Soybean Fungicide Seed Treatment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

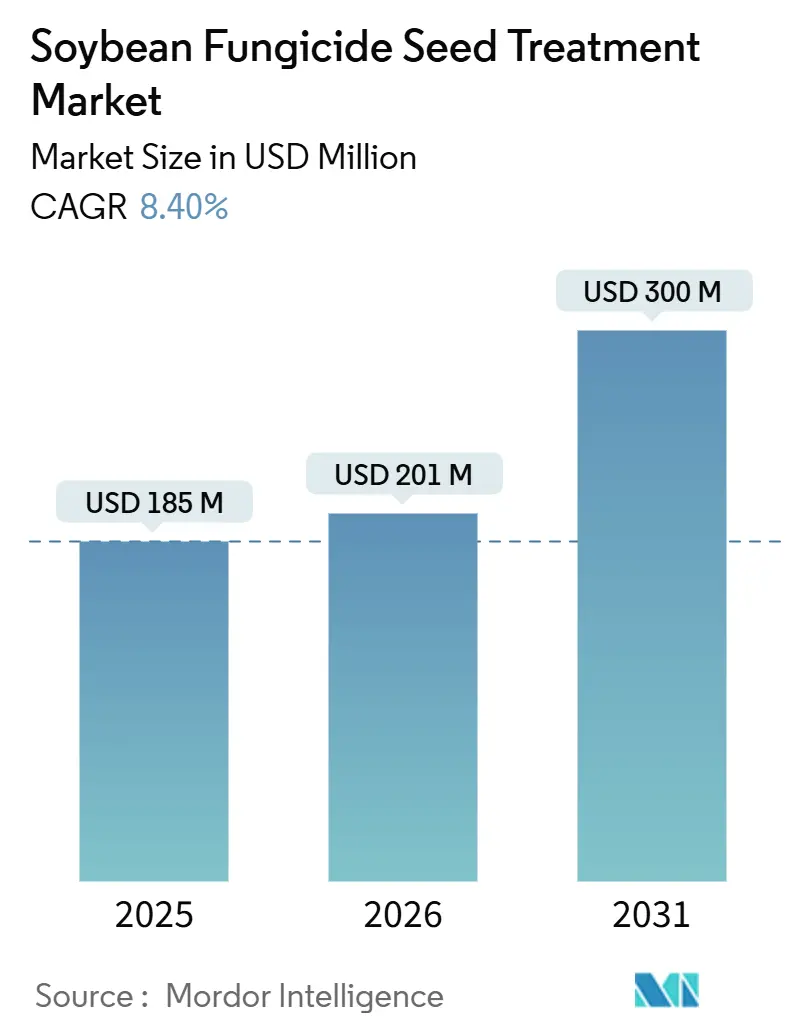

| Market Size (2026) | USD 201 Million |

| Market Size (2031) | USD 300 Million |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

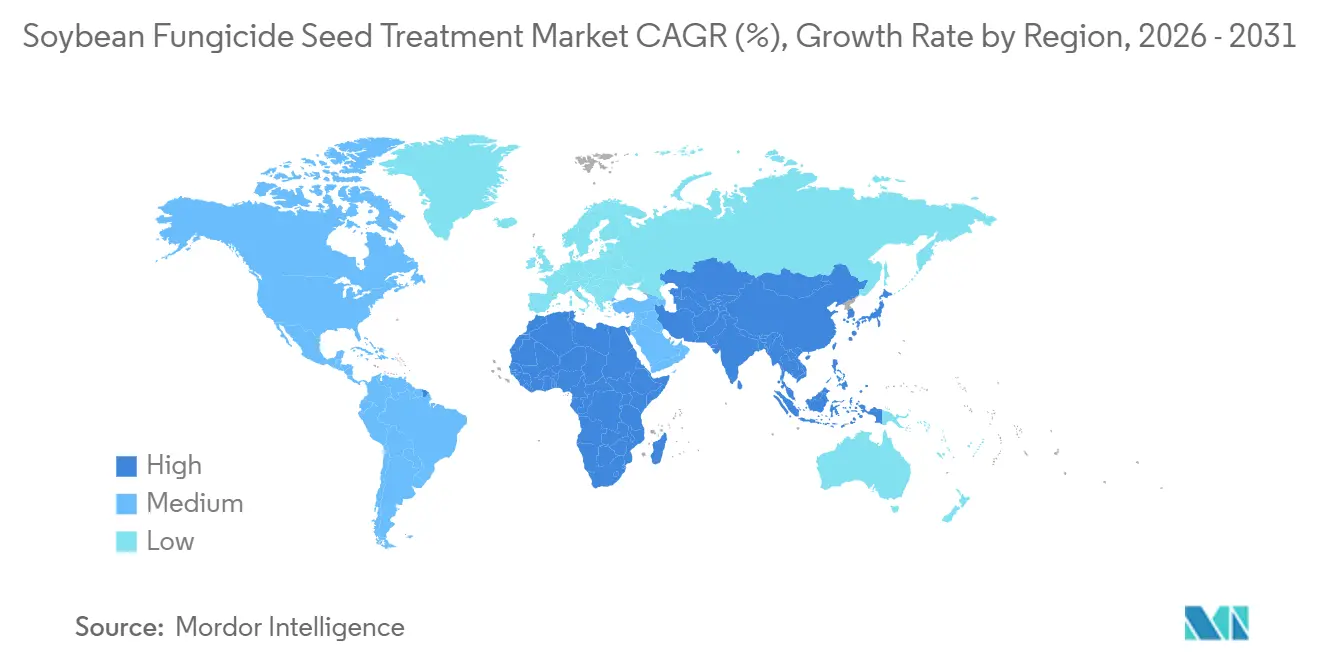

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

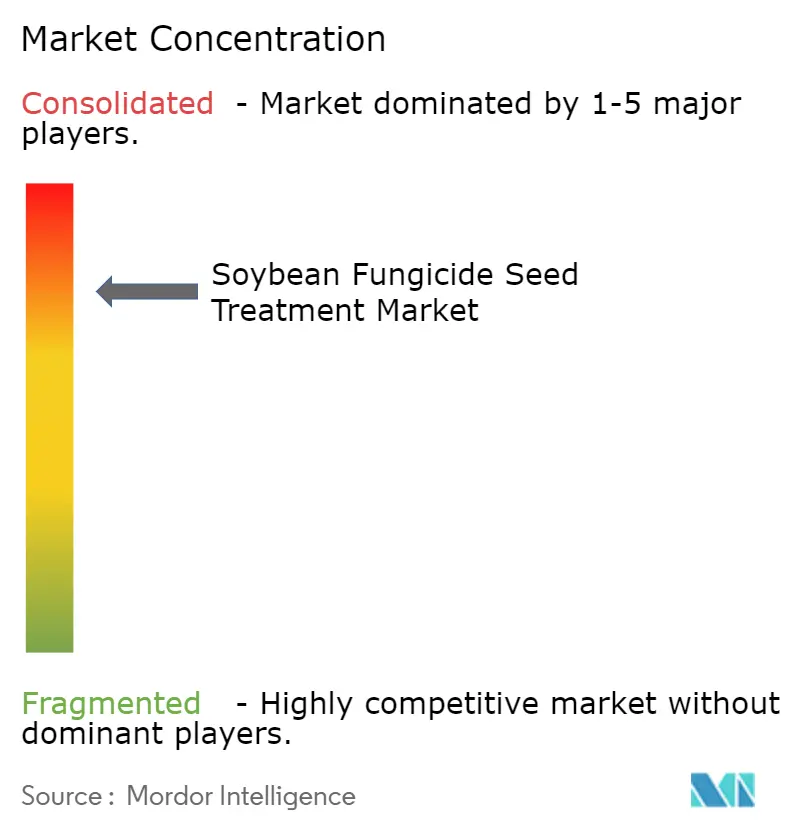

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soybean Fungicide Seed Treatment Market Analysis by Mordor Intelligence

The soybean fungicide seed treatment market was valued at USD 185 million in 2025 and is projected to grow from USD 201 million in 2026 to USD 300 million by 2031, registering a CAGR of 8.4% from 2026 to 2031. This trend highlights a significant change in how growers safeguard yield potential before planting. It is driven by the combination of fungicide-resistant pathogen strains and advancements in precision-coating technologies that enhance the efficiency of active ingredient delivery. The continuous evolution of pathogens is surpassing the effectiveness of single-mode chemistries, prompting growers to adopt multi-active coatings. These coatings combine phenylamides, strobilurins, and chemical antagonists to ensure successful stand establishment within the critical early stages after planting. Precision drum, electrostatic, and plasma-enhanced coaters provide uniform coverage, reducing active ingredient waste and reinforcing the value proposition for both large commercial processors and smaller regional conditioners.

Key Report Takeaways

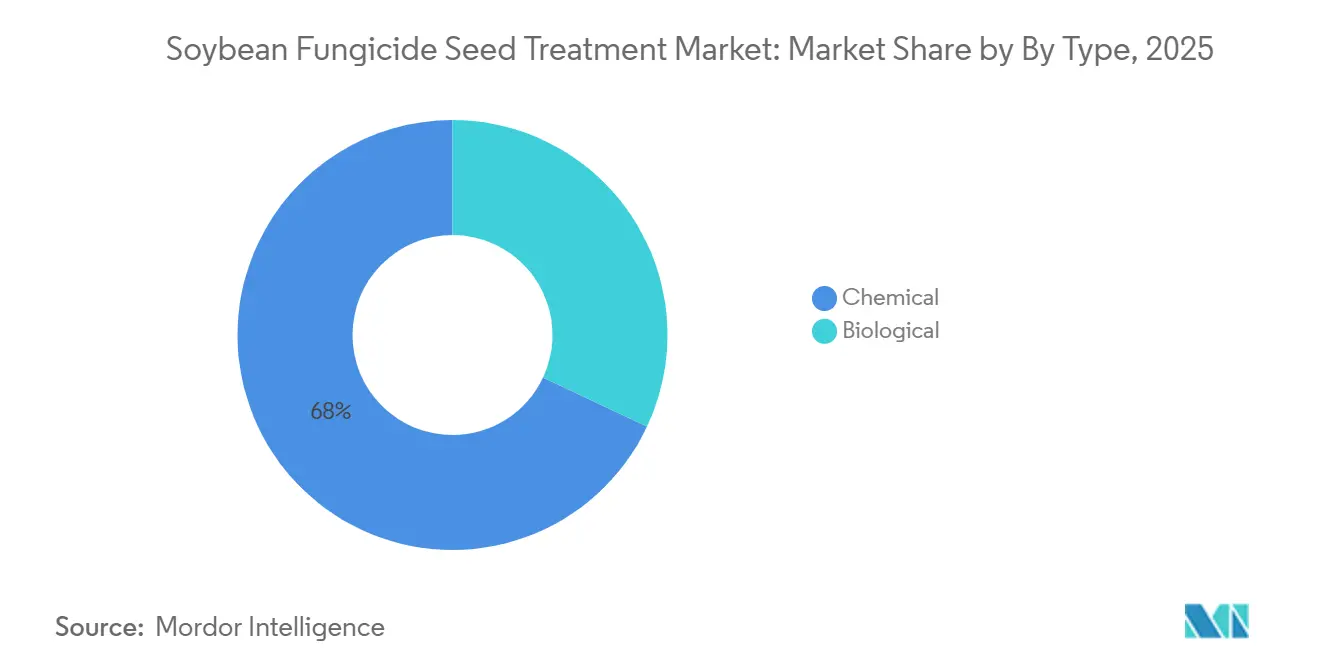

- By type, chemical formulations held the largest market share, 68%, for the soybean fungicide seed treatment market in 2025, and the biological type is projected to grow at the fastest CAGR of 9.3% from 2026 to 2031.

- By geography, North America accounted for the largest market share, 34%, for the soybean fungicide seed treatment market in 2025, and the Asia-Pacific market size is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soybean Fungicide Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of fungicide-resistant Phytophthora sojae strains | +1.8% | North America, South America, and Asia-Pacific | Medium term (2-4 years) |

| Growing demand for high-quality crop yields | +1.5% | Global | Long term (≥4 years) |

| Government subsidies for seed-treatment adoption | +1.2% | North America, Europe, and Asia-Pacific | Short term (≤2 years) |

| Expansion of cold-plasma coating technologies | +0.9% | North America, Europe, and early Asia-Pacific | Medium term (2-4 years) |

| Adoption of drone-enabled seed pelleting | +0.7% | North America and South America | Medium term (2-4 years) |

| Integration of RNA-based fungicides into seed-treatment stacks | +1.1% | Global, led by North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Fungicide-Resistant Phytophthora sojae Strains

Field surveys have identified multiple Phytophthora sojae pathotypes capable of overcoming long-standing Rps genes, reducing genetic resistance, and driving growers toward multi-mode seed treatments. Variability is accelerating the adoption of stacked chemistries that combine phenylamides with ethaboxam and biological antagonists. Additionally, South American researchers have reported azoxystrobin-resistant Colletotrichum truncatum, highlighting the need for new active ingredients. Pathogen populations are evolving more rapidly than the introduction of new active ingredients to the market, prompting growers to adopt seed treatments with multiple modes of action.

Growing Demand for High-Quality Crop Yields

Exporters are facing stricter regulations on mycotoxins and protein variability, making seed treatment an essential quality assurance measure. For instance, Chinese importers often reject shipments containing deoxynivalenol levels exceeding 1 part per million, a risk mitigated by managing Fusarium infections during germination. In Argentina, producers aiming for premium contracts with European crushers have standardized seed treatment practices across multiplication plots. According to seed companies, most of the foundation seed lots are now treated to ensure varietal purity.

Government Subsidies for Seed-Treatment Adoption

According to the United States Department of Agriculture, Climate-smart agriculture programs in the United States partially reimburse costs for biological seed treatments and precision coaters, reducing entry barriers for small farms. These initiatives encourage early adoption. However, most incentives are designed to phase out within five years, requiring suppliers to demonstrate tangible on-farm returns. In Europe, pilot programs restrict eligibility to low-risk or biological actives, gradually shifting the portfolio away from triazoles. The temporary nature of these subsidies results in rapid, front-loaded market growth.

Expansion of Cold-Plasma Coating Technologies

Cold plasma seed treatment technologies are increasingly utilized in soybean fungicide applications due to their effectiveness in enhancing seed performance and reducing pathogen loads without leaving chemical residues. Research indicates that cold plasma treatment can improve soybean seed germination rates by up to 14.66% and vigor indices by 63.33%, contributing to better early-stage crop establishment and decreased disease susceptibility. [1]Source: National Center for Biotechnology Information (NCBI), “Cold Plasma Treatment Improves Soybean Seed Germination and Vigor,” pmc.ncbi.nlm.nih.gov. Compatibility tests indicate that plasma pre-treatment enhances biological adherence, positioning this technology as a potential link between synthetic and microbial approaches. Broader adoption will depend on throughput efficiency and demonstrated yield improvements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse effects of chemical fungicides on soil microbiota | −0.8% | Global, acute in organic and regenerative systems | Medium term (2-4 years) |

| Stringent regulations on agrochemicals | −1.1% | Europe, North America, and expanding Asia-Pacific | Long term (≥4 years) |

| Supply-chain volatility for key triazole actives | −0.6% | Global, concentrated in Asia-Pacific sourcing | Short term (≤2 years) |

| Farmer perception of phytotoxicity in low-organic-matter soils | −0.5% | North America Great Plains, and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Effects of Chemical Fungicides on Soil Microbiota

The application of chemical fungicide seed treatments in soybean cultivation is facing growing limitations due to their negative impact on beneficial soil microbiota, particularly nitrogen-fixing Rhizobium species. These fungicides can interfere with root nodulation, thereby reducing the efficiency of biological nitrogen fixation. According to a study published in Bioscience, soybean seeds treated with fungicides exhibited a 36% decrease in root nodules, adversely affecting plant-microbe symbiosis and nutrient absorption [2]Source: Nyzhnyk et al., “Rhizobium Inoculant and Seed-Applied Fungicide Effects on Soybean Nodulation,” Frontiers in Bioscience, imrpress.com . This reduction can constrain yields in low-fertility soils, leading to increased regulatory scrutiny and driving the adoption of microbiome-friendly or biological seed treatment alternatives.

Stringent Regulations on Agrochemicals

The Farm to Fork strategy targets a 50% reduction in synthetic pesticide use by 2030, with several triazoles already being phased out [3]Source: European Commission, “Farm to Fork Strategy: For a Fair, Healthy and Environmentally-Friendly Food System,” ec.europa.eu. In the United States, Environmental Protection Agency re-assessments have reduced application limits for mefenoxam, increasing compliance costs. Smaller seed companies face challenges with multi-jurisdictional dossiers, driving further consolidation into multinational portfolios. Biologicals benefit from less stringent regulatory requirements. However, efficacy challenges persist in high-pressure environments. As a result, regulatory developments continue to limit growth opportunities for the synthetic segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chemical Dominance Meets Rising Biological Momentum

Chemical formulations accounted for the largest market share, at 68%, for the soybean fungicide seed treatment market in 2025. Meanwhile, the biological market size is projected to grow at the fastest CAGR of 9.3% from 2026 to 2031. Triazole and phenylamide combinations continue to be widely used for managing Phytophthora and Rhizoctonia due to their extensive field history, cost-effectiveness per hectare, and broad regulatory approvals, making them a staple across commodity crops. However, resistance concerns in Brazil and the United States are driving the adoption of rotation and stacking practices, encouraging growers to opt for premium multi-active blends.

Biological seed treatments include living microbes such as Bacillus and Trichoderma, along with fermentation-derived metabolites. Examples like Corteva Agriscience’s Pseudomonas-based Lumisena and Syngenta’s Bacillus-based Saltro highlight the growing adoption of high-performance biofungicides. Advances in encapsulation technologies, such as alginate matrices, have improved shelf life and on-seed viability. If efficacy continues to improve, biological seed treatments could achieve a comparable market share by 2031, shifting competition toward companies with extensive microbial libraries and large-scale fermentation capabilities.

Geography Analysis

North America accounted for the largest market share of 34% for soybean fungicide seed treatment revenue in 2025, driven by widespread coating practices across the Corn Belt and Prairie provinces. Growth through 2031 is projected to be moderate due to saturated acreage. However, premiumization trends are evident as processors adopt atmospheric-pressure cold-plasma units, which enhance germination and reduce synthetic inputs. Additionally, subsidies linked to climate-smart agriculture are facilitating the transition to biological and precision-applied stacks, helping to sustain revenue even as planted hectares stabilize.

The Asia-Pacific market size is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031, as growers address challenges such as Asian soybean rust, Phytophthora root rot, and Diaporthe stem canker. India and China are at earlier stages of adoption, with lower penetration rates. However, government initiatives providing subsidized treated seeds to smallholders are helping to close the gap. In Brazil, where approximately three-quarters of soybean seeds are already coated, rising disease pressure in regions like Mato Grosso and Paraná supports continued volume growth, alongside a shift toward multi-active or biological products.

Europe and the Middle East and Africa are projected to experience slower growth, due to smaller soybean acreage and stricter residue regulations under the Farm to Fork strategy, which is phasing out several triazoles. In Europe, organic and integrated pest management producers in countries such as Germany, France, and Italy are early adopters of microbial coatings from BASF SE agricultural solutions and Novozymes, though overall volumes remain limited. In Africa, irrigation-dependent regions in Egypt and South Africa rely on seed treatments to mitigate high pathogen pressure, while Turkey is emerging as a formulation hub serving neighboring markets.

Competitive Landscape

The five major companies, including Syngenta Group Co., Ltd., Bayer AG, BASF SE, Corteva, Inc., and UPL Limited in 2025, jointly command a highly concentrated share of global revenue through extensive active-ingredient portfolios, long-term seed-company alliances, and broad regulatory dossiers. Their flagship stacks blend triazoles, strobilurins, and succinate dehydrogenase inhibitors to maintain efficacy against shifting pathogen populations, an advantage smaller rivals find costly to replicate.

Competitive intensity is rising as venture-backed biological specialists such as GreenLight Biosciences Inc. and Valent U.S.A. LLC commercializes microbe- and dsRNA-based coatings that satisfy residue-sensitive export channels [4]Source: Zheng Y. et al., “Double-Stranded RNA-Mediated Gene Silencing for Fungal Disease Control,” Frontiers in Microbiology, frontiersin.org. Incumbents are countering through acquisition and licensing. BASF SE is enhancing its biological seed treatment capabilities by constructing a new fermentation plant in Germany. This facility, designed for the production of biological fungicides and seed treatment products, is scheduled to become operational in the second half of 2025.

Process innovation is an area of growing focus. Currently, a limited proportion of global seed volumes utilize drone-enabled variable-rate pelleting or plasma-based surface activation. However, these technologies help reduce active-ingredient waste and customize dosing based on soil risk. Companies integrating proprietary active ingredients with equipment platforms are well-positioned to generate service revenue and establish switching costs. For instance, Syngenta's patent filings on clay-nanosheet carriers for dsRNA highlight the increasing strategic importance of delivery science alongside molecule discovery.

Soybean Fungicide Seed Treatment Industry Leaders

Syngenta Group Co., Ltd.

Bayer AG

BASF SE

Corteva, Inc.

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: BASF SE introduced Poncho Votivo Precise, a seed treatment solution combining biological and chemical components. This product offers early-stage protection against pests and diseases, enhancing soybean seed treatment programs.

- September 2023: Corteva Inc. introduced LumiTreo fungicide seed treatment, a three-mode-of-action solution designed to address early-season soybean diseases such as damping-off and root rot, thereby improving stand establishment.

- March 2021: Syngenta Group Co., Ltd. announced the U.S. registration of VAYANTIS fungicide seed treatment, developed for crops such as soybeans, to address early-season diseases, including Pythium and Phytophthora.

Global Soybean Fungicide Seed Treatment Market Report Scope

Soybean fungicide seed treatment entails the application of fungicides to soybean seeds before planting. This process protects the seeds from soil-borne and seed-borne fungal diseases during the early growth stages. It supports better germination, improves crop establishment, and helps increase yield by minimizing disease-related losses in soybean cultivation. The soybean fungicide seed treatment market report is segmented by type (chemicals and non-chemical/biological), and by geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Chemical |

| Non-Chemical/Biological |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| Type | Chemical | |

| Non-Chemical/Biological | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the soybean fungicide seed treatment space today?

The market is projected to grow at USD 201 million in 2026 with 8.4 % CAGR from 2026-2031 and reach USD 300 million in 2031.

Which product category currently leads global revenue?

Chemical formulations remain the largest category, holding 68 % share in 2025.

Where is adoption expanding the fastest geographically?

Asia-Pacific is the fastest region, advancing near 9.8 % CAGR 2026-2031 due to rising uptake in China and India.

What is driving the move toward biological coatings?

Export residue limits, government subsidies, and improvements in microbial formulation technology are accelerating biological demand.

Page last updated on: