that increases cement intensity per square meter. Kuwait’s fiscal reforms have unlocked private-public partnership financing for large housing sites, making output less sensitive to annual oil receipts. Collectively, these projects create a predictable offtake across the cycle and dampen volatility that characterized earlier infrastructure-heavy booms. The demographic imperative also ensures that residential budgets remain politically protected even when macroeconomic conditions soften.

Public-Sector Megaproject Pipeline

Sovereign wealth fund backing provides durable capital for megaprojects from Saudi Arabia’s USD 500 billion NEOM program to the UAE’s national rail network. Etihad Rail’s 1,200-kilometer corridor requires extensive track beds, bridges, and passenger termini that consume large volumes of ready-mix concrete. Post-World-Cup redevelopment in Qatar keeps stadium sites active as mixed-use districts, maintaining demand long after initial event deadlines. Because these projects are embedded in diversification strategies, they face fewer cancellation risks tied to short-term oil prices. They also improve regional trade links, benefiting cement plants near export corridors.

Mandatory Clinker Capacity Consolidation Policies

Saudi Arabia, followed by other GCC members, has introduced licensing rules that tie renewal to energy-efficiency benchmarks and environmental compliance. Sector studies found that only 23.21% of Saudi producers achieved technical efficiency during 2016-2019, underscoring consolidation potential. New requirements encourage mergers, modern kilns, and waste-heat recovery systems that can deliver up to 30% of plant electricity and lift EBITDA margins by 10-15%[1]“A Concrete Energy Efficiency Solution,” World Bank Group, worldbank.org . The policies shrink marginal capacity, reduce oversupply, and support a balanced GCC cement market over the forecast window.

Rapid Adoption of Blended/PLC Cements to Meet Net-Zero Road Maps

The UAE activated its National Register of Carbon Credits in December 2024, obliging large emitters to record and verify footprints starting June 2025. Blended cement adoption, which can lower clinker factors toward 60%, is the quickest path to compliance. Saudi Arabia’s methane-reduction pledge and planned carbon-capture clusters reinforce the shift. Producers are scaling imports of slag and fly ash even as freight inflation raises landed costs, accelerating trials of locally calcined clay to stabilize supply.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-pricing frameworks under discussion in UAE and Saudi Arabia | -0.5% | UAE immediate, Saudi Arabia phased implementation | Short term (≤ 2 years) |

| Rising sea-borne slag/SCM costs amid tight global supply | -0.3% | GCC-wide, import-dependent producers are most affected | Medium term (2-4 years) |

| Chronic regional over-capacity keeping utilisation at a lower level | -0.7% | GCC-wide, particularly Saudi Arabia and the UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carbon-Pricing Frameworks Under Discussion in UAE and Saudi Arabia

The UAE’s Cabinet Resolution 67 of 2024 imposes monitoring, reporting, and verification on facilities emitting more than 0.5 million tons of CO₂e and sets fines that reach AED 1 million. Saudi Arabia is drafting a parallel market aligned with its 30% methane reduction goal. First Abu Dhabi Bank has launched a carbon-trading desk to supply liquidity and price discovery[2]“FAB partners with Masdar and Blue Carbon,” First Abu Dhabi Bank, bankfab.com . While well-managed plants may monetize surplus credits, less efficient producers could face cost escalation that compresses margins until retrofits are completed.

Rising Sea-Borne Slag/SCM Costs Amid Tight Global Supply

Widening global demand for low-carbon cement has outpaced slag and fly-ash production growth. GCC producers depend on imports from East Asian and European steel hubs, exposing them to shipping-rate volatility and currency shifts. The imbalance raises the delivered cost of blended cement and could delay aggressive clinker-replacement targets. Investment in calcined-clay processing is emerging as a hedge, yet capital outlays and performance testing extend commercialization timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Portland Dominance Faces Blended Cement Innovation

Portland cement retained a 71.68% share of the GCC cement market 2025, reflecting entrenched design codes and supply-chain familiarity. The segment continues to anchor production economics; however, the blended category is set to deliver a 5.18% CAGR that will gradually lower Portland’s dominance. Blended grades benefit from policy incentives, corporate ESG commitments, and the rising cost of carbon credits under discussion. Yet the transition requires retooling mills, recalibrating quality protocols, and educating downstream contractors.

Energy-efficiency retrofits support both segments. Waste-heat recovery turbines produce baseload power that shields plants from tariff hikes and enhances profitability. Producers also optimize kiln scheduling around peak renewable output to shrink emissions. These operational gains combine with blended cement adoption to strengthen the overall competitiveness of the GCC cement market while advancing decarbonization objectives.

By End-User Industry: Residential Sector Drives Dual Leadership

Residential construction accounted for 64.12% of total volume in 2025 and is forecast to grow at a 4.89% CAGR, maintaining clear supremacy in both share and momentum. Large-scale housing under Vision 2030 satisfies social targets and redirects investment from expatriate-oriented luxury units toward mid-income segments. Towers like Burj Binghatti illustrate a premium niche and highlight the engineering shift to vertical urbanism that lifts cement demand per housing unit.

Commercial buildings benefit from tourism diversification, especially in Riyadh’s cultural districts and Dubai’s hospitality corridors. Infrastructure projects, including high-speed rail and desalination plants, provide a steady baseline demand. Industrial and institutional builds—universities, hospitals, logistics hubs—offer specialized applications like sulfate-resistant cement but remain smaller slices of the GCC cement market. The breadth of end-users supports portfolio diversification for producers and cushions cyclical dips in any single category.

Geography Analysis

Saudi Arabia held 51.62% of regional consumption in 2025 and is projected to post a 5.31% CAGR through 2031 on the back of multiple Vision 2030 clusters. Projects ranging from Oxagon’s industrial port to The Line’s linear city require high-performance concrete mixes that drive consistent bulk orders. Capacity consolidation policies also remove inefficient lines, allowing remaining plants to improve utilization.

The UAE remains a key centre of demand, propelled by 24 flagship projects spanning transport, tourism, and residential verticals. Its carbon-credit framework is already influencing procurement specs, accelerating blended cement uptake, and rewarding efficient producers. Qatar, Kuwait, Oman, and Bahrain round out the market, contributing niche opportunities in marine structures, petrochemical complexes, and tourism resorts that demand specialized formulations. Their combined activity diversifies revenue streams for region-wide players and balances the geographic risk inherent in a Saudi–UAE concentration.

Competitive Landscape

The GCC Cement Market is partially fragmented. Chronic over-capacity remains the core competitive challenge. Producers are responding with plant upgrades, alternative-fuel lines, and regional mergers. Domestic leaders rationalize parallel kilns and digitize maintenance to extend asset life and free cash flow. Niche opportunities in marine and high-alumina grades remain underserved, creating a white space for specialized players as regional port expansions accelerate. Market participants that align capacity additions with high-growth corridors and secure long-term offtake agreements stand to improve asset turns. Conversely, companies that delay decarbonization investments risk regulatory penalties and losing bids on government projects that increasingly embed carbon-intensity scoring. Overall, strategy is shifting from volume capture to value capture, emphasizing efficiency, product differentiation, and environmental credentials.

GCC Cement Industry Leaders

Southern Province Cement Company

Saudi Cement Co.

Yanbu Cement Company

Qatar National Cement Co.

Najran Cement Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Yanbu Cement and Southern Cement have extended their memorandum of understanding to continue evaluating the feasibility of a merger. This move reflects ongoing consolidation efforts in the GCC cement sector, as companies seek to optimize operations, enhance competitiveness, and navigate regional market dynamics.

- January 2024: Yamama Cement announced the expansion of a production line and shifted its old plant site south of Riyadh to its new site at Northern Halal in the Al-Kharj governorate. The expansion and shifting of the project will increase the capacity from 10,000 tons/day to 12,500 tons/day.

GCC Cement Market Report Scope

Cement, a crucial building component, is a binding agent that sets and hardens to cling to building units such as stones, bricks, and tiles. It is a fine powdery substance composed primarily of limestone (calcium), sand or clay (silicon), bauxite (aluminum), and iron ore. It may also include shells, chalk, marl, shale, clay, blast furnace slag, and slate.

The GCC cement market is segmented by type, application, and geography. The market is segmented into Portland, blended, and other types (rapid hardening cement, quick setting cement, expansive cement, hydrographic cement, and colored cement). The market is segmented by application into residential, commercial, infrastructure, industrial, and institutional. The report also covers the size and forecasts for the cement market in six regional countries. Market sizing and forecasts were made for each segment based on volume (tons).

| Portland |

| Blended |

| Other Types (rapid-hardening, quick-setting, expansive, hydrographic, coloured) |

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By Type | Portland |

| Blended | |

| Other Types (rapid-hardening, quick-setting, expansive, hydrographic, coloured) | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain |

Key Questions Answered in the Report

What is the current volume of the GCC cement market?

The GCC cement market size stands at 115.86 million tons in 2026 and is projected to climb to 141.67 million tons by 2031.

Which segment uses the most cement across the Gulf?

Residential construction leads consumption with a 64.12% share in 2025 and continues to grow faster than other end-user categories.

How fast is blended cement demand expanding in the region?

The blended segment is forecast to grow at a 5.18% CAGR through 2031 as policies favor lower-carbon formulations.

Why does Saudi Arabia dominate regional cement demand?

Vision 2030 megaprojects, such as NEOM and sustained housing programs, give Saudi Arabia a 51.62% market share and the highest regional growth rate.

What key policy trend will shape future plant economics?

Emerging carbon-pricing frameworks in the UAE and Saudi Arabia will influence production costs and accelerate investment in emissions-reduction technology.

Which technology offers immediate cost savings for producers?

Waste-heat recovery systems can supply up to 30% of a plant’s electricity and lift EBITDA margins by 10-15%, helping offset fuel and carbon costs.

Page last updated on: