Space Propulsion Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

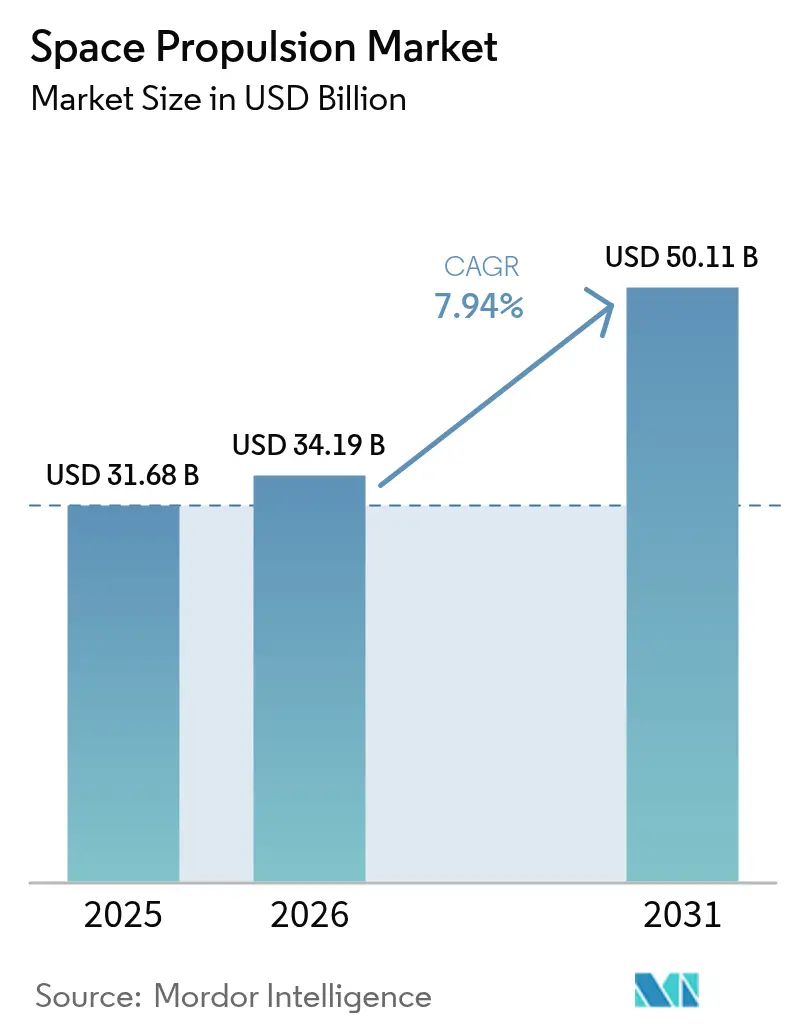

| Market Size (2026) | USD 34.19 Billion |

| Market Size (2031) | USD 50.11 Billion |

| Growth Rate (2026 - 2031) | 7.94% CAGR |

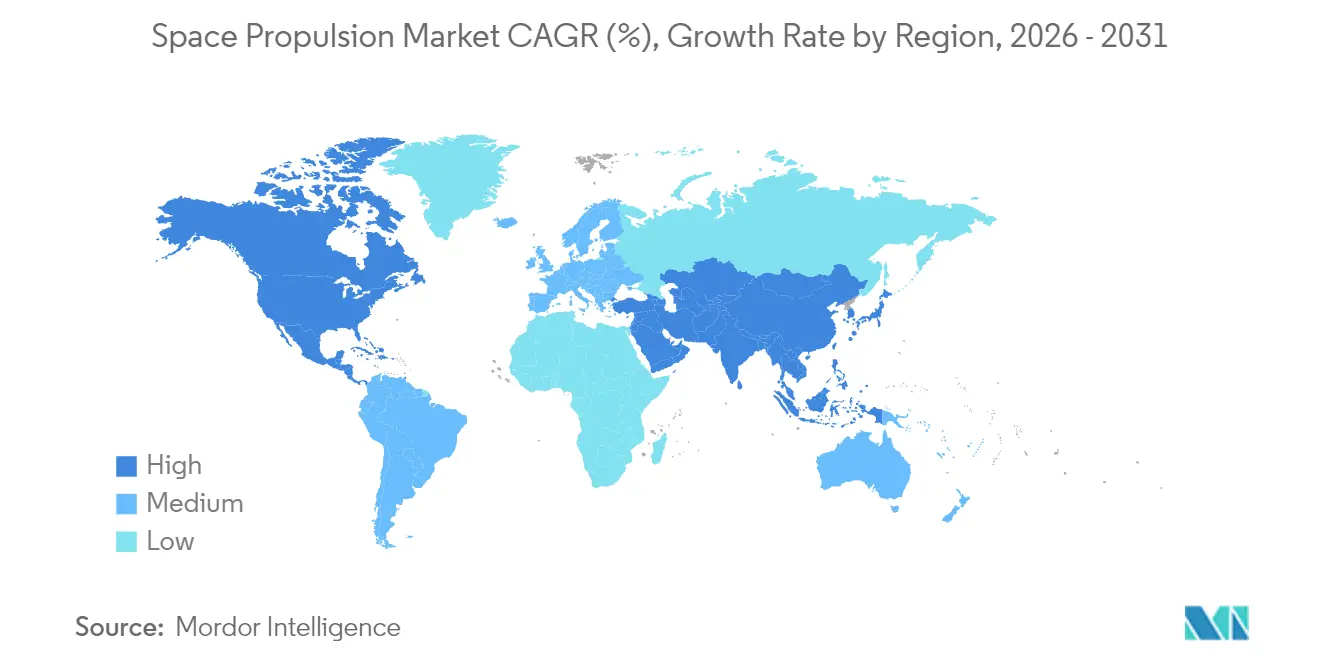

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

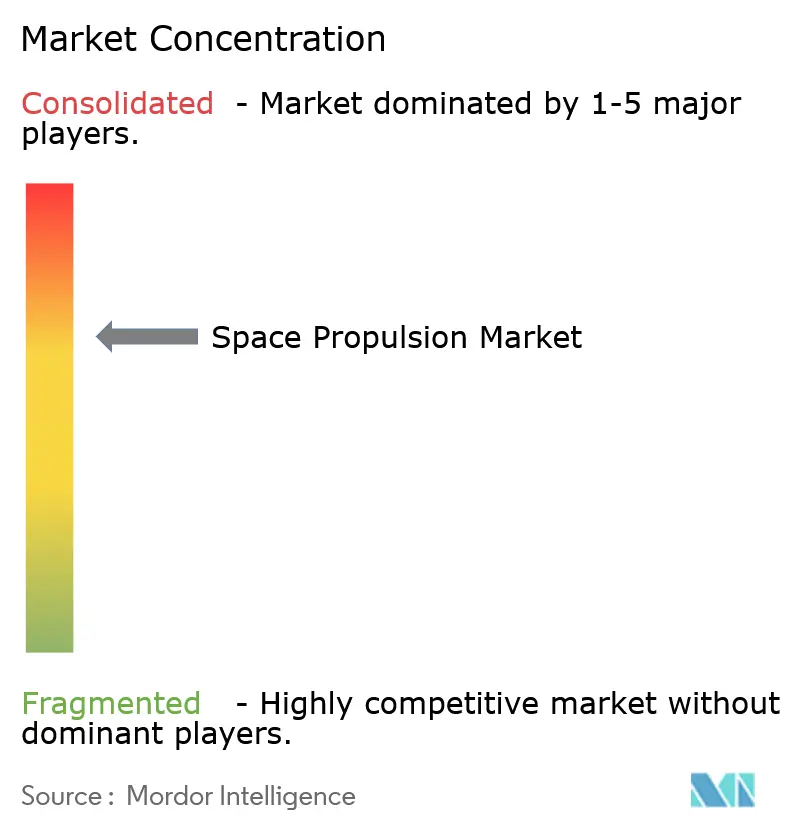

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Propulsion Market Analysis by Mordor Intelligence

The space propulsion market size in 2026 is estimated at USD 34.19 billion, growing from 2025 value of USD 31.68 billion with 2031 projections showing USD 50.11 billion, growing at 7.94% CAGR over 2026-2031. The expansion stems from three reinforcing forces: (1) large sovereign constellation programs that order propulsion systems in the hundreds, (2) private‐sector races to field crewed missions beyond low Earth orbit, and (3) the sharp drop in cost per launch enabled by reusable rockets. Demand flows from heavy-lift launchers, deep-space probes, small-satellite constellations, and the emerging logistics layer of space tugs, driving sustained capital investment in chemical, electric, and experimental nuclear engines. Technology procurement cycles now emphasize bulk orders of standardized modules, shorter integration schedules, and lifetime fuel efficiency, all of which reward suppliers able to scale production without sacrificing reliability. Export-control tightening, xenon scarcity, and a still‐immature refueling infrastructure moderate near-term growth, yet progress in nuclear-thermal demonstrators and in-situ propellant production keeps the long-run outlook positive for the space propulsion market

Key Report Takeaways

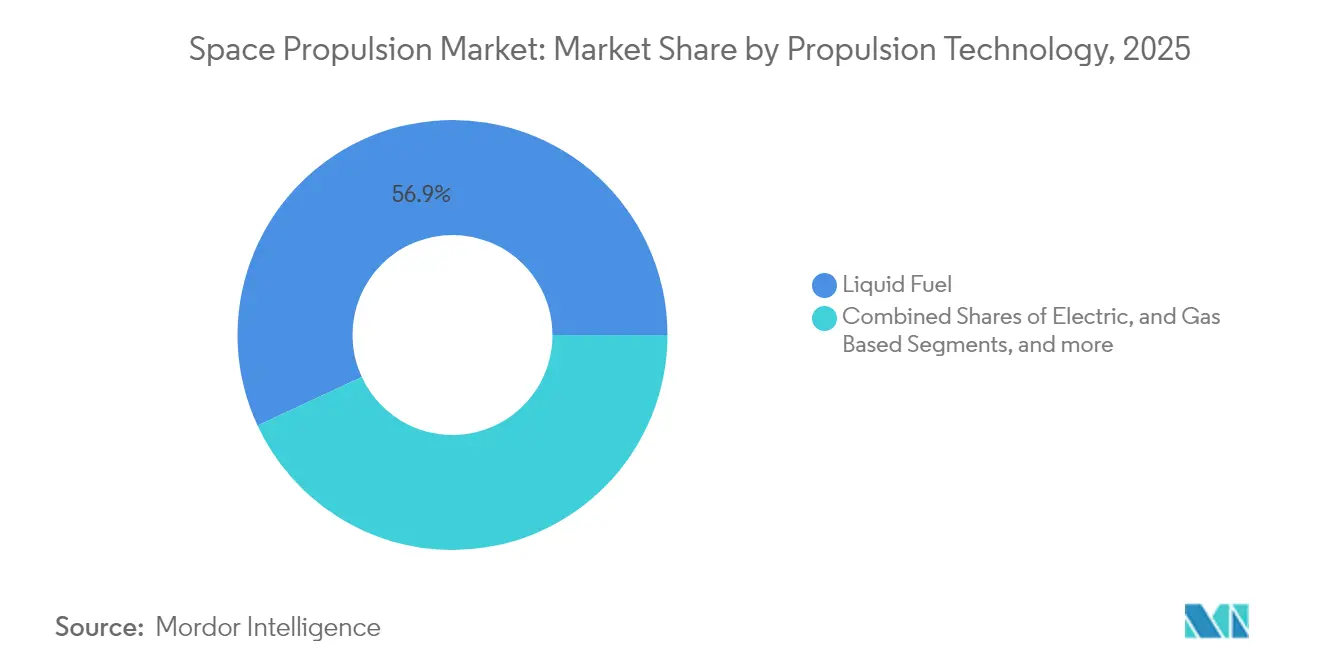

- By propulsion technology, liquid fuel engines accounted for 56.92% of the space propulsion market share in 2025, while electric propulsion is projected to post a 10.13% CAGR through 2031.

- By component, thrusters commanded 47.31% of the space propulsion market size in 2025; power processing units are expected to expand at an 8.51% CAGR to 2031.

- By platform, satellites accounted for 57.76% of the revenue in 2025; space tugs represent the fastest-growing category, with a 9.09% CAGR through 2031.

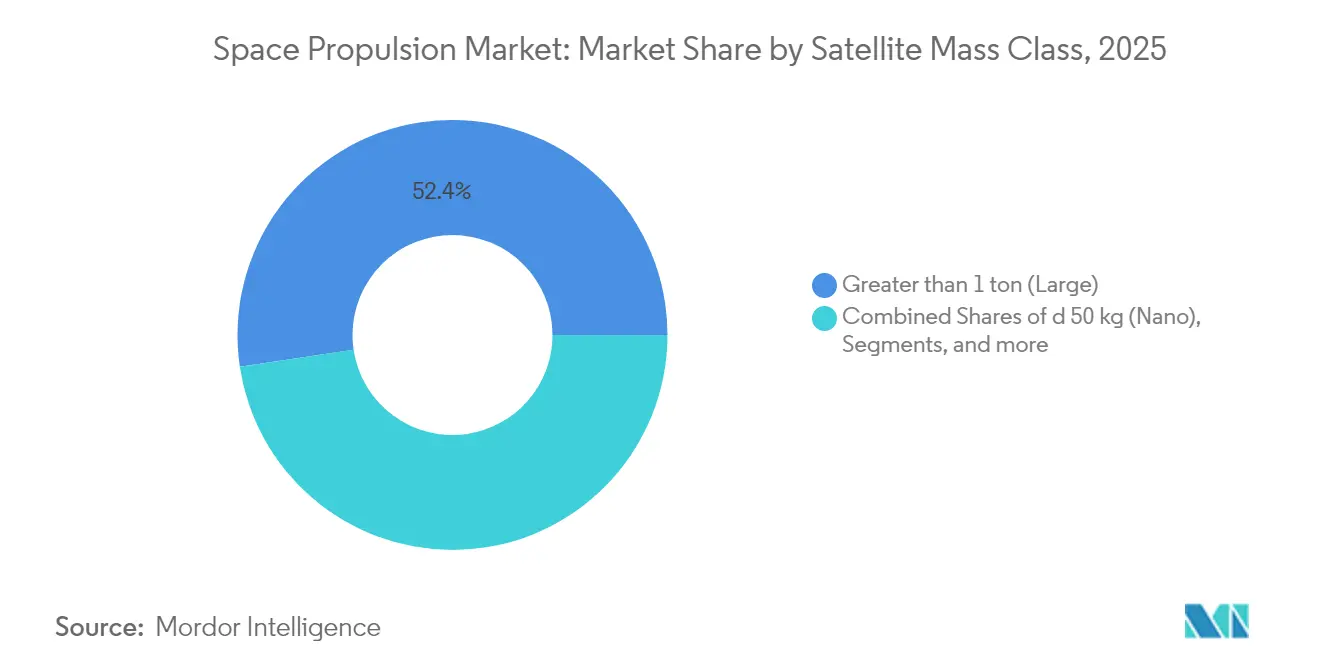

- By satellite mass class, large satellites (>1 ton) captured 52.35% of the space propulsion market size in 2025, whereas nano satellites (≤50 kg) are advancing at a 9.60% CAGR.

- By geography, North America accounted for 42.12% of the space propulsion market share in 2025; the Asia-Pacific region stands out with the highest regional CAGR of 8.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Space Propulsion Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mega-constellation funding surge | +1.8% | North America and Europe, global spill-over | Medium term (2-4 years) |

| Commercial crewed-mission race (Moon/Mars) | +1.5% | North America and Europe, Asia-Pacific build-up | Long term (≥ 4 years) |

| Falling launch costs from reusable vehicles | +1.2% | Global | Short term (≤ 2 years) |

| DARPA and ESA nuclear-thermal demonstrators | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Orbital debris-removal mandates | +0.7% | Global, early adoption in Europe | Medium term (2-4 years) |

| In-situ propellant production R&D | +0.6% | North America core, Asia-Pacific expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mega-Constellation Funding Surge

Mega-constellation budgets reshape procurement by shifting orders from single bespoke satellites to repeatable batches. The European Union earmarked USD 2.78 billion for the IRIS² secure-communications network, while Japan’s Space Strategy Fund assigned JPY 1 trillion (USD 6.7 billion) to develop domestic capability through 2030.[1]Space News Staff, “Japan Space Strategy Fund Allocation,” Space News, spacenews.com The United Kingdom dedicated GBP 1.84 billion to propulsion R&D and factory upgrades.[2]UK Government, “National Space Strategy,” GOV.UK, gov.uk As a result, prime contractors are installing automated production lines, modular thruster interfaces, and digital twins that reduce unit costs across the space propulsion market. Standardization, in turn, encourages commercial operators to adopt off-the-shelf engines that match constellation cadence requirements.

Commercial Crewed-Mission Race (Moon/Mars)

NASA’s Artemis program, now funded at USD 93 billion through 2030, requires propulsion systems with human-rating certifications that exceed those for uncrewed spacecraft. SpaceX’s methane-oxygen Starship continues integrated flight tests that validate high-thrust engines for interplanetary transit.[3]SpaceX Communications, “Falcon Heavy Performance Data,” SpaceX, spacex.com ESA’s USD 19.55 billion Explore 2040 plan earmarks capital for lunar cargo and crew vehicles.[4]European Space Agency, “Explore 2040 Strategy,” ESA, esa.int Blue Origin and Rocket Lab are adding competitive pressure by maturing large-diameter launchers, signaling that deep-space propulsion reliability will command premium pricing. As a result, the space propulsion market is experiencing increased demand for redundant engine architectures, advanced fault-detection software, and extended-duration testing campaigns.

Falling Launch Costs from Reusable Vehicles

Reusable boosters have cut launch prices by nearly 70% since 2020; Falcon Heavy hovered at USD 1,400/kg to LEO in 2024. Lower costs free satellite builders to increase payload mass and embed higher-performance thrusters that were previously deemed uneconomic. ArianeGroup’s MaiaSpace aims for similar efficiency by 2027, sparking a global race toward reusable rockets. Larger mass budgets translate into bigger propellant tanks, dual-mode propulsion stacks, and electric thrusters with longer burn times. The competitive vortex intensifies procurement for standardized propulsion-to-bus interfaces, accelerating time-to-orbit and cementing the space propulsion market’s transformation from single-mission craft to rapidly refreshable constellations.

DARPA and ESA Nuclear-Thermal Demonstrators

DARPA’s DRACO program, backed by USD 499 million in 2024, pursues a 2027 nuclear-thermal flight test. ESA has budgeted USD 173.52 million to mature complementary technologies. Nuclear-thermal engines promise thrust levels twice those of chemical systems and specific impulse approaching electric propulsion, enabling 45-day Mars cargo transfers. Reactor shielding, high-temperature materials, and regulatory compliance create formidable entry barriers that favor incumbent aerospace majors. Breakthroughs here could reorder the competitive landscape and inject fresh momentum into the space propulsion market well beyond 2030.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control regime tightening (ITAR, MTCR) | -1.4% | Global, highest impact on cross-border partnerships | Short term (≤ 2 years) |

| Limited on-orbit refueling infrastructure | -1.1% | Global | Medium term (2-4 years) |

| Persistent xenon supply bottlenecks | -0.8% | Global, concentrated in electric propulsion | Short term (≤ 2 years) |

| Investor pull-back in NewSpace SPACs | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Export-Control Regime Tightening (ITAR, MTCR)

The US State Department broadened ITAR definitions in 2024 to encompass advanced electric thrusters and autonomous guidance electronics, ensnaring roughly 40% of cross-border propulsion transactions. The Missile Technology Control Regime similarly expanded its coverage to small-satellite engines. European suppliers react by opening US subsidiaries or pivoting to domestic supply chains, while Asian operators fund indigenous engine programs to sidestep licensing delays. Compliance documentation now adds up to six months to typical delivery schedules, compressing production buffers for constellation deployments. These hurdles tilt demand toward home-country vendors, fragmenting the global space propulsion market into regional supply blocs.

Limited On-Orbit Refueling Infrastructure

NASA’s OSAM-1 mission delays push the first autonomous refueling demonstration beyond 2026, leaving operators to oversize propellant loads to guarantee mission life. The mass penalty constrains payload capacity and mutes enthusiasm for high-performance but fuel-hungry thrusters. Orbit Fab’s proprietary “fuel depot” network advances, yet propellant standards remain unsettled, risking fragmentation. Without accepted fueling ports and propellant grades, satellite builders are hesitant to invest in refuel-ready engines, which dampens near-term growth for the space propulsion market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Technology: Liquid Fuel Dominance Persists

Liquid engines accounted for 56.92% of the revenue in 2025, as they were the primary source of revenue in that year, due to the continued demand for heavy-lift boosters and high-delta-V planetary probes, whichrequiring still require dense propellants and high thrust-to-weight ratios. Electric engines, though smaller in dollar terms, are forecast to grow 10.13% annually as constellation operators prize specific impulse above 3,000 s compared with 450 s for chemical alternatives. The space propulsion market size allocated to hybrid gas-based systems remains relatively flat, with a concentration in attitude control. ThrustMe’s iodine engine reached orbit in 2024 and showed 40% cost savings over xenon units, setting a precedent for alternative propellants. Power processing units (PPUs) now ship in modular racks scaled from 200 W CubeSat levels to 20 kW GEO buses, allowing platform integrators to reuse common avionics across fleets. Suppliers with both liquid and electric lines hedge demand swings, while pure-play electric providers target constellations that sign multi-year frame agreements.

Electrification influences launch profiles: some LEO missions adopt electric orbit raising, sacrificing early operational capability for propellant mass savings. Meanwhile, deep-space explorers combine high-thrust chemical injection burns with multi-year ion payload cruises, placing blended engine packages on procurement shortlists. The dual-mode approach widens the scope, enabling the space propulsion market to accommodate overlapping mission architectures without forcing a single technology to fit all.

By Component: Thrusters Lead Market Integration

Thrusters represented 47.31% of 2025 component revenue because engines remain the highest value-add element of any propulsion stack. The integration wave sees companies bundling valves, PPUs, and control electronics into single skids, shortening satellite assembly windows by 30% according to Busek. PPUs expand at 8.51% CAGR as electric engines climb up the power curve toward kilowatt-class constellations. Advanced composite tanks reduce liner mass, and 3D-printed propellant management devices improve residual fuel drawdown for GEO station-keeping, thereby lifting overall efficiency.

Propellant feed systems integrate health sensors that feed telemetry to ground AI, enabling predictive maintenance. Nozzle innovators utilize gradient alloys that can withstand thousands of thermal cycles in reusable boosters. Cross-component convergence means customers now issue requests for proposals that cover full propulsion modules, pushing specialists into partnerships or acquisitions. The space propulsion market rewards suppliers capable of offering drop-in “propulsion suites” certified for popular satellite buses.

By Satellite Mass Class: Large Satellites Maintain Leadership

Large platforms (>1 ton) captured 52.35% of the revenue in 2025, as GEO communications and high-resolution imaging still rely on ample power budgets and robust station-keeping reserves. Nano satellites, however, post a 9.60% CAGR as operators favor disaggregated architectures that tolerate single-unit failures without disrupting service. Dawn Aerospace’s milli-Newton thrusters fit inside a 1U envelope, enabling precise pointing for CubeSats as small as 3 kg.

Micro (51-500 kg) and mini (501 kg–1 ton) classes bridge capability gaps, adopting hybrid chemical/electric packages. Regulatory debris rules incentivize mass classes under 200 kg due to simplified licensing, further propelling the uptake of nanomaterials. Still, high-value broadcast, broadband, and meteorological missions continue to order multi-ton buses, which anchor the space propulsion market in the near term. Component vendors address both extremes by miniaturizing valves for cubes and scaling cryogenic pumps for large craft.

By Platform: Space Tugs Drive Specialized Growth

Satellites accounted for 57.76% of the revenue in 2025, while space tugs emerged as the fastest-growing platform, with a 9.09% CAGR. Tugs conduct last-mile deliveries, rescue satellites stuck in transfer orbits, and perform debris removal. Impulse Space raised USD 150 million in 2025 to mass-produce tugs equipped with mixed-mode engines capable of fast burns and economical station-keeping.

Launch vehicles retain chemical engine concentration, but methane and “green” propellants open niches for newcomers. Orbital transfer vehicles, distinct from tugs, focus on constellation deployment by releasing batches of small satellites into multiple planes. Deep-space probes, although fewer in number, are equipped with bespoke electric or planned nuclear engines. The diversification forces propulsion suppliers to supply modular interfaces that fit across different platforms, expanding the total reachable revenue for the space propulsion market.

Geography Analysis

North America led with 42.12% of the revenue in 2025, driven by NASA’s USD 25 billion budget and DoD space expenditures exceeding USD 30 billion. Export-control rules direct government orders to domestic suppliers, providing incumbents with predictable demand streams. Canada contributes to additive growth through Telesat’s Lightspeed constellation and participation in the Artemis Gateway. The regional ecosystem clusters manufacturing talent, test infrastructure, and capital, sustaining the largest single regional slice of the space propulsion market.

The Asia-Pacific region records the fastest expansion at a 8.98% CAGR. China’s state-directed program topped USD 13 billion in 2024, prioritizing methane engines and high-thrust kerolox variants for crewed lunar sorties. India aims to establish a USD 44 billion space economy by 2033, channeling ISRO and private capital into research and development for liquid and electric propulsion. Japan’s USD 6.4 billion fund supports domestic thruster production lines and reactor component prototypes. South Korea invests USD 2 billion to build small-satellite propulsion capacity, demonstrating regional competition that fragments supply chains and magnifies local sourcing.

Europe sustains strategic autonomy through ESA’s USD 19.55 billion Explore 2040 budget and national initiatives in France, Germany, and the United Kingdom. Safran and ArianeGroup lead chemical and hybrid engine programs, while Exotrail and ThrustMe push electric thruster innovation that attracts global customers. The United Kingdom’s USD 2.42 billion plan to enlarge propulsion manufacturing supports sites in Scotland and the East Midlands, illustrating government-backed reshoring. European export-control parity with the United States encourages intra-bloc collaboration but erects obstacles for third-country buyers, subtly steering global procurement patterns in the space propulsion market toward regional hubs.

Rest-of-World participants Brazil, Iran, Saudi Arabia, and the United Arab Emirates scale from sounding rockets to orbital vehicles, generating incremental engine demand tailored to national regulatory frameworks. Localized programs often start with imported subsystems but transition toward indigenous thrusters, gradually enlarging the global footprint of the space propulsion market.

Competitive Landscape

Innovation and Partnerships Drive Future Success

The space propulsion market is moderately concentrated. Aerojet Rocketdyne (L3Harris Technologies, Inc.), Space Exploration Technologies Corp., and Northrop Grumman dominate the launch and deep-space contracts, leveraging deep engineering benches and certified production processes. Rocket Lab, Exotrail, ThrustMe, and Busek gain share in commercial constellations by offering rapid-production electric thrusters at price points attractive to NewSpace operators. Patent filings for Hall effect and alternative-propellant thrusters rose 45% in 2024, evidencing a wave of intellectual property generation.

Vertical integration is the leading strategic theme. SpaceX manufactures engines, chambers, turbo-pumps, and control electronics under one roof, squeezing margins for component specialists. In response, suppliers either partner, like Phase Four pairing with Redwire to merge propulsion and bus manufacturing, or pursue mergers that marry thrusters with PPUs. Nuclear-thermal efforts require specialized fuel fabrication and reactor vessel expertise, favoring conglomerates with defense nuclear portfolios.

Market entry barriers remain high for launch-vehicle propulsion; still, electric thruster niches spawn newcomers funded by venture capital targeting CubeSat and OTV segments. Regulatory filters such as ITAR tilt US defense programs toward incumbents, while Europe’s push for sovereignty insulates its suppliers. Growing demand for standardized refueling interfaces and debris-removal propulsion presents green-field territory where neither legacy primes nor startups hold dominant sway, leaving competitive outcomes open over the forecast horizon.

Space Propulsion Industry Leaders

Space Exploration Technologies Corp.

ArianeGroup GmbH

Blue Origin Enterprises, L.P.

Northrop Grumman Corporation

Aerojet Rocketdyne (L3Harris Technologies, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Honda R&D Co., Ltd., a subsidiary of Honda Motor Co., Ltd., independently developed and conducted a launch and landing test of an experimental reusable rocket. The rocket measures 6.3 m in length, 85 cm in diameter, and weighs 900 kg when dry and 1,312 kg when wet.

- June 2025: Desert Works Propulsion (DWP) completed initial testing of multiple prototype discharge and neutralizer cathodes, which were developed for Turion Space Corp.’s TIE-20 ion thruster.

- June 2025: NASA, in partnership with L3Harris Technologies, conducted the first hot-fire test of the RS-25 rocket engine. This engine is designated to power the fifth launch of the Space Launch System (SLS) rocket as part of the Artemis Moon exploration campaign.

Global Space Propulsion Market Report Scope

Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Asia-Pacific, Europe, North America are covered as segments by Region.| Electric |

| Gas Based |

| Liquid Fuel |

| Thrusters |

| Propellant Feed Systems |

| Power Processing Units |

| Tanks and PMDs |

| Nozzles |

| Less than or equal to 50 kg (Nano) |

| 51–500 kg (Micro) |

| 501 kg–1 ton (Mini) |

| Greater than 1 ton (Large) |

| Satellite |

| Launch Vehicle |

| Orbital Transfer Vehicle |

| Deep-Space Probe |

| Space Tug |

| North America | United States |

| Canada | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Singapore | |

| Rest of the Asia-Pacific | |

| Europe | France |

| Germany | |

| Russia | |

| United Kingdom | |

| Rest of Europe | |

| Rest of the World | Brazil |

| Iran | |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of the World |

| By Propulsion Technology | Electric | |

| Gas Based | ||

| Liquid Fuel | ||

| By Component | Thrusters | |

| Propellant Feed Systems | ||

| Power Processing Units | ||

| Tanks and PMDs | ||

| Nozzles | ||

| By Satellite Mass Class | Less than or equal to 50 kg (Nano) | |

| 51–500 kg (Micro) | ||

| 501 kg–1 ton (Mini) | ||

| Greater than 1 ton (Large) | ||

| By Platform | Satellite | |

| Launch Vehicle | ||

| Orbital Transfer Vehicle | ||

| Deep-Space Probe | ||

| Space Tug | ||

| By Geography | North America | United States |

| Canada | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Singapore | ||

| Rest of the Asia-Pacific | ||

| Europe | France | |

| Germany | ||

| Russia | ||

| United Kingdom | ||

| Rest of Europe | ||

| Rest of the World | Brazil | |

| Iran | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of the World | ||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.