Medical Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

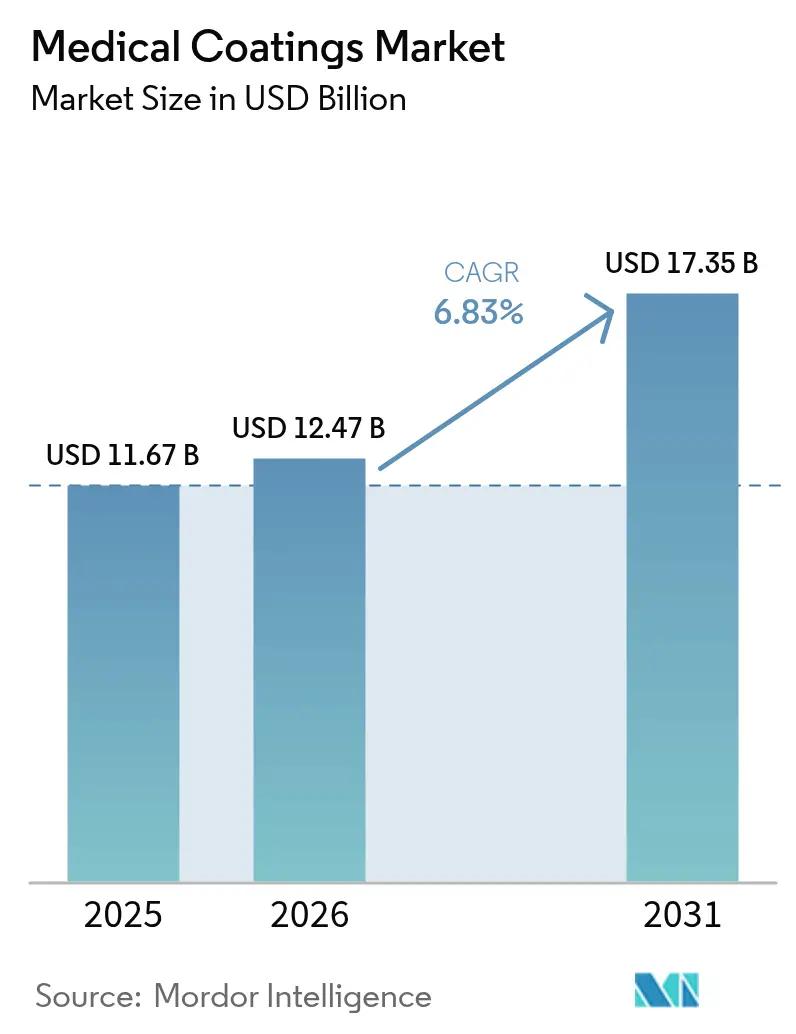

| Market Size (2026) | USD 12.47 Billion |

| Market Size (2031) | USD 17.35 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

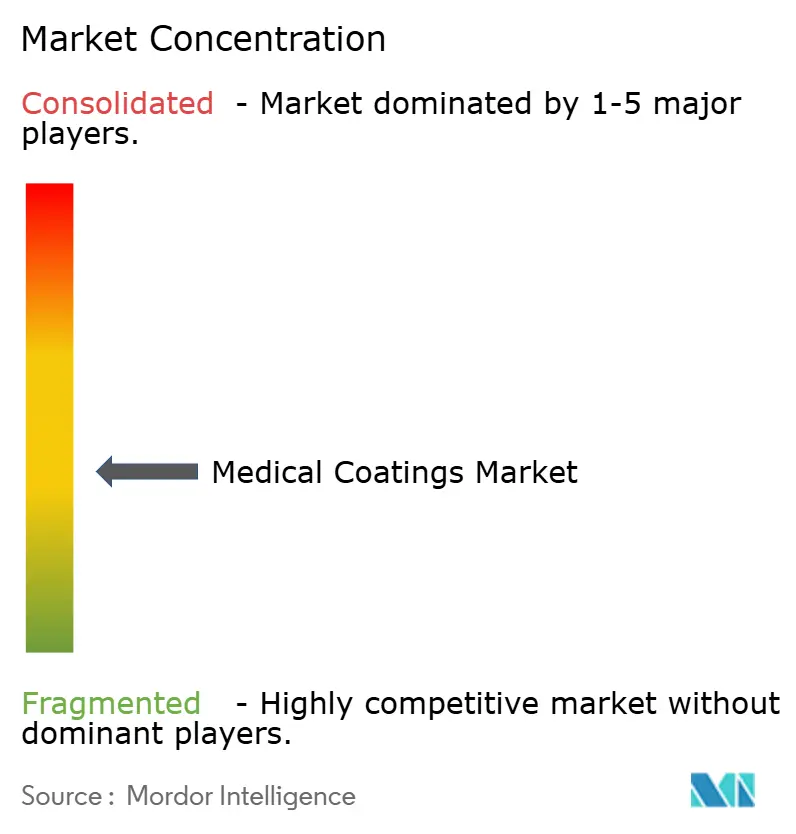

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Coatings Market Analysis by Mordor Intelligence

The Medical Coatings Market size was valued at USD 11.67 billion in 2025 and estimated to grow from USD 12.47 billion in 2026 to reach USD 17.35 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031). The market’s momentum comes from the convergence of aging populations, infection-control mandates and a surge in minimally invasive procedures that require highly engineered surface technologies. Parylene’s conformal barrier properties, fluoropolymer friction-lowering capabilities and antimicrobial chemistry are now core building blocks in new-generation implants and single-use devices. Consolidation pressures, raw-material price swings and regulatory oversight from bodies such as the FDA and FTC shape competitive behavior, yet sustained venture funding in smart implants signals lasting growth prospects. Regionally, North America anchors demand with 34.44% revenue share in 2024, while Asia Pacific advances at an 8.99% CAGR on the back of healthcare infrastructure expansion and rising surgical volumes.

Key Report Takeaways

- By chemistry, parylene led with 29.10% revenue share in 2025; fluoropolymer coatings are advancing at a 7.32% CAGR to 2031.

- By coating function, antimicrobial solutions held 30.10% of the medical coatings market share in 2025; hydrophilic/lubricious coatings are projected to expand at a 7.74% CAGR through 2031.

- By deposition technology, plasma spray accounted for 26.40% of the medical coatings market size in 2025; chemical vapor deposition is growing at 7.31% CAGR to 2031.

- By application, implants commanded 30.85% of the medical coatings market size in 2025; medical devices record the fastest growth at 7.08% CAGR to 2031.

- By geography, North America captured 34.10% of 2025 revenue; Asia Pacific is set to pace the field with an 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Awareness Regarding Advancement of Medical Treatments | +1.50% | Global, with concentrated impact in North America & Europe | Medium term (2-4 years) |

| Sharp rise in single-use, minimally-invasive devices post-pandemic | +1.20% | Global, with accelerated adoption in APAC | Short term (≤ 2 years) |

| Stricter HAIs regulations driving antimicrobial adoption | +0.80% | North America & EU primarily, expanding to APAC | Medium term (2-4 years) |

| Surge in ambulatory surgical centers requiring low-friction coatings | +0.60% | North America core, with spillover to developed markets | Medium term (2-4 years) |

| Venture funding into smart implant start-ups | +0.50% | North America & EU, with emerging activity in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Advanced Medical Treatments

Healthcare practitioners now view surface engineering as a pathway to transform passive devices into active therapeutic systems that deliver drugs, sense biological signals and resist infection. Multifunctional coatings that simultaneously provide antimicrobial protection and bone-integration support in orthopedics exemplify this shift. Academic evidence demonstrating lower revision rates in coated implants is convincing hospitals to pay premium prices, while device makers integrate sensing layers that enable remote patient monitoring.

Surge in Single-Use, Minimally Invasive Devices

Pandemic-era infection-control lessons accelerated the pivot to disposable catheters and surgical tools. Coating suppliers responded with cost-optimized hydrophilic finishes designed for one-time use, eliminating the sterilization burden of re-usable instruments. Ambulatory centers benefit through faster turnover and reduced cross-contamination risk, supporting volume growth in coated disposables.

Stricter HAI Regulations Boosting Antimicrobial Uptake

The CDC’s updated surgical site and MDRO guidelines underscore coated surfaces as key interventions, transforming antimicrobial layers from optional to expected on many devices[1]Centers for Disease Control and Prevention, “MDRO Prevention Strategies,” cdc.gov . Evidence that silver-, copper- or antibiotic-infused films curb biofilm formation propels hospital procurement policies toward coated products, ensuring a durable demand base.

Venture Funding in Smart Implants

Capital continues to flow into sensor-enabled orthopedic and cardiovascular implants that rely on conformal barrier coatings to protect electronics while maintaining biocompatibility. Coating innovators with expertise in parylene CVD or atomic layer deposition secure development contracts as start-ups race to clinical validation, planting seeds for long-run market expansion[2]U.S. Food and Drug Administration, “Recognized Consensus Standards: Medical Devices,” accessdata.fda.gov .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (silicones, parylene dimers) | -0.90% | Global, with acute impact in supply-constrained regions | Short term (≤ 2 years) |

| Complex, fragmented regulatory pathways for nanocoatings | -0.70% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Supply-chain risks for specialty fluoropolymers | -0.60% | Global, with concentrated impact in import-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Shortages of PTFE and spikes in silicone precursor costs in 2024 forced many coaters to renegotiate supply contracts, delay shipments and raise prices. Smaller providers lacking hedging capacity lost share to vertically integrated rivals. Although larger players absorbed shocks through inventory buffers, persistent energy-price swings keep input costs unpredictable.

Fragmented Regulatory Pathways for Nanocoatings

The FDA’s chemical characterization draft guidance coupled with Europe’s PFAS proposals lengthen approval timelines and add testing complexity. Divergent regional rules oblige manufacturers to pursue parallel dossiers, boosting compliance costs and discouraging start-up participation in the most advanced coating categories[3]Food and Drug Administration, “Chemical Analysis for Biocompatibility Assessment of Medical Devices; Draft Guidance,” federalregister.gov .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemistry: Parylene Dominance Faces Fluoropolymer Challenge

Parylene coatings represented 29.10% of the medical coatings market in 2025. Their pin-hole-free conformal layers protect neural probes, pacemakers and microfluidic chips, underpinning long-term trust in critical implants. Demand remains stable in cardiology and neuromodulation, yet raw material scarcity and deposition cycle length put cost pressure on suppliers. Fluoropolymer solutions are experiencing a robust growth rate of 7.32% CAGR, driven by the demand for ultra-low friction in catheter procedures. Regulatory focus on PFAS limits heightens uncertainty, but healthcare exemptions expected for life-saving devices preserve outlook. Silicone-based chemistries retain relevance in flexible tubing and wound-care films due to elastomeric properties, while metal-ion and bioceramic coatings inhabit high-value niches for osseointegration.

The medical coatings market is witnessing formulation cross-pollination whereby parylene films gain hydrophilic top-coats and fluoropolymer layers adopt antimicrobial additives. Suppliers offering such hybrid stacks secure multi-year contracts with OEMs looking to shrink vendor lists. Advancements in atomic layer deposition allow angstrom-level control of titanium oxide nucleation on parylene, boosting barrier performance.

By Coating Function Type: Antimicrobial Leadership Amid Hydrophilic Growth

Antimicrobial layers accounted for 30.10% of the revenue share in 2025, driven by hospital mandates to curb biofilm formation. Silver-ion and antibiotic coatings demonstrate sustained pathogen-kill rates in joint replacements and central-line catheters, enhancing device safety. Hydrophilic/lubricious finishes are experiencing the fastest growth at a 7.74% CAGR, powered by neurovascular and peripheral interventions that require smooth navigation through tortuous anatomy.

Multi-effect formulations that merge antimicrobial and lubricious traits stand out, particularly for urinary catheters where infection and comfort both matter. Anti-thrombogenic chemistries play a significant role in applications such as cardiovascular grafts and ventricular assist devices. Drug-eluting options in the “Others” basket gain traction as controlled-release stents receive new approvals, yet cost remains a barrier to widespread uptake outside critical cardiovascular segments. OEMs now specify performance dashboards—coefficient of friction, log-reduction values, cytotoxicity scores—and expect coaters to meet targets across parameters, raising technical entry hurdles.

By Deposition Technology: Plasma Spray Leads While CVD Accelerates

Plasma spray lines captured 26.40% of the total medical coatings market in 2025. These lines are particularly favored for orthopedic screws and dental implants, which benefit from thick, porous hydroxyapatite layers that enhance bone in-growth. Chemical vapor deposition is experiencing a 7.31% CAGR, driven by its unparalleled ability to coat intricate micro-architectures, a capability thermal techniques cannot achieve.

Dip-coat and spray-coat processes remain the workhorses for high-volume disposables, supplying over USD 2 billion of catheter and syringe demand. Meanwhile, nascent atomic layer deposition is piloting at select cardiovascular OEMs where barrier layers under 100 nm extend battery life in leadless pacemakers. Process choice increasingly hinges on throughput, capital cost and end-use performance, driving coater investments in multi-technology campuses that enable chemistry-agnostic manufacturing.

By Application: Implants Dominate While Medical Devices Surge

Implant coatings accounted for 30.85% of 2025 sales, covering orthopedic, cardiovascular, and dental segments. Hydroxyapatite plasma spray and antimicrobial dip coats reduce loosening, infection and revision procedures, safeguarding reimbursement economics. Coatings for drug-eluting bioresorbable stents secured new FDA approvals in 2024, cementing implants as a resilient revenue engine.

Medical devices, defined here as non-implantable instruments and disposables, accounted the highest 7.08% CAGR. Catheters, guidewires and endoscopes depend on hydrophilic performance to minimize insertion force and adverse events. Surgical tools employ hard, low-friction titanium-nitride or MICRALOX anodic layers for durability. Widening procedure complexity at ASCs multiplies unit volumes, lifting demand for pre-coated kits shipped sterile and ready to use.

Geography Analysis

North America retained the top spot with 34.10% of 2025 revenue, underpinned by robust reimbursement, rigorous FDA pathways and a concentration of multinational OEM headquarters. Hospital purchasing committees emphasize coatings that support infection-reduction metrics mandated by CMS, anchoring steady antimicrobial volumes. Canada’s device export incentives and Mexico’s contract-manufacturing clusters also stimulate regional growth.

Asia Pacific is the fastest mover at an 8.78% CAGR, driven by China’s Made in China 2025 targets and rising procedure rates among aging populations. Domestic Chinese manufacturers integrate parylene and hydrophilic chemistries to close performance gaps with imported devices, while Japanese and South Korean firms pioneer sensor-integrated implants. India and ASEAN markets progress from basic silicone coatings toward advanced fluoropolymer friction-reduction as catheter labs proliferate.

Europe contributes a sizeable revenue pool but faces PFAS uncertainty that clouds fluoropolymer futures. Nonetheless, Germany’s orthopedic clusters and Ireland’s export-oriented device plants sustain investment in plasma and CVD lines. South America and the Middle East & Africa remain nascent yet promising; Brazil’s tax incentives for implant factories and Saudi Arabia’s Vision 2030 healthcare build-out elevate demand for coated orthopedic and cardiovascular products.

Regulatory Landscape

Medical device coatings are regulated as part of the finished device under US FDA pathways (510(k)/PMA) and the EU Medical Device Regulation (MDR 2017/745), which makes coating chemistry, process validation, and lifecycle documentation part of the device technical file rather than treated as standalone chemical products. In the United States, the FDA Quality Management System Regulation (QMSR), effective February 2, 2026, aligns quality-system expectations with ISO 13485:2016 and raises scrutiny on supplier controls and validation for coating special processes.

Standards activity in 2026 added new compliance anchors for coatings used on implants and devices. ISO/TR 4234:2026 introduced a structured framework for assessing coating systems on non-active surgical implants across design, manufacturing, sterilization, and aging, while ISO 10993-1:2026 moves biological evaluation toward a risk-based model integrated with ISO 14971 and places greater emphasis on chemical characterization inputs (notably ISO 10993-18) for coating materials. In Europe, Commission Regulation (EU) 2026/1168 amended REACH Annex XVII (Entry 78) on synthetic polymer microparticles, including derogations for particles permanently incorporated into a solid matrix for uses lasting one year or longer, shaping formulation choices and documentation strategies for certain polymer-based coating systems.

Value Chain Analysis

The value chain starts with specialty raw materials and intermediates (medical-grade silicones and polymers such as PEG/PVP, fluoropolymer feedstocks, parylene dimers, metal/ceramic precursors, and antimicrobial actives), then moves into formulation and compounding. Coating application typically follows via CVD, plasma spray, or high-volume dip/spray operations. Coating is commonly performed either in-house at device OEM sites or by specialized coating service providers using validated equipment, cleanroom environments, and controlled sterilization and packaging interfaces before finished devices proceed through OEM distribution channels to hospitals, ambulatory surgical centers, and other care settings.

Bottlenecks tend to form where compliance and validation requirements constrain capacity, particularly for GMP-aligned, qualified raw-material supply and validated coating operations treated as special processes under ISO 13485 (where critical properties cannot be fully verified without destructive testing). With the FDA QMSR effective February 2, 2026, supplier purchasing controls and process validation (IQ/OQ/PQ) become more central to OEM qualification, which increases the cost and lead time for onboarding new coating suppliers. Raw material qualification timelines, often 12 to 24 months for medical-grade inputs, and dependence on certified suppliers also amplify supply risk, while recognized consensus standards such as ISO 13179-1:2021 for plasma-sprayed coatings on metallic surgical implants influence process selection and documentation practices for premarket submissions.

Competitive Landscape

The medical coatings market is moderately fragmented. Larger players pursue technology-platform breadth, pairing parylene CVD with fluoropolymer dip lines and offering regulatory consulting services that streamline OEM submissions. The FTC’s 2025 blocking of a hydrophilic-coating acquisition signaled regulators’ vigilance toward excessive concentration.

M&A momentum persists as Integer Holdings absorbed Precision Coating to secure proprietary GlideLine and MICRALOX platforms. Start-ups champion atomic layer deposition and smart-implant coating services, often partnering with contract manufacturers for scale. Material science breakthroughs, chiefly in antimicrobial peptides and non-PFAS fluorinated alternatives, represent competitive battlegrounds. Established firms hedge PFAS risk through R&D in silicon-based low-friction systems, signaling a pivot toward regulatory-resilient chemistries.

Medical Coatings Industry Leaders

AST Products, Inc.

Covalon Technologies Ltd.

DSM

Hydromer, Inc.

Surmodics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is emerging around compliance-led modernization of coating operations and supplier networks as quality and documentation requirements tighten across major markets. The FDA QMSR effective February 2, 2026 (aligned with ISO 13485:2016) increases demand for validated, auditable coating processes and stronger supplier controls, favoring providers that can combine coating chemistry with in-house process equipment, validation packages, and regulatory documentation support. This emphasis shows up in industry moves toward end-to-end models, including Hydromer’s February 2026 expansion into automated high-speed coating and UV-curing equipment supply integrated with proprietary coating chemistry.

Capacity and geographic footprint investments also point to whitespace in advanced coatings for drug-device combination products and in precision functional coatings near device manufacturing hubs. Freudenberg Medical announced an investment of over USD 50 million to expand Hemoteq AG in Aachen, Germany, including ISO Class 7 cleanrooms to support drug-device combination products, highlighting demand for controlled environments and validated coating scale-up. Surface Solutions Group announced a USD 10 million Costa Rica facility (construction slated to begin in 2026) and previously added automated electrostatic robotic capacity (30 operational coating lines as of May 2025), which underscores the growing emphasis on automation for consistency, throughput, and reproducibility in lubricious, hydrophilic, and other functional coatings. Standards published in 2026, including ISO/TR 4234:2026 for implant coating system assessment, further support more structured OEM-supplier communication and can speed qualification workflows where technical documentation readiness is a gating factor.

Recent Industry Developments

- February 2026: TheraDep Technologies Inc. and dsm-firmenich Biomedical announced a partnership to develop and commercialize advanced bio-surface and nano-coating technologies for medical devices. The collaboration included an initial product launch, positioning dsm-firmenich to extend its biomedical coatings portfolio with partner-enabled surface technology and commercialization pathways.

- January 2025: Integer Holdings Corporation acquired Precision Coating from Katahdin Industries, adding surface functionality platforms such as GlideLine fluoropolymer coatings and MICRALOX anodic coatings. The deal strengthened Integer's ability to offer broader coating capabilities alongside contract manufacturing, supporting OEM efforts to consolidate suppliers across coated device programs.

- June 2024: Freudenberg Medical committed over USD 50 million to develop a new production facility in Aachen, Germany, under its Hemoteq AG brand, targeting drug and hydrophilic coatings for medical devices and components. The investment expanded cleanroom-centric coating capacity and reinforced Europe as a hub for advanced coating operations tied to regulated device manufacturing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the medical coatings market covers coating materials applied on medical devices, implants, and medical tools to improve surface performance, including biocompatibility, lubricity, and infection control, and the market value is tracked in USD across major regions.

Scope exclusions: We exclude coatings used mainly for non-medical industrial end uses and general-purpose paints that are not qualified for medical device or implant applications.

Segmentation Overview

- By Chemistry

- Silicone

- Fluoropolymer

- Parylene

- Others (Metal-based (Ti, Ag, Au), Bio ceramics)

- By Coating Function Type

- Antimicrobial

- Hydrophilic/Lubricious

- Anti-thrombogenic/Hemocompatible

- Others (Drug-eluting, Radiopaque)

- By Deposition Technology

- Chemical Vapor Deposition (CVD)

- Plasma Spray

- Dip and Spray

- Others

- By Application

- Medical Device

- Implants (Orthopedic, Cardiovascular, Dental)

- Surgical Instruments and Tools

- Others

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

To build the first view of the market, we rely on public, citable information that shows how medical device production, procedure volumes, and coating adoption are moving. Sources used include official health and regulatory publications such as the US FDA device databases and safety communications, and statistical bodies such as the US Census Bureau for manufacturing indicators and trade direction.

We also refer to sources such as the US International Trade Commission for medical device related import and export context, the World Health Organization for population aging and care delivery trends, and peer reviewed journals that discuss coating performance and clinical use patterns. Company annual reports, investor presentations, press releases, and association websites are used to cross-check product positioning and end-use exposure. Where needed, we supplement this with paid subscriptions focused on company financials and intelligence, patent databases, and shipment-level import and export records to test assumptions around supply footprint and product mix. These examples are not exhaustive, and many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Interviews and structured surveys were completed with a mix of coating material suppliers, contract coaters, medical device and implant stakeholders, and downstream channel participants who understand demand by application. We used these inputs to validate which coating types are being specified, how pricing is moving for common chemistries, and where adoption is accelerating by region and device category, before assumptions were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 18% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 22% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

The core sizing was built using a top-down approach where medical device and implant demand signals are reconstructed by application, and then mapped to coating penetration and typical coating value intensity for each use case. To keep the totals realistic, the output is then cross-checked with selective bottom-up approximations, such as sampled supplier revenue exposure, channel checks, and a simple volume times average selling price build for a few high-use device families.

Key inputs used in the model include procedure and utilization trends for minimally invasive interventions, implant and catheter shipment direction, the mix shift toward antimicrobial, hydrophilic, and drug-eluting coatings, average selling price progression for common chemistries (such as silicone, fluoropolymer, and parylene), and region-level manufacturing and trade indicators. When a sub-area has thin data, we fill gaps by using proxy variables (for example, device shipment growth as a stand-in for coatingable surface volume), and the assumption is re-tested with expert feedback.

For forecasting, scenario analysis is used around adoption and pricing, supported by consensus ranges gathered from industry respondents, and then refined with historical trend smoothing so year-to-year movement stays explainable. The final forecast is kept consistent with regulatory and infection-control momentum that affects specification decisions, and with the regional pace of device production and healthcare access.

Data Validation & Update Cycle

After the first model run, outputs are validated through multiple checks that compare results against independent signals, including device manufacturing direction, trade movement, and reported category growth in public disclosures. If a region or application shows a sharp jump that is not supported by these signals, we revisit penetration, pricing, or mix assumptions and re-contact selected respondents when needed.

Before sign-off, the work is reviewed in steps so calculation logic, units, and year alignment are consistent across the workbook and narrative. Reports are refreshed annually, and interim updates are made when material events change demand or pricing expectations. Right before delivery, a final pass is completed so clients receive the latest updated view rather than an older model snapshot.

Mordor Intelligence's Medical Coatings Market Size Versus Other Published Estimates

Published market values for medical coatings can look far apart, even when the topic name is the same, because the scope and counting logic often differ. The biggest shifts usually come from whether the estimate is limited to coatings tied to medical devices and implants, how applications are grouped, and how the base year is chosen.

In practice, gaps also come from how pricing is handled across coating chemistries and whether penetration is assumed to rise evenly across devices, which rarely happens. Some estimates also blend adjacent categories like broader medical device coatings without clearly separating implants, tools, and equipment, and currency timing and refresh cadence can further widen the spread. For this reason, the 2026 value is anchored to a defined device-and-implant demand pool and then verified through coating-type adoption checks, a modeling choice used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.47 B (2026) | |

| Global Consultancy A | USD 10.40 B (2024) | This figure is presented as a medical device coating total for 2024, which can undercount implant-heavy and tool-specific coating demand when applications are grouped broadly, and it is not aligned to the 2026 base year used in this study. |

| Regional Consultancy B | USD 8.25 B (2024) | The estimate uses a 2024 starting point and appears to rely on a wider device classification lens, with limited clarity on coating-type penetration and pricing by chemistry, which can push totals down when higher-value functional coatings are not weighted by application mix. |

Looking across the three figures, the main difference comes from year alignment and what gets counted as medical coating value. When the same demand pool is built from procedures and device categories, and then pricing and penetration are checked by coating function and chemistry, the market size becomes easier to trace and repeat from one refresh to the next.

Key Questions Answered in the Report

What is driving the strong CAGR in the medical coatings market?

Continuous demand for infection-preventive surfaces, growth in minimally invasive procedures and investment in smart implants lift the market to a 6.83% CAGR through 2031.

Which chemistry holds the largest medical coatings market share?

Parylene coatings led with 29.10% revenue in 2025 owing to their barrier strength and biocompatibility.

How big is the medical coatings market size for implants?

Implant applications contributed 30.85% of total 2025 revenue within the medical coatings market size.

Why are hydrophilic coatings growing fastest?

They reduce friction in catheters and guidewires, supporting procedural efficiency in expanding minimally invasive surgeries and explaining their 7.74% CAGR.

Which region is the fastest growing?

Asia Pacific is advancing at an 8.78% CAGR as China, India and ASEAN nations expand healthcare infrastructure and local device manufacturing.

How does regulatory scrutiny affect competition?

The FTC’s 2025 action against a hydrophilic-coating merger shows regulators will block deals that threaten market balance, influencing consolidation strategies among suppliers.

Page last updated on: