Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

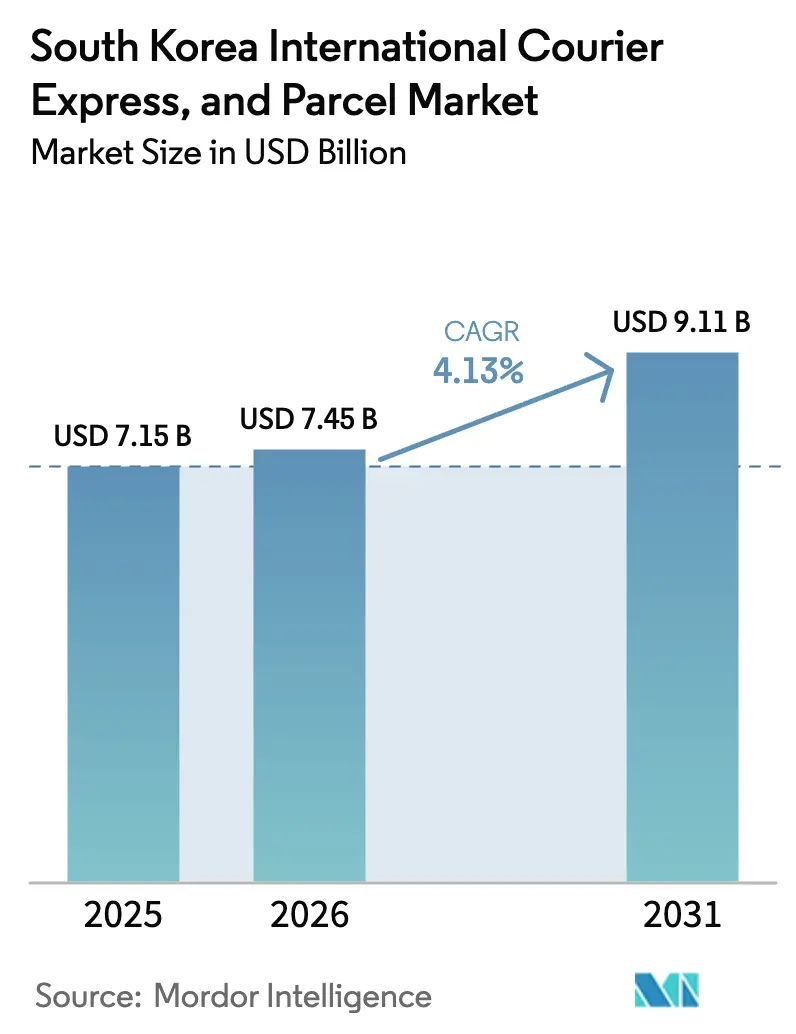

| Base Year Market Size (2025) | USD 7.15 Billion |

| Market Size (2026) | USD 7.45 Billion |

| Market Size (2031) | USD 9.11 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

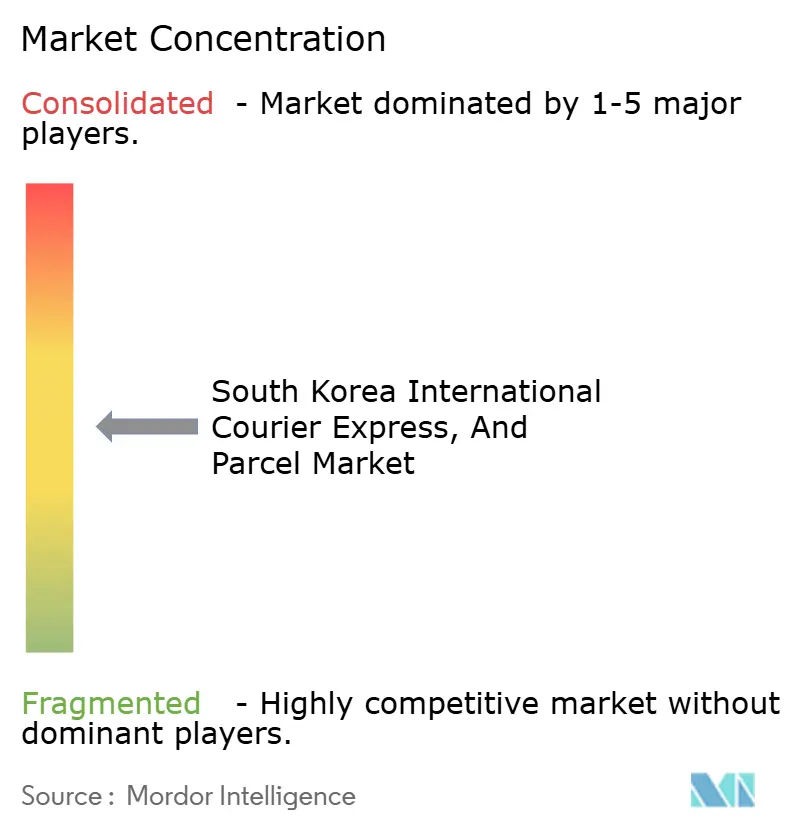

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea International Courier Express, And Parcel Market Analysis by Mordor Intelligence

The South Korea International Courier Express, And Parcel Market size was valued at USD 7.15 billion in 2025 and estimated to grow from USD 7.45 billion in 2026 to reach USD 9.11 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031).

Robust cross-border e-commerce activity, wide-ranging free-trade agreements, and a world-class digital infrastructure keep parcel volumes on an upward trajectory even though absolute values remain modest beside domestic logistics flows. Incheon Airport’s role as a Northeast Asian air-cargo gateway, coupled with dedicated belly-cargo capacity additions by major airlines, safeguards network resilience and frequency availability. Government programs that subsidize export-oriented SMEs and rapid growth in cold-chain parcels for pharmaceuticals further strengthen demand for premium, time-definite services. Competitive intensity continues to climb as domestic players, Korea Post EMS, and global couriers invest in automation, real-time visibility tools, and AI-driven routing. At the same time, high urban last-mile costs, cargo-terminal congestion, and rising green-air surcharges compel operators to refine cost structures without sacrificing service reliability.

Key Report Takeaways

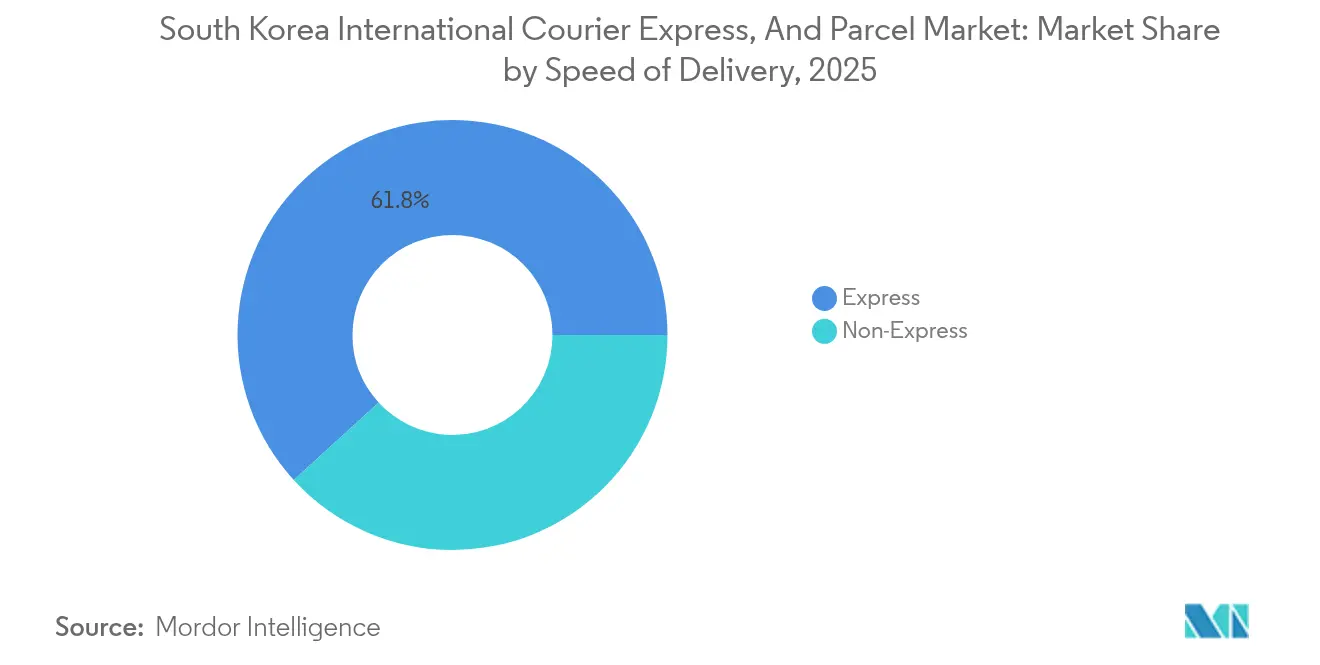

- By speed of delivery, express services held 61.78% of the South Korea International Courier Express and Parcel Market share in 2025 and are advancing at a 4.56% CAGR through 2031.

- By shipment weight, light parcels accounted for 62.10% of the South Korea International Courier Express and Parcel Market size in 2025, while heavy-weight parcels are forecast to post a 4.44% CAGR to 2031.

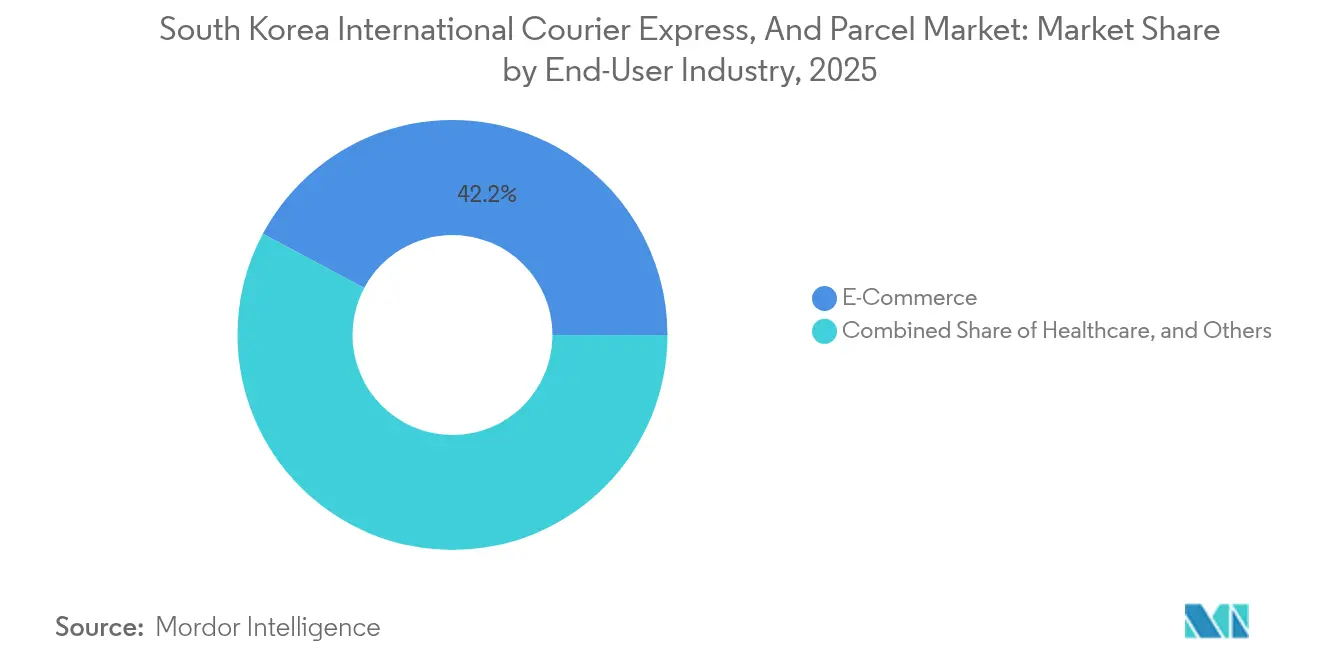

- By end-user industry, e-commerce contributed 42.20% revenue share in 2025; healthcare is projected to grow at 4.29% CAGR over 2026-2031.

- By model, B2B transactions captured 50.40% of the 2025 market, whereas B2C flows are set to rise at 4.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea International Courier Express, And Parcel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border e-commerce export boom | +1.2% | Global with APAC and North America concentration | Medium term (2-4 years) |

| SME demand for time-definite delivery | +0.8% | National, spillover to regional partners | Short term (≤ 2 years) |

| FTAs and digital customs facilitation | +0.6% | Global, notably U.K., China, APEC | Long term (≥ 4 years) |

| Dedicated belly-cargo capacity expansion | +0.5% | APAC routes toward Americas & Europe | Medium term (2-4 years) |

| Cold-chain cross-border parcel growth | +0.4% | Developed markets worldwide | Long term (≥ 4 years) |

| Digital tourist-tax refund returns | +0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cross-border e-commerce export boom

Online marketplaces allow Korean SMEs to reach global buyers, and the Ministry of SMEs and Startups has slashed freight charges by more than 60% for program participants. Exports still represent roughly 40% of national GDP, so seamless courier links are critical to macro performance. Beauty, fashion, and lifestyle brands prefer express parcels that offer integrated customs documentation and real-time tracking. Potential elimination of the U.S. de-minimis threshold could push shippers toward premium services that streamline new compliance requirements. Mobile commerce penetration and frictionless digital payments amplify traffic and encourage operators to embed checkout-to-doorstep fulfillment modules[1]“Korea in a Changing Global Trade Landscape,” International Monetary Fund, imf.org.

SME demand for time-definite delivery

Korean manufacturers in semiconductors, biotech, and precision machinery increasingly promise next-day shipping to overseas customers, forcing couriers to maintain tight delivery windows. UPS, DHL, and FedEx have all boosted overnight flight frequencies into Seoul to safeguard cut-offs. Real-time visibility tools, milestone alerts, and proactive exception handling now influence carrier selection as much as price. Government subsidies targeting SME export logistics ease adoption of higher-priced express tiers, supporting margin stability for operators[2]“Asia-Pacific Trade Facilitation Report 2024,” Asian Development Bank, adb.org.

FTAs and digital customs facilitation

A dense network of FTAs most recently with the U.K. under a continuity deal—eliminates or reduces duties on thousands of tariff lines, while Korea Customs Service’s single-window and pre-arrival systems accelerate clearance. The Asian Development Bank lists Korea with a 100% implementation score for sustainable trade facilitation measures. Electronic certificates of origin and paperless trade protocols cut dwell times and minimize documentation errors, directly benefiting express couriers that rely on predictable hand-overs.

Dedicated belly-cargo capacity expansion

Korean Air plans to introduce 54 new aircraft in 2025, combining freighters and passenger jets configured for cargo-friendly holds. ANA Group will operate at 108% of its 2024 international capacity, emphasizing cargo profitability on Asia-North America lanes. Flexible wide-body scheduling creates additional allotments for courier parcels, easing peak-season bottlenecks and enabling shorter transit times on multi-stop itineraries.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High urban last-mile costs | –0.7% | Seoul metropolitan area | Short term (≤ 2 years) |

| Incheon Airport cargo-terminal congestion | –0.5% | National gateway | Medium term (2-4 years) |

| Green-air-cargo surcharge pressure | –0.4% | Europe & North America lanes | Long term (≥ 4 years) |

| Low-cost Chinese postal packet rivalry | –0.3% | APAC with global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High urban last-mile costs

Dense building clusters, short delivery windows, and rising labor expectations push per-stop expenses upward in Seoul. Delivery workers temporarily halted service in June 2025 to participate in snap-election voting, underscoring labor’s leverage. Local e-commerce players such as Coupang invest heavily in owned networks to contain costs, a level of vertical integration that international couriers struggle to replicate at lower volumes. Regulatory mandates on vehicle emissions and parking restrictions further squeeze margins[3]“S. Korea Sets New Air Fleet Record, Plans Further Expansion,” The Korea Herald, koreaherald.com.

Incheon Airport cargo-terminal congestion

The airport ranked among the world’s top three for international passenger throughput in 2024, stretching cargo infrastructure during peak travel seasons. Slot scarcity leads to sub-optimal departure times and standby freight, eroding the reliability premium attached to express services. Planned terminal upgrades require significant capital and multiyear timelines, so congestion is expected to persist through at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Speed of Delivery: Express Services Drive Premium Growth

Express shipments captured a dominant 61.78% share of the South Korea international courier market in 2025, reflecting exporters’ willingness to pay for same- or next-day reliability. Non-express tiers cater to cost-sensitive bulk traffic but advance more slowly as customer expectations rise. FedEx’s nonstop Seoul-Taipei flights and DHL’s capacity upgrades on intra-Asia lanes shorten transit times and enlarge route density. Premium service providers continue to blend freighter lift with passenger belly space to preserve schedule flexibility.

Express operators leverage advanced tracking APIs, automated sortation, and AI-driven capacity forecasts to sustain customer satisfaction despite rising volumes. Integrated customs-brokerage modules handle electronic documents in seconds, offsetting Korea’s high labor costs by reducing manual touchpoints. As Korea’s semiconductor and bio-manufacturing firms widen overseas direct-to-customer channels, express parcels become integral to brand promises around speed and reliability. Over the outlook period, express shipments are on track to post a 4.56% CAGR, maintaining their central role within the South Korea international courier market.

By Shipment Weight: Light Parcels Dominate Volume

Light parcels represented 62.10% of the South Korea international courier market size in 2025, propelled by cross-border e-commerce orders for cosmetics, apparel, and consumer electronics. Their smaller physical footprint fits efficiently into passenger-aircraft belly holds, enabling higher flight frequency and rapid downstream processing. Conversely, heavy parcels—although only a minor share today—are projected to grow at 4.44% CAGR due to demand for industrial machinery, capital equipment, and oversized high-tech components. Couriers serving heavier segments adopt reinforced packaging, specialized handling crews, and dedicated freighter capacity.

Light-parcel dominance allows operators to standardize processes, install high-speed sorters, and negotiate favorable airline block-space agreements. Yet the growth in heavy parcels nudges carriers toward hybrid service models that blend courier-style tracking with freight-forwarder handling capabilities. Investments such as Taewoong Logistics’ T&C BUSAN hazardous-cargo terminal illustrate the infrastructure upgrades required to chase opportunities at the heavy end of the market.

By End-User Industry: E-commerce Leadership with Healthcare Acceleration

E-commerce sales accounted for 42.20% share in 2025, cementing their role as the single largest demand driver in the South Korea international courier market. The segment benefits from high smartphone penetration, quick adoption of global marketplaces, and government-backed SME export subsidies. Automated fulfillment hubs, such as CJ Logistics’ LoIS Parcel network, shorten outbound lead times and support same-day hand-over to air carriers.

Healthcare shipments, though smaller in value today, exhibit the fastest forward momentum at 4.29% CAGR thanks to Korea’s thriving biopharmaceutical pipeline. Temperature-controlled packaging, GDP-compliant chain-of-custody protocols, and on-board courier services create fresh revenue layers for operators able to certify compliance. Manufacturing, BFSI, and wholesale-retail continue to underpin base-load volume, safeguarding scale economies across the core network.

By Model: B2B Foundation with B2C Growth Momentum

B2B exchanges delivered 50.40% of 2025 transaction value, underscoring the export-oriented nature of Korea’s economy. Mature production networks in semiconductors, automotive parts, and precision instruments necessitate predictable delivery windows and deep customs-brokerage know-how. Nevertheless, B2C flows are climbing at 4.22% CAGR amid direct-to-consumer brand strategies and viral K-lifestyle product demand overseas. Integrated checkout-to-delivery APIs, transparent landed-cost calculators, and social-commerce extensions are reshaping service menus.

Customer-to-customer traffic remains a smaller steady niche covering personal gifts, student shipments, and relocation parcels. Digital self-service portals and drop-box networks keep this segment operationally viable despite its lower revenue per kilogram. Overall, balanced demand across models makes the South Korea international courier market resilient to sector-specific slowdowns.

Geography Analysis

South Korea’s compact national footprint concentrates shipment origins around the Seoul-Incheon corridor, enabling couriers to optimize pickup density and hub-sort cycles. The country’s 65.4% 5G penetration rate supports real-time parcel visibility and driver navigation, elevating customer service benchmarks. Incheon Airport remains the pivotal international node, with over 42 dedicated cargo aircraft in the national fleet as of 2025 and more on order to expand lift capacity.

Regional proximity to China, Japan, and Southeast Asian consumption hubs lets carriers capitalize on short haul, high-yield corridors, while deep-sea ports at Busan and Gwangyang offer intermodal alternatives for heavier consignments. Korea’s participation in APEC agendas and multiple bilateral FTAs speeds customs clearances and slashes tariff barriers, giving the South Korea international courier market a competitive edge on intra-Asia lanes. Still, single-gateway dependency on Incheon introduces congestion risks during peak export seasons, urging policymakers to fast-track terminal expansions and promote secondary air-cargo sites.

National digital trade initiatives including electronic certificates of origin and AI-assisted risk profiling minimize paperwork and reduce dwell times, allowing couriers to meet tight SLA promises to U.S. and European customers. Continued investment in AI, 6G pilots, and cybersecurity under the Digital Innovation & Diffusion Strategy ensures that the South Korea international courier market maintains its reputation for high service reliability and data transparency.

Competitive Landscape

Competition spans domestic integrators, the public postal operator, and global express giants. CJ Logistics and Korea Post EMS leverage dense national depots and localized know-how to manage challenging urban deliveries, whereas DHL, FedEx, and UPS bank on global networks for end-to-end visibility and cross-border capacity guarantees. Medium-size entrants such as SLX and ILYANG Logis carve out niches in specialized B2B lanes and hazardous cargo.

Technology forms the battleground. CJ Logistics’ LoIS Parcel platform automates warehousing and sortie planning, while DHL and UPS roll out AI-supported demand forecasting to match lift supply with volatile e-commerce peaks. Foreign direct investment is heating up: Ta-Hwa’s USD 15.48 million purchase of SKYWASTER EXPRESS secures a Korea-Japan dual-hub model to improve supply-chain resilience. Meanwhile, start-ups like Kokkan Logis deploy algorithmic brokerage engines that claim up to 20% route-cost savings, nudging incumbents toward pricing transparency.

Sustainability also shapes rivalry. Early movers lock in sustainable aviation fuel commitments to mitigate carbon surcharges, differentiating their B2B propositions on ESG compliance. Others retrofit city-center micro-hubs and deploy electric cargo vans to contain last-mile emissions and bypass traffic restrictions. Collective share held by the top five participants hovers near 45%, indicating moderate concentration yet ample space for specialized challengers.

South Korea International Courier Express, And Parcel Industry Leaders

CJ Logistics

Korea Post (EMS)

Hanjin Transportation

Lotte Global Logistics

DHL Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ta-Hwa International Holding completed the USD 15.48 million takeover of Korean freight forwarder SKYWASTER EXPRESS to build a dual hub spanning Japan and South Korea.

- September 2025: Taewoong Logistics inaugurated T&C BUSAN at Busan New Port for hazardous cargo and chemicals, targeting Northern Sea Route transshipment demand.

- September 2025: The Ministry of SMEs and Startups convened exporters and global platforms to discuss logistics barriers, highlighting the threat of a potential U.S. de-minimis removal.

- February 2025: South Korea’s aircraft fleet climbed to 416, with plans for 54 additional deliveries during 2025 to expand courier capacity

South Korea International Courier Express, And Parcel Market Report Scope

CEP (courier, express, and parcel) refers to a set of services that entails the delivery of various commodities and products across many places via land, air, or water. In contrast to courier and parcel services, express deliveries are frequently time-bound, with various high-value consignments arriving in a few days or at a pre-arranged date and time.

The report offers a comprehensive background analysis of the South Korean international CEP market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered in the study.

The South Korea International Courier, Express, and Parcel (CEP) Market is Segmented by Business Model (Business-to-Business (B2B), Business-to-Customer (B2C), and Customer-to-Customer (C2C)), By Type (E-commerce, Non-e-commerce), and By End User (Services, Wholesale and Retail Trade, Healthcare, Industrial Manufacturing, and Other End Users). The report offers market size and forecasts in value (USD billion) for all the above segments.

By Model

| Business-to-Business (B2B) |

| Business-to-Customer (B2C) |

| Customer-to-Customer (C2C) |

By Speed of Delivery

| Express | Route | Inter-Region |

| Intra-Region | ||

| Non-Express |

By Shipment Weight

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

By End User Industry

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| By Model | Business-to-Business (B2B) | ||

| Business-to-Customer (B2C) | |||

| Customer-to-Customer (C2C) | |||

| By Speed of Delivery | Express | Route | Inter-Region |

| Intra-Region | |||

| Non-Express | |||

| By Shipment Weight | Heavy Weight Shipments | ||

| Light Weight Shipments | |||

| Medium Weight Shipments | |||

| By End User Industry | E-Commerce | ||

| Financial Services (BFSI) | |||

| Healthcare | |||

| Manufacturing | |||

| Primary Industry | |||

| Wholesale and Retail Trade (Offline) | |||

| Others | |||

Key Questions Answered in the Report

How big is the South Korea International Courier Express, and Parcel Market in 2026?

It is valued at USD 7.45 billion for 2026, with a projected rise to USD 9.11 billion by 2031.

Which segment grows fastest by speed of delivery?

Express services grow at a 4.56% CAGR thanks to strong SME demand for time-definite exports.

What drives the surge in healthcare parcels?

Expansion of Korea’s bio-pharma exports and the need for GDP-compliant cold-chain logistics boost healthcare parcels at 4.29% CAGR.

Why are last-mile costs a restraint?

Dense urban geography, labor pressures, and emission rules raise per-stop delivery expenses, reducing margins in Seoul-Incheon corridors.

Which players dominate the competitive landscape?

CJ Logistics, Korea Post EMS, DHL, FedEx, and UPS together hold roughly 45% of market revenue, reflecting moderate concentration.

What impact will potential U.S. de-minimis changes have?

Removal could raise compliance costs for low-value exports, steering SMEs toward premium couriers with advanced customs-brokerage services.

Page last updated on: