Southeast Asia Internet Radio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

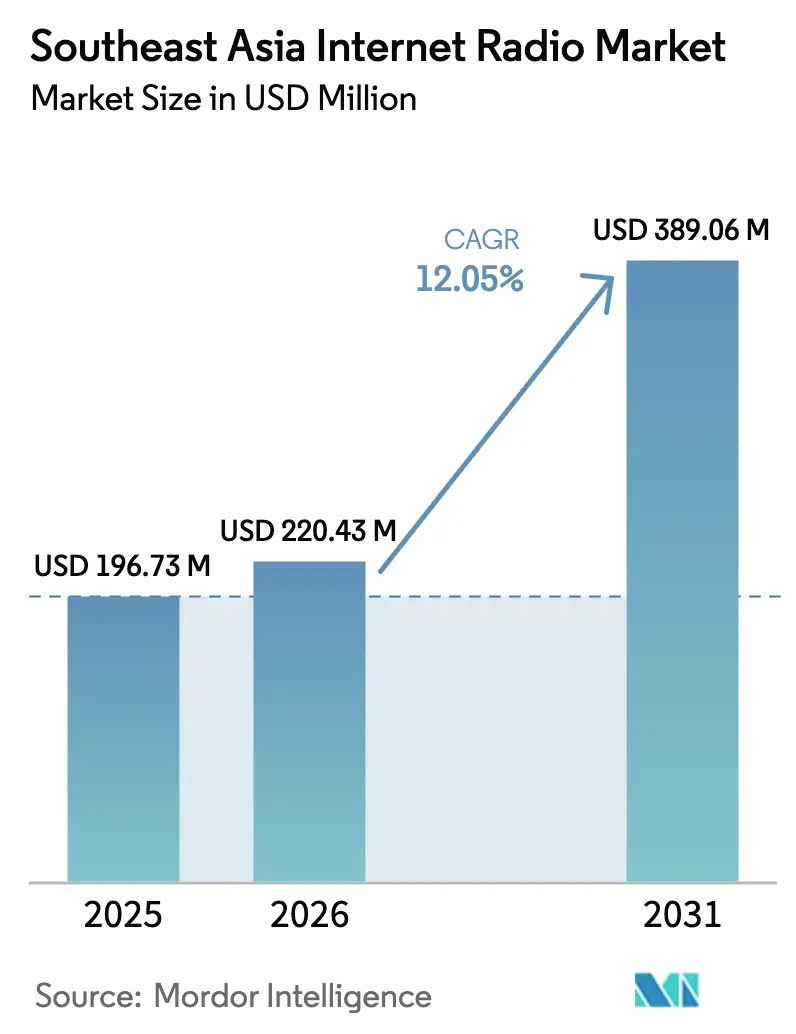

| Base Year Market Size (2025) | USD 196.73 Million |

| Market Size (2026) | USD 220.43 Million |

| Market Size (2031) | USD 389.06 Million |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Internet Radio Market Analysis by Mordor Intelligence

The Southeast Asia internet radio market size was valued at USD 196.73 million in 2025 and estimated to grow from USD 220.43 million in 2026 to reach USD 389.06 million by 2031, at a CAGR of 12.05% during the forecast period (2026-2031). Momentum stems from mandated analog switch-off deadlines, steady growth in LTE and 5G coverage, and the rising appeal of managed service contracts that bundle hardware, airtime, and cloud dispatch into a single invoice. Digital platforms that combine narrow-band private mobile radio with broadband backhaul now dominate deployments, reducing response times for public-safety teams and utilities while enabling the integration of telemetry and video add-ons. Falling unit prices for Chinese-sourced push-to-talk over cellular (PoC) terminals shrink the cost gap versus smartphones, yet rugged radios still command a premium due to 18-hour battery life and IP68 ratings. On the supply side, vendors are differentiating themselves with zero-trust encryption, low-earth-orbit (LEO) satellite links, and dual-mode radios that roam seamlessly between licensed spectrum and commercial LTE networks.

Key Report Takeaways

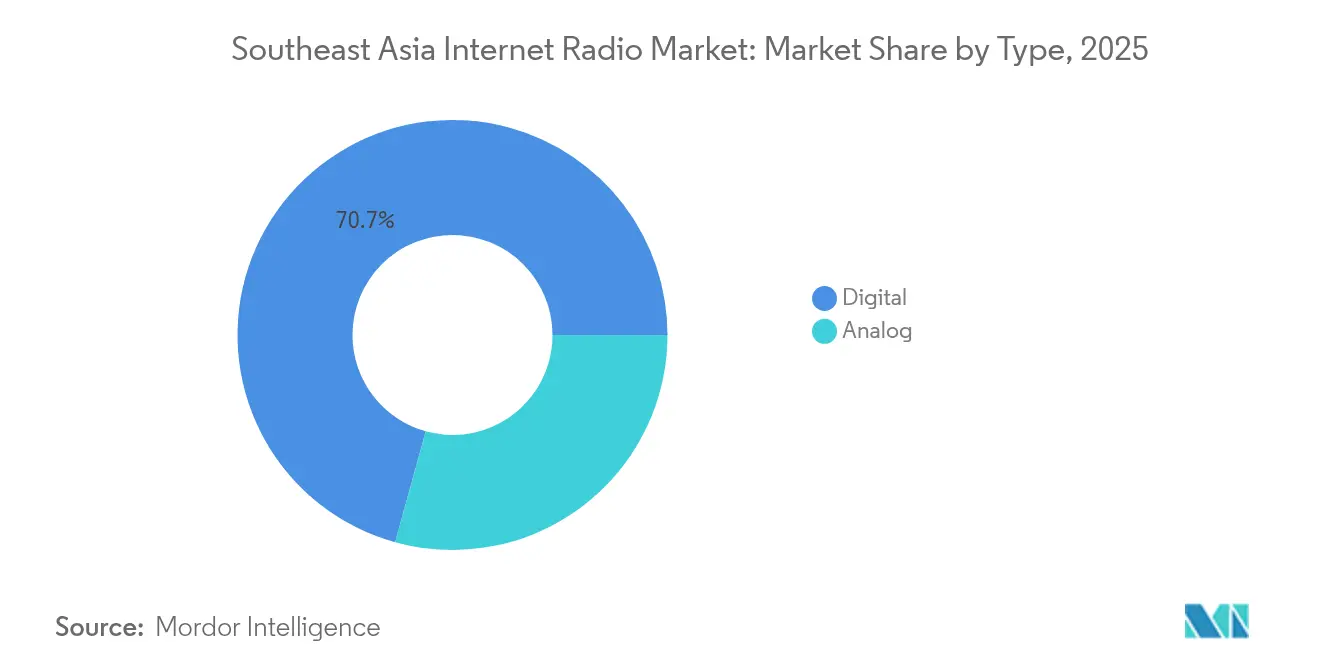

- By type, digital equipment accounted for 70.70% of Southeast Asia's internet radio market share in 2025 and is forecast to contract at a 13.03% CAGR through 2031.

- By internet radio terminal type, PoC devices held a 63.40% share of the Southeast Asia internet radio market size in 2025, while dual-mode rugged radios are projected to advance at a 13.48% CAGR to 2031.

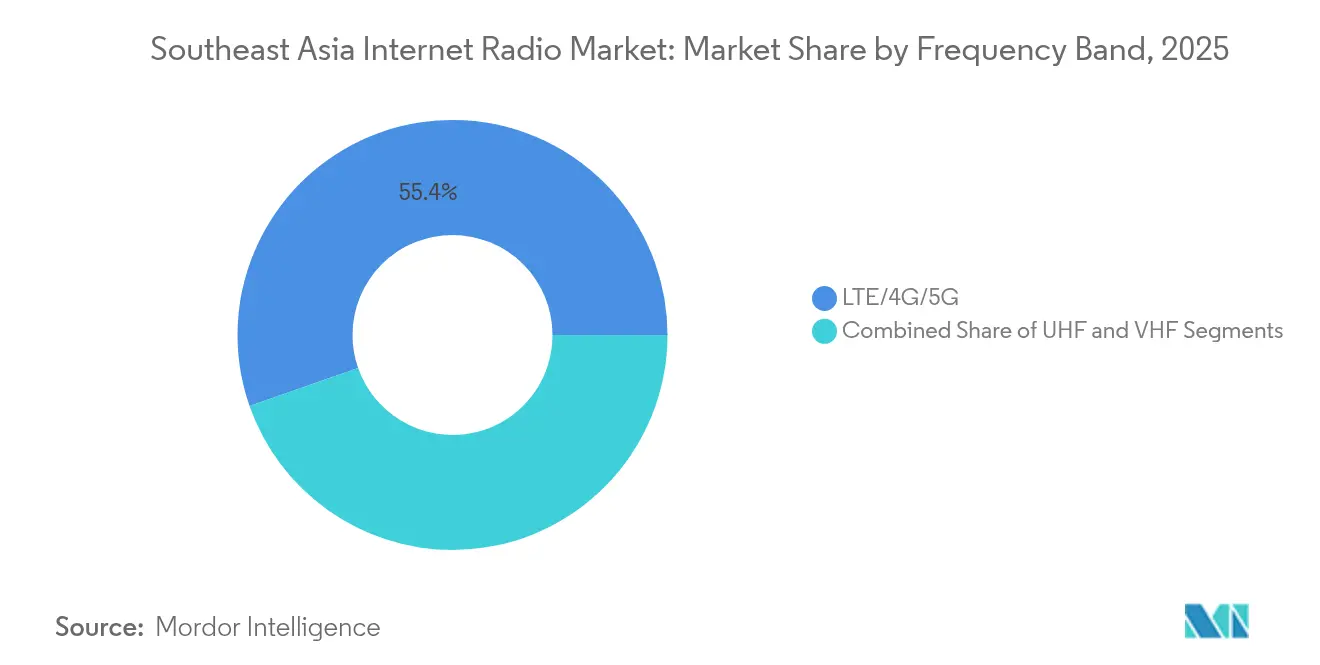

- By frequency, LTE/4G/5G captured 55.35% of the revenue in the Southeast Asia internet radio market in 2025 and is projected to expand at a 14.45% CAGR between 2026 and 2031.

- By end-user industry, utilities recorded the fastest growth, increasing at a 14.85% CAGR to 2031 and gradually narrowing the gap with government and public-safety buyers, which led with 48.32% of the revenue in the Southeast Asia internet radio market in 2025.

- By subscription model, managed service subscriptions grew at a 14.31% CAGR in 2025-2026, outpacing the capital-expenditure route favored by large public agencies, while capital expenditure on device purchase captured 57.21% of the Southeast Asia internet radio market.

- By country, Indonesia led the regional demand with a 29.90% share of the Southeast Asia internet radio market in 2025, whereas Vietnam is poised for the quickest expansion at a 15.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Internet Radio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Superior battery life and ruggedness over smartphones | +2.1% | Indonesia, Philippines, Malaysia, Thailand | Medium term (2-4 years) |

| Push-to-talk simplicity enhances workforce efficiency | +2.5% | Region-wide, led by public safety and utilities | Short term (≤ 2 years) |

| Rapid digital migration within public-safety networks | +3.2% | Indonesia, Vietnam, Thailand, Philippines | Medium term (2-4 years) |

| Rising adoption in smart-city command centers | +1.8% | Singapore, Jakarta, Bangkok, Manila, Hanoi | Long term (≥ 4 years) |

| Integration of LEO-satellite backhaul for remote islands | +1.4% | Indonesia east, Philippine archipelago | Long term (≥ 4 years) |

| Emergence of local OEM private-label PoC devices reducing TCO | +2.3% | Vietnam, Thailand, Malaysia, Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Superior Battery Life and Ruggedness Over Smartphones

Professional radios deliver 18-24 hours of operation on a charge, versus 6-8 hours for smartphones running PoC apps, an edge that matters during 24-hour shifts or deployments in natural disasters.[1]Motorola Solutions, “APX NEXT Mission-Critical Radio,” motorolasolutions.com Motorola’s APX NEXT and Hytera’s X1e, both introduced in 2024, feature large batteries paired with IP68 casings and MIL-STD-810H shock resistance, enabling first responders to stay online even in monsoon rains and extreme heat. The Philippines National Police logged a 35% reduction in device replacement costs after moving from consumer handsets to rugged DMR radios in 2024. Demand for IP67-plus ratings is increasing across palm-oil plantations and offshore platforms, where salt spray and particulate ingress can rapidly disable smartphones, yet often fall under radio warranty programs. In aggregate, superior durability adds roughly 2.1 percentage points to the forecast CAGR.

Push-to-Talk Simplicity Enhances Workforce Efficiency

Sub-300 millisecond call-setup time eliminates the dial screen, a benefit that compounds across thousands of interactions in logistics hubs and emergency control rooms. Singapore’s SBS Transit trimmed driver-to-control voice exchanges from 12 seconds to under 2 seconds once its 2024 TETRA rollout went live.[2]LTA Singapore, “Public Transport TETRA Upgrade,” lta.gov.sg Thailand’s Royal Thai Police extended TETRA to every province during the same year, enabling dispatchers to coordinate multi-agency missions without requiring multiple app taps. Cognitive-load studies show that a single PTT button helps officers maintain situational awareness under stress, a consideration that corporate ergonomics teams now cite when specifying radios for warehouses and other hazardous environments.

Rapid Digital Migration Within Public-Safety Networks

Mandatory analog shutdown windows between 2024 and 2027 are pushing agencies toward encrypted trunked radio, spurring USD 208 million in Vietnam alone under a 2024-2030 roadmap. Indonesia connected 34 provincial disaster centers via DMR Tier III in 2024, closing spectrum gaps and pulling telemetry from flood sensors that legacy FM rigs could never handle. LTE expansion to 95% of Philippine municipalities by mid-2024 further accelerates PoC adoption among rural firefighters and medics. Similar mandates in Malaysia and Thailand are expected to keep digital tender pipelines active at least through 2027.

Rising Adoption in Smart-City Command Centers

Integrated urban operations combine CCTV, traffic lights, and environmental sensors in a single dashboard, requiring low-latency radio communication. Punggol Digital District brought a private LTE plus MCPTT bundle online in early 2024 to orchestrate security, cleaning, and utility crews. Bangkok’s MRT board awarded Nokia a 2024 contract, knitting TETRA into its control room for real-time train disruption alerts. Early success stories encourage neighboring cities to embed radio into smart-streetlight and flood-monitoring projects, fuelling a long-run demand slope.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion in unlicensed bands | –1.6% | Singapore, Jakarta, Bangkok, Manila urban cores | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in IP-based radios | –1.2% | Region-wide, acute for public safety | Medium term (2-4 years) |

| Supply-chain dependence on China-based chipsets | –0.9% | All importing countries | Short term (≤ 2 years) |

| Capital constraints among SME industrial users | –1.4% | Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities in IP-Based Radios

As voice migrates onto IP networks, hackers gain new avenues for attack. ETSI upgraded its Tier III encryption baseline to AES-256 in 2024, yet many municipal fleets still deploy weaker ciphers.[3]ETSI, “TS 102 361-4 Encryption Standards,” etsi.org Indonesia’s cyber agency now mandates end-to-end encryption, but provincial compliance lags. Motorola patched its WAVE PTX system in June 2024 to bring in per-session keys. Persistent risk perceptions trim projected CAGR by 1.2 percentage points until zero-trust frameworks prove themselves broadly.

Spectrum Congestion in Unlicensed Bands

Cheap PoC units often default to 2.4 GHz or 5 GHz ISM channels, which Wi-Fi already crowds. Singapore’s regulator logged a 40% jump in interference reports downtown during 2024. Thailand is working on Band 28 licenses for commercial MCPTT users, but timelines stay fluid. Until refarming advances, voice drop-outs in malls, hotels, and ports will shave roughly 1.6 percentage points from growth forecasts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital Systems Dominate Migration Wave

Digital equipment controlled 70.70% of the Southeast Asia internet radio market share in 2025, growing at a 13.03% CAGR due to shutdown orders for analog equipment and encrypted voice mandates. Government buyers accelerate tender cycles before spectrum licenses expire, while utilities pivot to telemetry-ready radios that merge GPS, Bluetooth, and SCADA gateways. Analog persists in rural cooperatives where terminals cost USD 150, yet a lack of spare parts and vendor support is curtailing its lifespan.

Motorola’s MOTOTRBO R7, equipped with API hooks for third-party apps, illustrates how digital packages drive recurring software revenue. Across Java and Sumatra, PLN replaced 8,000 analog units with R7s in 2024, linking substations to a centralized control desk. Analog’s final refuge lies in micro-fleet rentals at construction sites, but most agencies now include digital procurement clauses in their 2025 budgets.

By Internet Radio Terminal Type: Dual-Mode Architectures Gain Traction

PoC devices generated 63.40% of the revenue in 2025, yet dual-mode rugged radios are slated for a 13.48% CAGR through 2031 as enterprises seek spectrum redundancy. Hytera’s HP7 and Motorola’s LEX L11 combine DMR or P25 with LTE, ensuring encrypted fallback when cellular fades. Malaysia’s Petronas and Singapore’s Civil Defence Force finalized national deployments in 2024, citing uninterrupted voice during offshore platform incidents and tunnel fires, respectively.

Entry-level PoC subscriptions, priced at USD 15-30 per month, attract SMEs that cannot afford a trunked repeater, explaining PoC’s numerical dominance. Emerging mid-tier devices embed Wi-Fi 6 and BLE tracking to support indoor way-finding, a feature popular among hospitals and malls.

By Frequency Band: LTE and 5G Reshape Spectrum Economics

LTE/4G/5G bands accounted for 55.35% of deployments in 2025 and are projected to grow at a 14.45% CAGR, driven by spectrum awards for Bands 28 and 31, as well as declining airtime tariffs. Pilot demonstrations of 3GPP Release 18 MCPTT over 5G recorded sub-200 millisecond latency, matching critical-voice criteria. Regulators now test shared-network business models to cut capex for smaller fleets.

UHF retains value among utilities where long-baseline propagation prevails over bandwidth. Indonesia’s national UHF backbone links 1,200 substations, with LTE backhaul slated for 2026 upgrades. VHF remains in use in civil aviation and maritime channels, governed by ITU reference tables, although domestic land users transition to digital UHF or LTE as licenses expire.

By End-User Industry: Utilities Emerge as Growth Engine

Utilities are growing at a 14.85% CAGR, driven by grid modernization projects and an increasing reliance on condition-based maintenance. Malaysia’s Tenaga Nasional refreshed 500 substation radios in 2024, integrating real-time switching instructions during outages. Government and public safety still top the absolute spend, holding 48.32% of the revenue, but their growth plateaus once migration milestones are complete.

Logistics, manufacturing, and hospitality add mid-tier PoC demand, illustrated by DHL’s 2024 decision to standardize Hytera radios region-wide for barcode scanning and route optimization. Private security and events favor rental bundles priced under USD 10 per day, underscoring the market’s diverse commercial tiers.

By Subscription Model: Managed Services Disrupt CapEx Norms

CapEx purchases claimed 57.21% transactions in 2025, yet the managed-service track rises at 14.31% CAGR as SMEs chase predictable opex and zero-maintenance obligations. Mobile Tornado launched USD 20 per-user bundles across Vietnam and the Philippines in 2024 that combine rugged Android handsets, unlimited talk, and web dispatch.

Smartcom’s tiered Thai offers scale up to THB 1,200 monthly when video streaming is required. Governments still lean toward outright ownership under public procurement rules, but provincial police in Indonesia and Vietnam now test subscription pilots when donor grants do not cover the infrastructure.

Geography Analysis

Indonesia generated 29.90% of 2025 revenue, making it the largest slice of the Southeast Asia internet radio market. National Police digital migration, PLN grid radios, and archipelagic coverage challenges together propel unit demand. LEO-satellite trials with Starlink ensure voice connectivity for eastern provinces and remote islands where LTE backhaul is scarce. Jakarta’s smart-city dashboards and Bali’s tourism hubs sustain commercial PoC adoption, while palm-oil estates in Kalimantan migrate to DMR units with GPS beacons for worker safety.

Vietnam is on track for a 15.44% CAGR, the region’s fastest clip. A USD 208 million Ministry of Public Security plan underwrites TETRA builds in Hanoi and Ho Chi Minh City. Industrial parks in Binh Duong enforce digital-radio standards for tenant factories, nudging analog out. FPT Telecom’s PoC cloud service extends managed options to SMEs that cannot afford trunked repeaters. The Philippines is expected to benefit from LTE coverage extended to 95% of municipalities by mid-2024. Globe Telecom’s partnership with Lynk Global will introduce satellite overlays in 2025, which are vital for the Mindanao and Visayas islands, where tower density is low. Rural fire brigades and municipal police shift from simplex VHF to PoC, lifting service-subscription counts. Malaysia maintains steady growth as Petronas, Tenaga Nasional, and Sarawak Energy complete phased TETRA refresh cycles. Regulator allocation of Band 31 for MCPTT in 2024 hints at future LTE/5G hybrids. Singapore’s spectrum policy and advanced fiber grid favor managed-service schemes and private LTE micro-cells. The Punggol Digital District serves as a showcase for integrated command centers, offering exportable templates for other ASEAN cities. Thailand’s Royal Thai Police finalized nationwide TETRA coverage in 2024. Bangkok’s MRT board sets the tone for public-transport adoptions, while industrial estates adopt dual-mode radios for chemical plants and refineries. The rest of Southeast Asia, including Cambodia, Laos, Myanmar, and Brunei, remains nascent; yet, Cambodia’s 2024 Phnom Penh DMR pilot signals early-stage uptake. Regional integration initiatives and cheaper Chinese radios could unlock latent demand within five years.

Competitive Landscape

First-tier vendors Motorola Solutions and Hytera accounted for approximately 58% of 2024 revenue, securing multi-year framework deals with police, utilities, and transportation agencies. Motorola leverages P25/TETRA interoperability and 20-year support pledges to command premium pricing, while Hytera undercuts by 20-30% yet delivers parallel feature sets, positioning itself for budget-tight provincial tenders.

Second-tier challengers include Tait, JVCKENWOOD, Sepura, and Icom, each specializing in dual-mode or narrow vertical applications such as metro rail and oil and gas. Tait’s LEO-enabled TP9600 showcases differentiation through satellite resilience, securing mining contracts in Indonesia’s eastern region. JVCKENWOOD’s NX-5000, launched in 2024, caters to utilities needing NXDN-DMR cross-compatibility.

Value-tier OEMs Inrico, Kirisun, and Qixiang increasingly flood the PoC segment with USD 180-250 units, pressuring distributor margins but widening addressable SME pools. Their limited local repair networks and slower firmware patch cadence restrict penetration into life-critical public-safety niches, yet the commercial and hospitality lanes remain fertile. Software layers become increasingly strategic as radio hardware becomes commoditized. Motorola’s WAVE PTX and Hytera’s SmartDispatch each topped 5,000 regional subscribers within six months of their 2024 upgrades, bundling push-to-talk with video, telephony, and shareable location data. Vendors that pair device fleets with cloud-native control rooms secure annuity revenue, shielding them from one-off hardware cycles.

Southeast Asia Internet Radio Industry Leaders

Motorola Solutions Inc.

Hytera Communications Corporation Limited

JVCKENWOOD Corporation

Icom Inc.

Uniden Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Motorola Solutions announced a multi-year expansion of its TETRA network infrastructure for Thailand's Royal Thai Police, adding 85 new base stations across southern provinces and upgrading dispatch systems in 12 regional command centers. The USD 42 million project integrates body-worn cameras and automatic vehicle location systems to enhance officer safety and improve border-security coordination, with completion scheduled for Q3 2026.

- September 2025: Hytera Communications secured a USD 35 million contract to deploy a nationwide DMR Tier III network for Malaysia's Fire and Rescue Department. Covering Peninsular Malaysia, Sabah, and Sarawak, the rollout includes 18,000 portable and mobile radios, 140 base stations, and a centralized dispatch platform that delivers real-time telemetry from fire trucks and ambulances, linking seamlessly with existing police and civil defense TETRA systems. Full operational capability is expected by mid-2027.

- August 2025: JVCKENWOOD Corporation partnered with Singapore's Land Transport Authority to supply 5,000 NEXEDGE NX-5000 digital radios for the Downtown Line and Thomson-East Coast Line. Valued at SGD 12 million (USD 9 million), the deal integrates the radios with centralized traffic control and automatic train supervision systems, while supporting dual NXDN and DMR modes for legacy interoperability. Installation began in September 2025 and is expected to be completed in Q1 2026.

- July 2025: Tait International and Telkomsat have launched a commercial low-earth-orbit satellite backhaul service for professional radio users across Indonesia's eastern archipelago, covering Papua, Maluku, and Nusa Tenggara. The hybrid service pairs Tait TP9600 DMR radios with Starlink terminals for automatic LTE-to-satellite failover. Early subscribers include mining firms, maritime patrol units, and provincial disaster agencies, at USD 85 per user per month, which includes unlimited voice and 5 GB of data.

- June 2025: Icom Inc. has introduced the IP601H, a next-generation LTE radio, for the Asia-Pacific markets. Featuring a 5.5-inch touchscreen, Android 14 OS, and an integrated thermal-imaging camera, the device targets fire departments and EMS teams in Singapore, Malaysia, and Thailand. It supports push-to-talk over cellular, video streaming, and third-party apps, with pricing starting at USD 680 per unit and airtime plans ranging from USD 22 per month. Initial shipments reached the Singapore Civil Defence Force in Jul 2025.

- May 2025: Sepura Limited supplied 4,500 SC21 TETRA radios to Indonesia's National Disaster Management Agency, replacing analog gear in 34 provincial command centers. The USD 18 million package, which includes five years of maintenance, delivers man-down alerts, lone-worker protection, and ETSI-compliant encrypted voice, and is now interoperable with the National Police’s existing TETRA network after the Sep 2025 rollout completion.

Southeast Asia Internet Radio Market Report Scope

The Southeast Asian internet radio market is studied through the sale of smart radio devices/terminals, which combine traditional analog radio, digital radio, and internet connectivity for communication purposes in the Southeast Asia region. Internet radios (also known as smart radio devices) are used for critical voice communication similar to two-way radios and can also be used for multimedia services and quick access to key data and mobile offices through a cellular/broadband internet network.

The Southeast Asian internet radio market is segmented into type (analog and digital), end-user industry (business use [government and public safety, utilities, and industry and commerce] and private use), and country (Indonesia, Malaysia, Singapore, Thailand, and rest of Southeast Asia region). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Analog |

| Digital |

| Push-to-talk Over Cellular (PoC) Radio |

| Dual-mode Rugged Radios |

| UHF |

| VHF |

| LTE/4G/5G |

| Government and Public Safety |

| Utilities |

| Industry and Commerce |

| Private Use |

| Capital Expenditure Device Purchase |

| Managed Service Subscription |

| Rental or Lease |

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Type | Analog |

| Digital | |

| By Internet Radio Terminal Type | Push-to-talk Over Cellular (PoC) Radio |

| Dual-mode Rugged Radios | |

| By Frequency Band | UHF |

| VHF | |

| LTE/4G/5G | |

| By End-user Industry | Government and Public Safety |

| Utilities | |

| Industry and Commerce | |

| Private Use | |

| By Subscription Model | Capital Expenditure Device Purchase |

| Managed Service Subscription | |

| Rental or Lease | |

| By Country | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How big will the Southeast Asia internet radio market be by 2031?

Forecasts peg the Southeast Asia internet radio market size at USD 389.06 million in 2031, reflecting a 12.05% CAGR from 2026.

Which country is growing the fastest?

Vietnam posts the quickest trajectory with a 15.44% CAGR on the back of a USD 208 million digital-radio blueprint for police and industry parks.

Why are utilities investing heavily in digital radios?

Grid-modernization programs require real-time voice plus telemetry, driving utilities toward TETRA, DMR Tier III, and PoC platforms that integrate GPS, SCADA, and fault-isolation workflows.

What is driving the shift from CapEx to managed services?

SMEs prefer subscription bundles that roll devices, airtime, and cloud dispatch into a single monthly fee, eliminating upfront hardware purchases and maintenance headaches.

How are vendors tackling coverage gaps in archipelagos?

Integrating low-earth-orbit satellite backhaul with dual-mode radios ensures continuous service when LTE drops, as shown by Telkomsat-Starlink and Globe-Lynk pilots.

Are cybersecurity risks slowing adoption?

Concerns about IP interception and weak encryption trim growth, but zero-trust updates such as Motorola’s WAVE PTX 4.9 and ETSI AES-256 standards are mitigating buyer hesitation.

Page last updated on: