Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

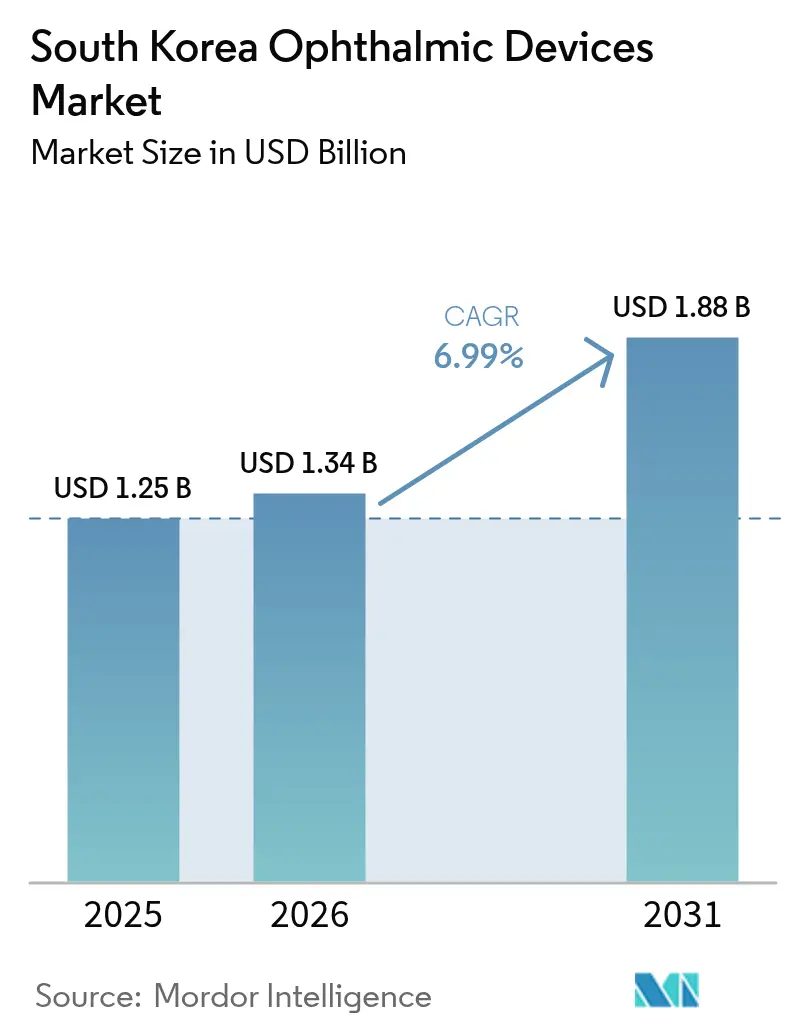

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

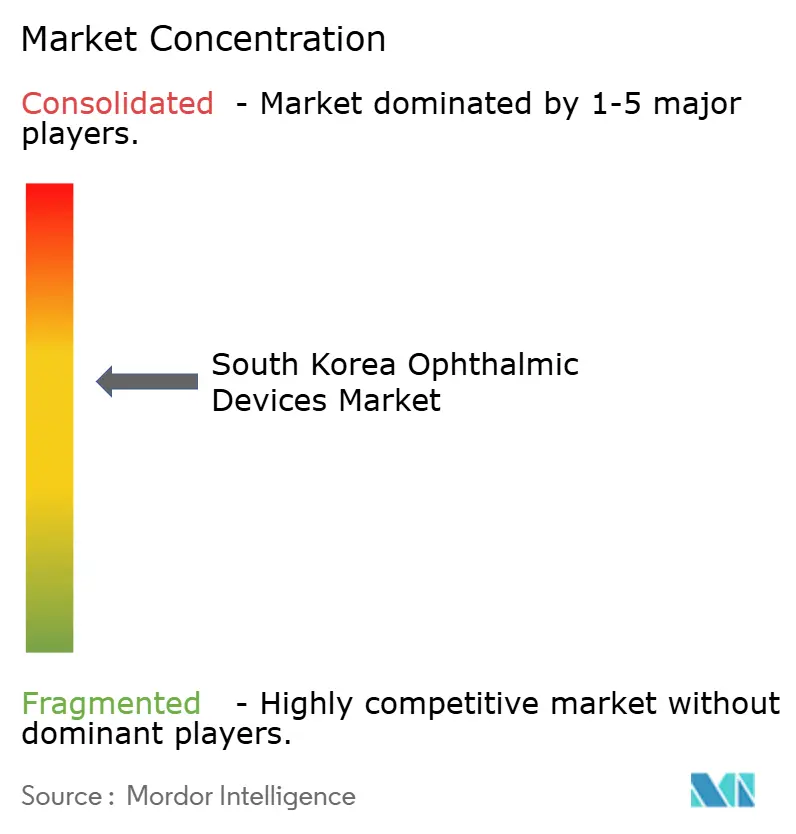

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Ophthalmic Devices Market Analysis by Mordor Intelligence

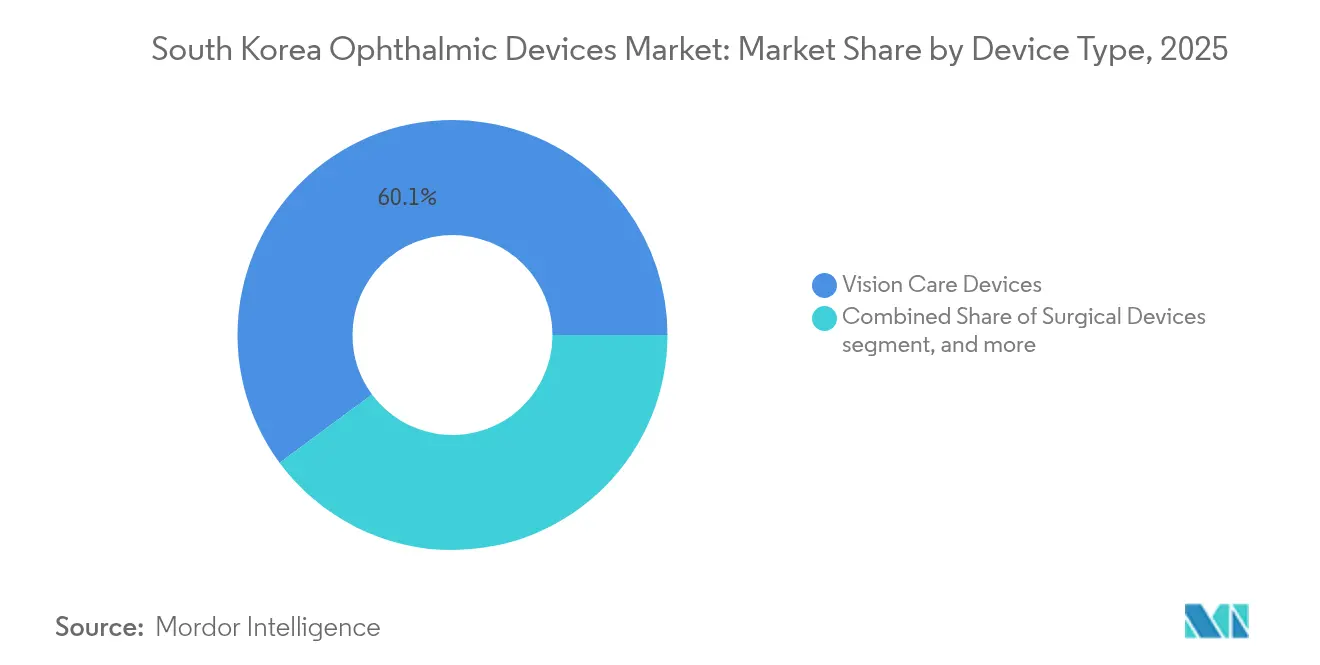

The South Korea ophthalmic devices market size was valued at USD 1.25 billion in 2025 and estimated to grow from USD 1.34 billion in 2026 to reach USD 1.88 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). Spiralling myopia rates, an older population that demands spectacle-free vision, and public reimbursements for early glaucoma detection underpin steady expansion. In 2024, vision-care products already accounted for 60.8% of the South Korea ophthalmic devices market as contact lenses, ortho-k lenses, and blue-light filters converged with fashion trends. Diagnostic hardware is catching up quickly; wide-field OCT angiography and AI-enabled fundus cameras are advancing at 9.23% CAGR on the back of new screening mandates. Hospitals command 43.6% of device placements, yet ambulatory surgery centres are carving share by offering day-case cataract and SMILE procedures. Multinational suppliers face long Ministry of Food and Drug Safety (MFDS) approval cycles, but they offset delays through joint ventures that localise service and training networks.

Key Report Takeaways

- By device type, vision-care products led with 60.12% of South Korea ophthalmic devices market share in 2025, while diagnostic and monitoring units record the fastest 9.08% CAGR to 2031.

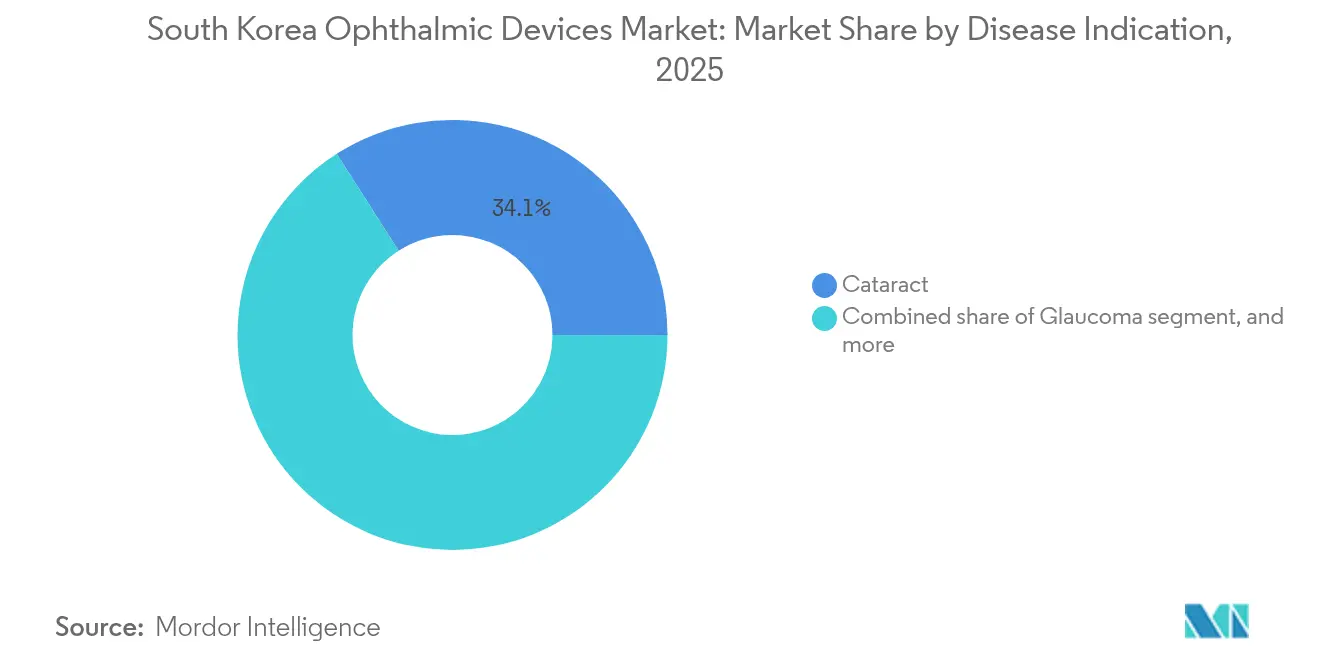

- By disease indication, cataract contributed 34.05% of the South Korea ophthalmic devices market size in 2025; diabetic-retinopathy solutions post the quickest 8.28% CAGR through 2031.

- By end-user, hospitals controlled 43.02% of 2025 revenues; ambulatory surgery centres are forecast to expand at an 8.12% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of premium IOLs among South Korea’s aging population | +1.8% | Seoul, Busan, Daegu | Medium term (2 – 4 years) |

| Government reimbursement expansion for nationwide glaucoma screening | +1.2% | Rural counties and provincial cities | Long term (≥ 4 years) |

| High penetration of LASIK driven by cosmetic-surgery culture | +0.9% | Seoul metropolitan area | Short term (≤ 2 years) |

| Growth of private-hospital health-check-up packages featuring OCT | +1.5% | Major hospitals nationwide | Medium term (2 – 4 years) |

| Surging myopia incidence in adolescents boosting diagnostic-device demand | +1.6% | Urban school districts | Long term (≥ 4 years) |

| Domestic AI-based ophthalmic diagnostic start-ups achieving MFDS approvals | +1.0% | National | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Premium IOLs Among the Aging Population

Multifocal optics reshaped cataract workflows, climbing from 16% usage in 2018 to 29% in 2020 and seizing 53.56% of the domestic IOL segment in 2023. Femtosecond laser-assisted cataract surgery expanded from 5% to 29% of cases over the same period, aided by 96% penetration of optical biometry. RxSight’s Light Adjustable Lens delivered unaided 20/20 vision to 70% of recipients versus 40% with other premium alternatives, bolstering surgeon uptake.

Government Reimbursement Expansion for Nationwide Glaucoma Screening

New National Health Insurance rules cover wide-field OCT angiography, which shows 87.28% sensitivity and 86.94% specificity for glaucoma diagnosis compared with legacy OCT units[1]Hong-Seok Hong et al., “Wide-Field OCT-Angiography for Glaucoma,” PLOS ONE, journals.plos.org. The initiative tackles disparities across 20 counties lacking any eye clinic, shrinking average travel time to specialised diagnostics.

High LASIK Penetration Driven by Cosmetic-Surgery Culture

Seoul’s refractive centres perform LASIK, LASEK, and SMILE at prices near USD 2,700, roughly one-third of typical Western tariffs. A 317-Hz excimer-laser study recorded 97.8% of treated eyes at 20/25 vision or better nine months after surgery, with patient satisfaction jumping from 27.7% to 98.1%.

Surging Myopia Incidence in Adolescents

Nationwide surveys report 65.4% myopia prevalence in children aged 5-18, while 19-year-old male conscripts in Seoul exhibit 96.5% prevalence; high myopia raises glaucoma odds 4.6-fold[3]National Center for Biotechnology Information, “Myopia Prevalence in Korean Youth,” ncbi.nlm.nih.gov. These trends spur demand for autorefractors, axial-length trackers, and low-dose atropine dispensing systems.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent MFDS approval timelines versus global peers | −1.2% | Nationwide | Short term (≤ 2 years) |

| Foreign-exchange cost volatility from heavy import dependence | −0.8% | Nationwide; higher exposure for rural providers | Medium term (2 – 4 years) |

| Shortage of trained ophthalmic surgeons outside Seoul Capital Area | −1.5% | 20 counties with no clinics | Long term (≥ 4 years) |

| Price caps on cataract-surgery reimbursement limiting premium devices | −1.0% | National | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Stringent MFDS Approval Timelines

AI-enabled scanners and new lens polymers fall into Class 3-4 risk categories. The Digital Medical Products Act of January 2024 demands extra cybersecurity validation, stretching launch cycles and raising documentation costs.

Foreign-Exchange Cost Volatility

Roughly 70% of high-end devices are imported. Won-dollar swings compress margins for smaller hospitals even though overall GDP is expected to grow 2.2% in 2024. Domestic suppliers see openings for mid-priced OCT decks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision-Care Dominance with Diagnostics Accelerating

Vision-care products controlled 60.12% of 2025 revenues as contact lenses served both corrective and cosmetic roles. The South Korea ophthalmic devices market continues to rely on repeat purchases of lens solutions, ortho-k modalities, and color tints. Diagnostic and monitoring systems post the quickest 9.08% CAGR. Their addressable value rises from USD 245.4 million in 2026 to an expected USD 379.3 million in 2031, anchoring future South Korea ophthalmic devices market size gains. Hospitals negotiate multi-year service contracts that bundle OCT hardware with AI subscription analytics, locking in predictable revenue for suppliers.

Surgical devices remain smaller but strategic. Femtosecond cataract platforms lifted operating efficiency and opened new premium IOL niches. Vendors now pitch disposable phaco tips and mobile surgical microscopes to ambulatory centres, a model suited to the South Korea ophthalmic devices market where outpatient cataract volumes are rising. Cross-licensing with Korean sensor makers shields multinationals from currency risk and qualifies them for preference points in public tenders.

By Disease Indication: Cataract Still Rules, Diabetic Retinopathy Rises

Cataract applications captured 34.05% of the South Korea ophthalmic devices market share in 2025, supported by nearly 420,000 annual surgeries. Multifocal IOLs, toric alignment tools, and intra-operative aberrometry reinforce premium-segment yields. Johnson & Johnson’s TECNIS Odyssey, cleared locally in 2024, improves low-light vision and commands premium price points. Diabetic-retinopathy devices are racing ahead at 8.28% CAGR. Only 29.5% of eligible diabetics undergo retinal screening, leaving ample headroom for AI fundus cameras and portable fluorescein angiography rigs.

Glaucoma devices benefit from national screening subsidies that emphasise early detection. Pediatric myopia management solutions, though a smaller revenue pool, present lifetime-value potential because patients transition from axial-length trackers to refractive surgery over decades. Companies explore sustained-release atropine implants that can be filed as combination products under MFDS rules, signalling convergence of therapeutics and diagnostics in the South Korea ophthalmic devices industry.

By End-User: Hospitals Lead, Ambulatory Centres Accelerate

Hospitals held 43.02% of 2025 sales thanks to 3,610 practising ophthalmologists concentrated in the Seoul Capital Area. Group purchasing contracts encompass femtosecond lasers, premium IOL consignments, and OCT networks that link provincial outpatient branches to metropolitan reading hubs. The hospital slice of the South Korea ophthalmic devices market size is projected to exceed USD 835 million by 2031.

Ambulatory surgery centres expand at 8.12% CAGR as insurers favour lower facility fees for cataract day-cases and LASIK. Their growth tempers hospital dominance and drives procurement of mobile phaco systems and compact SMILE lasers. Specialty ophthalmic clinics prosper in urban shopping districts by combining vision correction, cosmetic services, and tele-consultation platforms, which boosts high-margin diagnostic throughput. Optical retailers and e-commerce portals distribute daily-wear contact lenses, blue-light blockers, and smart-glasses add-ons, widening consumer touchpoints.

Competitive Landscape

The South Korea ophthalmic devices market features moderate concentration. Alcon, Carl Zeiss Meditec, and Johnson & Johnson Vision retain strongholds in premium IOLs, femtosecond systems, and diagnostic workstations. Domestic firms such as HanitaLenses Korea and ViewPharm leverage local-language service and MFDS expertise to capture mid-range lens, injector, and tonometer categories. Approximate total share for the five largest players sits near 60%, leaving room for agile challengers.

Strategic moves shape competition. Carl Zeiss Meditec’s April 2024 purchase of Dutch Ophthalmic Research Center broadened its MIGS and vitrectomy line-up for Korean tenders. RxSight collaborated with Seoul National University Hospital to validate adjustable-lens algorithms on Korean biometric profiles, cementing clinician confidence. NIDEK unveiled the RS-1 Glauvas OCT in June 2024, providing layered vascular imaging tailored for glaucoma clinics. Domestic AI start-ups license deep-learning modules to camera makers on revenue-share agreements, accelerating MFDS clearances under new software-as-a-medical-device provisions.

Price pressure is acute in contact-lens consumables. Global brands face competition from K-beauty conglomerates that bundle colour tints with cosmetics. Conversely, surgical hardware remains value-driven; buyers prioritise rotational stability and postoperative visual quality over unit price. Looking ahead, mixed-reality microscopes that overlay 3-D guidance onto live feeds promise to shift the basis of competition toward integrated software ecosystems by 2027.

South Korea Ophthalmic Devices Industry Leaders

Alcon Inc.

Johnson and Johnson

Topcon Corporation

Hoya Corporation

Carl Zeiss Meditec AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Alvotech and Teva’s biosimilar aflibercept (AVT06) received Biologics License Application acceptance, promising cheaper retinal-disease therapy.

- December 2024: Santen filed a New Drug Application for STN1013001 for open-angle glaucoma treatment.

- September 2024: Johnson & Johnson expanded local rollout of the TECNIS Odyssey multifocal IOL.

- June 2024: NIDEK launched the RS-1 Glauvas OCT unit for enhanced glaucoma-layer visualisation.

- April 2024: Carl Zeiss Meditec AG acquired Dutch Ophthalmic Research Center, strengthening its surgical-device slate in South Korea.

South Korea Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmology is a branch of medical sciences that deals with the structure, function, and various diseases related to the eye. Ophthalmic devices are medical equipment for diagnosis, surgical, and vision correction purposes. The market is segmented by device (surgical devices (glaucoma devices, intraocular lenses, lasers, and other surgical devices) and diagnostic and monitoring devices (autorefractors and keratometers, ophthalmic ultrasound imaging systems, ophthalmoscopes, optical coherence tomography scanners, and other diagnostic and monitoring devices). The report offers the value (USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

How large is the South Korea ophthalmic devices market in 2026?

The market stands at USD 1.34 billion in 2026 and will expand steadily through 2031.

Which segment is the fastest-growing within the South Korea ophthalmic devices market?

Diagnostic and monitoring devices register the quickest 9.08% CAGR, fuelled by nationwide glaucoma-screening reimbursements.

What is the role of hospitals versus ambulatory surgery centres?

Hospitals still hold 43.02% of 2025 revenues, yet ambulatory centres grow at 8.12% CAGR as insurers shift cataract and LASIK cases to day-care settings.

How significant is myopia for future demand?

Myopia prevalence reaches 96.5% among urban nineteen-year-olds, creating lifelong demand for refractive surgery, contact lenses, and monitoring devices.

What regulatory change affects AI-based ophthalmic devices?

The Digital Medical Products Act of 2024 imposes software-quality and cybersecurity validations, lengthening MFDS approval times for AI-driven hardware.

Which companies recently expanded their South Korea ophthalmic portfolios?

Carl Zeiss Meditec, Johnson & Johnson Vision, Santen, and NIDEK all launched or filed new products in 2024-2025, broadening competitive options for providers.

Page last updated on: