Global Aptamers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 4.55 Billion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Aptamers Market Analysis by Mordor Intelligence

The aptamer market size was valued at USD 2.05 billion in 2025 and estimated to grow from USD 2.34 billion in 2026 to reach USD 4.55 billion by 2031, at a CAGR of 14.22% during the forecast period (2026-2031). Momentum comes from regulatory validation, accelerated discovery powered by artificial intelligence, and rising deployment in precision diagnostics and targeted therapeutics. The U.S. Public Health Emergency Medical Countermeasures Enterprise has earmarked USD 79.5 billion for 2023-2027, a sizable funding pool that is spurring rapid pathogen-sensor development and directly benefiting the aptamer market [1]Source: Jing Zhang et al., “Prediction of Aptamer Affinity Using an Artificial Intelligence Approach,” pubs.rsc.org . Breakthroughs such as the FDA approval of IZERVAY for geographic atrophy in 2023 and the 2025 debut of UltraSELEX, which completes selection in a single round, are lowering risk perceptions and compressing development timelines. Alongside these drivers, microfluidic automation and enzymatic DNA synthesis are easing manufacturing constraints, although analytical-grade oligonucleotide capacity remains a near-term bottleneck that could temper expansion despite strong underlying demand

Key Report Takeaways

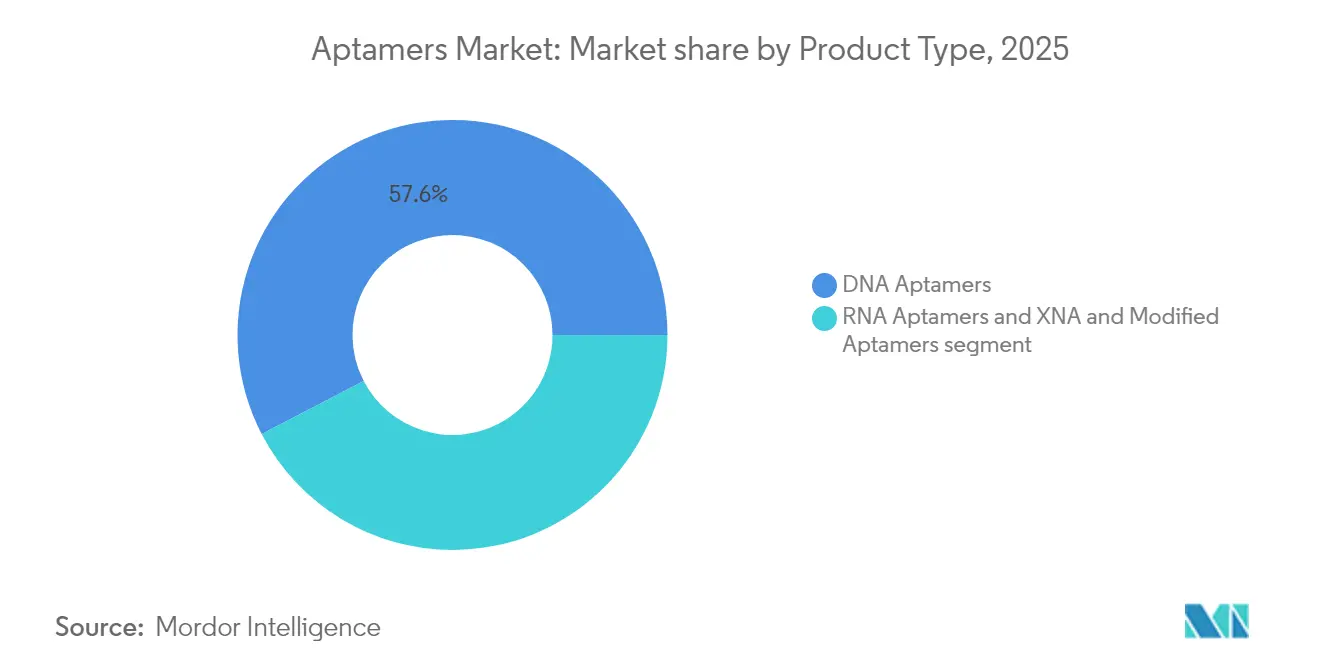

- By product type, DNA aptamers led with 57.62% of aptamer market share in 2025, while RNA aptamers are poised to advance at a 15.22% CAGR through 2031.

- By application, diagnostics commanded 45.90% share of the aptamer market size in 2025, whereas therapeutics applications are projected to expand at a 15.44% CAGR to 2031.

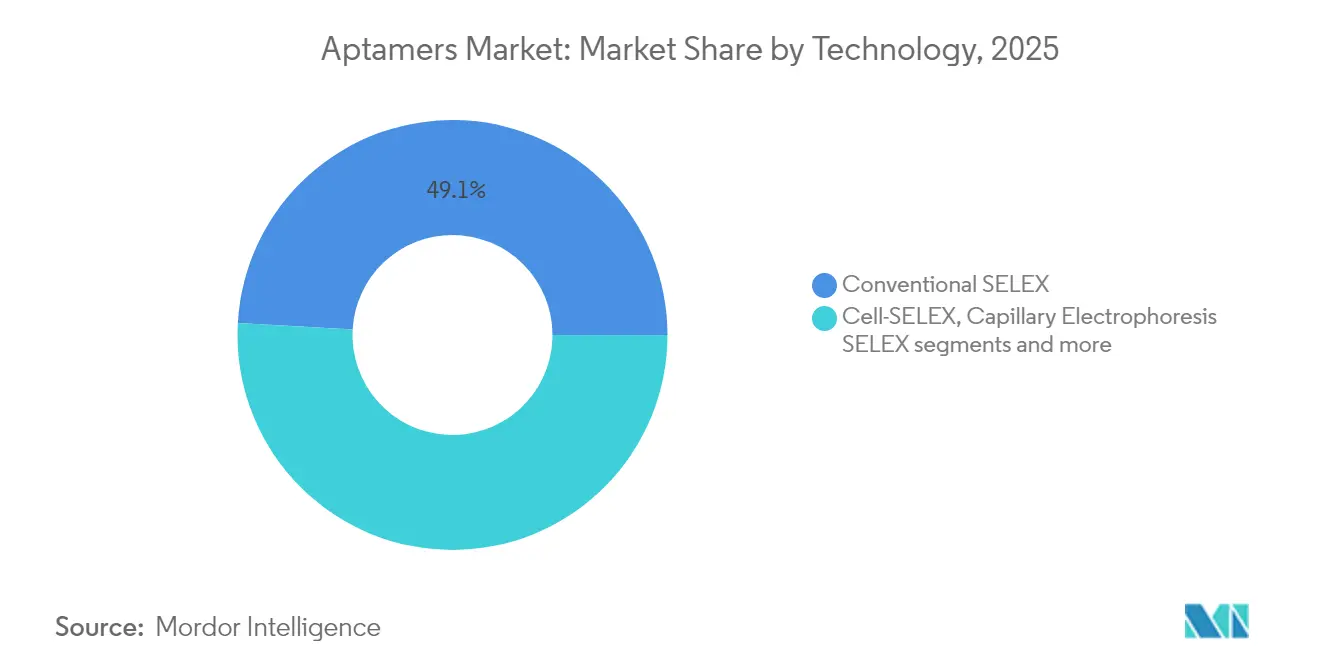

- By technology, conventional SELEX retained 49.12% share of the aptamer market size in 2025; microfluidic SELEX is the fastest-growing segment at 16.05% CAGR.

- By end user, pharmaceutical and biotechnology companies held 40.70% share of the aptamer market size in 2025 and are expected to grow at 16.78% CAGR through 2031.

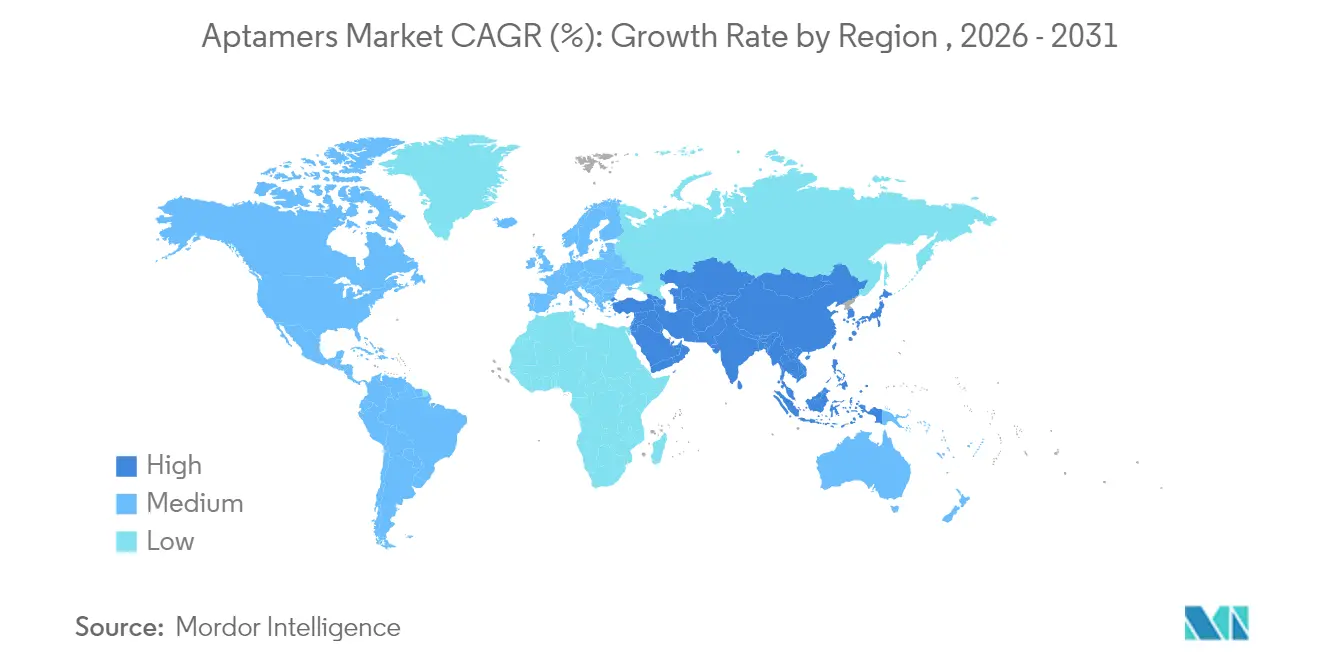

- By geography, North America dominated with 44.10% aptamer market share in 2025, while Asia-Pacific is the fastest-expanding region with a 17.28% forecast CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aptamers Market Trends and Insights

Gen AI-accelerated in-silico aptamer discovery

Artificial-intelligence models now predict binding affinities with close to 90% accuracy, cutting conventional SELEX cycles from months to weeks [2]Source: Administration for Strategic Preparedness and Response, “Public Health Emergency Medical Countermeasures Enterprise Multiyear Budget: Fiscal Years 2023-2027,” aspr.hhs.gov . UltraSELEX, disclosed in 2025, completes candidate identification in a single screening round, pushing discovery throughput to unprecedented levels. AI-driven platforms collectively raised more than USD 2 billion in venture capital during 2024, validating commercial confidence in algorithm-guided selection. Firms adopting AI-enhanced workflows report 60-80% cost reductions per candidate, a differential that is redefining competitive barriers. As discovery economics improve, smaller companies are entering the aptamer market, intensifying innovation and collaboration activity.

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gen AI-accelerated in-silico aptamer discovery | +2.8% | Global, with concentration in North America & China | Medium term (2-4 years) |

| Rising demand for ultra-sensitive diagnostics (sub-pico-molar LoD) | +3.2% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Growth of mRNA/LNP platforms enabling RNA aptamer co-formulation | +2.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Funding surge for novel bispecific aptamer–drug conjugates | +1.9% | North America & Europe | Long term (≥ 4 years) |

| Mainstream SELEX automation lowering cost per candidate | +2.4% | Global | Short term (≤ 2 years) |

| Government pandemic-preparedness grants for rapid pathogen sensors | +1.8% | North America & Europe, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for ultra-sensitive diagnostics (sub-pM LoD)

Point-of-care settings and precision-medicine workflows require assays that identify biomarkers at femtomolar levels. Aptamer-based sensors routinely achieve sub-1 pM limits of detection, outperforming enzyme-linked immunoassays by 2-3 orders of magnitude. COVID-19 underscored the value of rapid, sensitive pathogen screening, catalyzing sustained investment in next-generation diagnostic formats. Electrochemical aptasensors now detect cardiac troponin at 10 pg/mL, enabling early myocardial infarction triage in emergency departments. Integration with microfluidic chips reduces sample volumes to microliters, a critical benefit for pediatric and geriatric testing scenarios. These performance gains reinforce the aptamer market’s positioning against antibody-centric technologies.

Growth of mRNA/LNP platforms enabling RNA aptamer co-formulation

Successes in mRNA vaccination have normalized lipid nanoparticle (LNP) delivery, opening co-formulation pathways for RNA aptamers. Combined LNP-aptamer constructs demonstrate 10-fold improvements in cell-specific uptake relative to naked mRNA. Pharmaceutical pipelines targeting oncology and liver disease increasingly license aptamer ligands to sharpen tissue selectivity, as evidenced by an AstraZeneca–Aptamer Group collaboration announced in 2024. As formulation toolkits mature, RNA aptamers transition from research curiosities to core components of next-generation nucleic-acid medicines.

Funding surge for novel bispecific aptamer–drug conjugates

Bispecific aptamer constructs exploit dual binding to tumor antigens and immune cells, localizing potent cytotoxins while limiting systemic exposure. University of Illinois scientists reported 40% leukemia stem-cell reduction with one such construct in 2025. Venture financing for aptamer therapeutics topped USD 500 million in 2024, with bispecific programs commanding premium valuations. Regulatory review remains intricate because agencies evaluate both aptamer targeting specificity and payload safety, yet the FDA’s IZERVAY decision shows a workable path for nucleotide-modified agents. These developments elevate the therapeutic relevance of the aptamer market and expand its strategic collaborations with oncology drug developers

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intellectual-property thickets around modified nucleotides | -1.40% | Global, particularly North America & Europe | Long term (≥ 4 years) |

| Analytical-grade oligo synthesis capacity bottlenecks | -2.10% | Global, most acute in North America | Short term (≤ 2 years) |

| Low clinician familiarity versus antibodies | -1.20% | Global, varying by healthcare system maturity | Medium term (2-4 years) |

| Stringent FDA CMC expectations for oligo impurities | -0.80% | North America, with spillover to global markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intellectual-property thickets around modified nucleotides

More than 130 patents for 2'-modified nucleotides were filed between 2020-2024, creating overlapping claims that complicate freedom-to-operate analyses. Developers often negotiate complex cross-licensing deals, an expensive hurdle for smaller entrants and a deterrent to geographic expansion. Enforcement is strongest in the United States and Europe, prompting some firms to pivot early-stage R&D into jurisdictions with lighter patent scrutiny. Strategic partnerships mitigate the issue but can dilute long-term economics. Until landmark licensing frameworks emerge, intellectual-property uncertainty will remain a drag on aptamer market growth.

Analytical-grade oligo synthesis capacity bottlenecks

Demand for high-purity oligonucleotides from aptamer, antisense, and mRNA modalities outstrips current supply by an estimated 40% heading into 2026. Solid-phase synthesis struggles with diminishing coupling efficiency beyond 50-mer sequences, limiting throughput. North American plants carry the bulk of installed capacity, making the region vulnerable to supply shocks. Industry investment in enzymatic DNA synthesis and microfluidic reactors is accelerating, yet commercial-scale output is at least two years away. Near-term tightness risks delaying clinical timelines and inflating costs across the aptamer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: DNA Aptamers Maintain Leadership as RNA Platforms Accelerate

DNA aptamers accounted for 57.62% of aptamer market share in 2025, reflecting their superior nuclease stability and well-established production workflows. Diagnostics developers favor DNA scaffolds for room-temperature robustness, a key requirement for decentralized testing. The aptamer market size for DNA aptamers thereby remained the largest revenue contributor, anchored by strong demand from cardiac, infectious-disease, and environmental assays.

RNA aptamers are expected to grow at a 15.22% CAGR to 2031 on the back of mRNA-lipid nanoparticle co-formulation advances that mitigate historical stability challenges. Modified XNA forms achieve binding affinities up to 100-fold stronger than native sequences, albeit within a complex patent landscape. Pharmaceutical firms are signing option deals that attach milestone-rich structures to access RNA aptamer intellectual property, signaling confidence in clinical translation. This momentum diversifies the product mix and reinforces technology-driven competition within the aptamer market.

By Application: Therapeutics Gain Momentum Beyond Diagnostic Foundations

Diagnostics retained 45.90% share of the aptamer market size in 2025, underpinned by high-sensitivity biosensor rollouts in infectious-disease and cardiac triage settings. Laboratories embrace aptamer-based electrochemical and FET platforms because they deliver antibody-level specificity without cold-chain dependence.

Therapeutics exhibit the fastest expansion at 15.44% CAGR, a trajectory catalyzed by IZERVAY’s 2023 approval and encouraging oncology proof-of-concept data. The aptamer market size for therapeutics is projected to close the gap with diagnostics as bispecific conjugates reach clinical-phase milestones. Persistent awareness gaps among clinicians constitute a soft barrier, yet growing publication volume and targeted education are narrowing this divide, positioning therapeutic programs as the next major revenue pillar.

By Technology: Microfluidic SELEX Redefines Discovery Economics

Conventional SELEX retained 49.12% of the aptamer market share in 2025, a testament to entrenched protocols and sunk capital in legacy equipment. Academic labs value its flexibility in accommodating diverse targets, sustaining baseline demand.

Microfluidic SELEX is forecast to register a 16.05% CAGR to 2031. Magnetically activated continuous deflection chips demonstrated nanomolar-affinity aptamer isolation in six rounds, half the cycle count of traditional approaches pubs.rsc.org. Automated reagent handling slashes consumable costs ten-fold, broadening access for smaller institutes and contract research organizations. As reagent savings compound, the aptamer market expects a steady pivot toward microfluidic workflows, reshaping supplier demand for instrumentation and consumables.

By End User: Pharmaceutical Uptake Signals Market Maturation

Pharmaceutical and biotechnology companies commanded 40.70% share of the aptamer market size in 2025 and are expanding at 16.78% CAGR. Their participation underscores technology maturation and validates regulatory clarity for nucleotide-modified products. Capital-rich firms also finance scalability upgrades in oligonucleotide manufacturing, indirectly benefiting the entire value chain.

Contract research organizations gain traction as outsourcing partners, filling expertise gaps in SELEX optimization and regulatory documentation. Academic institutes continue to seed innovation, while hospital laboratories adopt FDA-cleared aptamer assays as reimbursement coverage stabilizes. The Standard BioTools-SomaLogic merger exemplifies a consolidation wave that combines tool providers with large bio-databases to offer integrated discovery-to-diagnostics services. Such moves reinforce competitive scale and deepen data moats inside the aptamer market.

Geography Analysis

North America held 44.10% aptamer market share in 2025 on the strength of its established biotech ecosystem, supportive regulatory framework, and USD 79.5 billion PHEMCE funding pipeline. FDA guidance following IZERVAY’s approval clarified chemistry-manufacturing-controls expectations for oligonucleotide impurities, accelerating therapeutic filings. Venture-capital inflows and well-capitalized instrument suppliers foster continuous platform upgrades. Production bottlenecks in analytical-grade oligos could temporarily cap growth, but ongoing investments in enzymatic synthesis plants are expected to ease pressure from 2027 onward.

Europe delivers steady revenue backed by advanced healthcare infrastructure and coordinated regulatory oversight from the European Medicines Agency. Germany’s analytical-instrumentation strength and France’s biotech research clusters provide fertile ground for diagnostic innovation. The United Kingdom maintains momentum despite Brexit through partnerships such as Aptamer Group’s projects in liver fibrosis and Alzheimer’s testing. Reimbursement policies favor high-value assays, making Europe an attractive launchpad for premium diagnostics and early-phase therapeutics.

Asia-Pacific is the fastest-growing region with a projected 17.28% CAGR through 2031. China invested more than CNY 20 billion (USD 2.8 billion) of public funds into biotech in 2023 and now hosts 27% of the global pipeline merics.org. Japan’s sophisticated pharma sector and Australia’s translational-research hubs further expand the addressable base. India and South Korea provide cost-competitive manufacturing and electronics capabilities that align with microfluidic SELEX automation. Intellectual-property complexities persist, yet government incentives and expanding local manufacturing temper risk perceptions, positioning the region as an essential growth engine for the aptamer market

Competitive Landscape

The competitive field is moderately concentrated, with intellectual-property depth and discovery automation defining advantage. The Standard BioTools-SomaLogic combination created a life-sciences tools leader holding over USD 500 million in cash and targeting USD 80 million in annual cost synergies by 2026. Aptamer Group leverages its Optimer platform to strike cross-sector licensing agreements, including a 10% royalty deal with the University of Glasgow for a swine-vaccine application news-medical.net. These moves highlight a strategic pivot toward scale and vertical integration.

White-space opportunities remain in targeting “undruggable” proteins and deploying aptamers as tissue-specific mRNA carriers. AI-powered discovery start-ups aim to commoditize SELEX by delivering optimized sequences within days, challenging incumbents that rely on more labor-intensive protocols. Manufacturing automation, especially microfluidic continuous-flow reactors, is emerging as a competitive battleground that can alleviate synthesis bottlenecks while improving gross margins. More than 130 patent filings covering modified nucleotides since 2020 signal an arms race for foundational chemistry assets that will shape long-term royalty streams.

In therapeutics, partnerships with large pharmaceutical companies provide critical validation and non-dilutive capital. Examples include AstraZeneca’s evaluation of Optimer vehicles for siRNA delivery and Moderna’s exploratory work on aptamer-guided LNP targeting. As clinical assets progress, the aptamer market expects heightened M&A activity as toolmakers and drug developers seek synergistic portfolios.

Global Aptamers Industry Leaders

Aptagen, LLC

Aptamer Sciences Inc.

Base Pair Biotechnologies Inc.

Aptamer Group

Aptus Biotech S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EPFL unveiled the MEDUSA technique for generating ultra-selective

- April 2025: 4basebio secured MHRA GMP certification and raised GBP 40 million to expand synthetic DNA output.

- December 2024: Aptamer Group signed a GBP 155,000 contract to create two Optimer binders for RNA therapy monitoring.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global aptamers market as the revenue earned from synthetic single-stranded DNA, RNA, or chemically modified nucleic acid sequences that are selected through SELEX-style platforms and then commercialized as diagnostic reagents, therapeutic actives, or specialized research tools. We capture value at the point an aptamer-based product or service is invoiced to pharmaceutical or biotech companies, clinical laboratories, contract research organizations, or academic institutes, thereby covering the full economic footprint of the molecule.

Scope exclusion: Screening-only service fees for peptide aptamers and multiplex assay kits where aptamers are minor ancillary reagents are omitted.

Segmentation Overview

- By Product Type (Value)

- DNA Aptamers

- RNA Aptamers

- XNA & Modified Aptamers

- By Application (Value)

- Diagnostics

- Therapeutics

- Research & Development

- Others

- By Technology (Value)

- Conventional SELEX

- Cell-SELEX

- Capillary Electrophoresis SELEX

- Microfluidic & Microarray SELEX

- Other Emerging SELEX Variants

- By End User (Value)

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

- Hospitals & Clinical Laboratories

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with R&D directors, diagnostic lab managers, CRO procurement leads, and regulatory advisors across North America, Europe, and Asia-Pacific. These conversations validate addressable volumes, typical contract values, and rollout timelines, while short surveys with hospital pharmacists and biotech business-development teams stress-test price and penetration curves.

Desk Research

We begin with tier-one life-science sources such as NIH RePORTER grants, FDA device and drug approvals, Eurostat biotech production indices, and customs data accessed through Volza. Complementary context is drawn from bio-industry association white papers, peer-reviewed journals, and public 10-K filings that disclose royalty or milestone income. Our paid dashboards, D&B Hoovers for company financials and Questel for patent volumes, help confirm the commercial standing of leading developers. These examples are illustrative; many additional sources inform our evidence base.

A follow-up sweep tracks import price shifts, venture investments, and regional regulatory decisions that signal near-term demand inflections and sharpen our preliminary sizing before reaching out to experts.

Market-Sizing & Forecasting

We build the 2025 baseline through a top-down reconstruction of global aptamer production and trade flows, then cross-check totals with bottom-up snapshots of average selling price multiplied by unit volumes from a sampled supplier set. Model inputs include SELEX throughput expansion, active clinical-trial counts, diagnostic kit placements, median grant outlays, exchange-rate shifts, and reimbursement milestones. Forecasts to 2030 rely on multivariate regression with scenario analysis, tuned by expert consensus on pipeline attrition and kit replacement cycles. Where supplier data run thin, totals are aligned to macro indicators such as NIH aptamer-tagged awards to avoid double counting.

Data Validation & Update Cycle

Outputs pass a three-tier analyst review that flags deviations beyond two standard deviations from historical growth bands; at that point, at least two primary sources are re-contacted. Models refresh annually, with interim updates triggered by major regulatory approvals or withdrawals, and a final sense-check occurs immediately before publication.

Why Mordor's Aptamers Market Baseline Commands Reliability

Published estimates diverge because firms bundle dissimilar product mixes, choose different currency dates, or apply varying success probabilities to early-stage pipelines.

Key gap drivers observed include some publishers merging peptide aptamer discovery fees with nucleic-acid reagent sales, others assuming uniform price erosion, and a few applying aggressive clinical success rates that our analysts temper after expert calls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.05 billion (2025) | Mordor Intelligence | - |

| USD 2.34 billion (2023) | Regional Consultancy A | Broader scope adds peptide aptamers and screening fees |

| USD 5.90 billion (2025) | Trade Journal B | Includes research funding alongside commercial sales |

| USD 0.34 billion (2026) | Global Consultancy C | Focuses only on SELEX kits and reagents |

The Mordor value stems from the 2025 edition of our report. The 2.34-billion, 5.90-billion, and 342-million figures are drawn respectively from a 2023 study by a regional consultancy, a 2025 trade journal outlook, and a 2021-2026 forecast by a global consultancy. These comparisons show that Mordor's disciplined scope selection, balanced probability modeling, and annual refresh cadence provide a dependable middle-path baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Global Aptamers Market?

The Global Aptamers Market size is expected to reach USD 2.34 billion in 2026 and grow at a CAGR of 14.22% to reach USD 4.55 billion by 2031.

What is the current size of the aptamer market?

The aptamer market size stands at USD 2.34 billion in 2026 and is forecast to reach USD 4.55 billion by 2031.

Which region leads the aptamer market and why?

North America leads with 44.10% market share due to strong regulatory clarity, abundant venture funding, and significant government grants for pathogen-sensor platforms.

Which application segment is growing fastest?

Therapeutic applications are expanding at a 15.44% CAGR, driven by the first FDA-approved aptamer drug and progress in oncology-focused conjugates.

How are artificial intelligence tools influencing aptamer discovery?

AI models shorten SELEX cycles from months to weeks and cut candidate identification costs by up to 80%, boosting pipeline velocity and lowering barriers to entry.

What is the main manufacturing challenge facing the aptamer market?

Analytical-grade oligonucleotide synthesis capacity is insufficient to meet near-term demand, creating production bottlenecks that could delay clinical programs.

Page last updated on: