Space Batteries Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

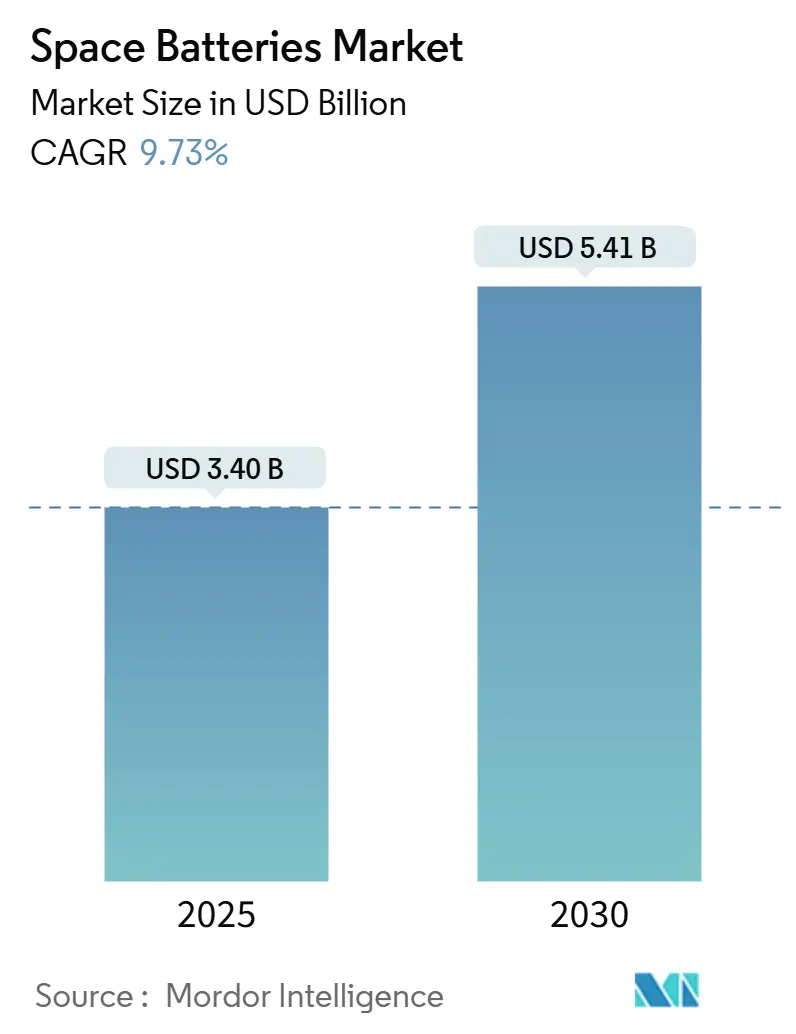

| Market Size (2025) | USD 3.40 Billion |

| Market Size (2030) | USD 5.41 Billion |

| Growth Rate (2025 - 2030) | 9.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Batteries Market Analysis by Mordor Intelligence

The space batteries market size stands at USD 3.40 billion in 2025 and is forecasted to reach USD 5.41 billion in 2030, reflecting a 9.73% CAGR. Space-grade lithium-ion (Li-ion) technology dominates the value mix, while deep-space programs and small-satellite constellations spur volume growth. Sustained public funding, illustrated by NASA’s FY 2025 Space Technology budget of USD 1.18 billion, anchors near-term demand, and rising qualification of radiation-hardened solid-state chemistries extends the long-term growth runway.[1]Source: National Aeronautics and Space Administration, “FY 2025 Budget Request,” NASA.GOV Platform builders increasingly favor batteries above 200 Wh/kg to trim launch mass, and suppliers respond with vertically integrated lines to stabilize lead times. Regional spending profiles diverge: North America prioritizes lunar infrastructure, Europe accelerates GEO telecom refresh cycles, and Asia-Pacific invests in cost-optimized LEO fleets. At the same time, supply-chain pressure on lithium and cobalt and stricter ECSS test matrices temper near-term margin expansion.

Key Report Takeaways

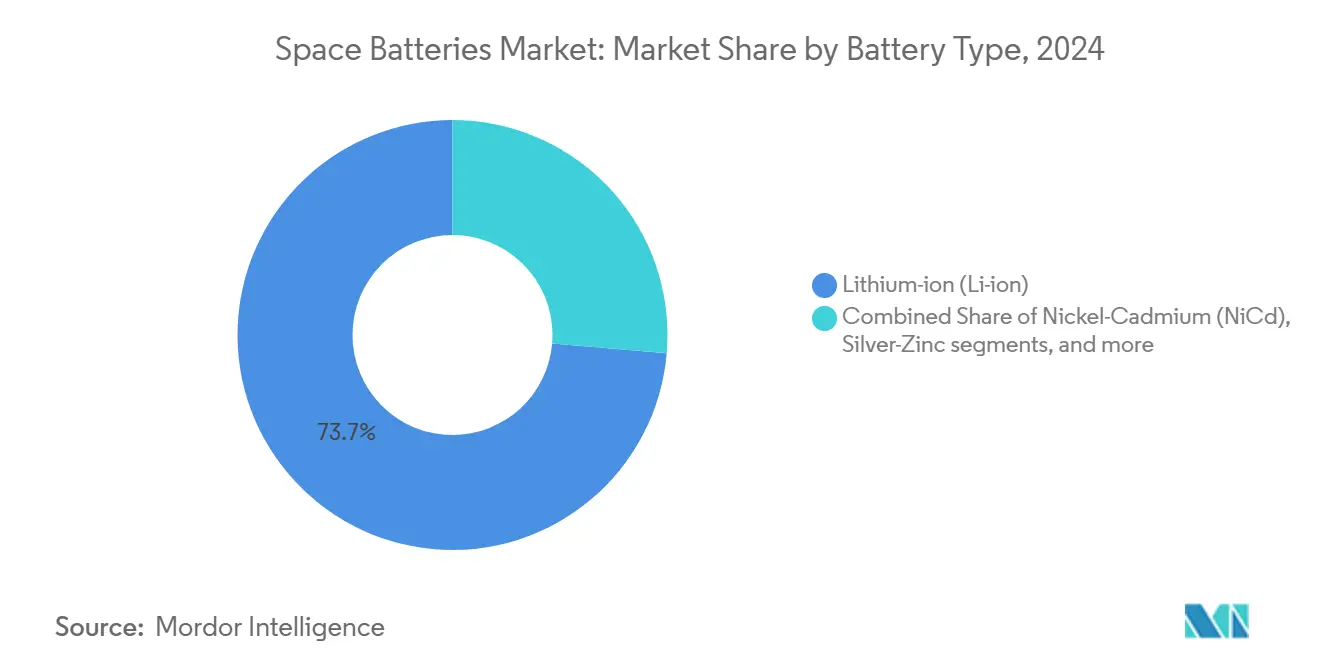

- By battery type, Li-ion led with 73.65% revenue share in 2024; solid-state and lithium-metal are projected to post the fastest 15.60% CAGR through 2030.

- By platform, satellites commanded a 67.80% share of the space batteries market size in 2024, while planetary landers and rovers are expected to advance at a 13.40% CAGR to 2030.

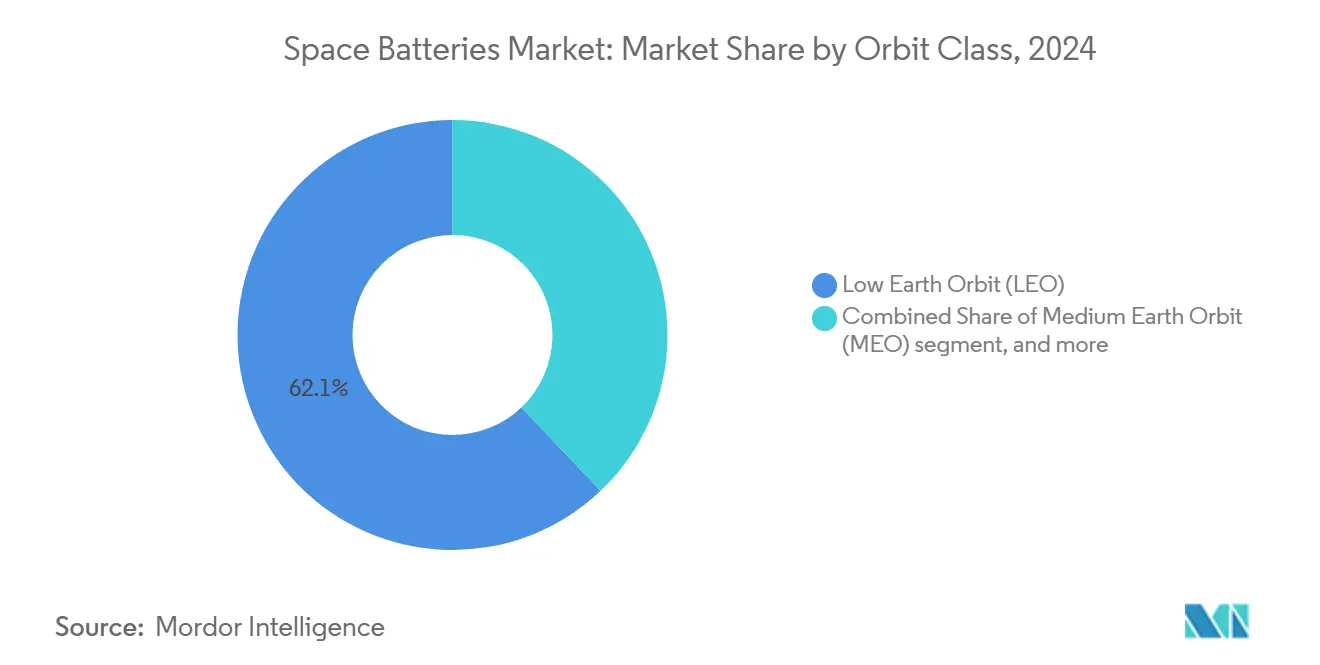

- By orbit class, LEO captured 62.10% of the space batteries market share in 2024; deep-space and interplanetary applications record the highest 14.60% CAGR.

- By energy-density band, 100-200 Wh/kg systems held 53.20% share in 2024; batteries above 200 Wh/kg are forecasted to expand at a 13.15% CAGR.

- By function, secondary rechargeable units accounted for 78.62% of the space batteries market size in 2024 and will grow at a 10.54% CAGR.

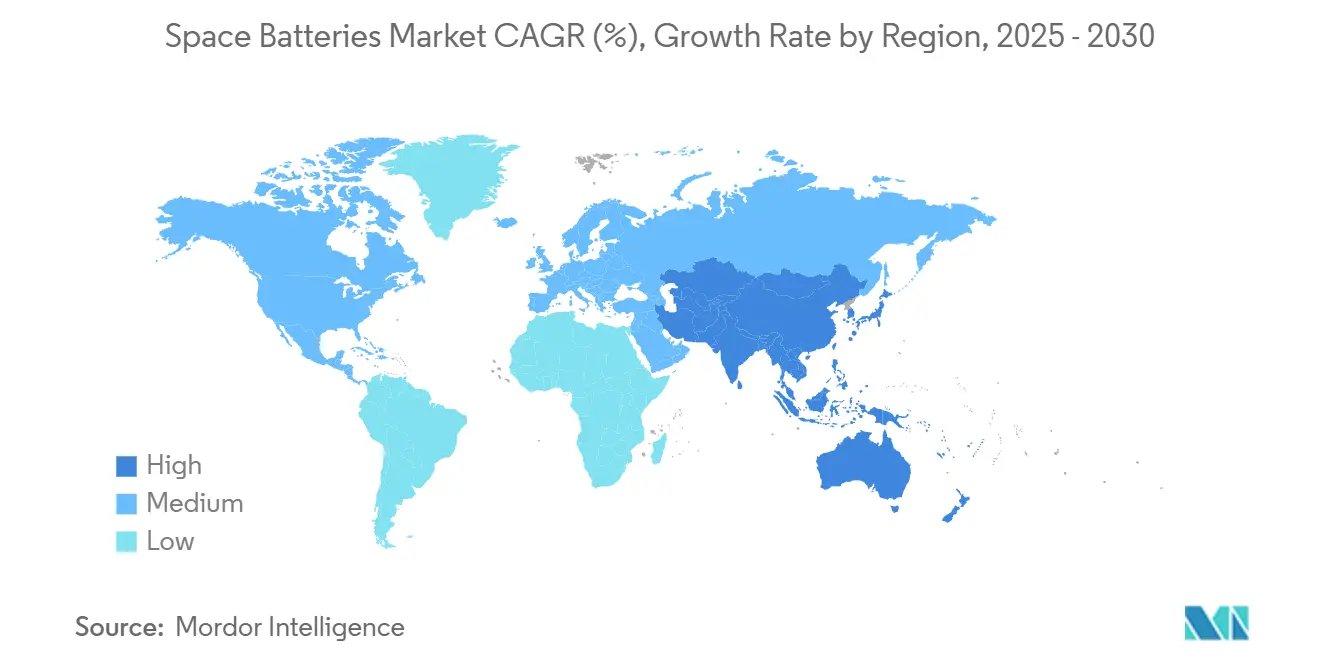

- By geography, North America retained a 37.90% share in 2024, whereas the Asia-Pacific is on course for the quickest 12.65% CAGR through 2030.

Global Space Batteries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid proliferation of small-satellite constellations | +2.1% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Migration from nickel-hydrogen to high-energy-density Li-ion chemistries | +1.8% | Global | Short term (≤ 2 years) |

| Government-funded deep-space and lunar missions demanding ultra-long cycle life | +1.5% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| On-orbit servicing and manufacturing creating recharge-intensive duty cycles | +1.2% | North America and Europe | Medium term (2-4 years) |

| Qualification of solid-state batteries for radiation environments | +1.0% | Global | Long term (≥ 4 years) |

| AI-enabled health-diagnostics extending battery lifetime | +0.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid proliferation of small-satellite constellations

Constellation operators require batteries that maintain more than 80% capacity after 50,000 cycles, translating into demand for standardized 18650 and 21700 lithium-ion cells specially ruggedized for space. Higher launch cadences compress procurement windows, so buyers gravitate toward suppliers with automated build-to-print lines and existing flight heritage. Volume orders improve economies of scale, allowing integrators to prioritize cost-per-watt rather than absolute price. Cold-temperature charge acceptance remains a key differentiator because LEO buses experience frequent eclipse transitions. Compliance with ECSS-E-ST-20-20C remains non-negotiable, placing the onus on vendors to maintain deep data packages.

Migration from nickel-hydrogen to high-energy-density Li-ion chemistries

Switching from legacy nickel-hydrogen to Li-ion reduces battery mass by up to 40%, freeing space for payloads or propellants. GEO telecom operators maximize revenue by launching heavier transponders within existing fairing envelopes, while government programs shorten mission timelines through lighter transfer stages. Li-ion also maintains capacity across an extended −20 °C to +50 °C window, reducing heater loads and simplifying thermal control. Flight data confirms sub-2% capacity loss after 13 years in GEO orbit, reinforcing operator confidence. As a result, historic nickel-hydrogen lines are shuttered, and component vendors are pivoting resources to advanced anode materials.

Government-funded deep-space and lunar missions demanding ultra-long cycle life

Artemis, Gateway, and Mars Sample Return missions need batteries that can survive five-year dormancy and re-activate in a −150 °C to +200 °C range. Agencies co-fund solid-state and lithium–sulfur (Li-S) R&D to reach 400 Wh/kg without flammable electrolytes. Test campaigns involve multiple thermal-vacuum chambers executing 3× the number of cycles required for LEO acceptance, and only suppliers with space-grade manufacturing controls can absorb the cost. Qualification timelines that exceed 24 months favor incumbents with proven deep-space flight heritage, particularly those with in-house vibration and radiation test assets.

On-orbit servicing and manufacturing creating recharge-intensive duty cycles

Robotic refueling tugs and in-space additive manufacturing platforms draw high peak currents, then demand rapid recharge as they transit sunlit arcs. Designs integrate advanced battery management software that adjusts charge cut-off voltage based on real-time thermal maps, extending usable life. The duty cycle also boosts demand for cell-level fusing and modular pack formats that simplify replacement during servicing. Thermal dissipation becomes central because the vacuum environment eliminates convective cooling; suppliers address this through embedded heat pipes and high-conductivity aluminum casings.

Restraints Impact Analysis*

| Restarint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent radiation and thermal qualification inflating cost and lead-time | -1.4% | Global | Short term (≤ 2 years) |

| Supply-chain dependence on space-qualified lithium cells and raw materials | -1.1% | Global, acute in Europe and smaller markets | Medium term (2-4 years) |

| High R&D and certification costs limiting new entrants | -0.9% | Global | Long term (≥ 4 years) |

| Looming PFAS bans squeezing advanced separator availability | -0.7% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent radiation and thermal qualification inflating cost and lead-time

ECSS and NASA standards oblige each battery design to prove performance at −40 °C to +60 °C under vacuum and withstand 100 krad or higher radiation exposure. End-to-end campaigns run 18-24 months and consume hundreds of cells, locking several million dollars of non-recurring cost into the program. Delays ripple through launch manifests and tie up test facility capacity, particularly shaker tables and gamma irradiation rooms. The burden deters startups and cements the position of incumbents with large qualification datasets.

Supply-chain dependence on space-qualified lithium cells and raw materials

Only a handful of certified lines output space-rate Li-ion cells, and most rely on nickel and cobalt extracted or refined in a narrow set of geographies. A price spike or export restriction can disrupt fixed-price satellite contracts, compressing margins for integrators and battery suppliers. Upcoming PFAS restrictions may also force separator redesigns, triggering fresh qualification loops and temporary shortages of compliant material. European programs feel the most pressure because they balance Buy-Europe mandates with limited domestic raw-material processing capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Energy-Dense Lithium-ion Retains the Lead While Solid-State Gains Traction

Li-ion occupied 73.65% of the space batteries market share in 2024, reflecting decades of operating data and manufacturing yield improvements. Flight heritage approaching 620 million cell-hours underpins procurement confidence, and high-nickel NCA and NCM blends now deliver 214 Wh/kg at pack level.[2]Source: Saft, “Taking Space Power to the Next Generation,” SAFT.COM The segment also benefits from mature supply chains spanning electrode foil to custom pressure vessels. The space batteries market size tied to solid-state and lithium-metal chemistries will accelerate at a 15.60% CAGR, driven by mission profiles that prize 400 Wh/kg specific energy and intrinsic resistance to thermal runaway. Nickel-cadmium (NiCd) and nickel-hydrogen (NiH2) systems survive in niche environments—particularly where −60 °C storage or unlimited trickle-charge endurance outweigh mass savings. Meanwhile, silver-zinc retains relevance for launch vehicles that need burst power at ignition and stage separation.

Momentum toward solid-state hinges on scaling sintered ceramic electrolytes to satellite-grade formats without cracking and demonstrating cycle life beyond 1,000 cycles. Leading suppliers pair solid-state stacks with flex-rigid battery management boards to mitigate micro-vibration-induced delamination. Funding from public agencies offsets early yield losses, but the complete transition will span the forecast horizon. Over the period, hybrid packs combining Li-ion strings for baseline loads and emerging chemistries for peak draws will proliferate.

By Platform: Satellites Drive Volume While Planetary Landers Command Premium Growth

Satellites accounted for 67.80% of the space batteries market share in 2024, reflecting their position as the core volume driver of the sector. Standardized battery requirements and large-lot manufacturing allow constellation operators to achieve a favorable cost per watt-hour, particularly for fleets such as SpaceX, OneWeb, and Amazon’s Project Kuiper that plan thousands of launches together. Typical satellite buses integrate 50–200 Wh battery systems to handle rapid eclipse cycling and tight mass budgets, giving qualified Li-ion chemistries a decisive edge in procurement contests. Volume demand also enables suppliers to amortize the high non-recurring engineering costs of ECSS qualification, lowering unit prices for follow-on orders. Launch vehicles form a smaller but technically demanding sub-segment that needs burst-power packs for ignition and stage separation. In contrast, crewed spacecraft and space stations specify human-rated batteries with redundant safety circuits and pressure-relief features to meet stringent flight-worthiness rules.

Planetary landers and rovers represent the fastest-growing platform class, advancing at a 13.40% CAGR through 2030 as Artemis-linked lunar assets and Mars reconnaissance craft move from concept to hardware. These missions require multi-kWh arrays capable of remaining dormant for years, then activating flawlessly in environments spanning −150 °C nights to dust-filled noon highs above 100 °C. Qualification campaigns include extended thermal-vacuum soaks, vibration to simulate launch and landing shocks, and radiation testing beyond deep-space cruise levels to secure mission assurance where repair is impossible. Mitsubishi Electric’s award to supply Li-ion batteries for NASA’s Gateway lunar platform underscores how premium, radiation-hardened packs reshape supplier portfolios. As planetary exploration broadens, battery vendors that demonstrate heritage on landers and rovers can command higher margins even as the wider space batteries market size scales with satellite volumes.

By Orbit Class: LEO Remains Core, Deep-Space Spurs Innovation

The space batteries market recorded a 62.10% share in LEO deployments during 2024, spurred by broadband and Earth-observation networks that value cost per watt-hour above all. Those fleets tolerate state-of-charge windows down to 20% during eclipse to frequent ground passes. Though fewer in number, deep-space craft prompt radical design leaps: cells must shrug off galactic cosmic rays and handle wide temperature swings without convective cooling. The segment’s 14.60% CAGR reflects new Artemis cargo landers and sample-return vehicles.

MEO navigation platforms require enhanced radiation shielding and low self-discharge to preserve clock stability. GEO com-sat batteries face prolonged eclipses lasting up to 72 minutes; thus, Li-ion strings adopt thicker current collectors and high-temperature binders. As spacecraft shift from chemical to electric propulsion, battery peak power demands rise, encouraging adoption of higher voltage architectures.

By Energy-Density Band: Mid-Range Dominates; More than 200 Wh/kg Segment Surges

Batteries between 100 Wh/kg and 200 Wh/kg provided 53.20% of 2024 shipments, balancing reliability and cost. Designs draw on mature 18650 and 21700 cells repackaged into welded aluminum enclosures with dual-redundant pressure-relief valves. The greater than 200 Wh/kg tier, projected to post a 13.15% CAGR, stakes its appeal on mass savings that translate into heavier payloads or extra propellant. Development emphasis falls on silicon-rich anodes and high-nickel cathodes stabilized by advanced separators free from PFAS compounds where feasible.

Sub-100 Wh/kg packs serve sounding rockets and re-entry capsules that confront extreme thermal shocks. Even so, the broader market expects to cross the 300 Wh/kg threshold in pilot flights by 2028 as sintered solid electrolytes and lithium–sulfur variants mature.

By Function: Secondary Batteries Dominate Long-Life Missions

Secondary rechargeable systems captured 78.62% of 2024 revenue because most spacecraft require thousands of eclipse cycles. Slow calendar aging and robust state-of-health algorithms underpin 10.54% CAGR through 2030. The Space Batteries industry concentrates its R&D budgets on silicon-based anodes that reduce swelling and extend calendar life beyond 15 years.

Primary batteries remain indispensable for launch vehicles and planetary probes for one-time bursts. Silver-zinc modules achieve gravimetric power densities above 400 W/kg but suffer limited cycle life, confining them to expendable stages. Mission architects weigh the trade-offs carefully: a rising number of landers now select hybrid setups pairing primary packs for descent burns with rechargeable arrays for surface operations.

Geography Analysis

North America led the space batteries market with a 37.90% share in 2024. Its dominance stems from NASA’s consistent procurement pipeline and tier-one primes that collectively award multi-year battery contracts. Saft’s Jacksonville plant expansion to 5 GWh annual capacity underscores the region’s commitment to domestic cell supply.[3]Source: Electronics Specifier, “Saft Gears Up for Li-ion Battery Production in the Americas,” ELECTRONICSSPECIFIER.COM The Inflation Reduction Act adds investment credits that partially offset the cost of US-sourced cobalt and nickel intermediates. Canada supplies specialty thermal insulation blankets and pressure vessels, while Mexico machines non-flight ground-support fixtures.

Europe contributes a robust demand pool anchored by ESA flagship programs and telecom satellite renewals. French, German, and Italian subsidiaries of global battery groups run R&D centers focusing on ceramic solid-state stacks and Europe-specific PFAS-free separators. Compliance with REACH regulations, alongside emerging PFAS bans, will steer chemistry roadmaps toward fluorine-free binders. U.K. small-satellite builders amplify volume, whereas Eastern European suppliers provide casings and non-critical structural hardware.

Asia-Pacific posts the strongest 12.65% CAGR. India aligns with its target of a USD 44 billion space economy by 2033, leveraging public-private partnerships to erect cell assembly lines co-located with launcher integration facilities. Japan’s satellite manufacturers prefer domestically produced batteries, as evidenced by the contract to supply Li-ion packs for the Gateway platform. China’s vertically integrated ecosystem essentially serves national programs, but technology-transfer rules limit Western participation. South Korea advances pouch-cell coating methods adopted from its EV sector, and Australia funds laboratory-scale Li-S research aimed at lunar surface rovers.

Competitive Landscape

The market remains moderately consolidated. Saft, EaglePicher, GS Yuasa, and ABSL hold entrenched positions through long-standing flight heritage and vertically integrated lines. Saft reports more than 35,000 cells in orbit across 768 satellites, creating unrivaled reliability datasets. Competitive leverage centers on qualification speed, in-house radiation testing, and the ability to supply mixed chemistries under single contracts.

Investment patterns show incumbents broadening chemistries: Saft partners with French institutes on solid-state, and GS Yuasa adapts automotive silicon-anode technology to GEO packs. New entrants focus on narrow niches, such as solid-state for micro-sats or lithium–sulfur for deep-space, where smaller lot sizes mitigate qualification cost disadvantages. M&A remains selective; primes prefer long-term supply agreements over outright acquisitions to preserve multi-vendor resilience.

Pricing is 20–25% higher than terrestrial equivalents due to stringent screening and an acceptance campaign that can double component costs. Nevertheless, constellation buyers push for cost efficiencies via frame contracts covering thousands of packs, tipping negotiation power slightly toward large fleet operators. Future competition will hinge on mastering PFAS-free separators and demonstrating >300 Wh/kg in orbital service.

Space Batteries Industry Leaders

Saft Groupe SA

GS Yuasa Corporation

EnerSys

Airbus SE

EaglePicher Technologies, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: KULR Technology Group, Inc. launched six new commercial off-the-shelf (COTS) versions of its KULR ONE Space (K1S) CubeSat battery line, with capacities ranging from 100 to 500Wh. These batteries are designed to meet the growing demands of customers in the space sector and showcase the company's innovation in frontier technologies.

- December 2024: KULR Technology Group, Inc. announced plans to launch its KULR ONE Space (K1S) battery via Exolaunch on a SpaceX rideshare mission in 2026. This milestone aligns with KULR’s focus on advanced battery systems for the growing space battery market.

Global Space Batteries Market Report Scope

| Lithium-ion (Li-ion) |

| Nickel-Cadmium (NiCd) |

| Nickel-hydrogen (NiH2) |

| Silver-zinc |

| Solid-state/Lithium-metal |

| Other |

| Satellites |

| Launch Vehicles |

| Crewed Spacecraft and Space Stations |

| Planetary Landers and Rovers |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

| Deep-Space / Interplanetary |

| Less than 100 Wh/kg |

| 100–200 Wh/kg |

| More than 200 Wh/kg |

| Primary (Non-Rechargeable) |

| Secondary (Rechargeable) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Battery Type | Lithium-ion (Li-ion) | ||

| Nickel-Cadmium (NiCd) | |||

| Nickel-hydrogen (NiH2) | |||

| Silver-zinc | |||

| Solid-state/Lithium-metal | |||

| Other | |||

| By Platform | Satellites | ||

| Launch Vehicles | |||

| Crewed Spacecraft and Space Stations | |||

| Planetary Landers and Rovers | |||

| By Orbit Class | Low Earth Orbit (LEO) | ||

| Medium Earth Orbit (MEO) | |||

| Geostationary Orbit (GEO) | |||

| Deep-Space / Interplanetary | |||

| By Energy-Density Band | Less than 100 Wh/kg | ||

| 100–200 Wh/kg | |||

| More than 200 Wh/kg | |||

| By Function | Primary (Non-Rechargeable) | ||

| Secondary (Rechargeable) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Space Batteries market?

The Space Batteries market size is USD 3.40 billion in 2025 and is set to reach USD 5.41 billion by 2030, , reflecting a 9.73% CAGR.

Which battery type leads in satellite adoption?

Lithium-ion (Li-ion) holds 73.65% share thanks to high energy density and extensive flight heritage.

Which orbit class shows the fastest growth?

Deep-space and interplanetary missions post the highest 14.60% CAGR through 2030 as lunar and Mars programs expand.

Which region grows the quickest?

Asia-Pacific registers a 12.65% CAGR fueled by India’s expanding launch sector and Japan’s satellite manufacturing.

What is the main restraint hindering new suppliers?

Stringent radiation and thermal qualification can extend design cycles up to 24 months and add millions to development cost.

How are suppliers addressing PFAS regulations?

Vendors are testing fluorine-free separators and ceramic solid-state layers to meet upcoming environmental standards.

Page last updated on: