Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

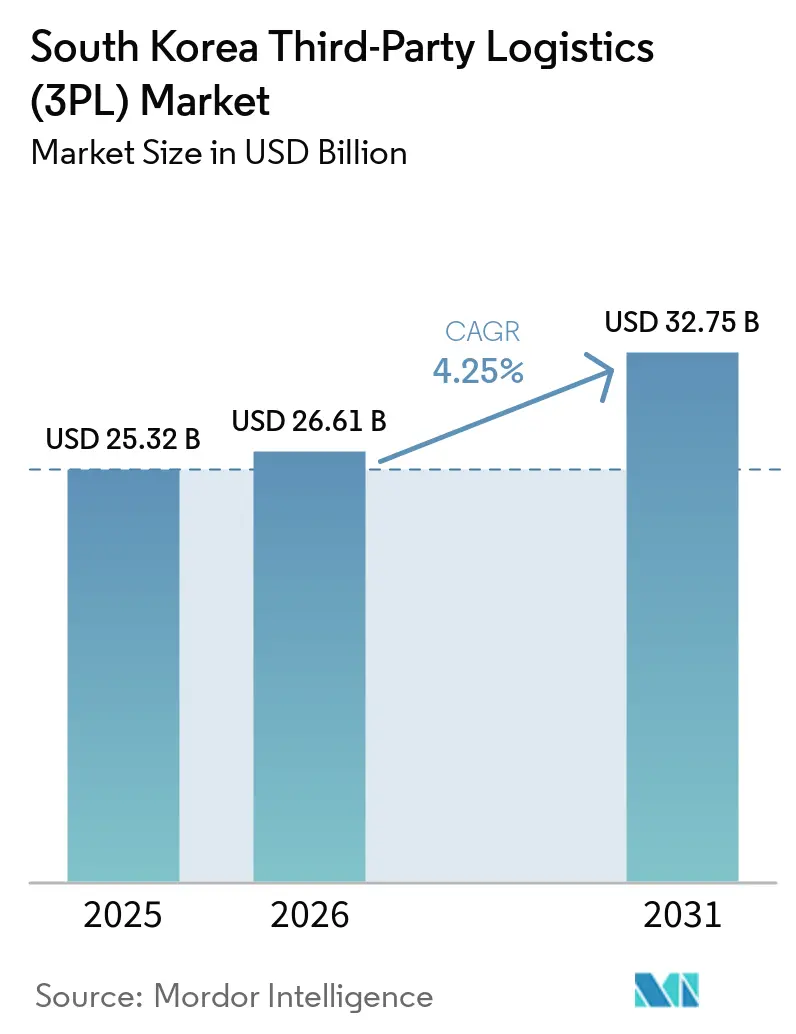

| Base Year Market Size (2025) | USD 25.32 Billion |

| Market Size (2026) | USD 26.61 Billion |

| Market Size (2031) | USD 32.75 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

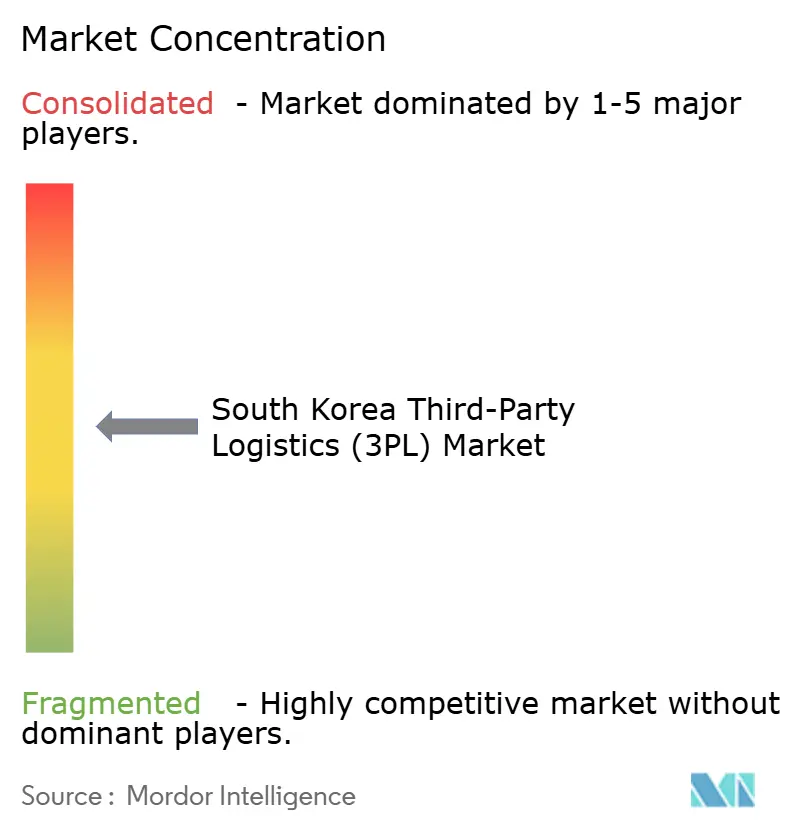

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The South Korea third-party logistics (3PL) market size is estimated to be USD 25.32 billion in 2025, and USD 26.61 billion in 2026, and projected to reach USD 32.75 billion by 2031, growing at a CAGR of 4.25% from 2026 to 2031.

Near-term growth decelerates versus pre-pandemic trajectories because freight-rate turbulence compresses margins, yet the South Korea third-party logistics (3PL) market continues to attract capital for cold-chain biologics corridors, underground automated delivery tunnels, and hydrogen-powered truck fleets that reset competitive benchmarks. National carbon-neutrality incentives accelerate fleet electrification, while AI-orchestrated transportation-management systems (TMS) and warehouse robots mitigate labor shortages and unlock real-time visibility. Retail returns and omnichannel fulfillment cultivate demand for value-added warehousing, and cross-border live-commerce parcel flows from China and Japan add new revenue pools beyond traditional domestic contracts. Regulatory tailwinds such as the Framework Act on AI and cold-chain certification schemes position technology-enabled providers to capture share in the South Korea third-party logistics (3PL) market over the forecast horizon.

Key Report Takeaways

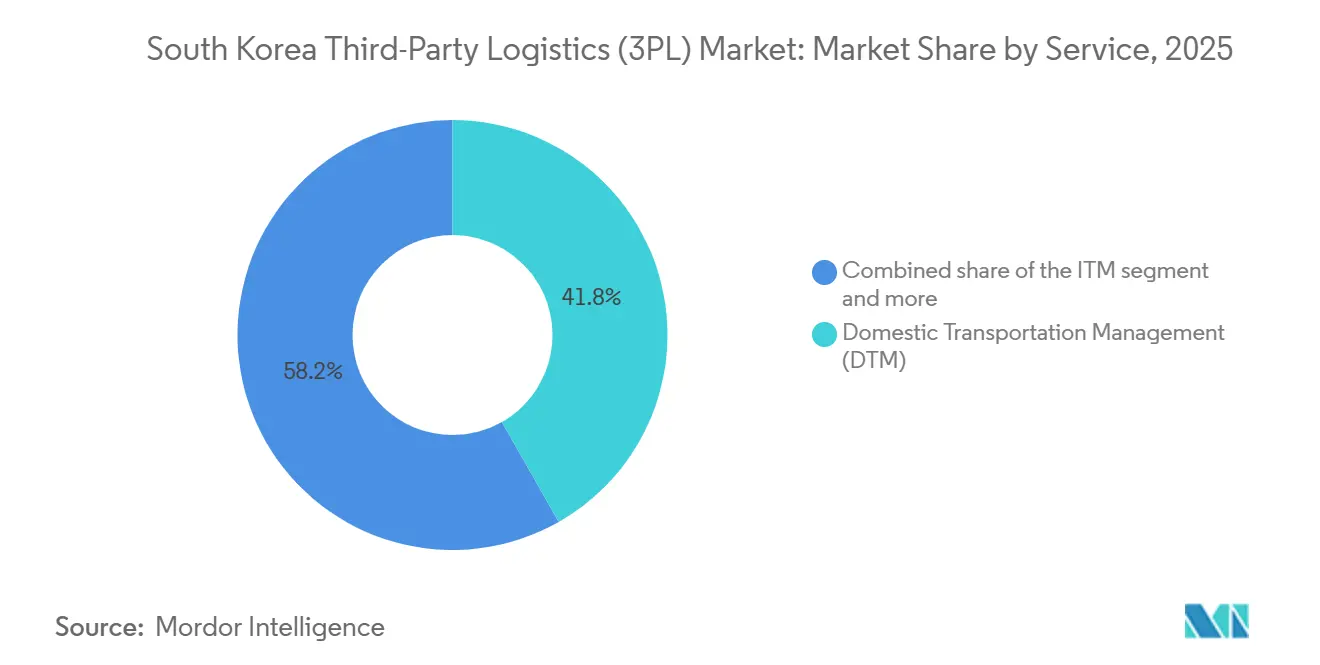

- By service, domestic transportation management led with 41.78% of the South Korea third-party logistics (3PL) market share in 2025, while value-added warehousing & distribution is advancing at a 6.50% CAGR through 2031.

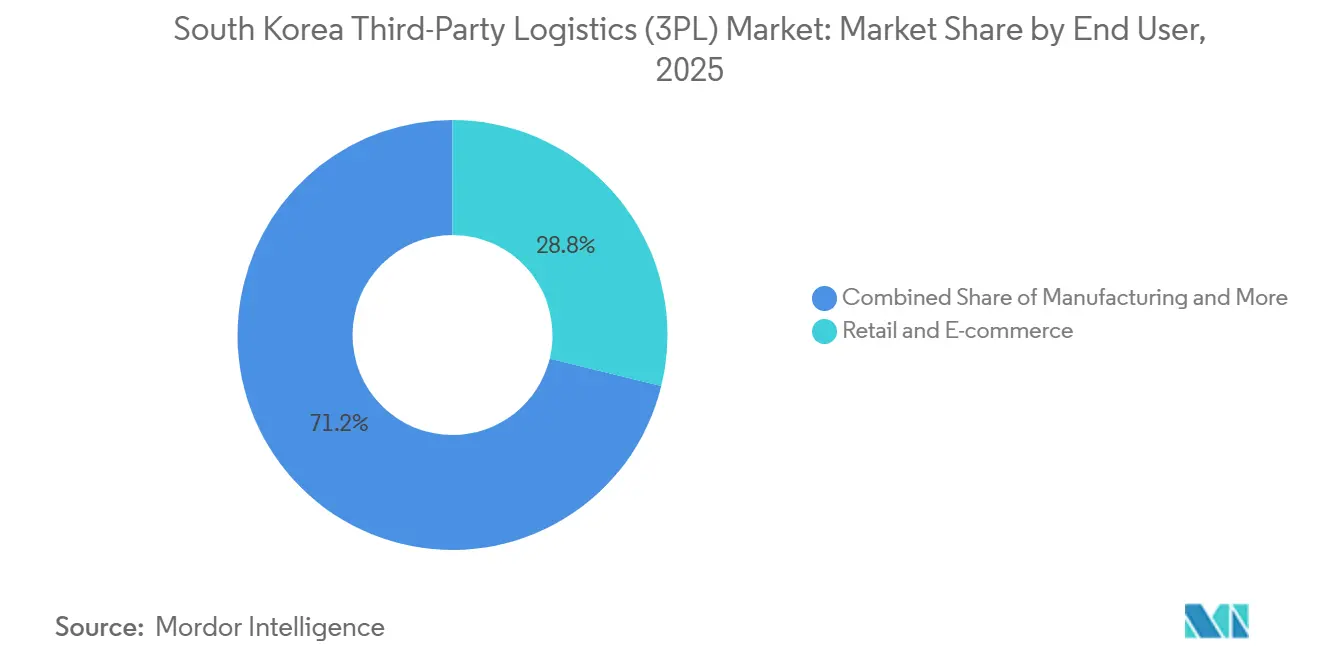

- By end user, life sciences & healthcare accounted for an 7.23% CAGR, the fastest among all sectors, whereas retail & e-commerce commanded 28.82% of the 2025 demand for the South Korea third-party logistics (3PL) market size.

- By logistics model, asset-light configurations retained 50.34% of the South Korea third-party logistics (3PL) market size in 2025, and hybrid models are projected to expand at a 6.95% CAGR between 2026 and 2031.

- By region, the Seoul Capital Area controlled 28.11% of the South Korea third-party logistics (3PL) market share in 2025, yet Jeju Province is forecast to grow at a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain escalation from biologics & K-food export boom | +0.9% | National; Seoul and Gyeongsang pharma clusters | Medium term (2-4 years) |

| AI-orchestrated TMS and warehouse robotics adoption | +0.8% | Seoul and Chungcheong logistics hubs | Short term (≤ 2 years) |

| Omni-channel retail surge driving reverse-logistics integration | +0.6% | Major metropolitan retail corridors | Short term (≤ 2 years) |

| Tax-credited low-emission truck fleets | +0.5% | Nationwide, early in Seoul & Busan | Long term (≥ 4 years) |

| Underground automated logistics-hub projects | +0.4% | Yongsan CBD pilot | Long term (≥ 4 years) |

| Cross-border live-commerce parcels to China & Japan | +0.3% | Incheon Airport FTZ | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Escalation From Biologics & K-Food Export Boom

Biologics manufacturing expansion and rising K-food shipments require validated cold-chain corridors that command premium pricing but impose rigorous Ministry of Food & Drug Safety (MFDS) compliance on 3PL providers. First-arrival laboratory testing and two-year facility pre-registration create dwell-time risks that only warehouses with temperature-controlled holding capacity can absorb. Hyundai’s battery reverse-logistics network illustrates how hazardous-materials expertise and digital traceability form durable barriers. Converging GDP pharma standards with MFDS food-safety traceability favors operators integrating IATA CEIV Fresh and Pharma certifications. Sustained export growth for kimchi, ginseng, and fresh produce underscores the long-run value of multi-certified cold-chain networks within the South Korea 3PL market.

AI-Orchestrated TMS & Warehouse Robotics Adoption

Artificial-intelligence routing engines and autonomous mobile robots offset Korea’s labor shortages by boosting fulfillment throughput and reducing pick errors. The Korean AI market is catalyzed by the 2024 Framework Act on AI that clarifies governance over high-impact systems. WeLaser’s customs-automation suite demonstrates 85% faster document handling and 99% HS-code accuracy, shrinking clearance times and detention fees. Government allocations of more than USD 2.24 billion to raise domestic robot-part localization to 80% by 2030 improve supply security. Digital tachographs on hydrogen trucks synchronize fuel-efficiency data with TMS dashboards, aligning fleet operations with carbon-neutrality mandates within the South Korea 3PL market[1]Republic of Korea Ministry of Environment, “Net-Zero Government Initiative Roadmap,” sustainability.gov.

Omni-Channel Retail Surge Driving Reverse-Logistics Integration

Buy-online-return-in-store models push retailers to embed seamless returns, refurbishment, and circular-packaging flows. February 2024 micro-fulfillment regulations open 500 m² facilities inside neighborhood zones but impose 200-meter school setbacks, forcing distributed depot strategies that raise network complexity. ITF research shows cargo bikes cut parking time 60%, yet small payloads require more depots, inflating real-estate costs. Foldable, reusable packaging introduced by Hyundai reduces cubic utilization, supporting ESG claims but demanding specialized cleaning loops.

Tax-Credited Low-Emission Truck Fleets Under Digital Carbon Neutrality Plan

Public-sector procurement standards exclude hybrids from environmentally friendly vehicle lists, accelerating the transition to battery-electric and hydrogen trucks. Tax credits and accelerated depreciation narrow total-cost-of-ownership gaps. Hyundai targets deployment of 10,000 hydrogen trucks by 2030, integrating fleet telematics for real-time emissions reporting that shippers now require in RFPs. Infrastructure gaps outside metros slow adoption, but mandatory Scope 3 disclosures for automotive exporters embed compliance premiums in the South Korea third-party logistics (3PL) market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Freight-rate volatility compressing margins | -0.7% | National; EU & US lanes | Short term (≤ 2 years) |

| EU CBAM compliance paperwork | -0.5% | Export-oriented industrial sectors | Medium term (2-4 years) |

| Regulatory lag for Li-ion battery warehousing | -0.3% | Seoul and Gyeongsang battery belts | Medium term (2-4 years) |

| Urban quiet-hours curfews | -0.2% | Seoul metro residential areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Freight-Rate Volatility Compressing 3PL Contract Margins

Freight rate volatility put significant pressure on South Korea’s 3PL sector, especially asset-light providers. A sharp rise in Europe–South Korea rates due to Red Sea rerouting quickly turned fixed-price contracts signed at low levels unprofitable, squeezing margins. While some routes like Korea–China saw short-term declines, overall rates remained elevated year-over-year, prolonging cost pressures and highlighting the need for stronger pricing flexibility and risk management.

EU CBAM Compliance Paperwork Adding Cost to Export Logistics

New requirements for embedded-carbon reporting in exports like steel, cement, and aluminum are increasing administrative burdens, particularly around data collection and emissions tracking. Large shippers are pushing these responsibilities onto logistics partners, requiring detailed Scope 3 reporting and certificate management. This creates additional cost and complexity for 3PL providers, with smaller forwarders especially struggling to keep up with system and compliance demands ultimately accelerating market consolidation[2]Yonhap News Agency, “Container Shipping Costs on EU-S. Korea Route Surge,” yna.co.kr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Fulfillment Complexity Commands Premium Growth

Value-added warehousing & distribution is projected to expand at 6.50% CAGR, outpacing the 41.78% dominance of domestic transportation management in the South Korea third-party logistics (3PL) market size in 2025. Smart-center certification standards, especially around cold-chain integrity and automation, favor firms with advanced, tech-enabled facilities, giving players with automated logistics hubs a competitive edge. At the same time, international transportation management continues to benefit from cross-border e-commerce growth. However, sharp freight rate increases on key routes have weighed on profitability, significantly compressing margins on certain lanes.

Domestic road, rail, air, and coastal shipping show divergent prospects. Coastal lanes gain share as reusable foldable containers reduce cubic waste, while rail profits from state investment to cut expressway congestion. Air cargo captures high-value biologics and semiconductors; Gadeok's new airport, set for 2029, will unlock additional capacity valued at KRW 29 trillion (USD 22 billion) economic impact. Ports face congestion risk yet remain pivotal as Busan moves 20 million TEUs annually[3]Ministry of Land, Infrastructure and Transport, “Meatbox Global Obtains Smart Logistics Center Certification,” venturesquare.net.

By End User: Pharmaceutical Complexity Drives Premium Expansion

Life sciences & healthcare posts a 7.23% CAGR, fueled by biologics clusters needing validated GDP corridors and IATA CEIV Pharma gateways at Incheon. Retail & e-commerce retains 28.82% of South Korea third-party logistics (3PL) market share in 2025 but confronts saturation, pushing providers to diversify into cross-border flows that sustain the South Korea 3PL market. MFDS mandates two-year foreign-facility registration and 10-15-day laboratory holds, enlarging compliance workloads that favor seasoned 3PLs.

Automotive logistics rises as 4.5 million zero-emission vehicles are targeted by 2030, necessitating battery production feeds and reverse-logistics pipelines. Technology & Electronics volumes hinge on semiconductor exports but face CBAM paperwork on shipments to Europe. Consumer goods seek margin rescue through ESG-audited transport, while Food & Beverages lean on cold-chain integrity for chilled labeling rules.

By Logistics Model: Technology Integration Favors Hybrid Configurations

Asset-light setups held 50.34% of the South Korea third-party logistics (3PL) market size in 2025, yet demanding ESG audits and integrated tech stacks accelerate hybrid adoption at 6.95% CAGR. Hyundai Glovis will channel 36% of a KRW 9 trillion (USD 7 billion) spend into smart-logistics infrastructure and battery recycling, illustrating capital rotation toward proprietary assets that still retain flexibility.

Framework Act on AI compliance divides providers into those with certified data-governance systems and laggards. WeLaser partnerships let asset-light firms access automated customs without capex, while hybrid players invest directly in robotics and hydrogen fleets for Scope 3 cuts. Fully asset-heavy models grow slowest but secure sticky contracts in hazardous-goods and deep-freeze operations across the South Korea third-party logistics (3PL) market.

Geography Analysis

Jeju Province is projected to post the fastest regional CAGR at 6.15% through 2031 thanks to smart-logistics testbed status and maritime proximity that attracts transshipment pilots. Lower congestion and land cost ease development of micro-fulfillment nodes and hydrogen refueling corridors.

The Seoul Capital Area commanded 28.11% of 2025 revenue in the South Korea third-party logistics (3PL) market, buoyed by corporate concentration and consumer density. Yet land scarcity inflates warehouse rents and quiet-hours curfews fragment delivery windows. Yongsan Smart Core’s KRW 841.2 billion (USD 610 million) underground tunnel blueprint aims to relieve surface congestion and enable automated parcel drops by 2028[4]The Korea Times, “New Gadeok Airport to Open in 2029,” koreatimes.co.kr.

Gyeongsang relies on automotive and shipbuilding freight, with Busan Port handling 76% of national containers. Hyundai Glovis’s 95,000 m² New Port complex, operational by 2027, will streamline EV-battery flows and cold cargo. Chungcheong’s central location and lower real-estate costs lure bulk distribution centers, while Jeolla’s cold-chain upgrades at Gwangyang port capture Chinese and ASEAN traffic. Gangwon’s KRW 279.1 billion (USD 210 million) Geodu expansion eases industrial-site shortages, nurturing emergent logistics hubs.

Competitive Landscape

Competition is moderate as domestic giants deepen vertical integration and foreign majors target premium niches. Hyundai Glovis plans to grow its pure car and truck carrier fleet from 85 to 128 vessels and pursue M&A to pivot from carrier to total-logistics services. Hanjin Logistics’ partnership with DHL marries a global network with deep domestic reach to win pharma and semiconductor contracts.

Certification emerges as a moat. Incheon’s multi-party CEIV cluster boosts pharma cargo value to USD 17.3 billion, raising entry barriers for uncertified firms. Hybrid and AI-compliant operators gain by offering carbon-accounting dashboards that simplify CBAM filings for exporters. Meanwhile, investment funds back capacity expansions: BGF Retail’s KRW 220 billion (USD 170 million) Busan facility will open in 2026 to support convenience-store exports.

Asset-light startups pivot toward digital customs and city-hub robots, often licensing tech to incumbents chasing efficiency. Overall, the South Korea 3PL market tilts toward providers that bundle infrastructure control with data-rich platforms.

South Korea Third-Party Logistics (3PL) Industry Leaders

CJ Logistics Corporation

Hyundai Glovis Co. Ltd.

LX Pantos (LG Group)

Samsung SDS (Cello Square)

Lotte Global Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LX Pantos acquired a large logistics center in Katowice, Poland, to strengthen its European footprint and serve as an intermodal logistics node. This intermodal hub connects road, rail, and air networks, offering seamless supply chain visibility for South Korean manufacturers across Europe.

- November 2025: LX Pantos agreed with Sinotrans to form a joint venture, targeting sea-air intermodal growth in Northeast Asia (LX Pantos 60% / Sinotrans 40%).

- October 2025: CJ Logistics signed a financial partnership with Hyundai Commercial to offer dedicated finance products for logistics vehicle owners and Urban platform users.

- July 2025: Hyundai Glovis and Avikus (HD Hyundai) planned retrofitting of autonomous navigation systems on car carriers, aiming toward AI assisted ship navigation.

South Korea Third-Party Logistics (3PL) Market Report Scope

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

By Region (South Korea)

| Seoul Capital Area |

| Chungcheong Region |

| Gyeongsang Region |

| Jeolla Region |

| Gangwon Province |

| Jeju Province |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

| By Region (South Korea) | Seoul Capital Area | |

| Chungcheong Region | ||

| Gyeongsang Region | ||

| Jeolla Region | ||

| Gangwon Province | ||

| Jeju Province | ||

Key Questions Answered in the Report

How large is the South Korea third-party logistics (3PL) market today?

The South Korea third-party logistics (3PL) market size reached USD 26.61 billion in 2026 and is forecast to climb to USD 32.75 billion by 2031.

Which service segment is growing the fastest?

Value-Added Warehousing & Distribution is expanding at a 6.50% CAGR as shippers seek integrated fulfillment and cold-chain capabilities.

Why is Life Sciences & Healthcare an attractive customer base?

Stringent MFDS and IATA CEIV requirements give certified 3PL providers pricing power, pushing the sector to a 7.23% CAGR through 2031.

What role do hydrogen trucks play in Korean logistics?

Government tax credits and Hyundai’s plan for 10,000 hydrogen trucks by 2030 position zero-emission fleets as a cornerstone of future freight decarbonization.

How will EU CBAM affect Korean exporters?

New carbon-intensity filings raise administrative workloads, favoring 3PLs that offer embedded carbon-accounting platforms to simplify compliance.

What technology investments are Korean 3PL providers prioritizing through 2031?

Investors are pouring capital into AI-driven transportation management systems, autonomous mobile robots for warehouse automation, and digital twin platforms. These platforms connect underground delivery tunnels with real-time routing dashboards, all with the goal of enhancing speed, visibility, and the precision of carbon tracking.

Page last updated on: