Cognitive Radio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

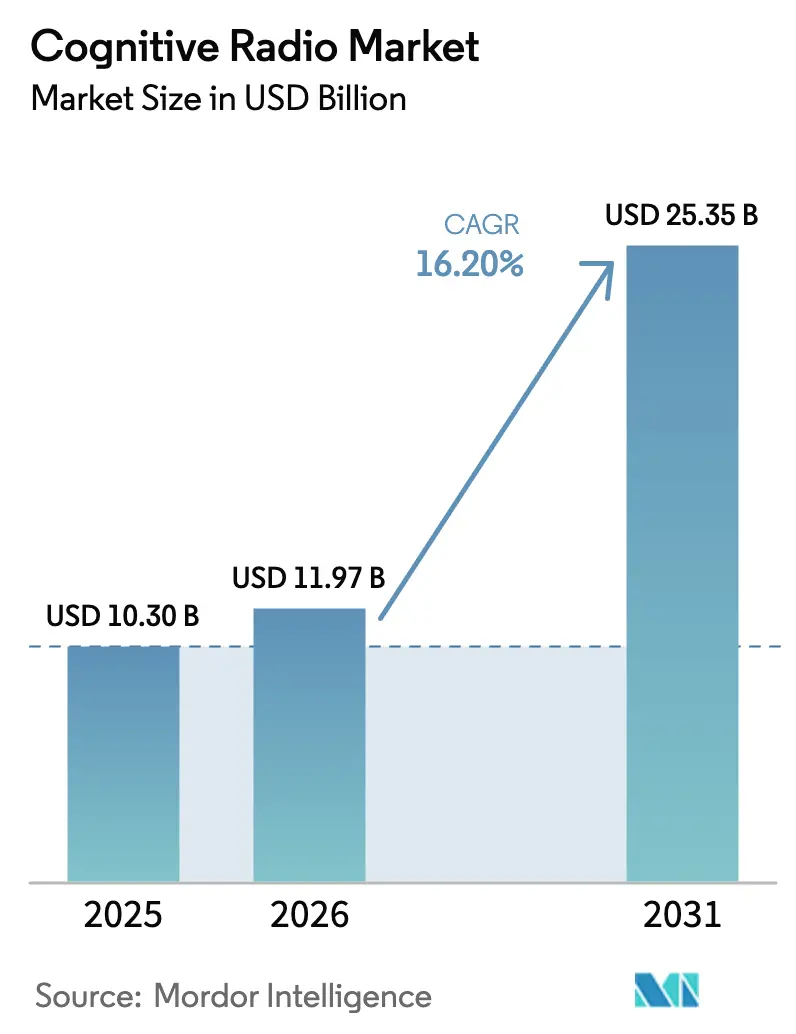

| Market Size (2026) | USD 11.97 Billion |

| Market Size (2031) | USD 25.35 Billion |

| Growth Rate (2026 - 2031) | 16.20% CAGR |

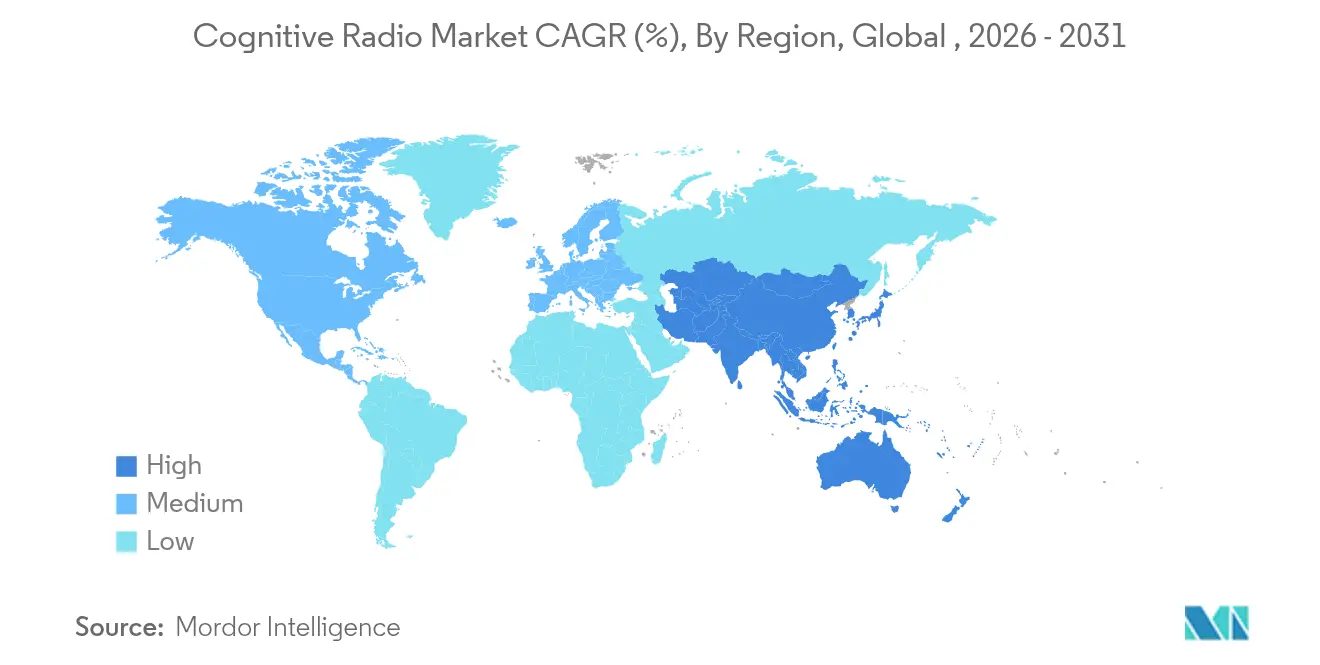

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

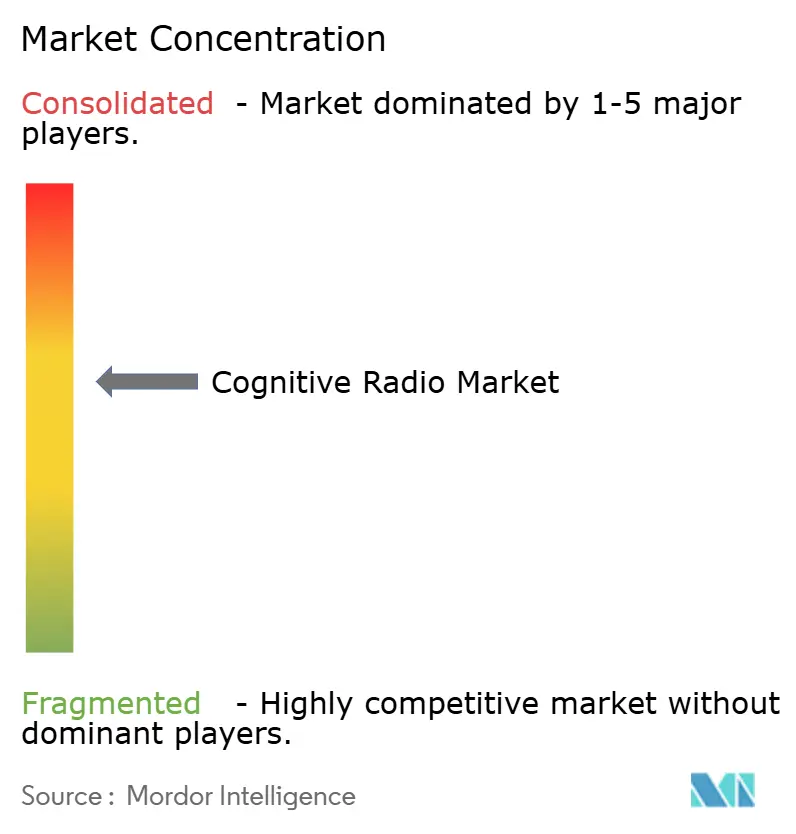

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Radio Market Analysis by Mordor Intelligence

The Cognitive Radio Market size was valued at USD 10.30 billion in 2025 and estimated to grow from USD 11.97 billion in 2026 to reach USD 25.35 billion by 2031, at a CAGR of 16.20% during the forecast period (2026-2031). Accelerated growth comes from widening mid- and high-band spectrum shortages, progress in artificial-intelligence-based sensing algorithms, and the pressing need to orchestrate 5G and early 6G networks on a dynamic, shared-spectrum basis. Governments endorse spectrum-sharing mandates and channel sizable research budgets toward testbeds, while defense agencies validate large-scale demonstrations that de-risk commercial adoption. Semiconductor incentives under the CHIPS Act bolster domestic semiconductor capacity, and millimeter-wave 5G rollouts drive demand for radios capable of agile beam steering and split-second spectrum handoffs. As chipset prices rise and AI workloads shift from the cloud to the radio edge, suppliers respond with vertically integrated designs and diversified sourcing strategies for raw materials to preserve their margins.

Key Report Takeaways

- By application, Spectrum Sensing and Allocation led with a 37.65% revenue share in 2025, while Cognitive Routing is projected to expand at an 18.12% CAGR through 2031.

- By component, Hardware captured 45.20% of the cognitive radio market share in 2025; Software and Firmware are forecast to grow at a 16.74% CAGR through 2031.

- By spectrum band, SHF (1-6 GHz) accounted for 40.55% of the cognitive radio market size in 2025, whereas EHF (More than 6 GHz) frequencies are set to climb at a 18.75% CAGR.

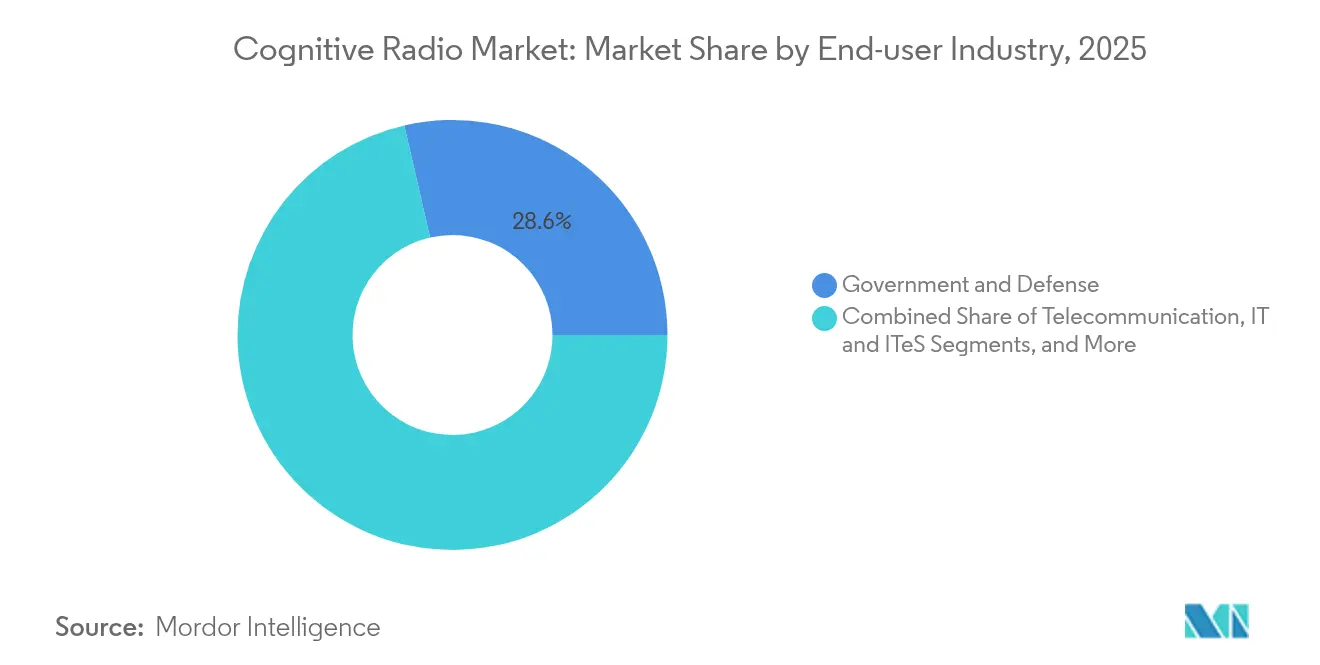

- By end-user industry, Government and Defense held a 28.60% share in 2025; Transportation and Logistics is poised to record a 17.25% CAGR by 2031.

- By network type, Opportunistic Spectrum Access networks accounted for 34.40% of 2025 sales; Cooperative Networks are expected to accelerate at an 18.25% CAGR through 2031.

- By geography, North America commanded 36.50% of 2025 revenues, while Asia Pacific is expected to post a 16.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cognitive Radio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing need to optimize spectrum utilization | +2.80% | North America, Europe | Medium term (2–4 years) |

| Rising deployment of 5G service applications | +3.20% | Asia Pacific, North America | Short term (≤ 2 years) |

| Surge in IoT-connected devices driving dynamic spectrum demand | +2.10% | Global – primarily in developed markets | Long term (≥ 4 years) |

| Government mandates for dynamic spectrum sharing frameworks | +1.90% | North America, Europe, Asia Pacific | Medium term (2–4 years) |

| AI-powered spectrum sensing algorithms mature | +2.40% | Global – telecom and defense innovation hubs | Long term (≥ 4 years) |

| Private 6G testbeds accelerating research and development funding | +2.70% | Asia Pacific, North America, select EU regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Need to Optimize Spectrum Utilization

Traffic growth is exhausting legacy allocations, prompting regulators to prioritize dynamic sharing policies that hinge on cognitive sensing. Citizens Broadband Radio Service rule updates alone unlocked service to 72 million more U.S. users without harming incumbent radars. New sensing engines scan wide swaths in milliseconds, and a USD 1.6 billion federal budget backs research aimed at reducing federal-commercial conflicts. Mid-band corridors remain the epicenter because they hold favorable propagation for 5G smartphones yet also host weather radars and defense systems. Vendors showcase chipsets that couple direct-RF sampling with on-chip AI inference to spot spectral holes on the fly. These advances let operators raise capacity without expensive new licenses, supporting the cognitive radio market’s long-run expansion.

Rising Deployment of 5G Service Applications

Dense 5G footprints require agile frequency management to sustain throughput targets within finite spectrum blocks. China has surpassed 228,700 base stations and is on track to achieve 60% user penetration by 2025, relying on cognitive scheduling to coordinate mid- and high-band carriers.[1]National Telecommunications and Information Administration, “National Spectrum Strategy Implementation Plan,” ntia.gov Japan issued 153 local 4.7 GHz licenses for private 5G, proving how context-aware radios enable factory networks inside tightly zoned channels. Integrated Sensing and Communication concepts for 6G merge radar and data links, further tightening spectral budgets. Vendors funnel multi-billion-dollar R&D investments into AI-native core software that leverages real-time spectrum intelligence to optimize traffic. As these deployments mature, the cognitive radio market secures a larger role in mobile-network reference designs.

Government Mandates for Dynamic Spectrum Sharing Frameworks

National roadmaps prioritize spectrum efficiency as a security measure. The U.S. Department of Defense plans its first multiband spectrum-sharing field trial in 2025, validating coexistence rules for radar and broadband services.[2]United States Department of Defense, “Joint Spectrum Sharing Trial,” defense.gov FCC band-manager models in the 4.9 GHz public-safety band enable licensed managers to allocate channels dynamically to those who can prove a real-time need. International agreements at WRC-23 harmonized cognitive-radio protocols, so equipment ships with fewer regional variants. Trilateral supply-chain pacts among the United States, Japan, and South Korea earmark critical minerals and testing hubs for cognitive chipsets, reinforcing ecosystem resilience.

AI-Powered Spectrum Sensing Algorithms Mature

Machine-learning models uplift detection accuracy beyond 96% in noisy IoT environments, letting radios move from reactive to predictive scheduling. Research on generative large language models, including RadioLLM, finds that hybrid methods achieve allocation accuracy significantly higher than classical heuristics. Hardware players embed GPU-class accelerators alongside converters so inference can stay local, cutting decision latency to microseconds. NVIDIA collaborates with carriers and defense labs to refine these edge inference stacks for future 6G meshes. Predictive awareness unlocks previously unusable fragments of the EHF spectrum and improves link resiliency for satellite-terrestrial handoffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of robust computational security infrastructure | −1.80% | Developing markets | Medium term (2–4 years) |

| Regulatory ambiguity on secondary spectrum usage rights | −2.10% | Global | Short term (≤ 2 years) |

| High capex for cognitive-enabled RF front-ends | −1.60% | Global, especially early-stage markets | Long term (≥ 4 years) |

| Scarcity of field-proven cognitive radio chipsets | −1.90% | Global – affects hardware-dependent applications | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lack of Robust Computational Security Infrastructure

Dynamic radios broaden the attack surface because adversaries can spoof sensing data or tamper with machine-learning models. Early blockchain-based sharing pilots achieve limited transaction throughput, slowing spectrum trades. Defense agencies test electromagnetic decoys to mask activity, but adversarial-AI countermeasures remain under active research. Quantum key distribution shows promise yet currently secures only kilobit-level streams over short ranges, falling short of field requirements. Until scalable, low-latency safeguards arrive, critical-infrastructure owners adopt wait-and-see postures that temper near-term uptake.

Regulatory Ambiguity on Secondary Spectrum Usage Rights

While governments promote sharing, specific liability rules for interference in secondary markets are still evolving. Operators weigh the risk of sudden policy shifts that could revoke access privileges mid-deployment. Divergent testing certifications across jurisdictions lengthen go-to-market cycles for multinational equipment suppliers. Small carriers fear that incumbent licensees may assert priority rights unpredictably, discouraging capital spending. Clearer dispute-resolution frameworks are required before the cognitive radio market fully penetrates highly regulated verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Spectrum Sensing Dominance, Cognitive Routing Momentum

Spectrum Sensing and Allocation controlled 37.65% of global 2025 revenue, solidifying its role as the prerequisite layer that every deployment must integrate. High-speed detectors satisfy FCC rules that demand incumbent radar protection within milliseconds. Mission-critical performance needs have prompted vendors to integrate direct-RF sampling with edge AI accelerators, enabling operators to gain near-instant insight into spectrum occupancy. Cognitive Routing, while smaller today, is scaling at an 18.12% CAGR as AI engines start to correlate link quality, user mobility, and latency budgets during path selection. Dynamic route adjustment becomes indispensable for vehicle-to-everything (V2X) rollouts, where split-second channel variations can jeopardize road safety alerts. Enterprises extend these principles to factory floor robots, ensuring reliable wireless coverage in metal-dense halls.

In quantitative terms, the cognitive radio market's size contributions from sensing currently surpass those from routing; however, routing augments overall system value by turning raw occupancy data into actionable decisions. As 6G testbeds merge sensing and communications, vendors bundle both features within a single stack, expanding average selling prices. Predictive frameworks that foresee network congestion and facilitate proactive resource allocation have bolstered double-digit growth in Location Detection and QoS Optimization. Emergency and satellite applications round out the portfolio, benefiting from multi-orbit handover mechanisms that let first responders switch from terrestrial to space links when terrestrial networks falter.

By Component: Hardware Strength, Software Acceleration

Hardware accounted for 45.20% of 2025 sales, thanks to continued demand for wideband converters, field-programmable gate arrays, and beam-steered antenna arrays. Direct-RF sampling chips, such as the AD9084, now digitize hundreds of megahertz of spectrum in a single step, thereby shrinking system footprints. That hardware base enables rapid gains in software value, which explains the 16.74% CAGR achieved by Software and Firmware. Vendors embed containerized microservices that continuously retrain spectrum models onsite, moving intelligence from the cloud to the edge. Services revenue rises as carriers seek system integrators to calibrate AI models for local propagation realities.

Over the forecast horizon, software gains steadily erode hardware-only differentiation because competing radio modules deliver similar noise figures and power outputs. Suppliers, therefore, highlight firmware update pipelines that extend field lifetimes without requiring board swaps. For users, this converts capex into opex and smooths upgrade paths that keep the cognitive radio market share of software on an upward glide path. Antenna innovation also marches ahead; electronically steerable arrays packaged with dual-band feeds support multi-orbit satellite roaming.

By Spectrum Band: SHF Prevails, EHF Accelerates

SHF (1-6 GHz) bands contributed 40.55% of 2025 revenue, buoyed by mid-band 5G launches that balance coverage with throughput. Citizens Broadband Radio Service stands out, having expanded affordable fixed-wireless access without displacing incumbent naval radar users. Meanwhile, EHF, the band above 6 GHz, is on a 18.75% CAGR trajectory because millimeter-wave cells shorten backhaul distances and feed augmented-reality endpoints with ultralow latency. The FCC recently unlocked 600 MHz at 37 GHz under flexible sharing rules that favor AI-driven beam management.

The cognitive radio market size in EHF remains smaller than that in SHF; however, the exploration of FR3 (7.125–24.25 GHz) widens the addressable opportunities for fixed-wireless, airborne, and backhaul links. Below-1 GHz options retain importance for massive IoT deployments demanding long reach at minimal power. With regulators eyeing cross-band neutrality, future radios will schedule traffic across several bands in parallel, strengthening vendor demand for multi-band synthesizers and ultrawide converter front ends.

By End-User Industry: Defense Core, Transportation Upswing

The government and Defense took a 28.60% share in 2025, reflecting steady procurement of jam-resistant, software-defined sets for land, sea, and air platforms. Large awards, such as a USD 85 million U.S. Navy contract for enhanced tactical links, sustain baseline volumes. Yet, the Transportation and Logistics sector is forecast to grow at a rate of 17.25% annually through 2031, driven by connected-vehicle mandates that require deterministic link reliability along highways and in densely urban areas. FCC rules pivoting the 5.9 GHz band toward C-V2X accelerate that shift.

Telecommunications carriers invest heavily as tighter spectral efficiency directly boosts EBITDA margins. Energy utilities are adopting cognitive radios for smart-grid self-healing functions and real-time distributed generation balancing. Healthcare and advanced manufacturing also emerge as growth nodes, replacing wired backbones with reconfigurable private 5G to enable surgical robotics and agile production lines.

By Network Type: Opportunistic Access Mainstay, Cooperative Networks Rise

Opportunistic Spectrum Access models represented 34.40% of 2025 billings, proving that mature sensing plus geo-location databases can let secondary users transmit while incumbents are idle. That success story is visible in the cognitive radio market share of Citizens Broadband Radio Service deployments, where real-time environmental sensing capability protects shipborne radars. Cooperative Networks, banking on blockchain-secured ledgers to automate spectrum swaps among operators, will grow 18.25% per year. The arrival of non-fungible spectrum tokens built on ERC4907 standards demonstrates credible settlement mechanisms without centralized brokers.

As 6G frameworks expand to multi-tier aerial, satellite, and terrestrial topologies, cooperative protocols will arbitrate between heterogeneous assets in milliseconds. Spectrum-sharing networks benefit from demonstration programs in the 37 GHz band that highlight co-equal federal-commercial usage, validating real-time dynamic rules. Collectively, these dynamics enlarge the overall cognitive radio market demand for distributed-ledger gateways and policy engines.

Geography Analysis

North America accounted for 36.50% of 2025 revenue and remains the leading market in regulatory innovation. The National Spectrum Strategy earmarks USD 6.6 billion for semiconductor buildouts and pilots that test dynamic sharing across low, mid, and high-band frequencies. Defense contractors such as L3Harris carry order backlogs exceeding USD 33 billion, which include spectrum-aware platforms for joint-all-domain operations. High civilian uptake mirrors aggressive fixed-wireless rollouts that bridge rural broadband gaps while preserving incumbent public-safety services.

Asia Pacific is projected to rise at a 16.95% CAGR as operators chase large addressable subscriber bases and governments treat 6G leadership as a strategic asset. China’s dense 5G macro-cell layer and 6G testbeds require radios able to juggle mid- and millimeter-wave assets, while Japan and South Korea incentivize private-5G licenses for factories and ports. Tri-lateral technology pacts among the three nations concentrate research funding on resilient supply chains and open-RAN experimentation.

Europe advances on the strength of vendor R&D and pan-EU harmonization. Ericsson allocated EUR 4.4 billion (USD 5.09 billion) to AI-native architectures in 2024, and Thales secured EUR 25.3 billion (USD 29.27 billion) in orders tied to defense communications. The EU’s Horizon Europe projects partner with Keysight to validate 6G radio prototypes, accelerating lab-to-field transition timelines. Cross-border alignment under ETSI reduces certification costs and supports multi-market equipment release strategies, cementing steady but less volatile regional growth.

Competitive Landscape

The market balances entrenched defense primes, large telecom vendors, and nimble software-radio specialists. Patent leadership sustains royalty streams. Ericsson alone booked roughly EUR 1.2 billion (USD 1.39 billion) in IPR revenue during 2024 and holds more than 60,000 active grants. M&A remains an accelerator, Motorola Solutions announced a USD 4.4 billion purchase of Silvus Technologies to fold advanced mesh algorithms into mission-critical portfolios. Keysight agreed to acquire Spirent to broaden test-emulation offerings, underscoring consolidation in measurement gear.

Hardware entrants pursue vertical integration to hedge semiconductor inflation, sourcing non-Chinese antimony and gallium while building captive packaging lines. Software-centric firms focus on edge-AI inference models that can be flashed onto any standards-compliant SDR, tilting competition toward algorithm depth and update cadence. Strategic alliances between cloud giants and carriers, such as NVIDIA’s AI-RAN program with T-Mobile, fuse hyperscale compute with radio resource management to shorten innovation cycles.

Emerging niches such as quantum-secured links motivate collaboration among defense contractors and photonics startups, exemplified by Elbit Systems’ successful 100-meter quantum key pilot. Collectively, players that pair robust IP with adaptive supply chains stand to capture outsized shares as the cognitive radio market transitions from early adoption into mainstream mobile and industrial fabric.

Cognitive Radio Industry Leaders

BAE Systems PLC

Thales Group

Raytheon Company

Rohde & Schwarz GmbH & Co KG

L3Harris Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The U.S. Department of Defense prepared its first wide-area spectrum-sharing demonstration, validating cognitive radios for multiband defense-commercial coexistence.

- March 2025: Thales reported EUR 25.3 billion order intake for 2024 and committed EUR 4 billion to R&D through 2028, emphasizing software-defined radios for aerospace and defense.

- March 2025: NVIDIA partnered with T-Mobile, MITRE, and Cisco to develop AI-native wireless networks targeting 6G spectral efficiency gains.

- February 2025: Ericsson launched a SaaS 5G core on Google Cloud featuring AI-guided troubleshooting and cognitive optimization.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cognitive radio market as the value generated from hardware, firmware, and software that autonomously senses, learns, and retunes across licensed or unlicensed spectrum to maximize utilization while respecting incumbent users. The definition covers units integrated in commercial telecommunications, defense, transportation, and industrial networks that ship with embedded cognitive engines or receive certified firmware upgrades.

Scope exclusion: Conventional software-defined radios that lack real-time spectrum-learning logic are not counted.

Segmentation Overview

- By Application

- Spectrum Sensing and Allocation

- Location Detection

- Cognitive Routing

- QoS Optimisation

- Other Applications

- By Component

- Hardware (RF Transceivers, SDR Modules, Antennas)

- Software and Firmware

- Services

- By Spectrum Band

- HF/VHF/UHF (Less than 1 GHz)

- SHF (1-6 GHz)

- EHF (More than 6 GHz, mmWave)

- By End-user Industry

- Telecommunication

- IT and ITeS

- Government and Defense

- Transportation and Logistics

- Energy and Utilities

- Other Industries

- By Network Type

- Opportunistic Spectrum Access (OSA)

- Spectrum Sharing

- Cooperative Networks

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed mobile-network planners, defense procurement officers, rural broadband operators, and chipset architects across North America, Europe, and Asia Pacific. These discussions clarified typical cognitive-radio penetration rates, spectrum-sensing performance thresholds, and evolving procurement budgets, which were vital for stress-testing secondary findings and refining assumptions.

Desk Research

We first mapped the addressable base using openly available, high-integrity sources such as FCC auction filings, ITU spectrum statistics, European Commission Radio Equipment Directive notices, US NTIA spectrum-sharing pilots, and peer-reviewed IEEE journals on dynamic spectrum access. Company 10-Ks, investor decks, and patent families (screened via Questel) provided shipment clues and average selling prices. News flow in Dow Jones Factiva, along with trade-association releases from the Wireless Innovation Forum, helped track policy shifts and deployment milestones. The sources cited above illustrate the breadth of secondary inputs; many additional publications were reviewed to cross-check data points.

Market-Sizing & Forecasting

A top-down demand pool was built from active cellular base-station counts and defense tactical-radio inventories, reconstructed through production and trade statistics, then benchmarked against sampled ASP × volume roll-ups from supplier channel checks. Bottom-up estimates plugged residual gaps where shipment visibility was limited. Key modelling variables include 5G site additions, government spectrum-sharing pilots, cognitive-chipset bill-of-materials trends, defense modernization outlays, and regulatory compliance deadlines. Multivariate regression, with 5G site growth and spectrum-sharing policy indices as leading drivers, underpins the 2025-2030 projection.

Data Validation & Update Cycle

Outputs pass a three-step review: automated variance scans, peer analyst audit, and senior sign-off. We revisit models annually, triggering interim refreshes when spectrum policy or major contract awards materially change the outlook.

Why Mordor's Cognitive Radio Baseline Stands Solid

Published estimates often diverge because firms choose different functional scopes, apply unlike adoption scenarios, or refresh on uneven cadences.

Key gap drivers for this market include whether software-defined radios without cognitive engines are counted, how aggressively 5G small-cell rollouts are projected, and the extent to which government R&D funds are folded into revenue. Mordor's scope stays disciplined around certified cognitive capability, our base-case adoption path mirrors publicly disclosed operator capex plans, and the model is re-benchmarked every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.30 B (2025) | Mordor Intelligence | - |

| USD 10.76 B (2025) | Global Consultancy A | Includes adjacent SDR hardware inflating total |

| USD 11.04 B (2025) | Market Analyst B | Uses aggressive IoT-device scenario and higher ASP ladder |

| USD 9.61 B (2024) | Regional Consultancy C | Excludes defense R&D spend captured in our scope |

These comparisons show that when scope breadth and variable selection vary, totals swing notably. Mordor's disciplined inclusion logic, transparent variables, and recurring validation give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the cognitive radio market?

The cognitive radio market stands at USD 11.97 billion in 2026 and is forecast to expand strongly through 2031.

Which application leads the market today?

Spectrum Sensing & Allocation holds the top position with 37.65% revenue share, reflecting the need for reliable interference detection in shared bands.

Why is Asia Pacific the fastest-growing region?

Aggressive 5G rollouts in China, Japan, and South Korea, combined with government-funded 6G testbeds, push regional growth at a 16.95% CAGR.

How are AI advances influencing cognitive radios?

Machine-learning algorithms raise sensing accuracy, enable predictive routing, and let operators reclaim idle spectrum fractions, boosting overall network efficiency.

What security challenges do cognitive radios face?

Expanded attack surfaces from dynamic control paths and AI models demand new safeguards, with quantum key distribution and blockchain emerging as promising but still maturing solutions.

Which spectrum band is growing the fastest?

EHF frequencies above 6 GHz are forecast to grow at 18.75% annually, propelled by millimeter-wave 5G and early 6G pilot deployments.

Page last updated on: