Space Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

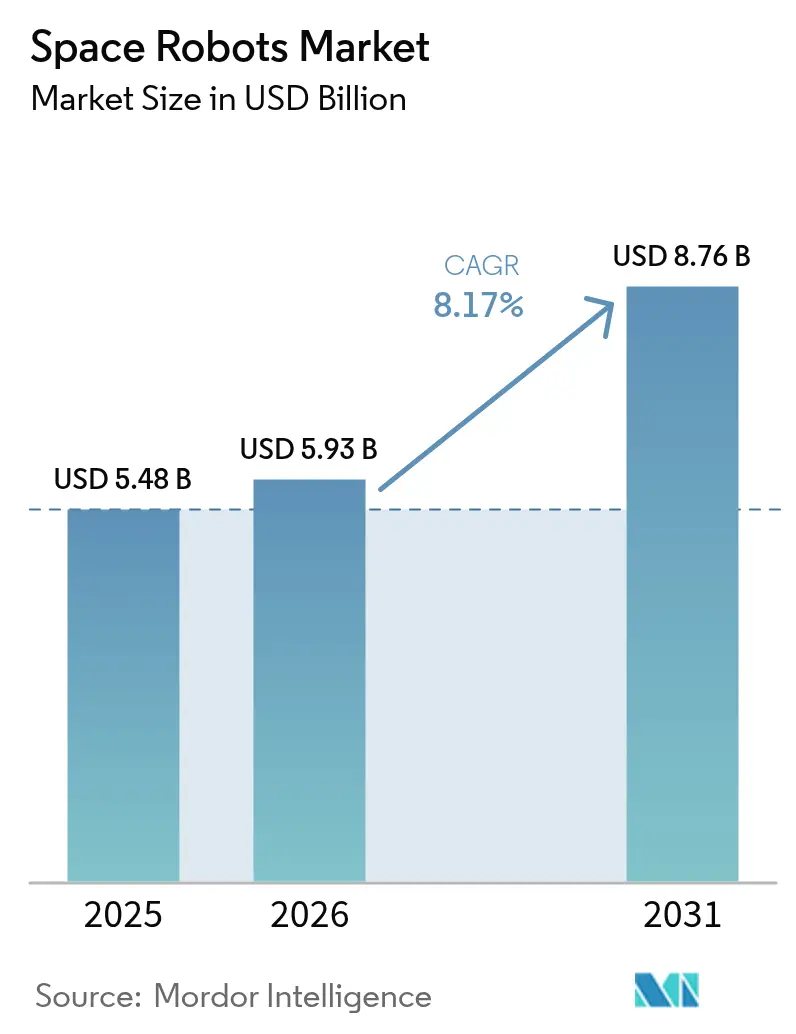

| Market Size (2026) | USD 5.93 Billion |

| Market Size (2031) | USD 8.76 Billion |

| Growth Rate (2026 - 2031) | 8.17% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Robots Market Analysis by Mordor Intelligence

The space robots market size is expected to grow from USD 5.48 billion in 2025 to USD 5.93 billion in 2026 and is forecast to reach USD 8.76 billion by 2031 at 8.17% CAGR over 2026-2031. Growing demand for autonomous servicing of aging satellites, expanding government exploration programs, and falling launch costs collectively strengthened near-term revenue growth. Large public contracts, such as the Canadian Space Agency’s USD 999.8 million award for Canadarm3, confirmed sustained capital inflows from national space agencies.[1]Source: Government of Canada, “Canada begins detailed design, construction and testing of Canadarm3,” canada.ca Commercial initiatives around active-debris-removal, on-orbit manufacturing, and lunar logistics further widened addressable opportunities. Meanwhile, relaxed US export-control rules improved international collaborations, lowering regulatory friction. Market entry remained costly, yet reusable launch vehicles reduced mission budgets and allowed smaller operators to field specialized robotic platforms.

Key Report Takeaways

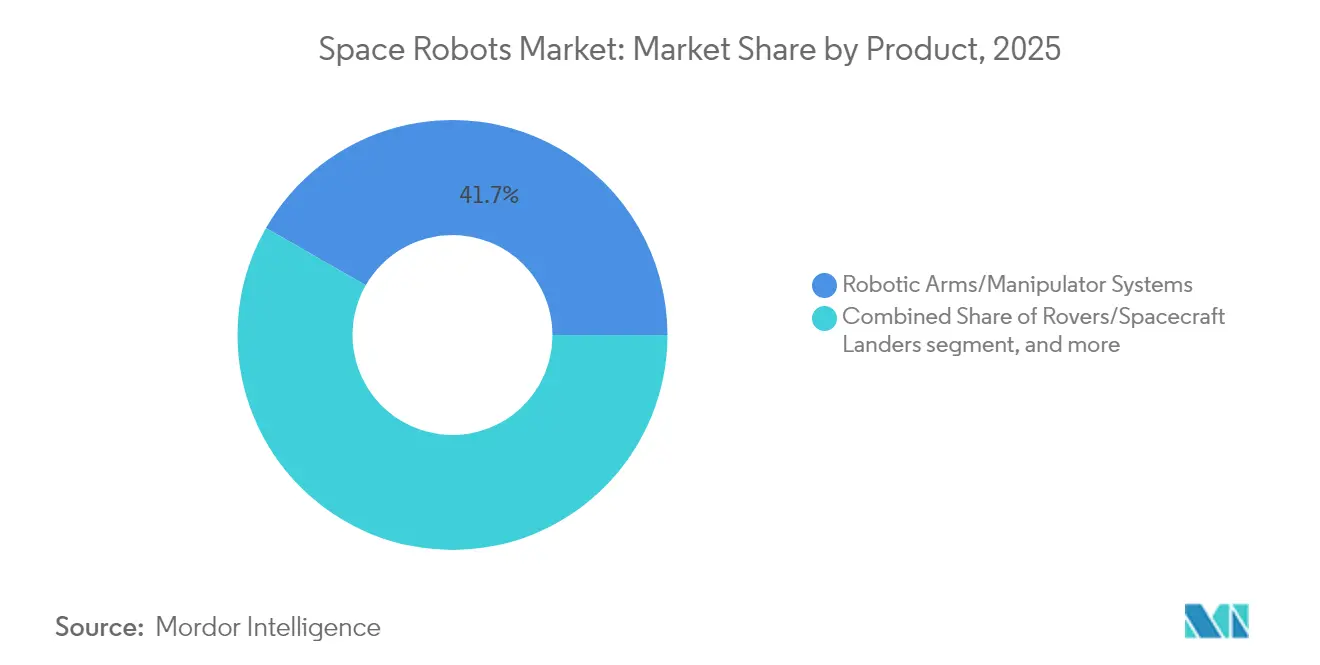

- By product, robotic arms and manipulator systems led with 41.72% revenue share in 2025; on-orbit servicing vehicles are projected to grow at a 9.33% CAGR through 2031.

- By mission type, near-space operations held 65.12% of the space robots market share in 2025, while deep-space missions are poised for a 9.86% CAGR to 2031.

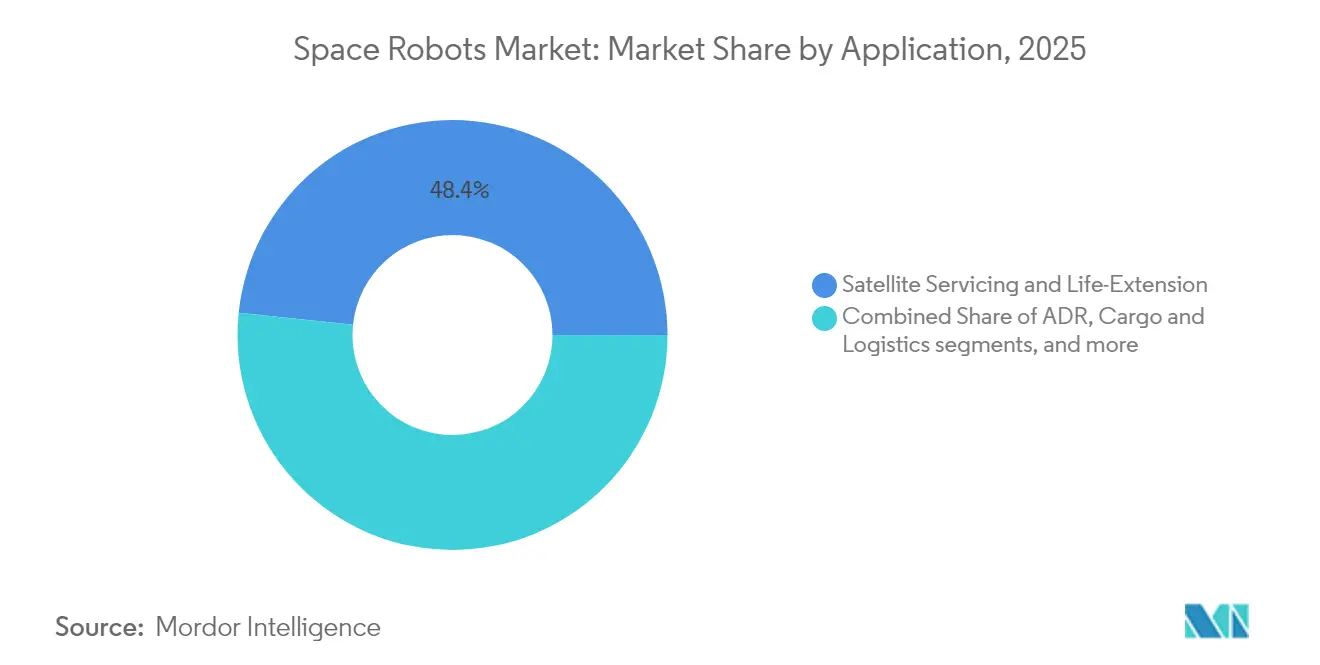

- By application, satellite servicing accounted for 48.35% of the space robots market size in 2025; active debris removal is advancing at a 11.92% CAGR.

- By end user, government entities held a 69.05% share of the space robots market in 2025, while commercial operators showed the fastest 10.22% CAGR.

- By component, hardware represented 71.88% of the space robots market size in 2025, yet software is rising at an 11.08% CAGR.

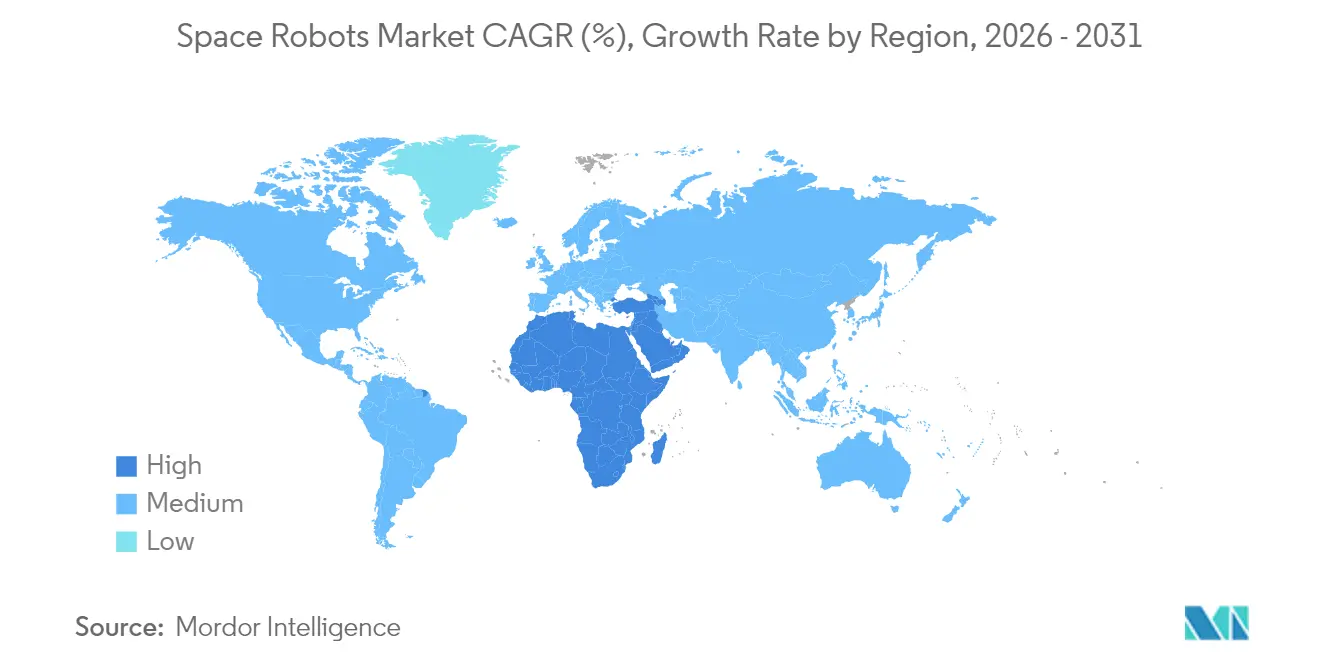

- By geography, North America led with 55.97% market share in 2025, while the Middle East and Africa region is expanding at a 11.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Space Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in on-orbit satellite-servicing demand | +2.1% | Global, concentrated in GEO belt operators | Medium term (2-4 years) |

| Government-funded lunar and Mars exploration programs | +1.8% | North America, Europe, Asia-Pacific core | Long term (≥ 4 years) |

| Falling launch costs from reusable launchers | +1.5% | Global, with early gains in US and China | Short term (≤ 2 years) |

| Expansion of commercial lunar logistics corridors | +1.2% | North America and EU, spill-over to APAC | Long term (≥ 4 years) |

| Growth in in-space manufacturing and 3-D printing needs | +0.9% | Global, early adoption in ISS operations | Medium term (2-4 years) |

| Defense-led demand for autonomous ISR rendezvous | +0.8% | National security focused regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in On-Orbit Satellite-Servicing Demand

High replacement costs for geostationary satellites, often surpassing USD 400 million, made life-extension missions economically compelling. Intelsat’s 2024 agreement with Starfish Space set a commercial precedent for robotic servicing, with the first mission slated for 2026. Northrop Grumman progressed toward a 2026 robot-armed Mission Extension Pod launch, validating confidence in near-term revenue. Parallel activity at the European Space Agency, which advanced its Geostationary Servicing Vehicle toward a 2028 debut, signaled agency-wide endorsement.[2]Source: ESA, “ESA moves ahead with In-Orbit Servicing missions,” esa.int Collectively, these milestones underpinned recurring demand for refueling, relocation, and inspection services, boosting predictable cash flows for in-orbit robotics providers.

Government-Funded Lunar and Mars Exploration Programs

NASA’s Artemis framework continued to allocate multi-year funding to robotic systems, evidenced by the CADRE rover network that passed integrated testing in March 2025. ESA’s Argonaut lunar lander target for 2031 introduced a 1,500 kg cargo capacity, supporting large-scale surface logistics. China accelerated its robotic lunar research outpost timeline by 2035, intensifying technology competition. These parallel programs stimulated demand for rugged manipulators, autonomous navigation software, and modular mobility platforms tailored to harsh lunar and Martian environments.

Falling Launch Costs from Reusable Launchers

SpaceX’s Falcon 9 drove launch prices down to USD 2,700 per kg to low Earth orbit, a fraction of historical expendable-vehicle rates. This pricing shift enabled more frequent missions and justified smaller, specialized robotic payloads. Chinese launch providers, including LandSpace, announced commercially reusable vehicles for 2025, adding competitive pressure. Lower cost-to-orbit dynamics encouraged venture investment in CubeSat-class servicing systems, shortening payback periods and spurring faster product cycles.

Expansion of Commercial Lunar Logistics Corridors

Venture funding flowed to private lunar-resource companies, such as Starpath Robotics' USD 12 million raise to develop mining systems. NASA's Commercial Lunar Payload Services contracts awarded to multiple firms institutionalized routine cargo delivery to the Moon. Partnerships like Astroport and Orbit Fab's in-space refueling initiative illustrated the private-sector commitment to a cis-lunar economy. With these logistics plans, demand for robotic cargo handling, excavation, and maintenance platforms rose in lockstep.

Restraints Impact Analysis*

| Restarint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and qualification costs | -1.4% | Global, particularly affecting smaller players | Long term (≥ 4 years) |

| Export-control (ITAR/EAR) complexities | -0.8% | US-centric, affecting international partnerships | Medium term (2-4 years) |

| Legal liability over active-debris-removal missions | -0.6% | Global, regulatory uncertainty | Long term (≥ 4 years) |

| Lack of open interface standards for servicing ports | -0.5% | Global, industry standardization needed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Development and Qualification Costs

Space-qualified components required extensive radiation testing, fault-tolerant design, and niche manufacturing, inflating non-recurring engineering expenses. Smaller entrants faced capital hurdles exceeding USD 50 million before first revenue, limiting new competition.[3]Source: Aerospace America, “Expanding the final frontier with robots,” aerospaceamerica.aiaa.org Government cost-sharing grants alleviated some burden, yet long design cycles still restrained near-term market acceleration.

Export-Control Complexities

Despite recent US reforms, International Traffic in Arms Regulations continued to require detailed licensing for space robotics hardware. Multinational projects often experienced month-long approval processes that delayed integration schedules. Partners outside the United States sought ITAR-free subsystems, fragmenting supply chains and increasing qualification testing redundancies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Manipulator Systems Maintain Revenue Leadership

Robotic arms dominated 2025 revenue, generating 41.72% of total sales from critical station maintenance and satellite capture assets. The space robots market size for manipulator systems is forecast to expand steadily through 2031 on the back of the Canadarm3 program. Complex joints, multi-sensor end-effectors, and radiation-hardened electronics supported premium pricing. Growth also stemmed from planetary rovers using lightweight arm variants to collect regolith and deploy instruments.

On-orbit servicing vehicles posted the quickest 9.33% CAGR outlook, reflecting operator interest in modular spacecraft hosting robotic arms and refueling pods. Service providers secured anchor customers through multi-year performance-based contracts, signaling confidence in pay-per-thrust business models. Gripping and docking mechanisms gained traction as agencies converged on standard interfaces, while emerging concepts such as surgical robots aboard the ISS captured niche R&D budgets.

By Mission Type: Near Space Dominance with Deep Space Momentum

Near-space activities within Earth’s gravitational sphere attained a 65.12% market share in 2025 thanks to high satellite density and immediate revenue opportunities. Robust demand for inspection, relocation, and station upkeep kept fleet operators focused on reliable robotic assets. As governments prioritize orbital safety, the market share for space robots for near-space platforms will remain elevated through mid-decade.

Deep-space missions recorded a smaller base but posted a leading 9.86% CAGR forecast. Investments in autonomous navigation, radiation-tolerant actuators, and adaptive AI allowed spacecraft to operate with longer communication delays. NASA’s Mars Ascent Vehicle program advanced reinforcement-learning algorithms for off-world ascent guidance. ESA’s 2028 ExoMars Rosalind Franklin rover and China’s sample-return initiatives defined sustained demand for sophisticated robotic explorers.

By Application: Servicing Leads While Debris-Removal Surges

Satellite servicing held 48.35% of 2025 revenue because fleet operators viewed life extension as cheaper than replacement. The space robots market size for servicing solutions is projected to post steady gains through dedicated life-extension contracts. Active debris removal, although nascent, achieved the fastest 11.92% CAGR projection after Astroscale’s ADRAS-J fly-around demonstration in July 2024. Agencies and insurers are increasingly considering regulatory measures that may soon mandate debris-mitigation services.

On-orbit assembly grew alongside in-space manufacturing proofs such as ESA’s Metal 3D Printer on the ISS. Exploration and scientific research applications retained stable budgets through planned planetary missions. Cargo and logistics robotics registered rising venture interest as commercial lunar operations crystallized.

By End User: Public Sector Still Dominant, Commercial Gains Pace

Governments captured a 69.05% market share in 2025, reflecting the historic dominance of space exploration budgets. Space agencies funded flagship lunar infrastructure, while defense organizations procured inspection and surveillance robots. The market size for space robots for government programs will grow steadily, yet the absolute share is set to decline marginally as commercial entities scale.

Commercial operators posted the 10.22% CAGR, supported by geostationary satellite owners adopting service contracts and NewSpace startups deploying micro-satellites. Research institutes partnered with agencies to test novel mobility concepts, while venture-backed startups such as GITAI raised USD 129 million to commercialize cost-effective arms. Market sentiment indicated a growing appetite for risk-sharing models, accelerating private technology validation.

By Component: Hardware Commands Spend, Software Drives Innovation

Hardware comprised 71.88% of 2025 sales, reflecting material-intensive structural, actuator, and sensor systems. The space robots market share for hardware remained high because qualified components demand premium margins. Composite booms, radiation-hardened processors, and redundant electromechanical joints dominated procurement budgets.

Software generated smaller revenue but delivered the highest 11.08% CAGR. AI-based autonomy stacks enabled spacecraft to evaluate contingencies without ground intervention. India’s Chandrayaan-3 landing sequence, guided by onboard machine-learning vision algorithms, highlighted the software’s rising mission-critical role. Sensor-fusion frameworks combined lidar, optical, and inertial data, while secure middleware managed time-sensitive commands over constrained bandwidth links.

Geography Analysis

North America retained a 55.97% market share in 2025, supported by NASA’s Artemis contracting pipeline and a vibrant commercial launch ecosystem. In June 2025, SpaceX secured a USD 843 million contract to build an ISS deorbit vehicle. Canadian expertise in robotic manipulators, anchored by MDA Space’s Canadarm heritage, further reinforced regional leadership.

Asia-Pacific sustained strong double-digit growth as China funded six-legged asteroid-mining robots to cut reliance on terrestrial rare metals. Japan’s JAXA awarded GITAI a concept study for a lunar rover arm in April 2025. India prepared its next generation of autonomous lunar rovers, while Australian startups explored robotic regolith processing, collectively widening the regional supplier base.

The Middle East and Africa region achieved the fastest 11.78% CAGR outlook. The UAE advanced sovereign AI-enabled spacecraft through state-backed programs, including secure communication contracts worth USD 5.1 billion. The African Space Agency, inaugurated in Cairo in May 2025, coordinated continental R&D objectives for satellite production and orbital debris management.

Europe maintained stable expansion, supported by ESA’s PERASPERA initiative, which pooled EU funding for modular servicing vehicles and dexterous manipulators. Regulatory clarity under the EU Space Law proposal bolstered investor confidence in cross-border robotics projects. Cooperative missions such as Hera, targeting asteroid-deflection rehearsals with robotic probes, underscored the region’s emphasis on planetary defense.

South America represented an early-stage opportunity. Brazil renewed discussions with ESA on hosting autonomous robotic testbeds at the Alcântara launch site, yet funding constraints limited near-term deliveries. Emerging public-private consortia signaled intent to participate once launch prices ease.

Regulatory Landscape

Space-robotics deployments sit across space safety rules, mission authorization, and national licensing for communications and launch. In the United States, the Office of Space Commerce (OSC) released an updated mission-authorization proposal in March 2026, including a voluntary Space Commerce Certification concept aimed at novel activities such as satellite servicing, in-space manufacturing, and lunar operations. This move toward a more unified, interagency approach interacts with established licensing touchpoints (notably the FCC for spectrum and the FAA for launch and reentry), shaping how servicing and inspection robotics are approved and how compliance evidence is packaged.

In Europe and multilaterally, sustainability requirements are tightening around debris and end-of-life outcomes, which in turn affects robotic design choices. ESA updated its Space Debris Mitigation Policy and Requirements in February 2026 (ESSB-ST-U-007, Issue 1, Rev. 1), strengthening expectations for end-of-life servicing or removal for objects in protected regions. At the EU level, the proposed EU Space Law (COM/2025/335) includes provisions such as Article 101 that call for spacecraft to be equipped with dedicated interfaces for in-space servicing, reinforcing the shift toward design-for-servicing and more standardized physical interfaces.

Value Chain Analysis

The space robots value chain begins with specialized materials and space-grade components, including radiation-tolerant electronics, sensors and vision stacks, actuators, mechanisms, and power subsystems. It then moves through subsystem integration, covering manipulators, end-effectors, docking and grappling devices, and autonomy software, followed by spacecraft bus integration and system-level qualification. Prime contractors and established aerospace manufacturers typically anchor final integration and verification, while niche suppliers provide dexterous joints, robotics software frameworks, and capture mechanisms. Downstream, launch providers and in-orbit operators enable deployment, and mission operations, ground control software, and on-orbit servicing workflows (inspection, rendezvous and proximity operations, capture and refuel or relocation, or assembly tasks) complete value delivery.

Recent moves highlight both ecosystem partnering and bottleneck risks. In September 2024, Momentus and Lodestar Space agreed to integrate a modular robotic arm on a Vigoride Orbital Service Vehicle, showing how in-space transport platforms are being paired with robotics payload providers. On the exploration and station side, MDA Space joined the Starlab Space joint venture in May 2024 to contribute external robotics and robotics mission operations, reflecting the linkage between commercial stations and robotics demand. At the same time, industrial-base constraints and supplier concentration for critical subsystems remain a constraint, illustrated by Rocket Lab closing its acquisition of Mynaric in April 2026, reducing the pool of independent suppliers for space-qualified optical terminals used across modern spacecraft architectures.

Competitive Landscape

The competitive field featured a blend of heritage aerospace firms and venture-backed specialists. Northrop Grumman, MDA Space, and Lockheed Martin leveraged decades of flight heritage and longstanding customer trust to secure flagship contracts such as NASA’s OSAM-2 architecture. Their vertically integrated production lines supported high-reliability subsystems.

Mid-size innovators targeted niche services. Astroscale specializes in debris-capture and secured a critical design review for OneWeb cleanup in June 2025. Starfish Space signed Intelsat for a 2026 life-extension mission, validating pay-per-maneuver economics. GITAI opened a US defense subsidiary to access classified opportunities, highlighting the strategic value of local presence.

Technology differentiation centered on autonomy. Apptronik partnered with Google DeepMind to embed large-language-model reasoning in humanoid robots to reduce teleoperator workload. Standardized docking interfaces emerged as a white-space opportunity, as inconsistent ports hindered multi-vendor cooperation. Startups promoting open standards sought early-mover advantages in servicing interoperability.

Investment dynamics favored dual-use capabilities that attracted both civil and defense customers. DARPA’s Robotic Servicing of Geosynchronous Satellites program remained a bellwether for advanced inspection and manipulation technologies. Private equity funds monitored upcoming regulatory decisions requiring debris-removal compliance, potentially unlocking recurring revenue akin to compulsory aircraft maintenance.

Space Robots Industry Leaders

Northrop Grumman Corporation

Lockheed Martin Corporation

Maxar Technologies Holdings Inc.

Astroscale Holdings Inc.

MDA Space Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is building around practical, repeatable robotics capabilities that lower the cost and risk of servicing, assembly, and manufacturing in orbit. Regulatory and agency signals are pushing design-for-servicing, and that increases the value of standardized capture points, grappling fixtures, and modular interfaces that allow multi-vendor servicers to operate across satellite fleets. With satellite replacement costs often cited above USD 400 million for GEO assets, commercial life-extension and inspection missions support a business case for robotic rendezvous, docking, and manipulation systems, while debris-related policy pressure increases attention on removal and end-of-life solutions that depend on reliable capture and containment robotics.

In-space manufacturing and on-orbit assembly also create an opportunity lane as government programs de-risk core technologies even after high-profile program resets. NASA discontinued OSAM-1 in March 2024 due to cost, schedule, and technical challenges, but adjacent efforts continue to mature enabling building blocks. In early 2025, DARPA advanced its NOM4D program into Phase 3 to run orbital demonstrations, and research teams have executed in-space and ISS-based demonstrations tied to autonomous robotic construction and precision forming. Examples include a Caltech autonomous robotic construction demonstration aboard a Momentus Vigoride vehicle in February 2026, and a University of Illinois Urbana-Champaign composite-forming demonstration in the ISS Bishop Airlock module in April 2026 via a NASA commercial resupply mission. Collectively, these activities concentrate demand on robotic manipulation, metrology, digital-twin-enabled quality control, and collision-avoidance autonomy for free-flying and modular configurations, reinforcing a product roadmap around interfaces, autonomy software, and flight-proven manipulation hardware.

Recent Industry Developments

- May 2026: Northrop Grumman reported its Mission Robotic Vehicle (MRV) is in final testing at its Dulles, Virginia facility, with a summer 2026 SpaceX launch campaign planned to deliver GEO refueling and life-extension services. The update reflects a shift from prototype servicing concepts to an operational platform model that couples a servicer bus with robotic capabilities for recurring satellite-operator use cases.

- June 2025: Northrop Grumman integrated the MRV robotics payload, including twin robotic arms developed by the U.S. Naval Research Laboratory (NRL), onto the spacecraft bus. Completing payload integration reduces downstream test and integration risk and helps lock in key interfaces between dexterous manipulators, guidance, navigation and control, and proximity-operations software.

- October 2024: Lockheed Martin completed its acquisition of Terran Orbital to strengthen manufacturing, automation, and robotics capabilities for modular spacecraft platforms. The deal broadens in-house capacity for producing spacecraft that can host robotic payloads and supports faster iteration cycles for missions spanning Earth orbit and cislunar activity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from space robots used to perform tasks in orbit or on planetary surfaces, where robotic systems replace or support human activity in harsh space conditions.

Scope exclusions: We do not count ground-only test rigs, lab prototypes that are not flight-ready, or consumer and educational robotics kits.

Segmentation Overview

- By Product

- Rovers/Spacecraft Landers

- Robotic Arms/Manipulator Systems

- Space Probes

- Gripping and Docking Systems

- On-Orbit Servicing Vehicles

- Others Products

- By Mission Type

- Deep Space

- Near Space

- By Application

- Satellite Servicing and Life Extension

- Active Debris Removal

- On-Orbit Assembly and Manufacturing

- Exploration and Scientific Research

- Cargo and Logistics

- By End-User

- Commercial

- Commercial Satellite Operators

- Research Institutes

- NewSpace Start-ups

- Government

- Space Agencies

- Defence and Intelligence

- Commercial

- By Component

- Hardware

- Manipulators

- Structural and Mobility Platform

- Sensor and Vision Systems

- Power Subsystems

- Commuincation System

- Software

- Autonomy and Navigation Software

- Sensor Fusion and Data Processing

- Commuincation and Data Management Software

- Others

- Hardware

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- Israel

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the demand pool and the mission pipeline, then linking it to what can be priced and delivered as a space robot. We refer to public sources such as NASA mission and procurement pages, ESA program publications, and national space agency budget documents to understand where programs receive funding and what gets contracted.

To avoid building the model from press headlines alone, we also check satellite and launch activity series from sources such as the FAA Office of Commercial Space Transportation, UN and ITU satellite registries where applicable, and customs or trade statistics where space-grade components show up in a consistent way. Company annual reports, investor presentations, and reputable aerospace press are used to validate what was shipped, what was delayed, and how revenue is recognized across programs. In parallel, we use paid subscriptions for company financials and intelligence, plus patent databases and a global contracts and tenders feed, so the model can be anchored to observable deal flow and technology readiness. The sources listed here are illustrative, and many other public references were used during data collection and clarification.

Primary Interviews and Surveys

Primary calls and surveys are used to test what desk sources cannot confirm well, such as how robotics content is split across the spacecraft bill of materials, and what portion is counted as robotics versus adjacent avionics or payload hardware. We spoke with a mix of manufacturers, subsystem suppliers, integrators, mission operators, and program stakeholders across major space economies, so assumptions on pricing, delivery schedules, and adoption rates could be adjusted before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 48% |

| Mid tier: 58% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 15% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where space program outlays, mission counts, and servicing activity are translated into a robotics demand pool, then filtered through what qualifies as a space robot under this scope. We corroborate the totals with selective bottom-up approximations, such as sampled program awards, typical unit pricing by robot class, and channel checks on delivered subsystems, which helps tighten the final number without assuming perfect visibility.

Key inputs used in the model include the annual cadence of launches and on-orbit missions, the mix of mission types that require manipulation or mobility, the rate of satellite servicing and inspection activity, typical robot payload mass and complexity, and observed pricing changes as autonomy and radiation-hard components mature. When a program is not fully disclosed, the gap is handled with conservative proxying based on comparable missions and confirmed component content ranges, then reviewed again during interviews.

For forecasting, scenario analysis is applied because timelines are sensitive to mission slips, policy changes, and procurement cycles. These shifts can move revenue between years without changing long-term demand. Assumptions are reviewed with experts so the scenario weights reflect realistic adoption of on-orbit servicing vehicles, rover deployments, and robotic arm upgrades.

Data Validation & Update Cycle

Outputs are checked against independent signals like reported mission schedules, procurement announcements, and aggregate space budget direction, so the results stay aligned with what is actually funded and flying. When a value looks out of pattern, it is traced back to its drivers, and the assumptions are re-checked through follow-up outreach or additional public confirmation.

Before sign-off, the model goes through multi-step analyst review, where calculations, unit economics, and year alignment are verified, and any large variances are documented. The report is refreshed annually, and interim updates are made when material events occur, such as major contract awards, mission cancellations, or policy shifts. Right before delivery, a final pass is completed so clients receive the latest view that matches the most recent public and interview inputs.

Mordor Intelligence's Space Robots Market Size Compared With Other Published Estimates

Published market sizes for space robots can vary even when they use similar labels, since firms often draw the line differently between flight hardware, software, services, and ground infrastructure. Differences also come from which year is treated as the anchor, how mission delays are handled, and whether pricing is updated with recent contract and component cost signals.

The benchmark table shows a spread that is mainly tied to scope and timing. In Mordor Intelligence's model, only revenue tied to space-qualified robotic systems used in orbit or on celestial bodies is counted, which leaves out ground-only test platforms and consumer kits that can inflate totals in broader definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.93 B (2026) | |

| Global Consultancy A | USD 5.04 B (2024) | Uses a 2024 base and a different year mapping of mission deliveries, which can shift revenue earlier, and it groups on-orbit manufacturing with robotics in ways that may overstate robot-specific value in mixed payload budgets. |

| Trade Journal B | USD 4.94 B (2024) | Relies on a broader component taxonomy and older program timelines, so some robotic subsystems are blended with general spacecraft equipment, and currency timing plus slower price refresh can keep the value lower for later years. |

Taken together, the comparison suggests that the largest drivers are the year used for the headline number and the inclusion rules for what counts as robotics versus adjacent spacecraft equipment. By keeping the demand pool tied to mission activity and then cross-checking with sampled awards and expert feedback, the estimate stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What was the size of the space robots market in 2026?

The market reached USD 5.93 billion in 2026.

What return on investment can a satellite operator expect from on-orbit servicing contracts?

Life-extension services commonly defer USD 400 million replacement costs for five to seven years, producing payback periods under two years for GEO fleet owners that spend USD 50–100 million per servicer mission.

Which robotic technologies are most likely to reach Technology Readiness Level 9 by 2028?

Autonomous manipulator arms qualified for the lunar Gateway and standardized grappling fixtures for GEO servicing vehicles are already at TRL 7–8 in 2025 and are scheduled for flight validation on commercial missions before 2028.

Which region is expanding most rapidly?

The Middle East and Africa are forecasted to grow at a 11.78% CAGR due to recent national space programs.

Which workforce skills will be most constrained over the next five years?

Deep-space autonomy software engineers, radiation-hardened avionics designers, and orbital dynamics specialists remain in short supply, with projected demand outpacing the current talent pool by at least 20% through 2030.

How should space insurers adjust risk models for missions that rely on autonomous servicers?

Actuarial teams increasingly apply a 5–10% premium discount when operators use flight-proven docking interfaces and redundancy-rich robotic arms, yet add a surcharge if debris-removal tasks involve uncooperative tumbling objects.

Page last updated on: