Italy Cement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

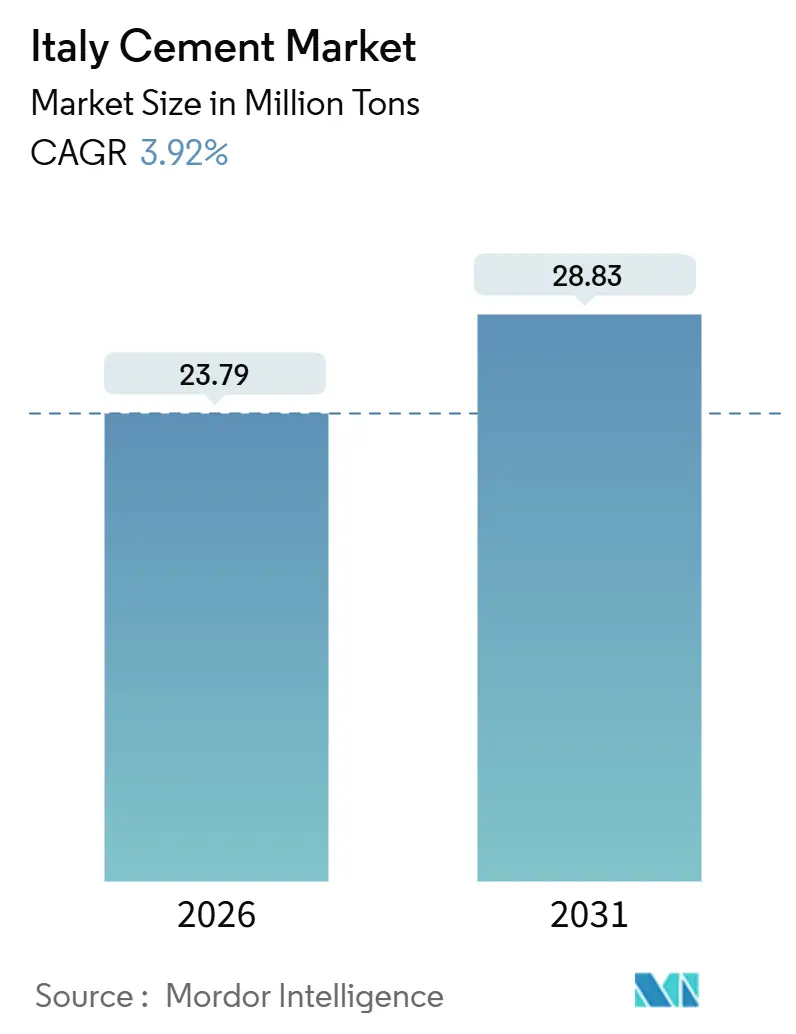

| Market Volume (2026) | 23.79 Million tons |

| Market Volume (2031) | 28.83 Million tons |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

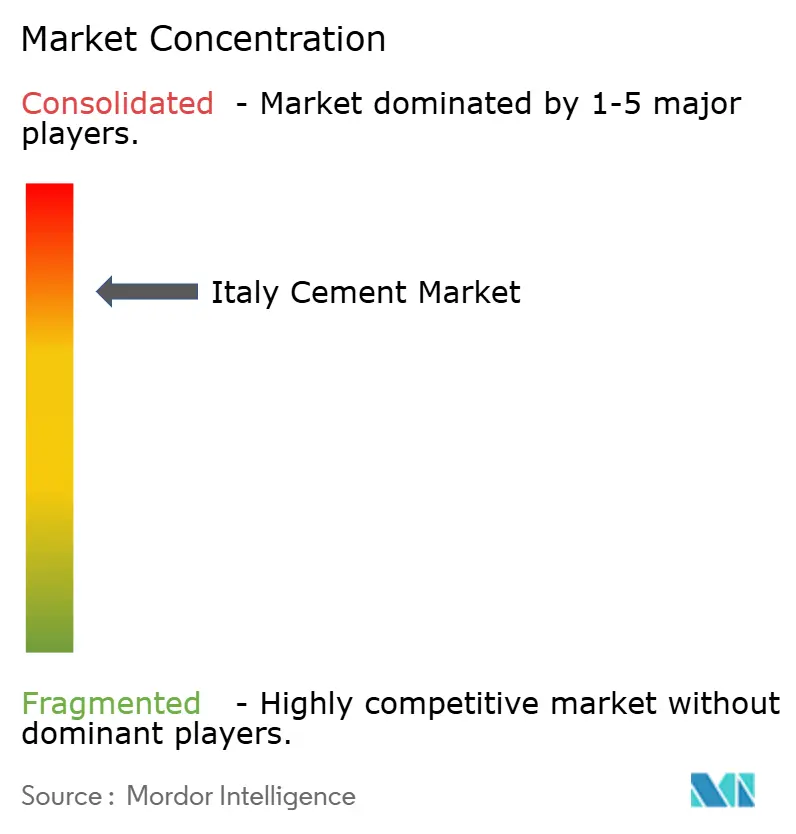

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Cement Market Analysis by Mordor Intelligence

The Italian Cement Market size is estimated at 23.79 million tons in 2026, and is expected to reach 28.83 million tons by 2031, at a CAGR of 3.92% during the forecast period (2026-2031). Infrastructure and non-residential construction are seeing a boost from the National Recovery and Resilience Plan (NRRP), even as the winding down of the Superbonus incentive dampens residential activity. Thanks to EN 197-5, blended formulations dominate the market, allowing producers to increase supplementary cementitious material (SCM) content. This adjustment reduces clinker demand and carbon emissions without sacrificing performance. While major players control a significant portion of the capacity, regional fragmentation offers mid-tier firms opportunities to secure niche contracts through strategic proximity and zero-kilometer sourcing. However, rising EU ETS costs, fluctuating energy prices, and dwindling domestic fly-ash supplies are tightening margins. In response, there's a noticeable shift towards investments in alternative fuels and digital logistics, both of which enhance cost control and regulatory compliance.

Key Report Takeaways

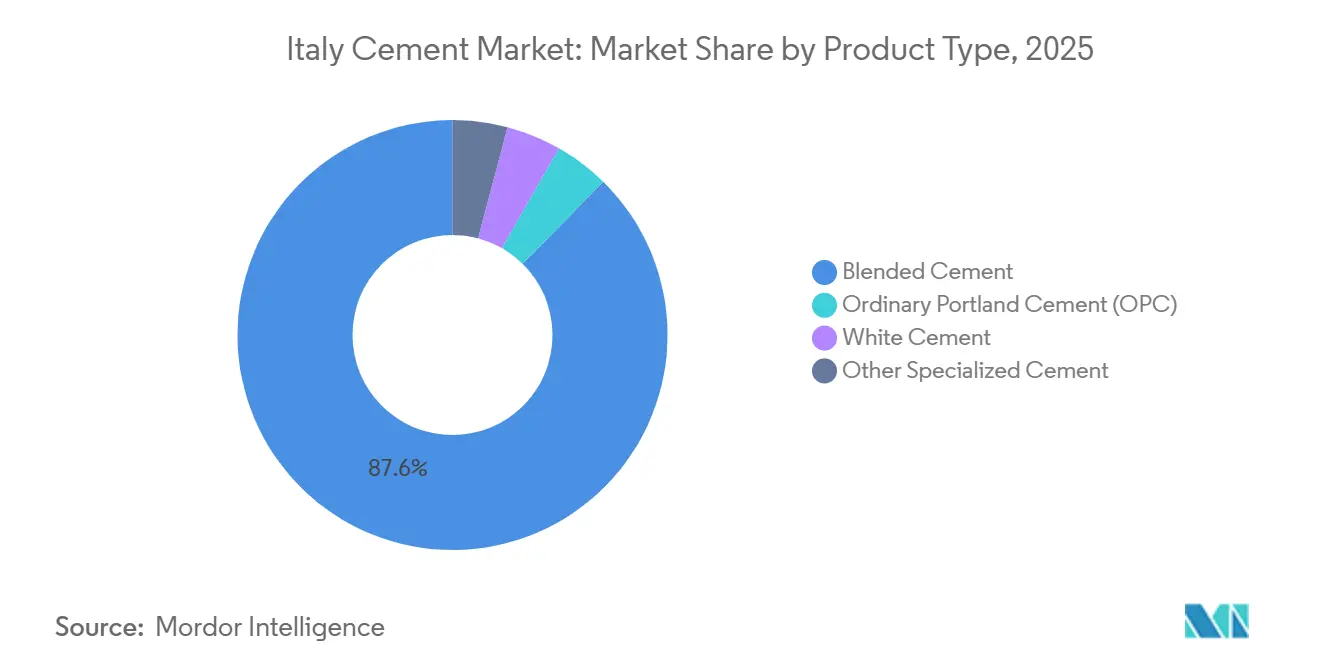

- By product type, blended cement led with 87.64% Italy cement market share in 2025, while Ordinary Portland Cement (OPC) is projected to post the fastest 4.01% CAGR through 2031.

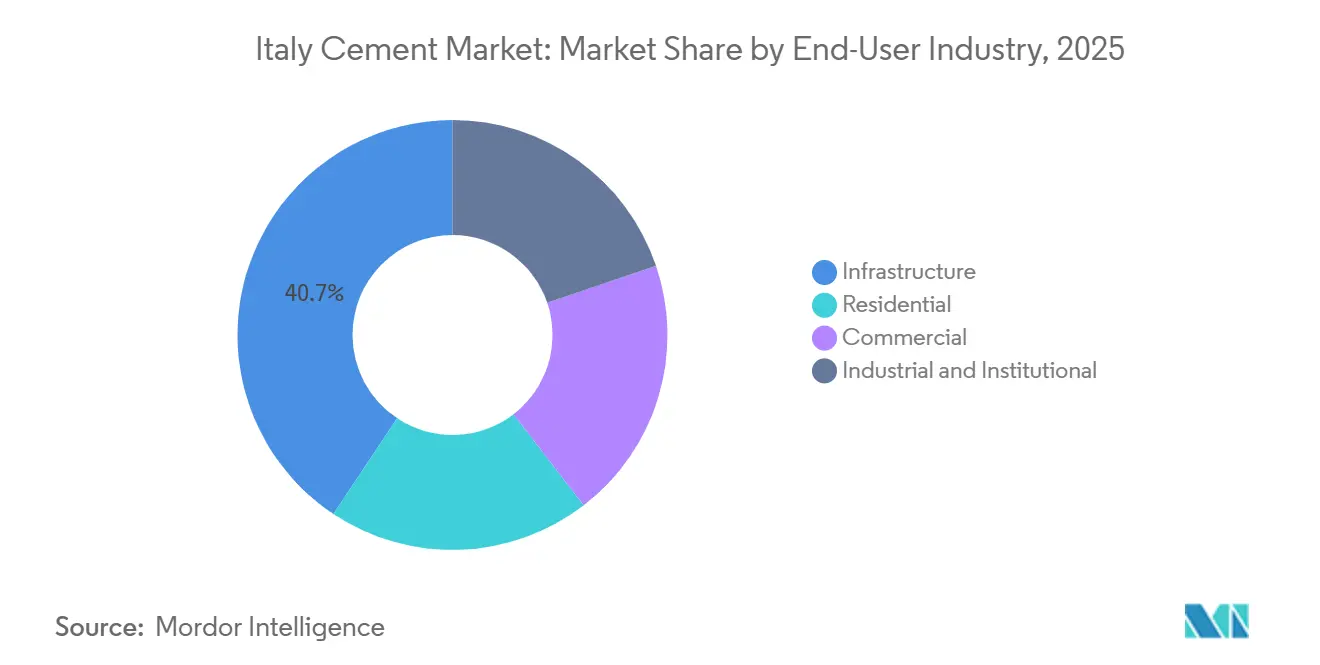

- By end-user industry, infrastructure accounted for 40.67% of the Italy cement market size in 2025 and is set to expand at a 4.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Cement Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-funded infrastructure pipeline (NRRP) | +1.2% | National, with concentration in Southern Italy (Naples-Bari corridor) and Northern Italy (Turin-Lyon tunnel) | Medium term (2-4 years) |

| Post-pandemic non-residential rebound | +0.8% | National, led by Lombardy, Lazio, and Emilia-Romagna industrial zones | Short term (≤ 2 years) |

| Regulatory push toward blended/low-clinker cements | +0.6% | EU-wide, with early adoption in Northern Italy cement plants | Long term (≥ 4 years) |

| Digitalisation of construction supply-chain | +0.3% | National, concentrated in Tier-1 metropolitan areas (Milan, Rome, Turin) | Medium term (2-4 years) |

| Zero-km pozzolan utilisation in Southern Italy | +0.4% | Regional, focused on Campania, Sicily, and Calabria volcanic zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Funded Infrastructure Pipeline Drives Structural Demand

The NRRP designates significant funding for sustainable mobility projects in Italy, including the Naples–Bari high-speed rail, the Turin–Lyon base tunnel, and metro extensions in Milan, Rome, and Naples[1]European Commission, “Recovery and Resilience Facility,” commission.europa.eu. This investment sets a multi-year demand floor for Italy's cement market. Additionally, funding allocated for water networks will drive demand for premium-priced, sulfate-resistant cement. Disbursements are milestone-linked, with tonnage peaking during major civil pours in 2027-2028. Contractors are granting long-term supply frameworks exclusively to producers compliant with EN 206 standards and holding verified environmental product declarations. With a substantial portion of NRRP funds directed towards Southern regions, there's a noticeable southward shift in Italy's cement market footprint, leading to a redistribution of both output and logistics resources.

Post-Pandemic Non-Residential Construction Rebounds Sharply

In 2024, non-residential output surged, driven by logistics hubs in Lombardy and Emilia-Romagna, alongside hyperscale data centers in Lazio and Piedmont. These facilities exert a more pronounced influence on Italy's cement market than traditional housing. Additionally, industrial and institutional retrofits, bolstered by NRRP's energy-efficiency funding, are keeping demand high for precast columns, floor slabs, and foundation upgrades. While this momentum is evident, analysts warn that the number of shovel-ready private projects is dwindling post-2028, coinciding with a tapering public stimulus. Thus, the trajectory of growth will largely depend on the resilience of corporate capital spending in the face of macroeconomic uncertainties.

Regulatory Mandates Accelerate Blended-Cement Adoption

Since 2024, Italy has fully enforced EN 197-5, allowing composite grades like CEM II/C-M to incorporate SCMs. This move not only cuts embodied carbon but also reduces exposure to the EU ETS. Buzzi's blend, using Campania pozzolan, achieved a reduction in carbon footprint while still meeting strength requirements. This achievement immediately qualified Buzzi for green-procurement bonuses under Italy's Minimum Environmental Criteria (CAM). As free allowances under ETS Phase IV decrease annually, any reduction in the clinker ratio translates directly to cost savings. However, smaller mills, which may not have immediate access to SCMs, face the risk of being sidelined in public tenders. To remain competitive, they might need to form partnerships for supply or upgrade their kilns to accommodate alternative binders.

Digitalisation Reshapes Construction Supply-Chain Coordination

Legislative Decree 50/2016 mandates BIM for public contracts. This pushes cement suppliers to meld enterprise resource planning, dispatch tracking, and quality dashboards with contractor digital twins. Holcim's IoT-enabled bulk fleet transmits real-time slump and temperature data to site tablets, reducing quality disputes and minimizing idle-time penalties. At Rezzato, Heidelberg Materials is piloting blockchain traceability, integrating verified carbon metrics into LEED scorecards. Such advancements are already shaping award criteria for NRRP mega-projects, making digital readiness a crucial determinant for opportunities in Italy's cement market. Producers lacking interoperable systems risk exclusion from lucrative contracts and might need to collaborate in consortia to maintain relevance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter ETS Phase IV CO₂ cost burden | -0.5% | National, with acute impact on Northern Italy clinker-intensive plants | Short term (≤ 2 years) |

| Rising Energy and Fuel Costs | -0.4% | National, particularly energy-intensive grinding operations | Medium term (2-4 years) |

| Shrinking availability of fly-ash and slag SCMs | -0.3% | National, with supply-chain dependencies on Turkey and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ETS Phase IV Imposes Escalating Carbon Compliance Costs

In 2025, EU ETS allowances fluctuated. As free allocations to the cement industry decrease annually, producers are compelled to purchase certificates to cover the deficit[2]European Commission, “EU ETS,” climate.ec.europa.eu. A plant producing with a clinker ratio of 70% is projected to incur additional carbon expenses. In the absence of cost-pass-through clauses tied to ETS prices, profit margins are squeezed, leading to delays in kiln upgrades and carbon-capture retrofits. Heidelberg Materials' Rezzato capture initiative underscores that only financially robust companies can invest in solutions that secure their foothold in Italy's cement market.

Energy-Price Volatility Sustains Operational Cost Pressure

Italian kilns, heavily reliant on natural gas, face spot prices in 2025 that remain elevated, keeping their variable costs high. High electricity costs for grinding have granted coastal importers from Turkey a significant advantage in landed costs. A surge in imports in 2024 highlights the vulnerability of Liguria and Campania ports to more affordable foreign cement. Holcim's waste-heat recovery retrofit at its Merone facility aims to reduce thermal energy use, but current gas price trends indicate a lengthy payback period. Energy pressures will continue until Italy adjusts its co-processed fuel rate closer to the EU average.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dominance of Blended Formulations Under Carbon and Cost Tailwinds

Blended cement accounted for 87.64% of Italy's cement market size in 2025, reflecting its cost advantage and eligibility for CAM green-procurement bonuses. With a reduced clinker content, blended cement not only minimizes direct CO₂ emissions but also protects producers from stringent ETS caps, facilitating adherence to corporate net-zero commitments. Infrastructure entities, particularly those under NRRP, often mandate CEM II/B-M or CEM II/C-M grades. This preference boosts demand for SCM suppliers and promotes localized pozzolan extraction in regions like Campania and Sicily. Concurrently, Ordinary Portland Cement (OPC) carves out a niche, proving indispensable for precast bridge girders, tunnel linings, and rapid pavement overlays, all demanding high strengths within 24 hours. While white cement constitutes a small portion of the total volume, it enjoys a premium in façade projects across Milan, Rome, and Florence. Specialty cements cater to marine applications, sulfate resistance, and cold-weather pours, ensuring a diverse portfolio for the Italian cement market, even amidst the dominance of blended grades.

Looking forward, the Italian cement market is poised for a two-pronged growth trajectory. Ordinary Portland Cement (OPC) is forecast to post a 4.01% CAGR through 2031 because its high early-strength chemistry suits time-sensitive public works. On the other hand, innovative low-clinker technologies like limestone-calcined-clay (LC³) and belite-ye’elimite-ferrite (BYF) are currently in pilot testing. Heidelberg Materials, targeting a significant reduction with LC³ at its Rezzato site, underscores the competitive edge in swiftly adopting alternative binders that meet EN standards. Thus, the market navigates a delicate balance of cost, carbon footprint, and engineering challenges, ensuring OPC's continued relevance even as regulations favor blended cement.

By End-User Industry: Infrastructure Sets the Pace While Residential Retracts

Infrastructure absorbed 40.67% of Italy's cement market share in 2025 and is projected to grow at a 4.23% CAGR to 2031. With a commitment to upgrades spanning rail, metro, highways, and ports, this segment is set to expand through 2031. The Naples–Bari corridor is projected to consume significant amounts of cement. In tandem, Milan’s M4 extension and Rome’s Line C are expected to draw substantial quantities. Notably, infrastructure's cement intensity surpasses that of housing, underscoring infrastructure's significant influence on Italy's cement market. Furthermore, procurement mandates like ISO 14001 certification and real-time logistics data tilt the advantage towards digitally adept major players, sidelining their analog mid-cap counterparts.

Residential construction is witnessing a slowdown, primarily due to the expiration of the Superbonus 110% incentive in December 2023. This has resulted in a backlog of completed renovations and a sharp decline in new permits. Additionally, Italy's demographic challenges—an ageing populace and stagnant household formation—pose structural hurdles. These factors could potentially reduce the residential sector's market share in the coming years. On a brighter note, commercial projects are on the mend, buoyed by a resurgence in tourism and stabilized occupancy rates. However, the rise of hybrid work models is dampening the demand for new office spaces. Meanwhile, industrial and institutional sectors—including factories, warehouses, hospitals, and universities—are reaping the benefits of NRRP retrofit subsidies, providing them with a consistent foundation. As a result, while other segments play a stabilizing role, the Italy cement market is clearly shifting its focus towards civil infrastructure.

Geography Analysis

Historically, Northern Italy, with its robust industrial base, has consumed the majority of the nation's cement. However, the NRRP design has shifted the funding focus southward, allocating a substantial portion to the Mezzogiorno. Consequently, Southern regions have surpassed the national average and are making strides to close a long-standing infrastructure gap. High-volume contracts, such as the Palermo metro, Calabria highway widening, and Bari port dredging, are driving clinker transportation southward via rail and barge. Central Italy benefits from projects like Rome’s metro completion, data-center clusters in Lazio, and heritage restorations in Tuscany, which favor white and sulfate-resistant cements.

Lombardy stands out as the largest provincial market. This is bolstered by logistic park developments around Milan-Bergamo and a dual role in the Turin–Lyon tunnel. However, growth is stagnating as the residential renovation surge peaks and commercial landlords hesitate on new towers due to hybrid-work uncertainties. In contrast, Southern infrastructure is set to grow at a faster pace than the North. This growth is steering production capacity towards Barletta, Colacem’s mills in Lazio, and Vicat’s terminal in Sicily. Coastal regions like Liguria, Campania, and Sicily grapple with fierce import competition, as Turkish and North-African shipments arrive at discounted rates in Genoa, Naples, and Palermo. While CBAM’s phased rollout has momentarily exempted cement, allowing for this price arbitrage, it has also pressured domestic producers. To maintain their foothold in the Italian cement market, these producers are now compelled to streamline logistics and diversify their fuel sources.

Competitive Landscape

The Italian cement market is consolidated. Competitive vectors increasingly revolve around decarbonization pathways and digital integration. Heidelberg Materials’ Rezzato carbon-capture plan targets 95% CO₂ removal routed to the Ravenna offshore hub, aligning its product line with EU Taxonomy debt instruments and allowing premium pricing on ultra-low-carbon grades. Smaller mills that cannot finance digital platforms or capture retrofits face a strategic crossroads: consolidate, specialize, or exit. Niche plays include white cement, rapid-hardening blends for heritage projects, and geographic redoubts with high trucking barriers. Disruption is also brewing from alternative binders.

Italy Cement Industry Leaders

Heidelberg Materials

Buzzi SpA

Colacem S.p.A.

Alpacem

Holcim

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Alpacem acquired the Fanna cement plant near Pordenone. Under this acquisition, the company acquired the 0.66Mt/yr integrated plant and a number of ready-mixed concrete plants.

- September 2024: Heidelberg Materials started a feasibility study for a decarbonisation project at its Rezzato Mazzano cement plant in the province of Brescia, which could become the first plant in Italy to produce carbon captured Net Zero cement and concrete.

Italy Cement Market Report Scope

Cement is a finely ground powder that, when mixed with water, forms a hard, durable substance called concrete. It is an essential ingredient in the construction industry, used as a binding material to hold together aggregates like sand, gravel, and crushed stone.

The cement market is segmented by product type and end-user industry. By product type, the market is segmented into ordinary portland cement (OPC), blended cement, white cement, and others (composite, colored). By end-user industry, the market is segmented into residential, commercial, industrial, and institutional, and infrastructure. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Ordinary Portland Cement (OPC) |

| Blended Cement |

| White Cement |

| Other Specialized Cement |

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| By Product Type | Ordinary Portland Cement (OPC) |

| Blended Cement | |

| White Cement | |

| Other Specialized Cement | |

| By End-User Industry | Residential |

| Commercial | |

| Industrial and Institutional | |

| Infrastructure |

Key Questions Answered in the Report

What is the current volume of the Italy cement market and its expected growth to 2031?

The market stands at 23.79 million tons in 2026 and is projected to reach 28.83 million tons by 2031, tracking a 3.92% CAGR.

Which segment drives the highest demand for cement across Italy?

Infrastructure leads demand with a 40.67% share in 2025, supported by NRRP-funded rail, metro, and highway projects and expected to grow at a 4.23% CAGR through 2031.

Why is blended cement dominant in Italy?

EN 197-5 permits up to 50% SCM content, lowering cost and carbon intensity, which helped blended grades capture 87.64% market share in 2025.

Which region is set to grow fastest in cement consumption?

Southern Italy is forecast to be fastest fastest-growing region as NRRP funds prioritize backlog infrastructure across Campania, Sicily, Calabria, Puglia, and Basilicata.

What technological trends are shaping competitive advantage?

Digital logistics integration through IoT fleets, BIM data-sharing, and blockchain traceability is now a prerequisite for winning long-term public works contracts.

Page last updated on: